What Is the Annual Maintenance Process for a Gold IRA?

The annual maintenance process for a Gold IRA comes down to three core requirements: recurring fees, IRS reporting, and — for traditional account holders over age 73 — Required Minimum Distributions.

Most of the administrative work runs through your custodian automatically. They calculate your account’s Fair Market Value using December 31 spot prices, file Form 5498 with the IRS by May 31, and issue a year-end statement each January. If you hold a traditional Gold IRA and have reached age 73, they’ll also calculate your RMD obligation for the year.

What falls directly on you is smaller than most people expect. You’ll need to confirm your annual fees are paid — typically $200 to $300 combined for custodial administration and secure storage — decide whether to make an annual contribution, and plan for any Required Minimum Distribution if you’re in that window. Owners who hold a No Fee Precious Metals IRA through Brighton Gold on qualified purchases don’t pay custodial or storage fees for the lifetime of the account, which simplifies the fee side of the process considerably.

The 2026 contribution limit is $7,500 for most IRA holders, and $8,600 for owners age 50 and older. The age-73 threshold for Required Minimum Distributions applies to traditional accounts — Roth Gold IRAs are not subject to RMDs during the owner’s lifetime.

This guide walks through each component of the annual cycle: what happens when, who handles it, what it costs, and what to watch for. The process is more routine than it looks from the outside.

- What Annual Gold IRA Maintenance Actually Involves

- The Annual Gold IRA Compliance Calendar

- Understanding Annual Fees: What You Pay and Why It Matters

- IRS Reporting Requirements: The Forms Every Owner Should Know

- What Your Custodian Handles vs. What Falls on You

- Frequently Asked Questions About Gold IRA Annual Maintenance

- How much are standard annual maintenance fees for a Gold IRA?

- Do I need to get my gold appraised every year for IRS purposes?

- What happens if I miss the RMD deadline for my Gold IRA?

- Can I pay my Gold IRA annual fees from a personal checking account?

- What IRS forms will I receive each year as a Gold IRA owner?

- How does the 2026 contribution limit increase affect my annual maintenance plan?

- What metals can I hold in a Gold IRA, and does that change during annual maintenance?

- The Annual Process Isn’t the Obstacle — Clarity Is

What Annual Gold IRA Maintenance Actually Involves

The precious metals industry has a way of making annual maintenance sound like a compliance obstacle course — layered deadlines, IRS paperwork, valuation schedules, and custodial requirements that seem to multiply every time you ask a question.

That framing isn’t accidental.

What annual maintenance actually involves is three recurring requirements, a predictable calendar, and a custodian who handles most of the IRS-facing work automatically. The parts that fall on you each year are fewer than the industry typically suggests — and more manageable once someone explains them without an agenda attached.

If you’re exploring a Precious Metals IRA and want to understand what year-over-year ownership involves before you commit, this is the right place to start. For the full cost picture — setup through long-term holding — understanding gold IRA fee structures is worth reading alongside this guide. And if questions about account compliance or risk have come up in your research already, identifying safe gold IRA practices addresses those directly.

The Three Requirements That Drive Every Year

Every Gold IRA owner faces the same three annual requirements — regardless of how much gold they hold, which custodian they use, or how long they’ve owned the account:

- Fees — Custodial administration and secure storage fees are due each year. Most owners with flat fee arrangements pay between $200 and $300 combined. The structure of those fees — flat versus percentage-based — matters more over time than the opening number suggests. We cover this in detail below.

- IRS Reporting — Your custodian files Form 5498 with the IRS each May, reporting your account’s Fair Market Value as of December 31. You receive a copy. The only action required on your end is confirming the number is accurate.

- RMD Compliance — Traditional Gold IRA holders who have reached age 73 are required to take a Required Minimum Distribution each calendar year. Your custodian calculates the amount. You decide how to satisfy it. This is the one piece of annual maintenance that genuinely requires advance planning.

That’s the complete list. Annual maintenance does not require a physical inspection of your metals, a visit to the depository, or an independent appraisal. Your custodian’s FMV calculation — based on December 31 spot prices — is what the IRS requires. Nothing more.

Why the Industry Treats Maintenance Like a Mystery

There’s a method worth naming directly — using the annual maintenance process as a retention tool.

Some firms present the compliance cycle as something only they can navigate on your behalf. A web of IRS requirements. Custodian deadlines. Documentation standards so involved that stepping away from their guidance puts your account at risk. The language is technical. The timelines are made to feel precarious. The message underneath the jargon is clear enough: don’t try to understand this without us.

