How Does a Gold IRA Transfer Work? (Step-by-Step Guide)

A Gold IRA transfer moves funds from an existing IRA directly to a new self-directed IRA (SDIRA) custodian — without those funds ever touching your personal bank account. This method is called a Trustee-to-Trustee Transfer, and it’s the cleanest, lowest-risk way to move retirement savings into physical gold or silver.

Here’s why that matters. When funds move directly from Institution A to Institution B, there’s no mandatory tax withholding, no 60-day clock counting down, and no annual cap on how many times you can do it. The IRS treats a direct transfer differently than a rollover — and that distinction is the starting point for everything in this process.

The basic sequence works like this. You open a new self-directed IRA with a qualified SDIRA custodian. You submit a transfer request authorizing that custodian to receive funds from your existing account. The two institutions coordinate the wire directly. Once the funds arrive, you select IRS-approved metals — like the Gold American Eagle or Gold American Buffalo — which are then shipped to an insured, approved depository on your behalf.

You never take possession of the metals. The depository holds them in your name, under your SDIRA. That structure is what keeps the entire transaction inside the IRS’s approved framework.

Most transfers complete in 10 to 14 business days. The timeline depends on how quickly your current custodian processes the outgoing request — not on how fast the new account opens.

This article walks through each step of the process, how IRS rules govern transfers versus rollovers, what the real timeline looks like, what costs to plan for, and who this structure is — and isn’t — designed to serve.

- Transfer vs. Rollover: Why the Distinction Changes Everything

- The Step-by-Step Gold IRA Transfer Process

- IRS Rules That Govern Gold IRA Transfers

- Timeline, Costs, and the Question About Speed

- Who This Process Isn’t Built For

- Frequently Asked Questions

- How long does a Gold IRA transfer take in practice?

- What’s the difference between a Gold IRA transfer and a Gold IRA rollover?

- Can I move part of my IRA to gold without moving the whole balance?

- Does my current custodian have to approve the transfer?

- What are the IRS penalties if a Gold IRA transfer is done incorrectly?

- How many Gold IRA transfers can I do in a single year?

- Does a Gold IRA transfer affect my annual contribution limits?

- The Bottom Line on Gold IRA Transfers

Transfer vs. Rollover: Why the Distinction Changes Everything

Most customers arrive at this question with the same assumption: transfer and rollover are just two words for the same thing.

They aren’t.

The IRS treats them as entirely separate mechanisms — with different rules, different timelines, and different consequences. When you’re moving retirement savings into physical gold, that distinction can be the difference between a clean, tax-neutral move and an unexpected bill you didn’t see coming.

