How Does Gold IRA Storage Work? (2026 Depository Guide)

If you’ve been looking into a precious metals IRA, you’ve probably hit the same question everyone asks: where does the gold actually go?

It’s a fair question. You’re putting real money into something you can physically hold—but you don’t get to hold it yourself. That part trips people up.

Here’s the short version: your gold goes to an IRS-approved depository, not your home, not a personal safe, and not a bank vault you rent on your own. The IRS requires that a qualified trustee—a bank or approved non-bank institution—maintain physical possession of any precious metals held inside an IRA. That rule comes directly from IRC Section 408(m)(3).

Break that rule—even with good intentions—and the IRS can treat your entire account as distributed. We’ll get into what that actually looks like later in this guide.

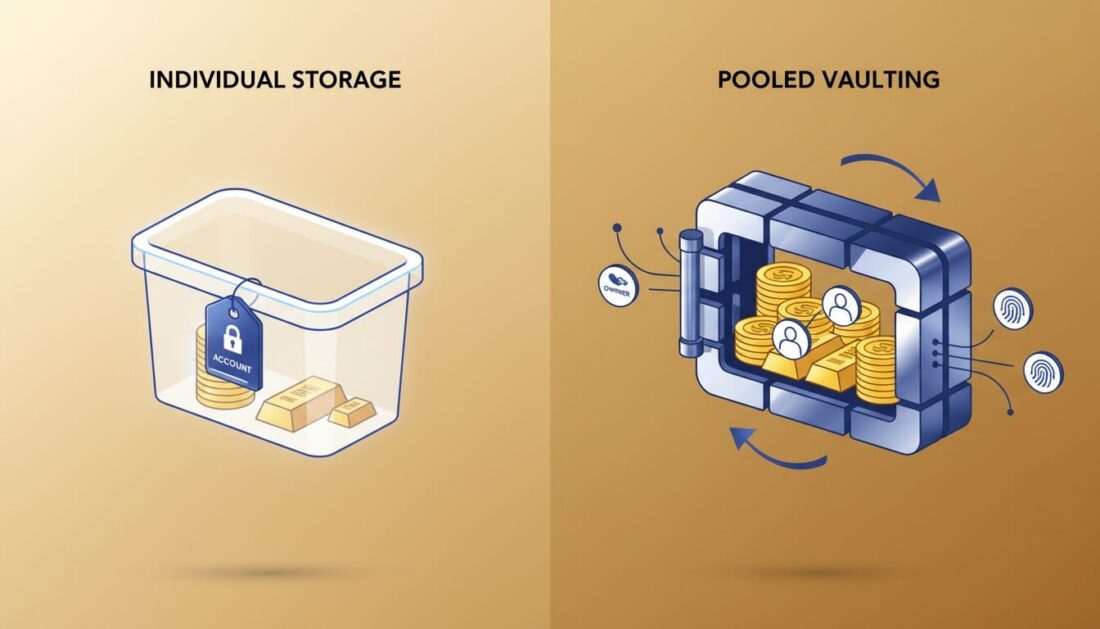

The storage process itself is straightforward. You purchase IRS-approved metals through a dealer. The dealer ships them directly to a depository. Your custodian records the transaction and updates your account. You choose between segregated storage—where your metals sit in their own labeled container—and commingled storage, where they’re pooled with other owners’ metals of the same type.

Both options are held in Class 3 vaults with armed security, biometric access, and all-risk insurance coverage.

What should you know before choosing a depository? What does it cost? And how do you make sure your gold is really there?

That’s what this guide covers. If you’re looking for a broader starting point on identifying safe gold IRA practices, Brighton’s safety guide pairs well with this one. And if you’ve come across confusing claims about storage, our resource on identifying safe gold IRA practices can help sort fact from fiction.

How the Gold IRA Storage Process Works—From Purchase to Vault

Most people assume this part is complicated. It isn’t.

Once you understand the four steps involved, the whole thing makes sense. There are built-in safeguards at every stage—and you don’t have to manage any of them yourself.

Step 1: You Choose Your Metals Through a Dealer

You work with a precious metals dealer—like Brighton—to select IRS-approved products. That includes coins like the Gold American Eagle and Canadian Maple Leaf, along with bullion bars that meet specific purity standards.

For gold, the minimum fineness is .995 (99.5% pure). Silver requires .999. Platinum and palladium need .9995.