That’s not education. It’s dependency engineering.

What’s actually true is that the IRS requirements for a Gold IRA are standardized, publicly documented, and identical for every self-directed IRA. Form 5498 reporting. RMD calculation rules. Contribution deadlines. All of it is spelled out in IRS Publication 590-A and IRS Publication 590-B. Your custodian follows established protocols — not proprietary ones. Nothing about the annual process requires firm-specific expertise to understand.

We believe plain language earns more trust than complexity. That’s not a positioning statement — it’s how we approach every customer relationship. When owners understand what their account actually requires each year, they ask sharper questions, catch discrepancies earlier, and stay in the relationship because it’s working — not because leaving feels risky.

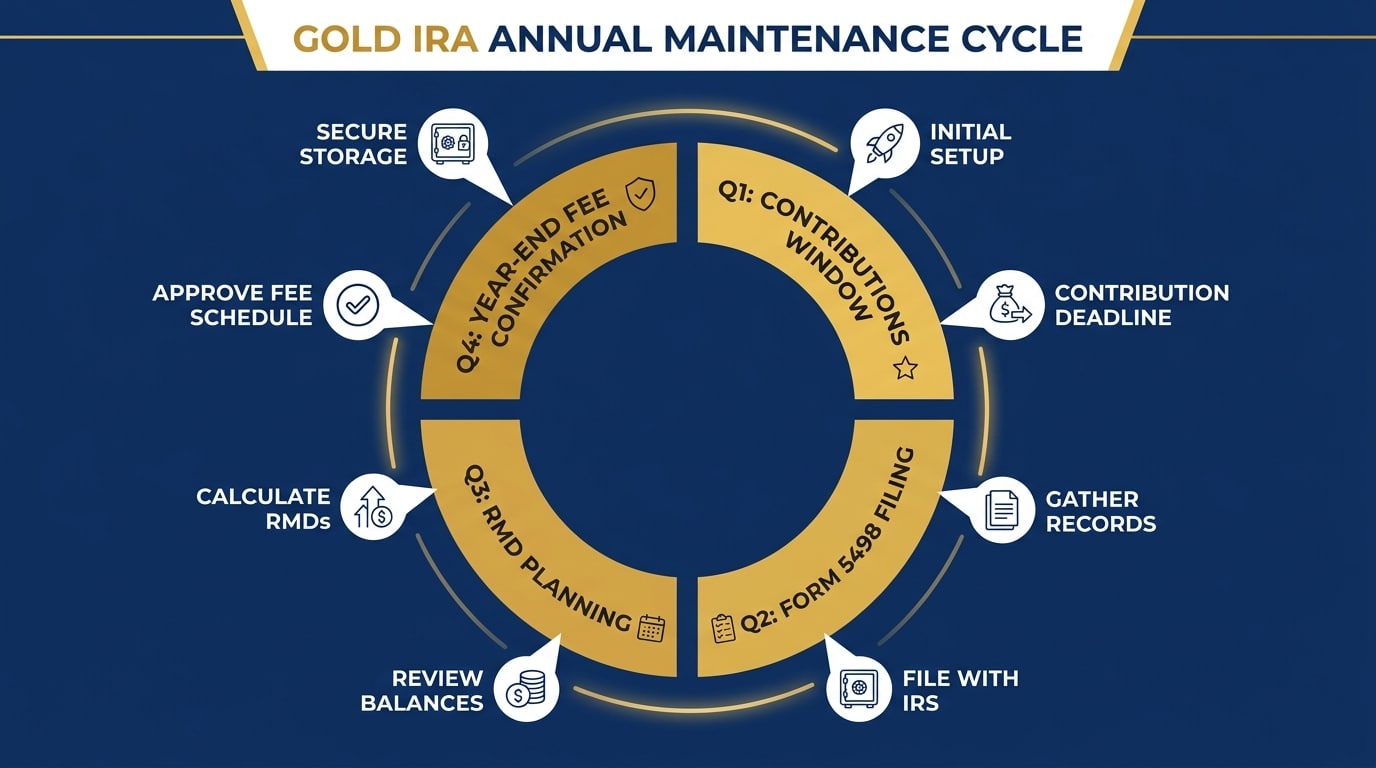

The Annual Gold IRA Compliance Calendar

The maintenance cycle runs the same way every year. Same forms. Same deadlines. Same sequence of custodian actions and owner decisions.