What a Direct Transfer Actually Does

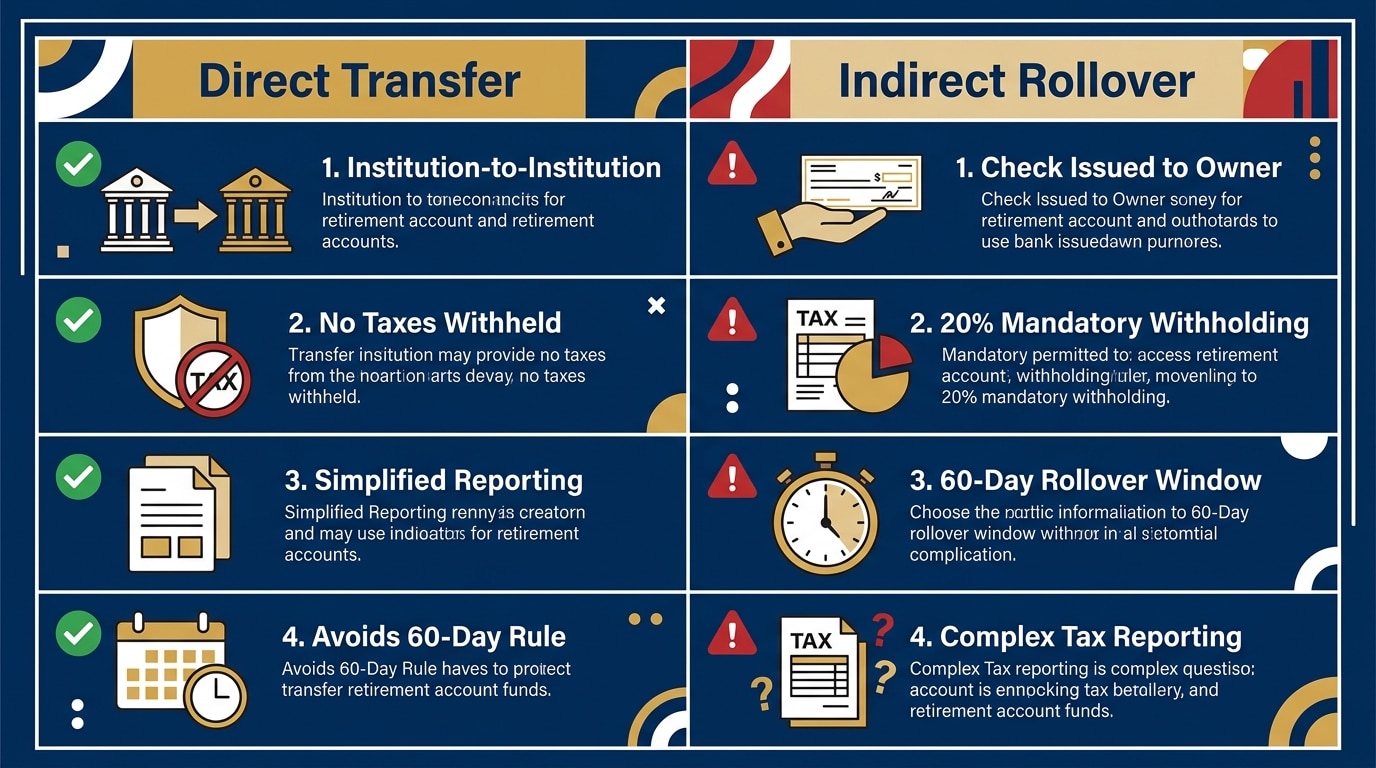

A direct transfer — Trustee-to-Trustee — means funds move from your existing IRA custodian straight to the new one. You never see a check. You never hold the money. The IRS doesn’t classify it as a distribution.

- No tax withholding — Because you never receive the funds personally, the IRS doesn’t trigger any withholding event. The money moves institution to institution without passing through your personal accounts.

- No 60-day deadline — There’s no distribution event, so there’s no clock. The funds move when the two custodians coordinate the wire — on a normal processing timeline, not a penalty-backed countdown.

- No annual frequency limit — You can execute as many direct transfers as your situation requires in a single year. The one-per-year restriction belongs to indirect rollovers only.

An indirect rollover works differently. Your current custodian sends the funds to you — minus 20%, withheld for federal taxes at the moment of distribution, per IRS Publication 590-A. You have 60 days to deposit the full pre-withholding amount into the new account. Move $100,000 and you receive $80,000. To avoid a taxable event, you have to come up with the $20,000 gap from personal funds. Miss the deadline, and the entire amount is treated as a taxable distribution. The indirect rollover also carries a one-per-year restriction across all your IRAs combined.

For anyone executing a precious metals IRA rollover or repositioning existing retirement funds into physical gold, the direct transfer is the right structure. Not because rollovers can’t work — but because the room for error is too wide, and the cost of a mistake is too real.

Why the 60-Day Rollover Catches People Off Guard

The 60-day indirect rollover wasn’t designed for this.

