How Do I Choose the Right Gold IRA Custodian for Wealth Preservation?

Choosing the right Gold IRA custodian comes down to three non-negotiable benchmarks.

First: IRS Approval. Every institution holding retirement assets in a self-directed IRA must appear on the IRS list of Approved Nonbank Trustees. That’s not a formality — it’s a legal requirement. If a custodian isn’t on that list, they don’t have the authority to hold your IRA. The list is public and searchable. Check it.

Second: Fee Transparency. Custodial fees come in two structures — flat and scaled. A flat fee charges the same fixed annual amount regardless of account value, typically $200–$300 per year. A scaled fee is calculated as a percentage of your account’s total value. As gold prices rise, a scaled fee takes more money out of your account every single year — without you buying a single additional ounce. At current gold prices, that distinction is not trivial.

Third: Audit Compliance. Reputable custodians submit to SSAE-18 audits — an independent, third-party review of their internal controls, record-keeping processes, and financial reporting. If a custodian can’t produce documentation of a current SSAE-18 audit, treat that as a red flag worth taking seriously.

Beyond those three benchmarks, there’s a structural layer most articles skip entirely: the relationship between your custodian, your dealer, and the depository where your metals are physically stored. Each party serves a different legal function. Each one should remain independent of the others. Understanding how those three roles interact is what separates an informed custodian decision from a costly assumption.

This guide walks through every dimension of that decision — how to verify custodial authority, how to read a fee schedule, what audit compliance actually means, how the three-party structure protects you, and what questions to ask before you sign anything.

- What a Gold IRA Custodian Actually Does — and Why the Industry Doesn’t Want You to Know

- The Four-Step Framework for Vetting Any Gold IRA Custodian

- Custodian Fee Structures — The Number That Grows With Your Gold

- The Three-Party Structure That Protects Your Gold IRA

- This Is a Long-Term Ownership Decision — Not a Speculation Play

- Frequently Asked Questions About Gold IRA Custodians

- What is the difference between a Gold IRA dealer and a custodian?

- Can I choose my own custodian, or does the dealer choose for me?

- What are standard annual custodial fees for a Gold IRA?

- Is my gold safer with a bank or a non-bank trust company?

- What is an SSAE-18 audit and why does it matter for my retirement gold?

- How do I know if a Gold IRA custodian is IRS-approved?

- The Bottom Line on Custodian Selection

What a Gold IRA Custodian Actually Does — and Why the Industry Doesn’t Want You to Know

Most customers arrive at the custodian question with their mind already made up about the Gold IRA itself. The product decision is done. What nobody has asked yet is who’s actually going to hold the account.

By that point, a dealer has usually made a recommendation. The customer assumes the dealer has done the vetting — and goes with it.

That assumption is what costs people later.

Choosing a gold IRA custodian isn’t an administrative detail. It’s the decision that determines who holds the legal framework of your entire retirement account — the entity whose name is on the IRA, responsible for every record, every transaction report, and every IRS filing throughout your holding.

That deserves independent scrutiny. Not a handoff.

Here’s the friction running through this industry: complexity in custodian selection benefits the firms that create it. Jargon-heavy explanations, bundled decisions, and a single recommended custodian with no alternatives offered aren’t there to protect the customer. They simplify the process for someone else.

If you’ve already started setting up a Precious Metals IRA — or you’re evaluating whether one makes sense — understanding the custodian’s specific role inside that structure is where the process needs to start. Not the last thing you figure out.

Before going further, identifying safe gold IRA practices — what warning signs look like at each stage — is worth reading alongside this guide.

The Legal Role of a Custodian in a Self-Directed IRA

IRS rules require that every self-directed IRA — Gold IRA included — be held by a qualified trustee. That’s the custodian’s legal function.

Their responsibilities are specific. No interpretation required:

- Holding the account — The IRA is established in the custodian’s name on your behalf. They maintain legal title throughout your holding and are responsible for the account’s integrity at every stage.