The dealer doesn’t send the metals to you. They ship directly to the depository your custodian has on file.

Step 2: The Metals Ship Under Insured, Registered Transport

Once your order is confirmed, the metals move through insured carriers that specialize in secure logistics. Companies like Brink’s Global Services—one of the oldest names in secure transport—handle armored shipping with chain-of-custody tracking from pickup to delivery.

Your metals are fully covered during transit. That includes theft, damage, and loss.

Step 3: The Depository Verifies and Your Custodian Updates Your Account

When the depository receives the shipment, they verify the contents against the purchase order—weight, type, quantity, and serial numbers if applicable.

Your custodian gets notified. Your account gets updated. You should receive a depository receipt confirming exactly what arrived.

Step 4: Your Metals Go Into the Vault

Now your gold is placed into one of two storage arrangements:

- Segregated storage — Your specific coins and bars are placed in a dedicated container with your name and account number attached. When you eventually take a distribution, you get back the exact items you purchased. This option costs more—but for many owners, that clarity is worth it.

- Commingled storage — Your metals are pooled with other owners’ holdings of the same type and purity. You still own the full equivalent amount—but upon withdrawal, you may receive different items of the same specifications. It’s less expensive, and for standard bullion products, it works just fine.

Both options meet IRS requirements. Both sit inside the same Class 3 vault. The difference is organization—not security.

| Step | What Happens | Who Handles It | Typical Timeline |

|---|---|---|---|

| Purchase | You select IRS-approved metals | You + Dealer | Day 1 |

| Shipping | Insured, registered transport to depository | Dealer + Carrier | 3–7 business days |

| Verification | Depository confirms contents against order | Depository + Custodian | 1–2 business days |

| Vaulting | Metals placed in segregated or commingled storage | Depository | Same day as verification |

| Confirmation | Your account is updated, receipt issued | Custodian | 1–3 business days |

Why the IRS Won’t Let You Store It Yourself

This is the part that frustrates people—and understandably so. You’re buying something real and tangible, but you can’t keep it in your own home. Why not?

The IRS has a straightforward reason. Without a third-party custodian maintaining physical control, there’s no way to verify that metals still exist, haven’t been sold, or aren’t being used for personal benefit. The entire tax-advantaged status of your IRA depends on that independent oversight.

And the penalties for getting this wrong? They’re not small.

The “Physical Possession” Rule

IRC Section 408(m)(3) allows precious metals inside an IRA—but only if a bank or approved non-bank trustee holds them physically. That’s the condition. Without it, the IRS treats your metals as “collectibles,” and the purchase triggers an immediate taxable distribution.

It doesn’t matter if you label the metals as belonging to your IRA. It doesn’t matter if you store them in a separate safe. If you have direct access to them, you’re in violation.

What a $300,000 Mistake Looks Like

Back in 2021, a couple in Rhode Island learned this the hard way.

In McNulty v. Commissioner (157 T.C. No. 10), the U.S. Tax Court ruled that storing IRA-owned American Eagle coins in a home safe—even through an LLC structure—counted as a taxable distribution. The court said Mrs. McNulty had “unfettered control” of the coins, and that was enough.

The entire IRA—nearly $730,000—was treated as distributed. The couple owed roughly $270,000 in back taxes plus over $50,000 in accuracy-related penalties. One home safe. One decision. Over $300,000 gone.

The National Coin & Bullion Association had actually warned about this exact scenario in a 2018 white paper—years before the ruling came down.

The “LLC Home Storage” Myth

You’ve probably seen the ads. “Be your own custodian.” “Store your gold at home—legally.” They sound appealing. But here’s what those promoters don’t tell you:

- The IRS treats home storage as a prohibited transaction. Storing IRA metals anywhere you have direct access—your safe, your closet, a safe deposit box—triggers a distribution. The LLC structure doesn’t change that. The Tax Court was clear on this point.

- The penalty doesn’t stop at the metals you stored. The IRS can disqualify your entire IRA balance—not just the coins in the safe. Everything becomes taxable in the year the violation occurred.

- A 10% early withdrawal penalty may apply. If you’re under 59½ when the distribution is deemed to have happened, the IRS adds another 10% on top of the income tax.

- Accuracy-related penalties of 20% can follow. Under Section 6662(a), the IRS can penalize you further for understating your tax—because you didn’t report the distribution you didn’t know you triggered.