What varies is whether you know what’s coming — and whether your custodian is communicating it without you having to ask. The calendar below maps every key event across a full year of Gold IRA ownership. Most of these don’t require anything from you directly. But knowing when they happen gives you the kind of oversight your account deserves.

January Through April: Statements, Contributions, and First-Year RMD Window

The year opens with paperwork your custodian initiates.

- January — Year-End Statement — Your custodian issues your annual account statement showing the December 31 Fair Market Value of your holdings. This is the baseline for the year ahead — and the number your RMD calculation, if applicable, is built from.

- January / April 1 — First RMD Window (Year-73 Only) — If you turned 73 during the prior year, this is your first year of RMD eligibility. The IRS allows your first required distribution to be deferred to April 1 of the following year. After that first distribution, every subsequent RMD is due by December 31. One note: deferring to April means you’ll take two distributions in the same calendar year — which carries tax return implications. Consult your CPA or tax professional.

- April 15 — Annual Contribution Deadline — Contributions for the tax year must be in the account by the filing deadline. The 2026 limit is $7,500 for most owners, and $8,600 for those age 50 and older.

- April — Prior-Year Tax Return — If your custodian issued a Form 1099-R for any distribution taken during the prior year, that distribution amount is reported on your return. Consult a licensed CPA or tax professional for specifics on how distributions affect your broader tax picture.

May Through September: Form 5498 and Mid-Year Review

- May 31 — Form 5498 Filed — Your custodian files Form 5498 with the IRS and sends you a copy. This form reports your account’s December 31 Fair Market Value and any contributions made during the year. Review it when it arrives. If the FMV doesn’t align with what you’d expect based on December 31 spot prices, contact your custodian.

- June Through September — Mid-Year Review Window — No mandatory deadlines fall in this window. But it’s a reasonable time to confirm your fee payment method for year-end, review your account’s metals composition, and begin thinking through RMD logistics if you’re approaching or already in the distribution window.

October Through December: RMD Execution and Year-End Fees

- October–November — RMD Planning Window — If you’re subject to RMDs, this is when to confirm your distribution method and coordinate the logistics with your custodian. Don’t wait until December. Your custodian calculates the required amount; you determine how to satisfy it. For a full breakdown of each distribution approach, understanding gold IRA distribution options covers the mechanics.

- December 31 — RMD Deadline — Your Required Minimum Distribution must be fully satisfied by December 31 every year after your first. Missing this deadline triggers a 25% excise tax on the undistributed amount — reduced to 10% if corrected in a timely manner per IRS guidelines.

- December — Annual Fee Confirmation — Confirm that custodial and storage fees are paid for the year. Fees can be paid from the IRA directly or from a personal checking account. Paying from outside the account keeps more of your metals inside it — worth asking your custodian about if you haven’t already.

| Month | Event | Who Acts | Owner Action |

|---|---|---|---|

| January | Year-end statement issued | Custodian | Review FMV for accuracy |

| January / April 1 | First-year RMD window (age 73 only) | Owner | Take distribution if first RMD year |

| April 15 | Annual contribution deadline | Owner | Fund account up to limit |

| May 31 | Form 5498 filed | Custodian | Verify FMV; confirm contributions |

| October–November | RMD planning window | Owner + Custodian | Confirm amount and distribution method |

| December 31 | Annual RMD deadline | Owner | Complete distribution |

| December | Annual fee payment | Owner or Custodian | Confirm payment method and amount |

Understanding Annual Fees: What You Pay and Why It Matters

Most owners know they’ll pay annual fees. What fewer examine closely enough — until the numbers compound against them — is how fee structure affects what they actually keep over a 10- or 20-year holding period.

Annual Gold IRA fees fall into two categories: custodial administration and secure storage. Combined, the cost typically runs $200 to $300 per year when fees are flat. But not all fee structures are flat — and that distinction is worth understanding before the account is opened, not a decade into ownership.

What Standard Annual Fees Actually Cover

- Custodial Administration Fee — This covers account maintenance, transaction processing, IRS reporting coordination, and compliance documentation. Flat fees for custodial administration typically run $75 to $150 annually.

- Storage Fee — Your approved depository charges this to hold your physical metals in a secure, IRS-compliant vault. Segregated storage — where your metals are held separately from other customers’ holdings — typically costs more than commingled arrangements. Flat storage fees generally range from $100 to $200 per year depending on the facility and storage type.