It was built for a narrow use case — a short-term bridge when someone needs temporary access to retirement funds before redirecting them. That’s a legitimate scenario. Using it to move IRA savings into physical metals — which involves opening a new account, coordinating two custodians, and selecting eligible products — is a different process entirely. But the two get conflated constantly in how Gold IRA moves get marketed, and customers don’t always understand the exposure until something goes wrong.

Here’s what the actual risk looks like. The 20% withholding happens at the moment of distribution. Your custodian is legally required to hold it back — there’s no option to waive it. If you fund the gap from personal funds, hit the 60-day mark, and the paperwork clears, the rollover completes without a taxable event. If any piece of that slips — the gap isn’t funded, the deadline is missed, or a document error stalls the deposit — the shortfall is treated as ordinary income for that year. If you’re under 59½, a 10% early withdrawal penalty applies on top.

IRS Notice 2026-13 provides limited safe harbor exceptions for missed deadlines — documented financial institution errors, specific medical emergencies, federally declared disasters. Confusion about the rules doesn’t qualify.

The direct transfer removes every piece of that exposure. No withholding. No deadline. No gap to fund. Most of the complexity that surrounds Gold IRA moves in the content you’ll find across the internet traces back to the indirect rollover. That’s not a coincidence. It’s a mechanism most people don’t realize they’re using until something goes wrong.

Our approach has always been to explain the difference before anything moves. Customers who understand what they’re setting up make better decisions. That’s been consistent, across every type of account and every kind of customer we work with.