The Tax Court called these arrangements a “questionable internet scheme.” There’s no gray area left.

| Factor | Depository Storage | Home Storage (LLC) |

|---|---|---|

| IRS Compliance | Fully compliant under IRC 408(m)(3) | Prohibited transaction—triggers full distribution |

| Insurance | All-risk coverage, typically Lloyd’s of London | Homeowner’s policy unlikely to cover IRA metals |

| Security | Class 3 vaults, 24/7 surveillance, armed guards | Home safe, personal alarm system |

| Tax Risk | None if properly maintained | Income tax on entire IRA balance + penalties |

| Legal Precedent | Supported by IRS guidance and case law | Rejected in McNulty v. Commissioner (2021) |

| Audit Protection | Independent audits, custodian reporting | No third-party verification |

For a closer look at understanding gold IRA fee structures—including what depository storage actually costs compared to other IRA expenses—Brighton’s cost guide has the full breakdown.

Segregated vs. Commingled Storage: Which One Makes Sense for You?

This is one of the first decisions you’ll make after opening a precious metals IRA—and it’s simpler than it sounds.

Both options are IRS-compliant. Both keep your metals in the same high-security vault. The only difference? How your specific metals are organized inside that vault.

What Segregated Storage Looks Like

With segregated—sometimes called “allocated”—storage, your coins and bars go into a dedicated container. It’s labeled with your name and account number. Nobody else’s metals go in there.

What you buy is what you get back. If you purchased ten Gold American Eagles, those exact ten coins are waiting for you when you take a distribution.

That clarity matters to a lot of owners. There’s no guesswork, no question about which items are yours. Your custodian and the depository can point to the exact container holding your metals at any time.

At Delaware Depository—the largest precious metals depository in North America—segregated storage runs about 1.5% of value per year, with a minimum around $220.

What Commingled Storage Looks Like

Commingled—or “non-segregated”—storage pools your metals with other owners’ holdings of the same type and purity.

Think of it like a bank account. Your balance is tracked precisely, but the specific dollar bills aren’t set aside just for you. When you withdraw, you get the same amount—just not necessarily the identical bills.

Same idea here. You own the exact equivalent in weight and purity. Upon distribution, you may receive different items of the same kind—but nothing changes about what you own.

It’s the less expensive option. At Delaware Depository, commingled storage runs about 0.50% of value per year with a $125 minimum. For owners holding standard bullion products—Gold American Eagles, Silver Maple Leafs—the savings add up over time.

How Do You Decide?

There’s no wrong answer. But a few things might tip the scales:

- Segregated makes sense if — You plan to take in-kind distributions and want the exact items you purchased. Or you’re holding higher-premium coins and want a clear audit trail. Or the peace of mind is simply worth the extra cost to you.

- Commingled makes sense if — You’re holding standard bullion products, you’d rather minimize annual fees, or you’re comfortable receiving equivalent items when the time comes. For most owners with straightforward IRA holdings, this is the practical choice.

Either way, your metals are insured, independently audited, and sitting in the same Class 3 vault. The storage type doesn’t change the security—just the organization.

| Feature | Segregated Storage | Commingled Storage |

|---|---|---|

| Your metals kept separate | Yes—dedicated, labeled container | No—pooled with same type and purity |

| Receive exact items on distribution | Yes | Equivalent items of same specifications |

| Typical annual cost | $150–$290+ (or ~1.5% of value) | $100–$150+ (or ~0.50% of value) |

| Best for | High-premium coins, peace of mind | Standard bullion, lower annual fees |

| Audit trail | Specific items tied to your account | Account balance tracked precisely |

| Insurance coverage | Full replacement value | Full replacement value |

If you’re already thinking about what happens when you eventually access your metals—whether that’s years from now or at retirement—Brighton’s guide on executing a precious metals IRA distribution covers every option.

Inside an IRS-Approved Depository: What You’re Actually Paying For

Ever wonder what a place that stores billions of dollars in physical gold actually looks like?

Most people haven’t seen the inside of a precious metals depository. But knowing what goes on behind those vault doors can change how you think about storage fees—because what you’re paying for is real, and it’s substantial.

Class 3 Vault Security

“Class 3” is the highest commercial vault security rating issued by Underwriters Laboratories. These vaults are engineered to resist forced entry for extended periods—even with the most advanced tools available.

What does that look like in practice?