- Maintaining transaction records — Every purchase, transfer, rollover, and distribution is documented by the custodian. These are the official records of your IRA’s activity — not the dealer’s records, not yours.

- Filing IRS Form 5498 — At year end, the custodian reports the fair market value of your account to the IRS using established valuation standards. This is not a dealer estimate. It is a formal, regulated filing.

- Executing your directions — When you direct a purchase, the custodian coordinates with the dealer and arranges delivery to the depository. They act on your instruction. The decision is yours; the execution is theirs.

What the custodian does not do — and this matters — is direct what you buy, when you buy it, or whether a Gold IRA is the right choice for your retirement situation. They are administrators, not planners.

Why Dealer-Custodian Bundling Deserves Scrutiny

Some dealers route customers to custodians they have preferred referral arrangements with. That custodian may carry higher fees, offer fewer depository options, or operate under less favorable terms than alternatives a customer would have found with independent research.

It’s legal. It’s also not disclosed the way it should be.

SEC Rule 206(4)-2 was built around a principle that applies here: the management and custody of assets should involve separation — not bundling. The rule covers registered financial professionals in a specific context, but the logic extends. When a single firm controls both what you acquire and where it’s held, a conflict of interest is possible — even when no fraud is involved.

Ask any dealer directly: “Can I choose my own custodian, or are you directing me to a preferred institution?”

One option offered. No explanation for why. That’s your signal.

Fee differences between custodians are significant — and they compound across years of holding. Understanding gold IRA fee structures before you commit is part of that independent research.

The Four-Step Framework for Vetting Any Gold IRA Custodian

Here’s the reality: vetting a custodian doesn’t require a legal background. It requires four questions — asked in writing, answered in writing. Any institution worth working with answers all four without hesitation.

Hesitation, on any of them, is useful information.

| Step | What to Verify | Where to Confirm |

|---|---|---|

| 1 | IRS Approved Nonbank Trustee status | IRS Approved Nonbank Trustee list (irs.gov) |

| 2 | Written fee schedule — all-in costs, flat or scaled | Written fee disclosure document from the custodian |

| 3 | SSAE-18 audit compliance — most recent report date | Request directly from the custodian |

| 4 | Depository options — customer chooses, not custodian | Confirmed in writing at account opening |

Step 1 — Confirm IRS Approved Nonbank Trustee Status

The IRS maintains a publicly accessible list of Approved Nonbank Trustees — every institution that has received formal authorization to hold retirement assets without being a chartered bank.

Search it. Find the custodian you’re evaluating. Confirm they appear on it.

Most self-directed IRA custodians are nonbank trust companies — a legitimate structure. What matters is that this specific institution, the one in front of you right now, is on the list.

If they’re not, or if they’re slow to confirm, stop. A real custodian doesn’t hesitate on this question. There is no legitimate reason to.

Step 2 — Request a Written Fee Schedule Before Signing Anything

Verbal quotes are not binding. They also rarely include everything.

Ask for a complete, written fee schedule before any funds move, any documents are signed, or any commitment is made. It should itemize:

- Annual custodial maintenance fee — Stated as a fixed dollar amount (flat) or as a percentage of account value (scaled)

- Account setup fee — One-time, charged at opening; some institutions charge several hundred dollars, others charge nothing

- Wire transfer fees — Applied when funds move in or out

- Precious metals transaction fees — Charged when you direct a purchase or sale within the IRA

- Distribution fees — Some custodians charge a processing fee on distributions; others don’t

This connects directly to executing a precious metals IRA rollover. Knowing the full cost structure before a rollover begins is the most straightforward way to avoid surprise.

Step 3 — Ask for Their Most Recent SSAE-18 Audit Report

SSAE-18 is the audit standard that verifies a custodian’s internal controls have been reviewed and validated by an independent third party — record management, financial reporting, security protocols, all of it.

Ask for the most recent report. Ask for the name of the auditing firm.