- Transaction Fees — Some custodians charge a fee on each purchase or exchange within the account. Others don’t. If you plan to add metals over time, this structure matters alongside the annual figures.

For a detailed look at how depository arrangements are priced, what segregated storage means for your physical holdings in practice, and what to evaluate when comparing custodian relationships, understanding gold IRA storage rules covers each component.

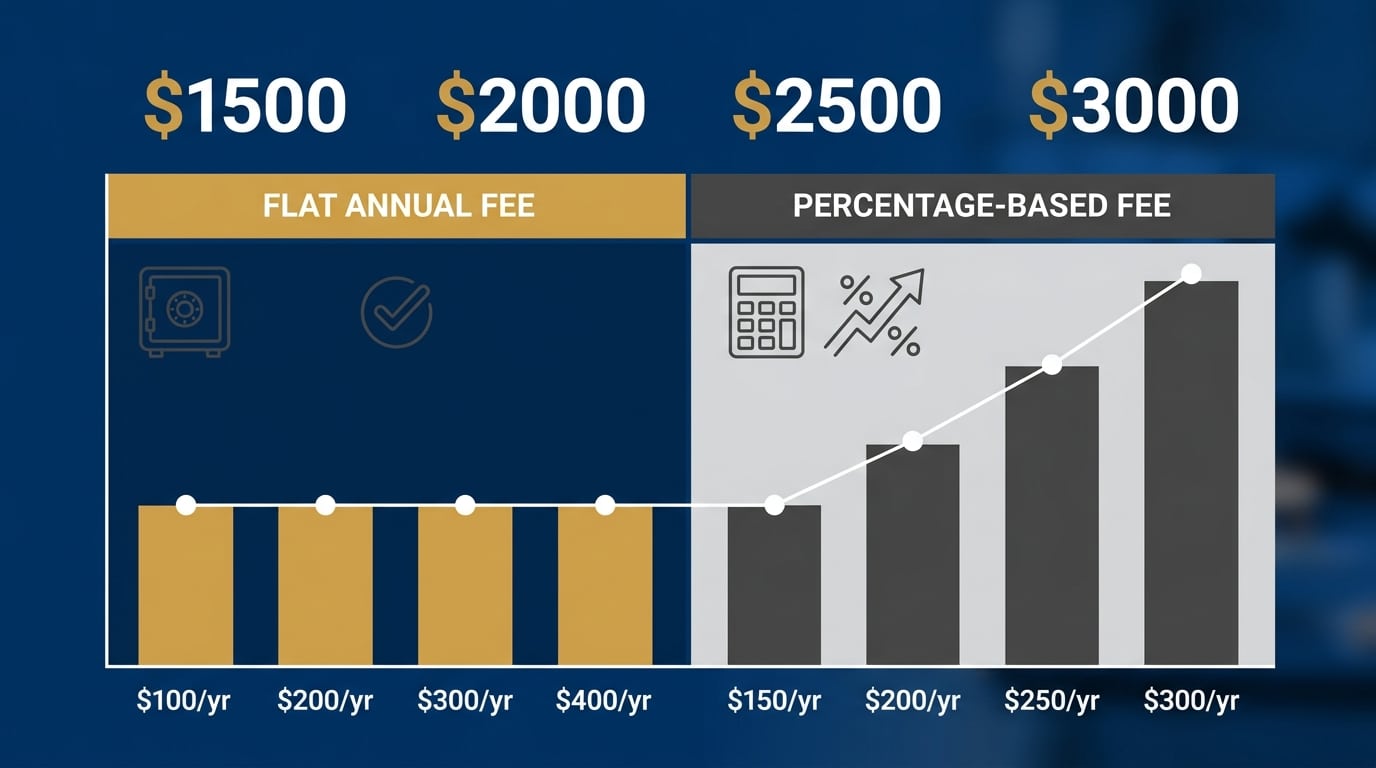

The Percentage Fee Problem

Here’s where the fee structure conversation becomes critical — especially for owners planning to hold for the long haul.

Some custodians price storage as a percentage of account value rather than a fixed annual amount. Starting at 0.5% to 1%, the number doesn’t sound alarming. But gold prices move. And when they do, a percentage-based fee grows alongside your account — not because the cost of storing your metals has changed, but because the price of gold has.