- Reinforced construction — Hardened concrete walls, bullet-resistant doors, and multiple controlled access points. These aren’t storage units with padlocks. They’re purpose-built fortresses designed to do one thing: keep precious metals secure.

- Biometric access controls — Fingerprint, retina, or palm scanners required for entry. No single person can access the vault alone. Facilities use what’s called “dual-control”—two authorized individuals must be present for every entry.

- 24/7 surveillance — Continuous video monitoring, motion sensors, sound and vibration detectors, and redundant power systems. If the lights go out, the security doesn’t.

- On-site security personnel — Armed guards, many with law enforcement or military backgrounds. The Texas Bullion Depository is protected by on-site Texas State Police. That’s a level of security you won’t find at a private storage facility.

All-Risk Insurance

Security protects against break-ins. Insurance protects against everything else.

Reputable depositories carry comprehensive “all-risk” policies—usually underwritten by Lloyd’s of London—covering theft, fire, flood, natural disasters, and even “mysterious disappearance.” Delaware Depository carries a $1 billion all-risk policy that covers metals in storage and in transit.

The cost of insurance is typically bundled into your annual storage fees. You don’t pay extra for it.

Here’s a detail that surprises most people: depository gold is held entirely off the balance sheet. Your metals aren’t a company asset. They can’t be seized by creditors, used as collateral, or claimed in a bankruptcy. That’s a critical difference between depository storage and a traditional bank deposit—where your money is, technically, the bank’s liability.

Independent Audits

How do you know the depository is doing what they say they’re doing?

Independent audits. The same kind used to verify major financial institutions.

Delaware Depository is continuously audited under SSAE-18 (SOC-1) standards. That means an independent accounting firm verifies physical inventory counts, tests internal controls, and confirms that chain-of-custody records match what’s actually in the vault.

As an account holder, you can request audit reports through your custodian. Many facilities also provide online portals where you can view your holdings, download statements, and track activity in real time.

For a full walkthrough of how a precious metals IRA fits together—from opening the account to making your first purchase—Brighton’s guide on establishing a precious metals IRA covers the complete process.

The Most Widely Used IRS-Approved Depositories in 2026

Not every vault qualifies for IRA storage. The IRS requires metals to be held by a bank or approved non-bank trustee—and only certain facilities meet those standards.

Here are the depositories you’ll encounter most often—and what makes each one different.

Delaware Depository Service Company (DDSC)

This is the one you’ll hear about the most—and for good reason. Delaware Depository is the largest precious metals depository in North America. Founded in 1999, it’s a limited-purpose trust company regulated by the Delaware State Bank Commissioner.

- Locations — Wilmington, Delaware (headquarters) and Boulder City, Nevada. Both vaults are IRS-approved for precious metals IRA storage.

- Security — Class 3 UL-rated vaults, 24/7 monitoring, dual-control access, and advanced surveillance systems. Continuously audited under SSAE-18 (SOC-1) standards.

- Insurance — $1 billion all-risk policy through Lloyd’s of London—covering theft, loss, fire, transit, and damage.

- Storage options — Both segregated and commingled. Online account portal for viewing holdings and downloading reports. A+ BBB rating with mostly five-star reviews.

- Licensing — CME Group (COMEX and NYMEX) and ICE Futures approved for gold, silver, platinum, and palladium.

Delaware also has no state sales tax on precious metals—which can make a difference depending on your custodian’s structure.

Texas Bullion Depository (TxBD)

This one’s unique. The Texas Bullion Depository is the only state-administered precious metals depository in the country. Created by the Texas Legislature in 2015, it operates under the oversight of the Texas Comptroller of Public Accounts.

- Location — Leander, Texas. A 40,000+ square-foot facility built specifically for precious metals, sitting on a secure 10-acre campus.

- IRA storage — Available through Lone Star Tangible Assets—an IRS-approved non-bank trustee—in partnership with Equity Trust Company.

- Security — Class 3 vault, bullet-resistant doors, biometric access, 24/7 surveillance, and on-site Texas State Police. Security personnel include commissioned officers and former military with SWAT experience.

- Storage — Segregated only. Your metals are never commingled with other owners’ holdings. That’s a policy decision—not an upsell.

- Insurance — Lloyd’s of London coverage with daily market value updates.

Texas has no state sales tax on precious metals, and assets stored at TxBD are exempt from property taxes.

Brink’s

If you’ve heard the name, it’s because Brink’s has been in the secure transport and storage business since 1859. They operate in over 100 countries with 1,100+ facilities worldwide.

