Here’s the short version: when you retire, you’ve got three main paths for your Gold IRA — take the physical metals directly, liquidate for cash, or transfer the account to a beneficiary.

Each path has different tax implications. Different timelines. Different logistics.

But here’s what matters most: you’re not trapped.

Your gold and silver are accessible. You’ve spent years building a position in physical precious metals — and now you get to decide how and when to access that value.

Most owners don’t realize they can receive the actual coins and bars they purchased. You’re not limited to selling everything and taking cash. Want your Gold American Eagles shipped directly to your door? That’s a real option.

Timing matters, though. The IRS has specific rules about when distributions must begin, how they’re taxed, and what happens if you miss a deadline.

Understanding these rules now — before you reach retirement age — gives you clarity and control over what comes next.

This guide walks through everything: the three distribution paths, current RMD requirements for 2026, tax treatment, physical delivery logistics, and what happens to your Gold IRA if you pass away before taking distributions.

By the end? You’ll have complete clarity on your options.

Understanding Your Three Distribution Options

When you reach retirement age, your Gold IRA opens up three distinct paths.

Each one serves a different purpose — depending on your goals, your tax situation, and what you want to do with the metals you’ve accumulated.

Maybe you want to hold the physical metal yourself. Maybe you need cash. Maybe you’re thinking about passing gold to heirs tax-efficiently.

The decision isn’t just financial. It’s about what makes sense for your life, your family, and your long-term plans.

In-Kind Distribution: Taking Physical Possession

An in-kind distribution means you receive the actual gold, silver, platinum, or palladium — not cash.

The depository ships your coins and bars directly to your home or a secure location you choose.

Why would you choose this? A few reasons stand out:

- Tangible ownership — You’ve held paper claims long enough. Now you can hold the metal itself. Many owners find peace of mind in physically possessing what they’ve built over the years.

- Flexibility after receipt — Once the metals are in your hands, you decide what happens next. Keep them in a home safe. Store them in a private vault. Sell them later at a time you choose. Or gift them to children and grandchildren.

- RMD satisfaction without selling — If you’re required to take a distribution but don’t want to liquidate, an in-kind distribution satisfies the IRS requirement based on the fair market value of the metals you receive.

Here’s how it works:

You contact your custodian and request an in-kind distribution. They coordinate with the depository. The depository prepares your metals for secure, insured shipping.

Most shipments arrive within 5–13 business days.

The metals are valued at fair market value on the day of distribution. That value becomes taxable income for the year — just like a cash distribution would be.

Cash Liquidation: Converting to Dollars

Cash liquidation is straightforward.

Your custodian sells your metals at current market prices. The proceeds come to you as cash — either wired to your bank account or mailed as a check.

This option makes sense when:

- You need liquid funds — For living expenses, medical costs, or other immediate needs

- You’d rather not store metals — Some owners prefer not to deal with securing physical gold at home

- You want to time the market — If prices are favorable, liquidating lets you lock in value

The process is faster than physical delivery. Once your custodian sells the metals, funds typically reach you within 24–48 hours.

One thing to keep in mind — timing matters. Precious metals prices move daily. If you’re liquidating a significant position, you may want to monitor market conditions and coordinate with your custodian on timing.

Beneficiary Transfer: Passing to Heirs

If you don’t need the funds during your lifetime, your Gold IRA can transfer to your named beneficiaries when you pass away.

This is where proper estate planning becomes essential.

The rules changed significantly with the SECURE Act of 2019. Most non-spouse beneficiaries now must empty inherited IRAs within 10 years of the original owner’s death — a major shift from the old “stretch IRA” rules.

Spouse beneficiaries have more flexibility. They can treat the inherited IRA as their own, roll it into their existing IRA, or take distributions based on their own life expectancy.

We’ll cover beneficiary rules in more detail later. For now, know this: who you name as beneficiary and how those designations are structured directly impact how your heirs will be taxed.

RMD Rules for Gold IRAs in 2026

Required Minimum Distributions — RMDs — are the IRS’s way of making sure tax-deferred retirement accounts don’t grow forever without being taxed.

Once you reach a certain age, you must begin withdrawing a minimum amount each year. And paying taxes on it.