Without an SSAE-18, you’re relying entirely on the custodian’s own account of how they operate. That’s not a standard we’d accept from any other institution holding retirement assets. It shouldn’t be accepted here.

Any legitimate custodian provides both answers — the report and the firm name — without delay. That response time is part of the evaluation.

Step 4 — Confirm That Depository Selection Is Yours to Make

Your custodian coordinates with the depository. The selection of which depository holds your metals — that belongs to you.

Ask directly: “Do I have options for which depository holds my metals, or is one pre-selected?” A trustworthy custodian offers at least two or three IRS-approved facilities and lets you choose based on location, storage type, and fee structure.

A pre-set depository with no explanation is worth pressing on before proceeding. Understanding gold IRA storage rules — what segregated versus commingled storage means in practice — gives you the foundation to ask the right questions at this step.

Custodian Fee Structures — The Number That Grows With Your Gold

Gold is trading at $4,733 per ounce as of April 2026.

That number matters to this conversation — not for what it says about price activity, but for what it does to a percentage-based custodial fee.

When gold was at $2,000 an ounce, a 0.35% annual fee cost $700. At $4,733, that same fee structure costs $1,658 — on the same account, with no additional ounces purchased. On a $300,000 account, you’re paying more than $1,000 per year in custodial fees, automatically, as a direct function of price movement.

That math is why fee structure belongs on the short list of consequential decisions in a Gold IRA setup.

Why Flat Fees Protect You as Gold Prices Rise

A flat annual fee is what it sounds like. One fixed dollar amount. Same charge every year, regardless of account value, price movement, or number of ounces held.

A scaled fee moves with the account. Every dollar of price appreciation — and every additional ounce you add — increases what you pay the custodian annually. You don’t have to do anything to owe more. The spot price does it for you.

| Fee Type | Structure | Fee on a $100K Account | Fee on a $300K Account | Fee on a $500K Account |

|---|---|---|---|---|

| Flat Fee | Fixed annual charge | ~$200–$300/yr | ~$200–$300/yr | ~$200–$300/yr |

| Scaled Fee (0.15%) | % of account value | ~$150/yr | ~$450/yr | ~$750/yr |

| Scaled Fee (0.35%) | % of account value | ~$350/yr | ~$1,050/yr | ~$1,750/yr |

At $100,000, a scaled fee can look competitive — sometimes cheaper than flat. At $300,000 or $500,000, the gap is no longer academic.

The industry benchmark for a flat annual custodial fee is $200–$300 per year. That’s the reference point.

Additional Costs to Clarify Before You Commit

Annual custodial fees are one layer. A complete cost picture separates custodian fees from depository fees — billed by a different institution entirely — and accounts for every other charge in between.

- Storage fees — Paid to the depository, not the custodian. Cost depends on storage type. Segregated storage — your metals held apart from other owners’ holdings — typically costs more, but provides cleaner documentation of what you own and where it is at any given time.

- Transaction fees — Applied each time you direct a purchase or sale within the IRA. Flat per transaction or percentage-based; ask before assuming.

- Wire and transfer fees — Some custodians bundle these into the annual fee; others itemize them. Verify before account opening.

- Distribution fees — Processing a distribution may carry a separate charge, depending on the institution and the form the distribution takes.

One option worth understanding — with your CPA’s guidance — is an in-kind distribution: physical metals transferred out of the IRA directly rather than sold and liquidated first. Tax treatment depends on a range of factors specific to your situation. That conversation belongs with a qualified tax professional. Brighton Gold does not provide tax advice.