- U.S. vault locations — New York, Los Angeles, Salt Lake City, and Dallas. International vaults in Zurich, London, and more.

- Storage options — Both segregated and commingled. Comprehensive insurance coverage on stored metals and those in transit.

- Logistics — Armored transport fleet for secure shipping. If your metals need to move between facilities, Brink’s handles it end to end.

International Depository Services (IDS)

IDS Group operates facilities in Delaware and Canada. They’re often recommended by Gold IRA custodians and offer both storage types with Lloyd’s of London insurance.

What sets them apart? IDS doesn’t charge extra for segregated storage on personal accounts. That’s unusual—and it makes them an attractive option for owners who want dedicated storage without the premium.

They also process withdrawal and transfer requests within 48 hours and provide monthly inventory reports.

| Depository | Locations | Storage Types | Insurance | What Sets It Apart |

|---|---|---|---|---|

| Delaware Depository | DE, NV | Segregated + Commingled | $1B Lloyd’s of London | Largest in North America, COMEX/NYMEX licensed |

| Texas Bullion Depository | TX | Segregated only | Lloyd’s of London | Only state-administered depository in the U.S. |

| Brink’s | Multiple U.S. + International | Segregated + Commingled | Comprehensive coverage | 165+ years in secure logistics |

| IDS Group | DE, Canada | Segregated + Commingled | Lloyd’s of London | No extra fee for segregated storage |

What Does Gold IRA Storage Actually Cost?

This is probably the question we hear most. And the answer is simpler than most people expect.

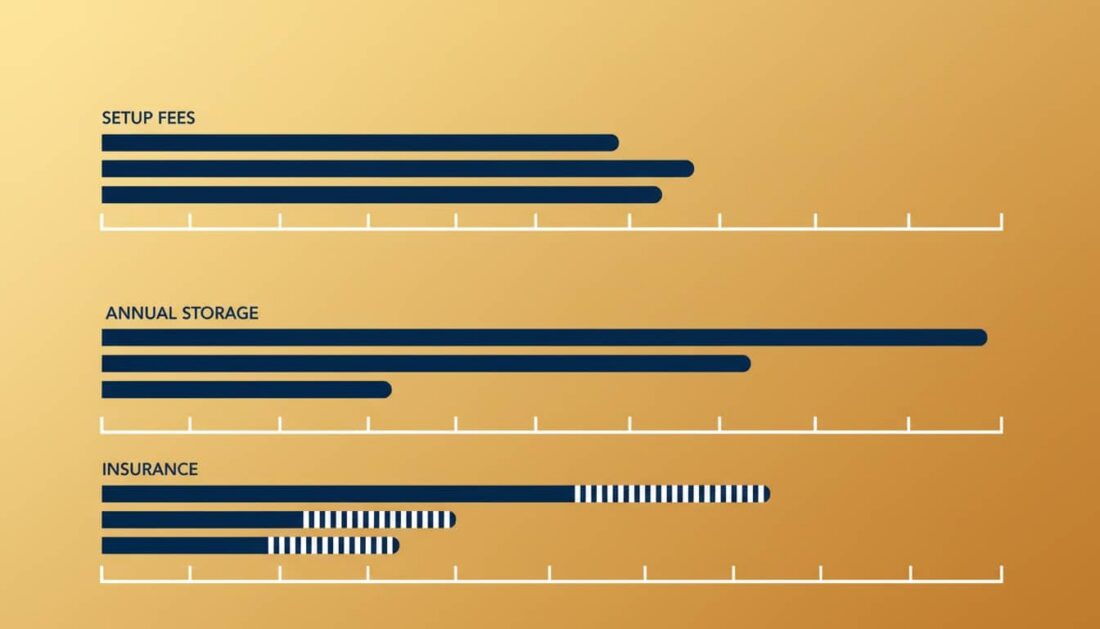

Annual storage fees typically run $100 to $300 per year. The exact number depends on three things: which depository you use, whether you choose segregated or commingled, and how much you have stored.

How the Fees Break Down

Most depositories charge a percentage of the total value of your metals, with a minimum annual fee. Here’s what that looks like with gold trading near $5,000 per ounce in 2026:

- Commingled storage — About 0.50% of value per year. On a $50,000 account, that’s roughly $250. On a smaller account, the minimum fee kicks in—usually $100 to $150 per year.