Gold IRAs follow the same RMD rules as traditional IRAs. The IRS RMD requirements apply to all tax-deferred retirement accounts — the fact that you’re holding physical metals doesn’t change the withdrawal requirements.

So what age triggers RMDs? And how do you figure out what you owe?

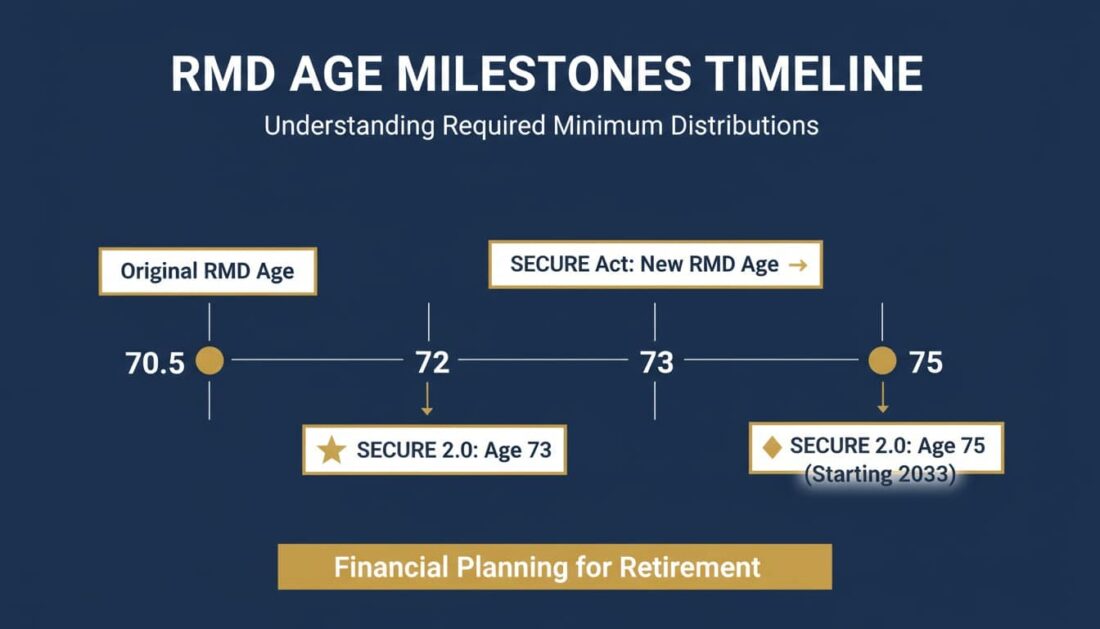

Current RMD Age Requirements

The SECURE Act 2.0 — passed in December 2022 — changed the RMD starting age. Twice, actually.

- Age 73 — Effective January 1, 2023, for folks born between 1951 and 1959

- Age 75 — Effective January 1, 2033, for those born in 1960 or later

If you’re approaching retirement in 2026, here’s what matters:

| Birth Year | RMD Starting Age | First RMD Due |

|---|---|---|

| 1950 or earlier | 72 | Already required |

| 1951–1959 | 73 | Year you turn 73 |

| 1960 or later | 75 | Year you turn 75 |

Your first RMD can be delayed until April 1 of the year following the year you reach RMD age.

But here’s the catch — if you delay, you’ll need to take two RMDs in that second year. That could push you into a higher tax bracket.

How RMDs Are Calculated for Precious Metals

The formula is the same as any traditional IRA.

Divide your account balance as of December 31 of the prior year by your life expectancy factor from the IRS Uniform Lifetime Table. You’ll find those tables in IRS Publication 590-B.

For Gold IRAs, the account balance is based on the fair market value of your metals — not what you paid for them.

Your custodian reports this value to the IRS annually on Form 5498.

Because precious metals have readily available spot prices, calculating fair market value is straightforward. Your custodian multiplies the number of ounces by the spot price on the valuation date.

Quick example: If your Gold IRA holds $100,000 in metals on December 31, 2025, and you turn 75 in 2026, your distribution period from Table III is 24.6. Your 2026 RMD would be approximately $4,065.

What Happens If You Miss an RMD?

The penalty used to be 50% of the amount not distributed. Ouch.

SECURE Act 2.0 reduced this to 25%. Still significant. And it drops to 10% if you correct the mistake within two years.