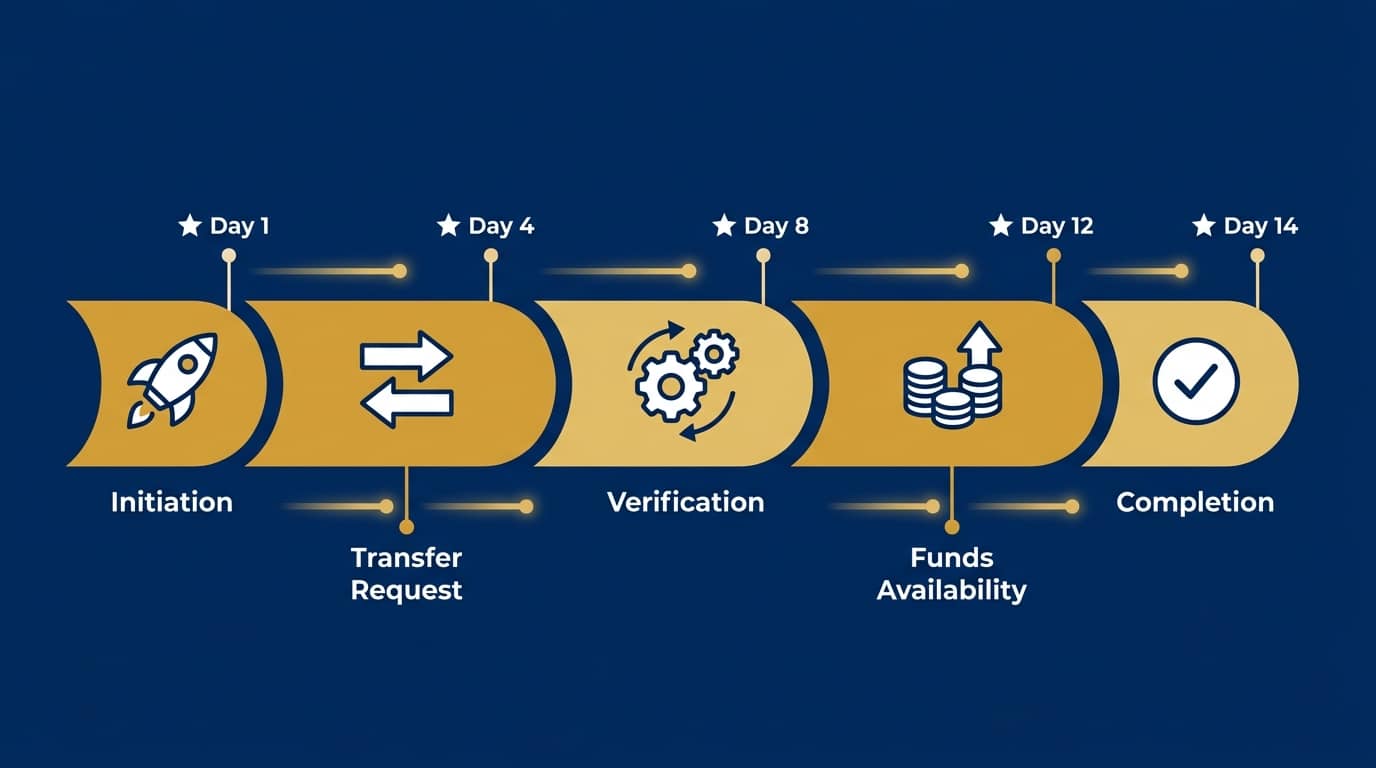

The Step-by-Step Gold IRA Transfer Process

Here’s how the process actually unfolds — who’s involved at each stage and what the realistic timeline looks like.

| Step | Action | Who’s Involved | Typical Timeline |

|---|---|---|---|

| 1 | Open a Self-Directed IRA | You + SDIRA Custodian | 1–3 business days |

| 2 | Submit Transfer Request | You + New Custodian | Same day |

| 3 | Funds Wire to New Account | Old Custodian → New Custodian | 5–10 business days |

| 4 | Select and Purchase IRS-Approved Metals | You + Dealer | 1–3 business days |

| 5 | Metals Shipped to Approved Depository | Dealer + Depository | 3–5 business days |

Total: 10–14 business days from SDIRA application to metals in vault.

Step 1: Open a Self-Directed IRA

Your existing IRA — whether it’s at a brokerage, a bank, or a mutual fund company — almost certainly can’t hold physical precious metals. Standard IRA structures were built for paper assets: stocks, bonds, mutual funds. A Self-Directed IRA opens the door to alternatives, including physical gold and silver, while keeping the account inside the IRS’s tax-advantaged framework.

Establishing a precious metals IRA starts with choosing a qualified SDIRA custodian — an IRS-approved trust company or specialty financial institution authorized to hold alternative assets on your behalf. The application is digital in most cases. Identity verification, beneficiary designation, account type selection. Most custodians complete this in one to three business days.

- Traditional SDIRA — Pre-tax contributions, taxes owed at withdrawal. The most common structure for IRA-to-IRA transfers, and the default for most customers coming from a traditional brokerage account.

- Roth SDIRA — After-tax contributions. Qualified withdrawals are tax-free. A Roth-to-Roth transfer keeps that tax treatment intact — no mixing of pre-tax and post-tax funds.

- SEP or SIMPLE SDIRA — Available for self-employed owners and small businesses holding those account types. The transfer mechanics are the same; the account structure has its own eligibility rules.

Brighton Gold works with qualified custodians and walks customers through the selection process. We don’t direct which custodian you use — that decision belongs to you. Our role is to make sure you understand what you’re choosing before you sign anything.

Step 2: Submit the Transfer Request

Once the new SDIRA is open, your new custodian sends a transfer authorization to your existing institution. This is the formal instruction that triggers the outgoing wire.

Your existing custodian may require their own documentation — a specific transfer request form, a medallion signature guarantee, or a letter of acceptance from the receiving institution. Most of that coordination happens directly between the two custodians. Your role is to authorize the transfer and confirm the request has been submitted.

Completing a gold IRA rollover documentation correctly at this stage is what prevents the most common delays. A single missing field or mismatched account number can add several business days to the processing window.

- Verify account details — Confirm the new SDIRA’s account number and routing information are accurate before submission. Mismatched numbers are the single most common documentation error.