- Segregated storage — About 1.5% of value per year. Same $50,000 account would cost around $750. Minimums here start around $150 to $290 depending on the facility.

For most owners—especially those holding $25,000 to $100,000 in metals—the minimum fee is what applies.

What’s Included—and What Isn’t

Your storage fee typically covers vault space, all-risk insurance, account administration, and online portal access. That’s a lot packed into one annual charge.

What’s usually billed separately:

- Custodian fees — Your IRA custodian charges their own annual fee for account administration, typically $75 to $200 per year. This is separate from what the depository charges.

- Setup fees — Some custodians charge $50 to $100 to open the account. Not all do.

- Transaction fees — Charges for buying or selling metals inside the IRA, usually $25 to $95 per transaction.

- Shipping and handling — Costs for moving metals into or out of the depository. Insured transport isn’t free—but it’s worth every penny.

Putting It in Perspective

Here’s what a lot of people don’t realize. The annual cost of storing physical gold in a depository is often comparable to the expense ratios on mutual funds or ETFs—but with one major difference. You own the actual metal. It’s sitting in a vault with your name on it, fully insured, independently audited, and completely outside the traditional financial system.

That’s not a paper promise. That’s peace of mind.

Brighton offers a No Fee Precious Metals IRA that covers custodial fees for the lifetime of the account on qualified purchases. That removes one of the recurring costs entirely—and for many owners, it changes the math on long-term storage.

If you’ve wondered why some professionals are hesitant about gold IRAs—and what’s behind that hesitation—Brighton’s article on evaluating institutional bias against gold is worth a few minutes.

How to Make Sure Your Gold Is Really There

“I’m buying gold I can’t see. How do I know it’s actually there?”

Fair question. And the good news is—the entire system is built around answering it.

Regular Account Statements

Your custodian should provide statements—either monthly or quarterly—that show exactly what’s in your account. That includes each product type, the quantity, the weight, and a current market value based on spot prices.

Review them. Compare them to your original purchase receipts. If something doesn’t match, your custodian should be your first call.

Independent Audit Reports

This is where things get serious. Leading depositories don’t just say they have your gold—they prove it through continuous independent audits.

Delaware Depository is audited under SSAE-18 (SOC-1) standards—the same framework used for major financial institutions. An independent accounting firm verifies that physical inventory matches records, internal controls are working, and chain-of-custody documentation is airtight.

You can request copies of these reports through your custodian.

Online Account Portals

Many custodians and depositories now offer secure online portals. You can log in any time to view your holdings, download tax documents for your CPA, and track deposits, withdrawals, and fees.

It’s not a substitute for reviewing formal statements—but it’s a quick way to check in whenever you want.

In-Person Visits

Here’s something most people don’t realize: you can actually visit the depository and see your gold.

Most IRS-approved facilities allow account holders to schedule tours by appointment. If you have segregated storage, they can show you the exact container holding your metals. Delaware Depository, the Texas Bullion Depository, and Brink’s all offer this.

It’s a powerful experience. There’s something about standing in front of a Class 3 vault—knowing your gold is inside—that makes the whole thing real in a way no statement or portal can match.

A Simple Verification Checklist

Here’s what we’d recommend:

- Review your account statements every quarter. Make sure holdings match your purchase records. If anything looks off, flag it immediately.

- Request an annual audit summary from your custodian. Confirm the depository is independently audited and ask for the latest report.

- Log into your online portal at least once a month. Check for any unexpected activity—fees, transactions, or changes you didn’t authorize.

- Schedule a depository visit at least once. See the facility. Meet the team. Walk through the security. You’ll be glad you did.

- Keep copies of all purchase receipts and depository confirmations. Store them separately from your other financial records—ideally in a fireproof safe or secure digital backup.

If you’re thinking about which U.S.-minted products work best for IRA storage, Brighton’s guide on choosing IRS-approved gold coins covers the most popular options and what makes each one different.

2026 IRA Contribution Limits and What They Mean for Storage

If you’re adding to your Gold IRA this year, here are the numbers that matter—and how they connect to your storage costs.

The IRS updated contribution limits for 2026, and the increases are worth noting.