Here’s what that looks like: If your RMD was $10,000 and you forgot to take it, you’d owe a $2,500 penalty — on top of the income taxes due.

Your custodian is required to notify you of your RMD amount by January 31 each year.

Pay attention to those notices.

Tax Treatment: What You’ll Actually Owe

One of the most common questions we hear: “Are Gold IRA distributions taxed as capital gains or ordinary income?”

The answer surprises most owners.

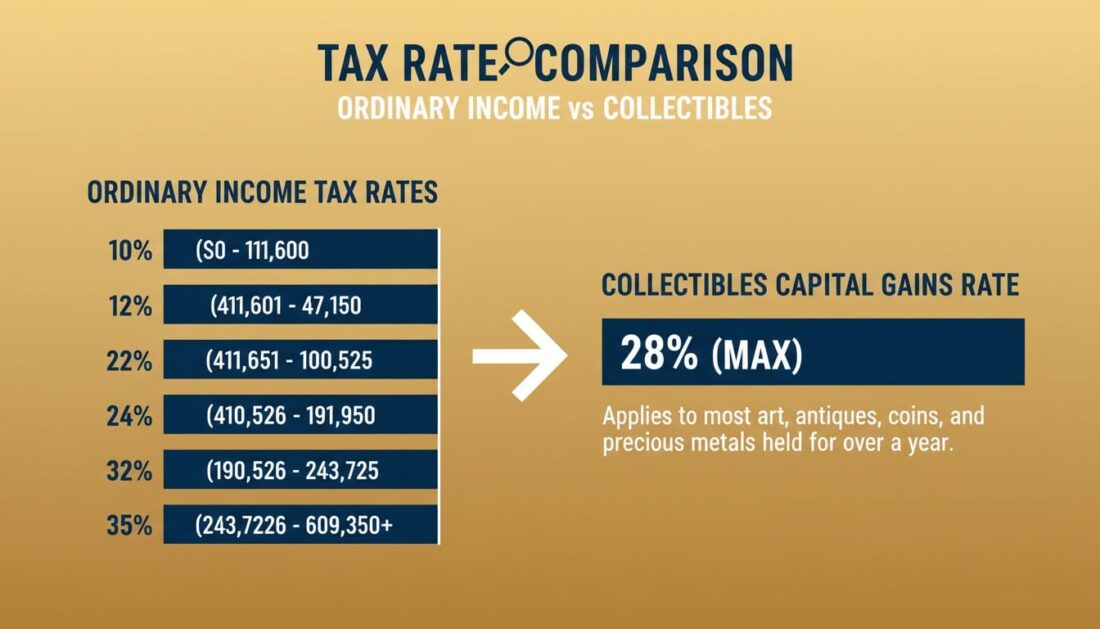

Distributions Are Taxed as Ordinary Income

When you take a distribution from a traditional Gold IRA — whether cash or in-kind — the amount is added to your gross income and taxed at your marginal tax rate.

This is true even though gold held outside an IRA is typically taxed as a “collectible” at a maximum 28% rate.

Inside an IRA, the collectibles capital gains rate doesn’t apply.

For 2026, federal income tax brackets range from 10% to 37% depending on your total taxable income.

| 2026 Tax Bracket | Single Filer Income | Married Filing Jointly |

|---|---|---|

| 10% | Up to $11,925 | Up to $23,850 |

| 12% | $11,926–$48,475 | $23,851–$96,950 |

| 22% | $48,476–$103,350 | $96,951–$206,700 |

| 24% | $103,351–$197,300 | $206,701–$394,600 |

| 32% | $197,301–$250,525 | $394,601–$501,050 |

| 35% | $250,526–$626,350 | $501,051–$751,600 |

| 37% | Over $626,350 | Over $751,600 |

If you’re in the 24% bracket, a $50,000 distribution means approximately $12,000 in federal taxes — plus any state income tax that applies.

Roth Gold IRA Distributions

Roth Gold IRAs work differently.

Because contributions were made with after-tax dollars, qualified distributions are completely tax-free.

To qualify, you must:

- Be at least 59½ years old

- Have held the Roth IRA for at least five years

Roth IRAs also have no RMD requirement during the original owner’s lifetime.

This makes them powerful tools for owners who don’t need the funds immediately — and want to maximize what they pass to heirs.