Consider what the difference looks like over time:

| Gold Price per Oz | Account Value (50 oz) | 0.5% Annual Storage Fee | $150 Flat Annual Storage Fee |

|---|---|---|---|

| $2,500 | $125,000 | $625 | $150 |

| $3,500 | $175,000 | $875 | $150 |

| $4,000 | $200,000 | $1,000 | $150 |

| $5,000 | $250,000 | $1,250 | $150 |

The flat fee holds. The percentage fee grows. Same metals. Same storage arrangement. A widening gap.

Precious metals may appreciate, depreciate, or remain unchanged — but your fee structure determines how much of that price growth you actually keep. Over a 10- to 20-year horizon, the difference is substantial.

Brighton Gold’s No Fee Precious Metals IRA eliminates custodial and storage fees on qualified purchases for the lifetime of the account. That’s a structural commitment — not a promotional offer — and it changes the long-term math considerably. We believe it’s the most owner-favorable fee structure in the industry. Most competitors can’t or won’t replicate it.

IRS Reporting Requirements: The Forms Every Owner Should Know

Gold IRA ownership doesn’t create new IRS filing obligations for you personally. Your custodian handles the annual reporting. What matters is understanding which forms they file, what those forms contain, and what to do if something doesn’t look right.

Form 5498: The Annual Fair Market Value Report

Form 5498 is the primary annual document for Gold IRA owners. Your custodian files it with the IRS each May and sends you a copy for your records.

Form 5498 reports:

- Your account’s Fair Market Value as of December 31 of the prior year

- Any contributions made to the account during the year

- Any rollover amounts received

- Whether you’re required to take an RMD in the upcoming year

The FMV is based on December 31 spot prices — not appraised value, not insurance value, not what you originally paid. It’s the market price of your metals on that specific date.

When the form arrives, review the FMV figure. Compare it to what you’d expect based on December 31 spot prices and your holdings. If the number looks off — contact your custodian right away. This figure drives your RMD calculation for the year. An error here carries downstream consequences that don’t fix themselves.

Form 1099-R and RMD Obligations for Owners Over 73

Any time a distribution is taken from your Gold IRA — required or otherwise — your custodian files Form 1099-R and sends you a copy. This form reports the gross distribution amount and any tax withheld.

For traditional Gold IRA holders who have reached age 73, per IRS Publication 590-B, Required Minimum Distributions apply every year. The IRS calculates the required amount using your December 31 FMV divided by a life expectancy factor from the Uniform Lifetime Table. Your custodian provides that calculation. You choose how to satisfy it:

- Cash distribution — Liquidate a portion of your holdings and take the cash proceeds as the distribution

- In-kind distribution — Take physical delivery of metals equal in value to your RMD, verified against U.S. Mint purity standards for IRS-eligible gold

- Combination — Part cash, part metals

In-kind distributions require close coordination with your custodian and depository. The metals must meet the same IRS purity standards they met on day one. For a full breakdown of how physical distributions work from start to finish, how physical distributions from a Gold IRA work covers the mechanics step by step.

A missed RMD deadline carries a 25% excise tax on the undistributed amount — reduced to 10% with timely correction per IRS guidelines. Correction means taking the missed distribution and filing Form 5329. Consult a licensed CPA or tax professional if you’ve missed a deadline or are approaching one without a confirmed plan.

Who This Process Is Not Built For

It’s worth being direct about something before going further.

If you’re evaluating Gold IRAs as a short-term position — something to acquire during a price dip and exit when gold moves — the annual maintenance framework described here isn’t the right frame for what you’re looking at. RMD timelines. Form 5498 reporting cycles. Long-term fee structures. These are built for owners who intend to hold physical metals for years or decades.

Brighton Gold works with customers who want to hold something real, outside the paper financial system, for the long haul.

If the plan is to trade in and out based on price direction, we’re probably not the right fit — and the annual process described here won’t feel relevant to the kind of ownership you’re considering. We’d rather be direct about that now than have the mismatch surface later in the relationship.

| IRS Form | Purpose | Filed By | Deadline | Owner Action |

|---|---|---|---|---|

| Form 5498 | Reports FMV and annual contributions | Custodian | May 31 | Review for accuracy; keep for records |

| Form 1099-R | Reports distributions taken | Custodian | January 31 | Report distribution on tax return |

| Form 5329 | Reports RMD shortfall if deadline missed | Owner | With tax return | File with excise tax if applicable |

What Your Custodian Handles vs. What Falls on You

A lot of uncertainty about Gold IRA maintenance comes from not knowing who owns which responsibilities. Once that division is clear, the whole process feels different.