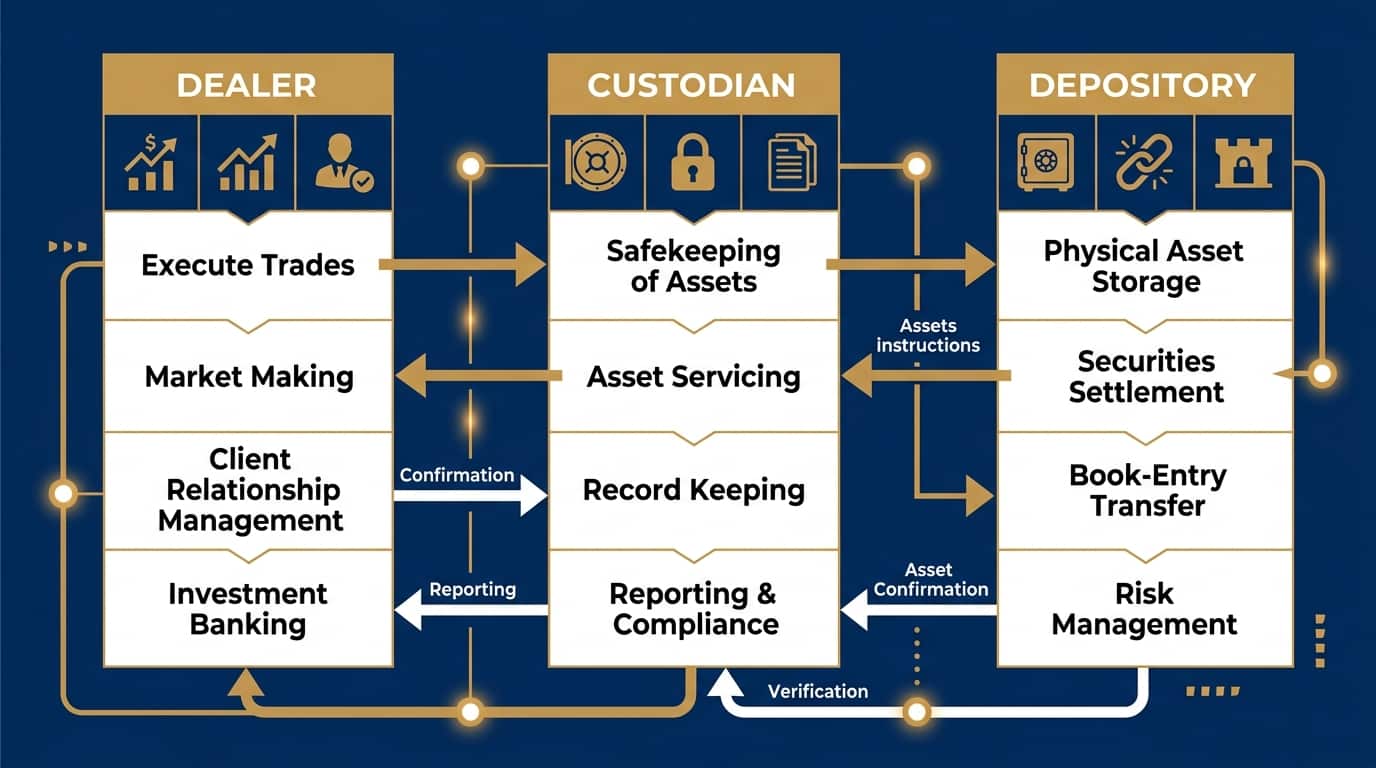

The Three-Party Structure That Protects Your Gold IRA

A Gold IRA involves three parties. Not two — three.

Most owners know the dealer. Some understand the custodian’s role. Fewer have thought carefully about the depository until they’re already in the middle of the process.

Here’s why all three matter — and why the separation between them is the design, not the complication.

| Party | Primary Role | What They Do Not Do |

|---|---|---|

| Dealer | Sources and sells IRS-approved metals | Holds the IRA; stores the metals |

| Custodian | Holds the IRA account; maintains records; files IRS forms | Sells the metals; stores the metals |

| Depository | Physically stores the metals; provides insurance and independent audits | Holds the IRA; sells the metals |

Why Each Party Serves a Different Function

The dealer’s role ends when the metals are purchased and delivered to the depository. From that point, the custodian administers the account and the depository maintains physical security. Separate functions. Separate institutions. Separate accountability.