Early Withdrawal Penalties

Take a distribution before age 59½? You’ll typically owe a 10% early withdrawal penalty on top of ordinary income taxes.

Exceptions exist for disability, qualified medical expenses, first-time home purchase (up to $10,000), and a few other situations outlined by the IRS.

The penalty applies to both cash and in-kind distributions. Taking physical possession of your gold before 59½ is still considered a distribution.

Physical Delivery: How It Actually Works

Taking physical delivery of your precious metals isn’t complicated. But it does require coordination.

Here’s what to expect when you request an in-kind distribution.

Step-by-Step Process

The process breaks down into five steps:

- Step 1: Contact your custodian — Submit a distribution request form specifying that you want physical metals. Indicate which metals and quantities you want to receive.

- Step 2: Verify fair market value — Your custodian calculates the value based on current spot prices. This determines your taxable income for the distribution.

- Step 3: Coordinate with the depository — Your custodian notifies the depository. They prepare your shipment, calculate shipping and insurance fees, and contact you to arrange delivery.

- Step 4: Confirm shipping details — Most depositories use secure carriers like UPS or FedEx with full insurance. You’ll receive tracking information and delivery confirmation requirements.

- Step 5: Receive your metals — Shipments typically arrive within 5–13 business days. Inspect the package carefully and verify contents match your request.

What to Know About Shipping and Insurance

Reputable depositories ship precious metals with full insurance against loss or damage.

Standard practice includes:

- Signature required — You or an authorized person must sign upon delivery

- Real-time tracking — Monitor your shipment from depository to door

- Discrete packaging — No external markings indicating contents

- Full insurance — Coverage for the shipment’s entire value during transit

Shipping fees vary by depository and shipment size. Expect to pay these separately — either from your IRA (if funds are available) or by credit card.

After You Receive Your Metals

Once the metals are in your possession, they’re yours to manage however you choose.

Common next steps:

- Home storage — A quality safe rated for valuables, preferably fireproof and securely anchored

- Private vault storage — Non-IRA depository services for continued professional storage

- Hold or sell — Keep indefinitely or sell to a dealer when you’re ready

The metals are no longer part of your IRA after distribution. Any future appreciation or loss happens outside the tax-advantaged structure.

Beneficiary Rules and Inheritance

What happens to your Gold IRA if you pass away before taking all distributions?

The answer depends on who inherits — and when you passed away.

This is where things get complicated. But it’s also where proper planning makes the biggest difference.

Spouse Beneficiaries

Surviving spouses have the most flexibility.

Options include:

- Treat it as your own — Roll the inherited IRA into your own IRA and follow standard distribution rules based on your age

- Remain as beneficiary — Keep the inherited IRA separate and take distributions based on your life expectancy

- Take a lump sum — Withdraw everything at once (triggers full taxation in that year)

Spouses who are significantly younger than the deceased owner may benefit from remaining as beneficiary rather than rolling over. This can delay RMD requirements.

Non-Spouse Beneficiaries: The 10-Year Rule

The SECURE Act of 2019 eliminated the “stretch IRA” for most non-spouse beneficiaries.

If you inherit a Gold IRA from someone who died after December 31, 2019, you generally must empty the account within 10 years of the owner’s death. The IRS beneficiary distribution rules outline exactly how this works.

This applies to:

- Adult children

- Grandchildren

- Siblings

- Friends

- Most trusts

Important: If the original owner died after reaching RMD age, you must also take annual RMDs during those 10 years — not just empty the account by year 10.

The IRS finalized this interpretation in 2024. Penalties for missed RMDs began applying in 2025.

Eligible Designated Beneficiaries

Certain beneficiaries can still stretch distributions over their life expectancy:

- Surviving spouse

- Minor children of the account owner (until age 21, then the 10-year rule kicks in)

- Disabled individuals (as defined by the IRS)

- Chronically ill individuals

- Individuals not more than 10 years younger than the deceased owner

If you plan to leave your Gold IRA to a child or grandchild, understand that the 10-year rule will likely apply.

They’ll need to withdraw — and pay taxes on — the entire account within a decade.

For owners concerned about legacy planning, working with a qualified estate planning attorney is essential. The beneficiary designation on your IRA supersedes your will.