Your custodian manages the IRS-facing work. You manage a short list of annual decisions. Between the two, the account stays in good standing — and neither side is carrying more than their role requires.

What the Custodian Manages Each Year

Your custodian handles everything that touches the IRS directly:

- Calculating your account’s Fair Market Value using December 31 spot prices

- Filing Form 5498 with the IRS and sending you a copy by May 31

- Calculating your RMD amount if you’re in the distribution phase (traditional accounts, age 73+)

- Filing Form 1099-R for any distributions taken during the year

- Coordinating with your approved depository on storage, segregation, and annual audit confirmation

- Maintaining transaction records and making them available on request

Depositories operate on a separate layer. Facilities like Delaware Depository conduct independent audits of stored metals annually — confirming your holdings are present, properly catalogued, and meeting IRS purity requirements. That happens without any involvement from you.

What Falls Directly on the Account Owner

Your responsibilities are limited — but they’re yours to own:

- Pay annual fees — Confirm that custodial and storage fees are paid before year-end. Whether you’re paying from the IRA or from a personal checking account, confirm the timing with your custodian ahead of December 31.

- Make your contribution decision — Decide whether you’re contributing this year and get the funds in by April 15. The 2026 limit is $7,500 base, $8,600 for owners age 50 and older.

- Review Form 5498 — Verify the Fair Market Value and contribution figures when the form arrives. Contact your custodian immediately if something looks off.

- Execute your RMD — If you hold a traditional account and are 73 or older, the distribution must be satisfied by December 31. Your custodian calculates the amount. You initiate it. That deadline is yours.

- Consult a CPA or tax professional — Brighton Gold does not provide financial, tax, or legal advice. Questions about how your Gold IRA affects your return, how distributions affect your other financial obligations, or how contributions interact with your deductible IRA limit — those belong with a licensed professional.

If you’re still in the setup or transfer phase — or considering moving an existing retirement account into a self-directed IRA — how a Gold IRA transfer works covers the process from existing account to funded precious metals IRA.

For guides covering every stage of ownership — from initial rollover through distributions — Brighton Gold’s Learning Center organizes them by topic.

| Annual Responsibility | Custodian | Owner |

|---|---|---|

| FMV calculation (Dec 31 spot) | ✓ | — |

| Form 5498 filing | ✓ | — |

| Form 1099-R filing | ✓ | — |

| Annual depository audit | ✓ (depository-initiated) | — |

| Form 5498 accuracy review | — | ✓ |

| Annual fee payment | — | ✓ |

| Contribution decision and funding | — | ✓ |

| RMD amount calculation | ✓ (calculates) | — |

| RMD execution and deadline compliance | — | ✓ (initiates) |

| Tax return reporting | — | ✓ |

Frequently Asked Questions About Gold IRA Annual Maintenance

How much are standard annual maintenance fees for a Gold IRA?

Most Gold IRA owners pay between $200 and $300 per year in combined custodial administration and storage fees — when those fees are structured as flat amounts.

The opening number matters less than the structure behind it. A flat $250 annual fee is still $250 in year fifteen — regardless of what gold is trading at. A 0.5% storage fee on a $125,000 account costs $625 annually. On a $250,000 account, that same fee doubles to $1,250. The metals haven’t changed. The storage hasn’t changed. The fee has.

Owners who hold a No Fee Precious Metals IRA through Brighton Gold on qualified purchases don’t pay custodial or storage fees for the lifetime of the account. Over a decade or more of ownership, that structural difference adds up to a number worth examining carefully before you commit to a custodian relationship.

Do I need to get my gold appraised every year for IRS purposes?

No. The IRS does not require an independent appraisal of your physical metals for routine annual reporting.

Your custodian handles Fair Market Value reporting using December 31 spot prices — the market price of gold on that date. That’s the IRS-accepted method for Form 5498 reporting. No third-party appraiser, no depository inspection visit, no separate certification is part of the standard annual process.

Independent valuation can come into play in specific circumstances — estate planning, certain in-kind distributions, charitable contribution scenarios. Your custodian can advise when that applies. For routine annual maintenance, spot-price FMV is the complete answer.

What happens if I miss the RMD deadline for my Gold IRA?