- Check custodian-specific requirements — Some outgoing institutions require their own transfer request format rather than accepting the new custodian’s paperwork directly.

- Follow up at seven days — If wire confirmation hasn’t arrived by business day seven, call the outgoing custodian’s transfer department directly. Document the date and the name of whoever you speak with.

Step 3: Funds Wire Directly to the New Account

Once the outgoing custodian approves the request, the funds wire straight to the new SDIRA. No check arrives at your door. The money doesn’t pass through your personal bank account. It moves institution to institution — and that’s exactly what makes this a non-taxable event.

The wire itself clears in hours once submitted. What takes time is the queue at the outgoing institution. Large brokerages and mutual fund companies are not structured to prioritize outgoing SDIRA transfers — those transfers represent an account they’re losing. Expect the longer end of the 5–10 business day window when the sending institution is a major brokerage.

Step 4: Select IRS-Approved Metals

Once funds confirm in the new SDIRA, the purchase moves forward. Not every gold or silver product qualifies for IRA holding. The IRS sets specific fineness standards — metals that don’t meet those requirements cannot be included, regardless of their market value.

| Metal | IRS-Approved U.S. Products | Minimum Fineness |

|---|---|---|

| Gold | American Eagle, American Buffalo | .995 (Eagles exempt at .9167 per statute) |

| Silver | American Eagle, 100 oz bars, .999 rounds | .999 |

| Platinum | American Eagle, select bars | .9995 |

| Palladium | American Eagle, select bars | .9995 |

Per the U.S. Mint, the Gold American Eagle qualifies for IRA holding despite not meeting the standard .995 fineness threshold — a specific statutory exemption under IRC Section 408(m) that applies to no other coin.

We work with customers on choosing IRS-approved gold coins and U.S.-minted products that meet these requirements. We’re not going to steer you toward something you don’t understand. U.S.-minted is our standard — provenance, purity verification, and long-term liquidity all matter to owners who are planning to hold for the long term.

Step 5: Metals Go to an Approved Depository

After purchase, the metals ship from the dealer directly to an IRS-approved depository on your behalf. You don’t take possession. You don’t sign for a package at your door. The metals move from the dealer to a secure, insured facility — held in your name, under your SDIRA.

Home storage of IRA metals isn’t permitted under IRS rules, regardless of what some marketing implies. Understanding gold IRA storage rules — including the practical difference between segregated storage and commingled storage — is worth doing before you make that selection, not after the account is funded.

IRS Rules That Govern Gold IRA Transfers

Most of the regulatory complexity people encounter when researching Gold IRA moves belongs to rollovers. The direct transfer framework is considerably cleaner. Here’s what the rules actually say.

No Annual Cap on Frequency

Trustee-to-Trustee transfers are unlimited. There’s no ceiling on how many you can execute in a calendar year. The one-per-year restriction applies to indirect rollovers — and it applies across all your IRAs combined, not per account. Direct transfers exist entirely outside that framework.

- Consolidating multiple IRAs — Each account transfers independently. No timing concern. No required sequencing. If you have four existing IRAs you want to consolidate into a single SDIRA, all four can move in the same window.

- Partial transfers — You specify a dollar amount, not a total account balance. A $50,000 transfer from a $200,000 IRA releases that portion while the remaining $150,000 stays exactly where it is, untouched.

- No 1040 reporting required — Direct transfers don’t appear as distributions on your tax return. The movement is institution to institution — invisible to the IRS as a distribution event.

SECURE 2.0 and Required Minimum Distributions

The SECURE 2.0 Act moved the Required Minimum Distribution age to 73 for most retirement account owners. Physical metals in an SDIRA fall under the same RMD framework as any other IRA — there’s no exemption because the assets are physical rather than paper.

Once you reach that threshold, annual distributions are required. If you’d rather not liquidate metals to satisfy the RMD, an in-kind distribution is an option — meaning the metals themselves are distributed, valued at fair market value for that tax year.