If those designations don’t align with your wishes? The wrong person could inherit.

Tax Planning Strategies for Distributions

Smart distribution planning can significantly reduce your lifetime tax burden.

Here’s what many owners do to manage their Gold IRA distributions effectively.

Spreading Distributions to Manage Tax Brackets

Rather than taking large lump-sum distributions, consider spreading withdrawals across multiple years.

Why? To stay within lower tax brackets.

If your ordinary income from other sources puts you in the 22% bracket, taking a distribution that pushes you into the 24% bracket costs you an extra 2% on every dollar above the threshold.

Work backward from your target income level. Calculate how much “room” you have in your current bracket. Then plan distributions accordingly.

This takes some coordination — but the tax savings add up.

Qualified Charitable Distributions (QCDs)

If you’re 70½ or older and charitably inclined, QCDs offer a powerful option.

You can donate directly from your IRA to a qualified charity — up to $108,000 per year in 2025 (indexed for inflation).

The donation satisfies your RMD but isn’t included in your taxable income.

For owners who don’t need RMD funds, QCDs effectively eliminate the tax on required distributions while supporting causes they care about.

One catch: QCDs must be made directly from the IRA to the charity. You can’t take a distribution, deposit it, and then write a check.

Roth Conversions Before RMDs Begin

Converting traditional IRA funds to a Roth before you reach RMD age can reduce future required distributions — and provide tax-free growth going forward.

The conversion is taxable. You pay income tax on the converted amount.

But once funds are in a Roth, they grow tax-free, distributions are tax-free, and there are no lifetime RMDs.

This strategy works best for owners who:

- Have years before RMDs begin

- Expect to be in a higher tax bracket later

- Want to leave tax-free assets to heirs

- Have other funds available to pay the conversion taxes

If you’re evaluating gold IRA advantages and disadvantages, Roth conversion timing is worth discussing with your tax professional.

Partial In-Kind Distributions

You don’t have to choose between all cash or all physical metal.

Partial distributions let you:

- Take some metals in-kind for personal possession

- Liquidate others for cash to cover taxes or living expenses

- Keep the remainder growing in your IRA

This flexibility lets you access your wealth without liquidating positions you want to hold.

When understanding gold IRA fee structures, factor in how partial distributions might affect your ongoing custodial costs.

Avoiding Common Distribution Mistakes

We’ve seen owners make the same mistakes over and over.

Here’s what to watch for — so you don’t leave money on the table or trigger penalties you could’ve avoided.

Mistake #1: Forgetting RMDs Entirely

It sounds obvious. But it happens more than you’d think.

Owners get busy. They assume their custodian will handle it. They forget December 31 is a hard deadline.

The penalty? 25% of what you should’ve withdrawn.

Solution: Set calendar reminders. Review your RMD notice when it arrives in January. Don’t wait until December to act.

Mistake #2: Taking Too Much at Once

Some owners think “I’ll just take it all this year and be done with it.”

The problem? A large lump-sum distribution can push you into a much higher tax bracket — sometimes costing tens of thousands in unnecessary taxes.

Solution: Spread distributions across multiple years when possible. Work with a tax professional to model different scenarios.

Mistake #3: Outdated Beneficiary Designations

Life changes. Marriages. Divorces. Deaths.

Your IRA beneficiary designation might still list an ex-spouse. Or a deceased parent. Or no one at all.

The designation on file with your custodian supersedes your will. If it’s outdated, your heirs could face expensive legal battles — or the wrong person inherits entirely.

Solution: Review your beneficiary designations annually. Update them whenever your life circumstances change.

Mistake #4: Not Coordinating Across Accounts

If you have multiple IRAs, you can aggregate RMDs.

That means you can calculate the total RMD across all your traditional IRAs — then take the full amount from whichever account makes the most sense.

Some owners don’t realize this. They take RMDs from each account separately, missing opportunities to be strategic.

Solution: Look at all your IRAs together. If you want to preserve your Gold IRA holdings, take your RMD from a different account with more liquid assets.

Mistake #5: Ignoring State Taxes

Federal taxes get most of the attention. But state income taxes vary widely.

Some states don’t tax retirement distributions at all. Others tax them fully.

If you’re considering relocating in retirement, state tax treatment of IRA distributions should factor into your decision.