When one firm controls more than one of these roles — through affiliated entities, internal referral arrangements, or opaque structural relationships — the customer loses the protection that independence provides. What’s being sold as convenience is often just the removal of a check that existed to protect you.

Independence is the point. It’s what keeps each relationship clean.

Brighton Gold’s educational library covers the full landscape of Gold IRA topics — structure, storage, transfers, distribution options — for owners who want to understand every layer before they commit to any of them.

For those approaching the transfer side of this decision, what a Gold IRA transfer actually involves — including how custodian selection shapes timing and mechanics — is a natural companion to this guide.

The Home Storage Problem and Why Professional Custody Exists

We get this question regularly: can IRA-held gold be stored at home?

The U.S. Tax Court’s ruling in McNulty v. Commissioner answers it without ambiguity. Personally storing metals that belong to an IRA constitutes a taxable distribution. The moment those metals leave a qualified depository and enter your possession, the IRS treats them as distributed — regardless of your intent or how you stored them. The tax liability follows immediately.

This isn’t a gray area. It’s a settled question with documented consequences for owners who found out the hard way.

BBB-accredited custodians work exclusively with IRS-approved depositories — Class 3 vault facilities with appropriate insurance coverage and independent auditing of their holdings. That infrastructure isn’t regulatory overhead. It’s what keeps your account classified as an IRA rather than a taxable distribution event.

This Is a Long-Term Ownership Decision — Not a Speculation Play

The process above — four-step vetting, fee structure analysis, three-party structure review — is built for a specific type of owner.

Not every buyer fits that profile. We’d rather say so directly.

Who the Gold IRA Custodian Process Is Built For

The owner who benefits most from getting custodian selection right is one who:

- Wants to hold physical gold or silver in an IRA for years, not months — The structure, the three-party coordination, and the associated setup all point toward long-term holding. It’s not a vehicle designed for rapid movement.

- Is focused on protecting what they’ve built — Not chasing price activity. Not timing a market entry. The orientation is stability, preservation, and holding something real outside the paper financial system.

- Understands that guidance quality matters more than the lowest price — Custodians who cut fees often cut corners elsewhere — on audit compliance, depository options, or support when questions arise. The real cost of custody shows up over years.

- Has accepted the full reality of physical metals ownership — Precious metals may appreciate, depreciate, or remain unchanged. That’s built into the decision — not a caveat to get past.

If that’s where you are, custodian selection is foundational. Get it right and you won’t revisit it.

For owners working through product selection at the same time, choosing IRS-approved gold coins is a natural companion step — product eligibility and custodian selection happen in the same phase of the process.

Who Should Look Elsewhere

Brighton Gold isn’t the right fit for everyone. We’d rather say that plainly than have someone go through this process and land in the wrong place.

If your primary question is “when is gold going to go up?” — we’re not your best option. Brighton Gold doesn’t forecast prices, time the market, or provide anything that functions as financial advice. No custodian can tell you what gold will do. Any firm that suggests otherwise isn’t being straight with you.

If you’re approaching a Gold IRA as a short-term trade — acquire today, sell when the price moves — the structure works against that goal. Distributions before age 59½ carry tax obligations and potential penalties. It’s built for holding, not rapid movement.

If you want someone to make the financial decision for you — to function as a planner directing your retirement situation — that isn’t what Brighton Gold offers. Our team educates, guides, and supports customers through the process. We don’t direct financial decisions. A licensed financial professional handles that.

Owners still in the evaluation stage may find it useful to start by reviewing the custodians most often considered by Gold IRA owners — a practical comparison frame alongside the vetting steps in this guide.

Frequently Asked Questions About Gold IRA Custodians

What is the difference between a Gold IRA dealer and a custodian?

A dealer sources and sells the physical metals. A custodian holds the IRA account, maintains the transaction records, and handles the required IRS reporting. These are separate functions performed by separate institutions — by design.