This is a tax planning conversation, not a metals conversation. We recommend working through your RMD strategy with a CPA or tax professional before any transfer happens. Brighton Gold doesn’t provide financial, tax, or legal advice. That’s not language buried in fine print — it’s something we say clearly, every time.

The Partial Transfer Option

You don’t have to move the entire balance. A partial transfer specifies exactly the amount moving — the rest stays in the original account on its existing schedule. Many customers structure their first move this way: a partial transfer to get comfortable with the new custodian and the process, before committing additional retirement savings to the SDIRA.

| Transfer Feature | Direct Transfer | Indirect Rollover |

|---|---|---|

| Tax Withholding | None | 20% mandatory |

| 60-Day Deadline | No | Yes |

| Annual Frequency Limit | Unlimited | Once per 12 months |

| Partial Transfer Permitted | Yes | Yes |

| Triggers IRS Distribution | No | Yes (if not redeposited in full) |

| IRS Reporting Required | No | Yes (Form 1099-R + Form 5498) |

Timeline, Costs, and the Question About Speed

The concern we hear most often isn’t about compliance or documentation. It’s about timing.

Customers want to know whether a transfer that takes 12 business days means they’ve missed something.

Here’s the answer: a 12-business-day transfer isn’t a slow process. That is the process — working exactly as it’s designed to. The steps that require time — custodian approval, wire settlement, depository confirmation — exist to protect the tax-advantaged status of the account. There’s no shortcut that doesn’t create risk. The direct transfer is already the fastest legitimate vehicle for moving IRA funds into physical metals.

The Real Source of Delays

It’s not the wire.

The wire clears in hours once it’s submitted. The wait is in the outgoing custodian’s processing queue — and that queue isn’t structured around speed for outgoing transfers. Large brokerages and mutual fund companies are built to retain assets, not move them out. An outgoing SDIRA transfer represents a lost account, and it gets treated accordingly in their processing stack.

What you control: responding quickly when documentation is requested, verifying account details before submission, and following up at the seven-day mark if no confirmation has come through. What you can’t control is another institution’s internal timeline. If a specific custodian is consistently slow on outgoing transfers, that’s useful information before any additional accounts are consolidated there.

What the Costs Actually Look Like

Understanding gold IRA fee structures before choosing a dealer matters more than most first-time customers realize. Total cost of ownership changes the comparison — not any single line item in isolation.

- Custodial fees (annual) — Charged by the SDIRA custodian for account maintenance, IRS reporting, and recordkeeping. Structure varies by institution: flat annual fee or percentage-based, depending on account value and custodian model.

- Storage fees (annual) — Charged by the depository. Based on the value or weight of metals held. Segregated storage — where your metals are held in a dedicated space — typically runs higher than commingled storage, where your metals are pooled with others of the same type.

- Dealer premium — The spread between spot price and the purchase price on a specific coin or bar. This is where product selection and the dealer relationship have the most measurable impact on what you actually pay.

- One-time setup fees — Some custodians charge to open the SDIRA and process the initial transfer. Not universal. Worth confirming before you sign.

Brighton Gold offers a No Fee Precious Metals IRA for the lifetime of the account on qualified purchases. That’s a structural commitment — not a first-year promotional waiver that expires and leaves you absorbing fees you weren’t expecting. There’s a real difference between the two, and it’s the kind of detail worth asking about directly with any dealer you’re evaluating.

Who This Process Isn’t Built For

A Precious Metals IRA is a long-term ownership structure.

The customers who benefit from it most are thinking in years — sometimes decades. That framing shapes the entire relationship.

What This Structure Is Built For

The question underneath most conversations about Gold IRA transfers isn’t really about mechanics. It’s: “Is there a way to hold something real — something outside the paper financial system — while keeping my retirement savings protected?”