Solution: Understand how your state taxes retirement income. If you’re identifying safe gold IRA practices, include tax planning as part of your overall strategy.

Frequently Asked Questions

Can I take physical gold out of my IRA when I retire?

Yes. Once you reach age 59½, you can request an in-kind distribution of your physical gold, silver, platinum, or palladium. The metals ship directly to you from the depository. The fair market value on the distribution date becomes taxable income — but you avoid the 10% early withdrawal penalty that applies before 59½.

What age do I have to start taking distributions from a Gold IRA?

For 2026, the RMD starting age is 73 if you were born between 1951 and 1959. If you were born in 1960 or later, your RMD age is 75 (effective in 2033). Your first RMD is due by April 1 of the year following the year you reach RMD age. Subsequent RMDs are due by December 31 each year.

Are Gold IRA distributions taxed as capital gains or ordinary income?

Ordinary income — not capital gains. Even though gold held outside an IRA is typically taxed as a collectible at a 28% maximum rate, distributions from a traditional Gold IRA are added to your gross income and taxed at your marginal rate. That could be higher or lower than 28% depending on your total income.

What is the penalty for missing a Gold IRA RMD in 2026?

The penalty is 25% of the amount that should have been distributed. If you correct the mistake within two years — by taking the missed distribution and filing Form 5329 — the penalty drops to 10%. Before SECURE Act 2.0, the penalty was 50%.

How do I calculate the fair market value of my gold for a distribution?

Your custodian handles this. They multiply the number of ounces of each metal by the spot price on the valuation date. For RMD calculations, the December 31 year-end value is used. For distributions, the spot price on the distribution date determines the taxable amount. This gets reported to the IRS on Form 5498.

Can I roll over my Gold IRA into a standard IRA after I retire?

A Gold IRA is already a type of self-directed IRA. You can transfer funds between custodians — but you’d need to liquidate the physical metals if moving to a custodian that doesn’t support precious metals. If done as a trustee-to-trustee transfer of the proceeds, it’s not a taxable event. For more on how transfers work, see our guide on rolling over retirement funds to gold.

What happens to my Gold IRA if I pass away before taking distributions?

Your Gold IRA transfers to your named beneficiary. Spouse beneficiaries can treat the IRA as their own or take distributions based on their life expectancy. Most non-spouse beneficiaries must empty the account within 10 years under SECURE Act rules. Annual RMDs may also be required during those 10 years if you died after reaching RMD age.

How long does it take to receive physical gold after requesting a distribution?

Typically 5–13 business days from when you submit your request. This includes custodian processing time, depository preparation, and shipping. Your depository’s location, shipping method, and whether you’re taking a partial or full distribution can all affect timing.

Taking the Next Step

Your Gold IRA isn’t a one-way street.

The metals you’ve accumulated are accessible. You have real options for how to use them in retirement.

Whether you want physical gold shipped to your door, cash deposited in your bank, or a tax-efficient transfer to your children — the path forward starts with understanding the rules and planning ahead.

The owners who get the best outcomes? They’re the ones who think through these decisions before reaching RMD age.

They know their options. They’ve considered the tax implications. They’ve worked with professionals who understand both precious metals and retirement regulations.

If you’re still weighing your options — or if you’ve been putting off this conversation — now’s the time to get clarity and control over what’s next.

Precious metals may appreciate, depreciate, or remain unchanged in value. Brighton does not provide financial, legal, or tax advice. Consult your CPA or tax professional for guidance specific to your situation.

Ready to discuss your distribution options?

If you’re thinking “this all makes sense, but I want to talk through my specific situation,” you’re not alone.

Most customers we work with felt the same way before they realized how straightforward the process can be with the right guidance.

That’s why we offer a complimentary consultation to walk you through your options — including our No Fee Precious Metals IRA, which covers custodial fees for the lifetime of the account on qualified purchases.

We’ll show you exactly:

- How the No Fee IRA works and whether you qualify

- The difference between U.S.-minted coins and foreign alternatives

- What to expect from the distribution and delivery process

- How to structure your beneficiary designations for tax efficiency

- What ongoing support looks like after your purchase

Learn About the No Fee IRA — no obligation, just actionable insights you can use whether you work with us or not.

You’ve spent years building this position. Let’s make sure you access it the right way.