Missing your Required Minimum Distribution deadline by December 31 triggers a 25% excise tax on the amount that should have been distributed but wasn’t.

If the shortfall is corrected in a timely manner per IRS guidelines, that penalty drops to 10%. Correction means taking the missed distribution and filing Form 5329. The relief provision exists — but it’s not a reason to plan loosely.

The October–November window is there for a reason. Use it to confirm your distribution method with your custodian and get the logistics in place well before December 31. Consult your CPA or tax professional if you’re working through a missed RMD or navigating the first-year timing question.

Can I pay my Gold IRA annual fees from a personal checking account?

Yes — and for many owners, it’s the right call.

IRS rules permit custodial and storage fees to be paid from outside the account. When you pay from a personal checking account instead of the IRA itself, your metals stay intact inside the account — nothing needs to be liquidated to cover an operating cost. Over time, that means more physical gold remaining in the account rather than being converted to cover annual expenses.

Confirm with your custodian that external payments are accepted, that the payment is credited to the correct period, and whether there’s a preferred timing window for year-end processing. Most custodians accommodate this without friction.

What IRS forms will I receive each year as a Gold IRA owner?

Most owners receive two forms annually.

Form 5498 — Issued by your custodian by May 31. Reports your account’s December 31 Fair Market Value and any contributions made during the year. You don’t file this with your tax return — keep it for your records and review it for accuracy.

Form 1099-R — Issued if you take any distribution during the year, including Required Minimum Distributions. The gross distribution amount is reported on your tax return. If no distribution was taken, you won’t receive this form.

If a Required Minimum Distribution deadline is missed, Form 5329 also comes into play — that’s the form used to report the shortfall and calculate the applicable excise tax. Consult a CPA or tax professional on anything related to a missed distribution before assuming how the penalty applies to your situation.

How does the 2026 contribution limit increase affect my annual maintenance plan?

The 2026 contribution limit is $7,500 for most IRA holders, and $8,600 for those age 50 and older.

For owners who’ve been contributing below the maximum, the updated limit is worth factoring into your April planning. The window closes at April 15 — contributions after that date don’t apply to the prior tax year regardless of how close you were to the deadline.

The limit change doesn’t affect your RMD calculation, your fee structure, or anything else in the annual maintenance cycle. It’s a contribution decision — one that needs to be made before the deadline, not after.

What metals can I hold in a Gold IRA, and does that change during annual maintenance?

IRS-eligible gold for a self-directed IRA must meet specific purity requirements. Gold bullion must be at least 99.5% pure. Coins must meet IRS eligibility standards — U.S.-minted coins like the Gold American Eagle are IRS-approved and among the most widely held in these accounts. Verifying that current holdings meet purity requirements is part of routine custodian and depository oversight. You don’t manage that independently.

Eligibility questions come up most often when adding to the account. Before any new metals are acquired, confirm IRS compliance with your custodian. The U.S. Mint publishes specifications for every American-made coin. For a breakdown of which coins are most appropriate for long-term IRA ownership, choosing IRS-approved gold coins covers each option in detail.

The Annual Process Isn’t the Obstacle — Clarity Is

Gold IRA maintenance is a repeating calendar. The same requirements, the same forms, the same deadlines — year after year. Once you’ve been through the cycle once, the second year is familiar territory.

What makes the process feel complicated isn’t the process itself. It’s the way some firms present it — as something fragile, intricate, and dependent on their ongoing involvement to avoid costly mistakes. That framing benefits the firm. It doesn’t benefit the owner.

Physical gold and silver exist outside the paper financial system. For the customers who hold them — people who’ve spent decades building something real and want to protect it from the risks that digital accounts and dollar-denominated savings can’t insulate against — the annual maintenance cycle is what keeps that ownership in good standing with the IRS. It should feel manageable. With the right custodian and the right dealer, it does.

Knowing what the process requires is one part of the decision. The other part — whether a Gold IRA fits your specific situation, what the fee structure looks like over your actual holding timeline, and what ownership involves from the first year through the long term — is best answered in a direct conversation.

Brighton Gold offers a complimentary consultation to walk you through your options, including how the No Fee IRA works and whether you qualify. No commitment. No pressure. Just a clear picture of what this actually involves before you make any decisions.

Most customers who go through that conversation leave with a sharper sense of exactly what they’re deciding between. That’s what it’s designed for — and it’s the part of the process no article alone can deliver.