That’s the customer this structure serves. Former professionals, business owners, veterans, and families who’ve spent decades building what they have. People who value self-reliance, want to move outside the traditional financial system, and want to leave something tangible for the next generation.

- Long-term owners — Customers who measure their holding timeline in years, not quarters. The SDIRA structure, custodial relationships, and depository arrangements all become more efficient over a multi-year hold.

- Preservation-focused customers — People who aren’t trying to outperform a benchmark. They want something held in their name, outside paper asset volatility, with a clear chain of ownership.

- Legacy planners — Customers who want physical assets that can be passed to family — something tangible and clear, not a brokerage statement with inherited complexity.

Brighton Gold’s No Fee Precious Metals IRA for the lifetime of the account on qualified purchases was built around this customer. Long-term holding is what makes that commitment sustainable — and meaningful — on both sides of the relationship.

It also means this structure isn’t designed for everyone. We’d rather be clear about that now than discover it three months into a relationship that wasn’t the right fit to begin with.

A Word to Speculators

If the goal is to move retirement savings into gold today and sell in six months because prices look like they’re moving — this structure isn’t built for that, and Brighton Gold isn’t the right partner for it.

We don’t forecast gold prices. We don’t time markets. We don’t tell customers when to buy or sell. Precious metals may appreciate, depreciate, or remain unchanged. Anyone presenting price predictions as professional guidance is offering something that doesn’t exist — and recognizing that distinction is part of what identifying safe gold IRA practices actually looks like.

The World Gold Council’s demand research reflects consistent long-term interest in physical gold from central banks and institutional holders — not as a short-term trade, but as a structural holding strategy. That’s the framing our customers share. It’s not the only way to own gold. It’s the way that fits the structure being described here.

- Price forecast seekers — We don’t tell customers where gold is headed. Not because we won’t, but because no one can do it honestly. A dealer who claims otherwise is worth a second look.

- Short-term traders — Custodial fees, storage fees, and transfer timelines make a Precious Metals IRA a poor vehicle for a six-month hold. The structure itself works against that goal.

- Guaranteed outcome expecters — Brighton Gold doesn’t guarantee buybacks or fixed resale pricing. Resale depends on market conditions at the time you decide to sell. That’s disclosed upfront, before anything is signed, every time.

We work with customers who want to hold for the long term. If that’s not where you are right now, we understand — and we’d rather know that in this conversation than after the transfer is done.

Frequently Asked Questions

How long does a Gold IRA transfer take in practice?

Most Gold IRA transfers complete in 10 to 14 business days from SDIRA application to metals in the depository. The variable that matters most is the outgoing custodian — large brokerages run slower than smaller or specialty custodians, and that gap can be meaningful. Once funds clear into the new SDIRA, metals selection and depository delivery typically add another three to five business days. If a transfer is running well past the 14-day window, the first question is always whether the outgoing custodian has processed the wire. That’s where delays originate, almost without exception.

What’s the difference between a Gold IRA transfer and a Gold IRA rollover?

A transfer is a direct Trustee-to-Trustee movement — institution to institution, no check issued, no distribution event. The rollover sends funds to you personally, triggers mandatory 20% federal tax withholding at the time of distribution, requires you to deposit the full pre-withholding amount within 60 days, and carries a one-per-year restriction across all your IRAs. Direct transfers do none of those things. For customers moving existing IRA funds into a precious metals IRA, the direct transfer is the standard recommendation — not because rollovers are impossible, but because the risk profile is entirely different.

Can I move part of my IRA to gold without moving the whole balance?

Yes. Partial transfers are permitted and common. The transfer request specifies a dollar amount — not a full account balance. Your existing IRA releases exactly what you specify, and the remainder stays put. Many customers structure their first move as a partial transfer — it’s a practical way to get familiar with the SDIRA custodian, the process, and the depository before committing additional retirement savings. There’s no minimum dollar threshold to open the SDIRA, though custodian fee structures may make very small transfers less efficient.