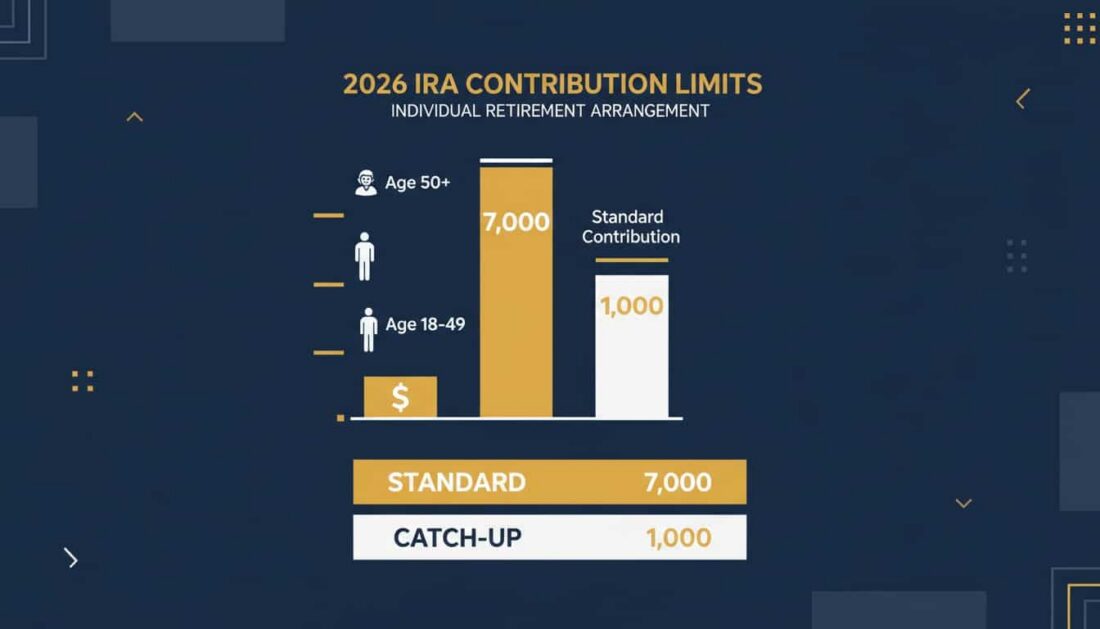

The 2026 Numbers

- Standard IRA contribution — $7,500 per year (up from $7,000 in 2025).

- Catch-up contribution (age 50+) — An additional $1,100, bringing the total to $8,600 per year. If you’re in this group, that’s real money you can put to work.

- Rollovers and transfers — No dollar limit. You can move your entire 401(k), 403(b), TSP, or existing IRA into a precious metals IRA without triggering a taxable event—as long as it’s done correctly.

Why This Matters for Storage

Every time you contribute and purchase metals, those items ship to your depository and get added to your existing holdings. With segregated storage, they go into your dedicated container. With commingled, they join the general pool.

For owners making annual contributions, the incremental storage cost is small. Adding $7,500 to a $50,000 account barely moves the needle on your annual fee.

The bigger impact comes from rollovers. Moving $100,000 or more from an existing 401(k) will increase your storage costs—because fees are tied to total account value. That’s the moment when it pays to compare depository fee structures and decide whether segregated or commingled makes more sense for your account size.

| Contribution Type | 2026 Limit | What It Means for Storage |

|---|---|---|

| Standard IRA (under 50) | $7,500 | Minimal change to annual fees |

| Catch-up (age 50+) | $8,600 total | Minimal change to annual fees |

| Rollover (401k, TSP, IRA) | No limit | May shift your fee calculation meaningfully |

| SEP IRA (self-employed) | Up to $72,000 | Higher storage fees apply at larger balances |

Frequently Asked Questions

Can I visit the depository and see my gold?

Yes. Most IRS-approved depositories let account holders schedule in-person visits by appointment.

If you have segregated storage, the facility can show you the exact coins or bars assigned to your account. Commingled holdings are pooled by metal type, so specific items won’t be individually identifiable—but you can still see the vault and the security systems in person.

Contact your custodian to arrange a visit. Depositories like Delaware Depository and the Texas Bullion Depository welcome scheduled tours.

Is my gold insured if the depository goes bankrupt?

Yes—and here’s why. IRS-approved depositories hold all precious metals off their balance sheet. Your gold isn’t a company asset. It can’t be claimed by creditors in a bankruptcy.

Facilities like Delaware Depository also maintain all-risk insurance through Lloyd’s of London—covering theft, fire, damage, and natural disasters. In the unlikely event of a closure, your metals would transfer to another approved facility.