Some precious metals dealers maintain referral arrangements with specific custodians. That’s legal — but it doesn’t obligate you to use the referred institution. The custodian relationship is between you and the entity holding your IRA. If any part of that arrangement feels pre-decided without explanation, ask for clarification in writing before you proceed.

Can I choose my own custodian, or does the dealer choose for me?

You choose the custodian. The dealer executes the purchase of your metals and coordinates delivery to the depository. The custodial relationship is between you and the institution holding your IRA.

If a dealer presents a single custodian with no alternatives and no explanation of why, ask directly: is this a requirement, or a suggestion? That answer matters. A requirement with no rationale is worth examining before you sign anything.

What are standard annual custodial fees for a Gold IRA?

The industry benchmark for a flat annual fee is approximately $200–$300 per year. Scaled fees — calculated as a percentage of account value — vary more widely and increase in dollar terms as gold prices rise.

Always request a written, itemized schedule that covers every charge — setup fees, wire fees, transaction fees, distribution fees — not just the headline annual figure. Verbal quotes don’t hold. A written schedule does.

Is my gold safer with a bank or a non-bank trust company?

Both structures can be legitimate. The critical factor is IRS approval — the institution must appear on the IRS Approved Nonbank Trustee list regardless of whether they operate as a bank or a trust company. Institution type matters less than audit compliance, depository partnerships, and documented insurance on stored metals.

What “safer” actually means here: independently audited, held in a Class 3 vault, insured against loss, and legally separated from the custodian’s own balance sheet. Ask for written confirmation of all four before committing to any institution.

What is an SSAE-18 audit and why does it matter for my retirement gold?

SSAE-18 is the audit standard that service organizations use to demonstrate that their internal controls have been independently reviewed. For a custodian holding retirement assets, a current SSAE-18 report means a qualified third party has verified that the custodian’s processes — record-keeping, financial reporting, security protocols — are operating as represented.

Without it, the custodian’s account of how they operate is the only account you have. That’s not enough. Request the most recent report and the name of the auditing firm. Any legitimate custodian provides both promptly. The time it takes to answer is part of the answer.

How do I know if a Gold IRA custodian is IRS-approved?

Search the IRS Approved Nonbank Trustee list directly. The IRS maintains this list and updates it regularly. It includes every institution that has received formal approval to serve as trustee or custodian for IRAs without being a chartered bank.

If the custodian you’re evaluating isn’t on that list, they don’t have the legal authority to hold your IRA assets — regardless of any other credentials, ratings, or claims they present. This is the first check. Run it before any other conversation.

The Bottom Line on Custodian Selection

The right Gold IRA custodian isn’t the one a dealer recommends by default.

It’s the one that is IRS-approved, fee-transparent, independently audited, and willing to put all of it in writing before you commit to anything.

This is the institutional foundation of your entire Gold IRA holding. Not a formality to get through. Not the last piece of the puzzle. The foundation everything else sits on.

We’ve worked with customers who discovered fee surprises years into their holding — owners who accepted the recommendation, assumed the arrangement was standard, and never ran the four-step check. That conversation is much harder than the one before account opening. Asking the right questions doesn’t take long. It takes the willingness to ask them before the ink is dry.

If you’re at the point of choosing a custodian — or reconsidering the one you were pointed toward — a complimentary consultation with Brighton Gold walks through your options specifically. That includes how the No Fee Precious Metals IRA is structured and whether you qualify.

The custodian question gets treated as a footnote in most Gold IRA guides.

It isn’t a footnote. It’s the question that determines the institutional integrity of everything else inside that account — every acquisition, every record, every IRS filing, every distribution.

If you’re working through this decision, or you’ve already opened an account and want a clearer picture of what you’re holding, that’s exactly what a complimentary consultation is for. We’ll walk through IRS approval, fee structure, audit compliance, and depository options together — so you know what you’re committing to before you commit.

See If You Qualify for the No Fee IRA

Getting custodian selection right from the start is far simpler than correcting it later. Most of the owners we work with are glad they asked these questions before they signed.