Does my current custodian have to approve the transfer?

Your current custodian processes the outgoing transfer request, but they cannot refuse a legitimate transfer to another IRS-approved custodian. They may require specific documentation — a transfer authorization form, a letter of acceptance from the new institution, or medallion signature verification — but the transfer itself cannot be blocked without cause. If you encounter unusual resistance or delays significantly beyond the custodian’s stated processing window, call their transfer department directly and document the conversation.

What are the IRS penalties if a Gold IRA transfer is done incorrectly?

A direct Trustee-to-Trustee transfer, executed correctly, carries no penalty. The risk is in indirect rollovers. If the 60-day deadline is missed, the full distributed amount is treated as taxable income for that year, and if you’re under 59½, a 10% early withdrawal penalty applies on top. The 20% withheld by the outgoing custodian counts as a payment toward that tax obligation — but only the amount actually redeposited within the 60-day window qualifies for rollover treatment. Missed deadlines are rarely forgiven. This is one of the central reasons the direct transfer is the preferred approach for moving retirement savings without triggering a penalty.

How many Gold IRA transfers can I do in a single year?

Direct Trustee-to-Trustee transfers are unlimited. There’s no cap on frequency. The one-per-year restriction applies only to indirect rollovers — and across all IRAs combined, not per account. Customers consolidating several existing IRAs into a single SDIRA can transfer each one independently, without any timing or sequencing requirement. Three transfers, four transfers — same window, no conflict.

Does a Gold IRA transfer affect my annual contribution limits?

No. A transfer is a movement of existing funds — not a new contribution. The IRS treats contributions and transfers as entirely separate mechanisms. A Trustee-to-Trustee transfer doesn’t count toward your annual IRA contribution limit, and you can complete one in the same tax year you make a standard contribution — subject to income eligibility and contribution limits for your account type.

The Bottom Line on Gold IRA Transfers

The process of moving existing IRA funds into physical gold isn’t complicated. That’s not a sales line — it’s what the mechanics actually show. You open a Self-Directed IRA. You submit a transfer request. You wait for the wire to clear. You select IRS-approved metals, and they go to a secure depository in your name. That’s the whole sequence.

What makes it feel complicated — in most of the content written about it, and in conversations with customers who’ve spent weeks researching online — is the persistent conflation of transfers and rollovers. The 60-day window, the mandatory withholding, the one-per-year restriction: those are real constraints. They belong to indirect rollovers. Not one of them applies to a direct Trustee-to-Trustee transfer. And for the vast majority of customers moving IRA funds into physical metals, the direct transfer is the right tool — structurally, logistically, and from a risk standpoint.

Brighton Gold’s position is straightforward. Customers who understand what they’re doing — the mechanics, the costs, the timeline, the IRS structure — make better decisions and have better experiences. That’s why the Brighton Gold Learning Center exists. Not to generate content, but because the clearest path to a good customer relationship is one where the customer already knows what they agreed to before anything moves. Precious metals may appreciate, depreciate, or remain unchanged. What doesn’t change is how the IRA transfer process works. Done correctly, it places physical gold in your name — held in a secure, insured depository, outside a brokerage, outside a mutual fund — under the full protection of the IRS’s tax-advantaged framework. That outcome is worth understanding clearly before you decide whether it’s right for you.

You’ve now got a clear picture of the mechanics — the steps, the IRS rules, the timeline, and the costs. What this article can’t give you is a look at how the structure fits your specific retirement situation.

That’s what Brighton Gold’s complimentary consultation is built to do.

We’ll walk through how the transfer works for your specific account type, what the No Fee Precious Metals IRA structure looks like in practice, and whether this makes sense given where you are. No obligation. No pressure. Just a clear conversation — so if you move forward, you do it with your eyes open.

Most customers who have that conversation leave with more clarity than they expected. The goal isn’t to sell you something. It’s to give you a picture clear enough to make your own call.