Delaware Depository is owned by the Loomis Group, one of the world’s largest security companies. That scenario is extremely unlikely.

What’s the penalty for storing Gold IRA metals at home?

The penalties are severe—and they don’t stop at the metals you stored.

The IRS treats home storage as a taxable distribution of the entire IRA balance. You’d owe income tax on the full amount, a potential 10% early withdrawal penalty if you’re under 59½, and accuracy-related penalties of up to 20%.

In the McNulty v. Commissioner case, a couple owed over $300,000 in combined taxes and penalties after storing $411,000 in gold coins at home. Their entire IRA—nearly $730,000—was treated as distributed on the day the first coin arrived.

What’s the difference between segregated and commingled storage?

Segregated storage keeps your specific coins and bars in a dedicated container, tagged with your account number. You get back the exact items you purchased.

Commingled storage pools your metals with other owners’ holdings of the same type and purity. You own the equivalent amount—but upon withdrawal, you may receive different items of identical specifications.

Segregated typically costs $150–$290 per year. Commingled runs $100–$150 per year. Both are fully insured and IRS-compliant.

How much does Gold IRA storage cost per year?

Most owners pay somewhere between $100 and $300 per year, depending on the depository, the storage type, and total account value.

Commingled storage at Delaware Depository runs about 0.50% of value with a $125 minimum. Segregated is higher—roughly 1.5% of value with a $220 minimum.

Always ask for a written fee breakdown before committing. Some custodians bundle storage and custodian fees into one charge, which makes it harder to compare.

Are there gold depositories in Texas?

Yes—two notable ones.

The Texas Bullion Depository in Leander is the nation’s only state-administered precious metals depository. It now offers IRA storage through Lone Star Tangible Assets and Equity Trust Company. Segregated-only storage, Lloyd’s of London insurance, and on-site Texas State Police.

Texas Precious Metals Depository is a private facility also offering fully segregated storage with Lloyd’s of London coverage. Both feature Class 3 vaults, 24/7 surveillance, and no state sales tax on precious metals.

How quickly can I get my gold if I take an in-kind distribution?

Most custodians can process an in-kind distribution within 5 to 10 business days—though some take up to two weeks.

The process involves paperwork from your custodian, a shipping order to the depository, and insured delivery to your home or a designated location.

Confirm the timeline and any associated fees before you start. Precious metals may appreciate, depreciate, or remain unchanged—so factor current market conditions into the timing of your distribution.

How do I verify my metals are actually stored at the depository?

Multiple ways.

Your custodian provides regular account statements showing your holdings. Reputable depositories undergo independent audits—Delaware Depository is audited continuously under SSAE-18 (SOC-1) standards. Many facilities offer online portals for real-time access.

And you can schedule an in-person visit to see your metals at most depositories.

Consult your CPA or tax professional for guidance specific to your situation regarding any tax implications.

The Takeaway

Gold IRA storage isn’t complicated. But it does require the right facility, the right custodian, and a clear understanding of how the IRS rules work.

Here’s what it comes down to: your gold goes to an IRS-approved depository. It’s held off the balance sheet—in a Class 3 vault with all-risk insurance, independent audits, and 24/7 security. You choose between segregated and commingled storage based on your preference and budget. And home storage isn’t an option—the legal and financial consequences of trying it are devastating.

The right setup gives you something paper promises can’t: the knowledge that your gold is physically there, independently verified, and fully under your control. Not a ticker symbol. Not a promise from a fund manager. An actual, tangible product—stored safely, insured completely, and waiting for you when you need it.

That’s what support at every stage of ownership looks like.

If you’ve been thinking about how storage fits into your retirement plan—but aren’t sure where to start—you’re not alone. Most customers we work with felt the same way before they realized how straightforward the process can be with the right guidance.

That’s why we offer a complimentary consultation to walk you through your options—including our No Fee Precious Metals IRA, which covers custodial fees for the lifetime of the account on qualified purchases.

We’ll show you exactly:

- How the No Fee IRA works and whether you qualify

- The difference between U.S.-minted coins and foreign alternatives

- What to expect from the purchasing and delivery process

- How to roll over or transfer existing retirement funds

- What ongoing support looks like after your purchase

Learn About the No Fee IRA — no obligation, just actionable insights you can use whether you work with us or not.

Your gold deserves the same level of protection you’ve spent a lifetime building for your family. The right depository makes that possible.