Why a No-Fee IRA for Life Is the Best Choice for Retirees?

A No-Fee IRA for life is the best choice for retirees because it eliminates the one cost most dealers never highlight upfront — the recurring annual fees that quietly compound against your savings for as long as your account remains open.

The standard precious metals IRA model charges between $150 and $300 in annual administration fees, plus $100 to $300 in annual storage fees. Combined, that’s $250 to $600 per year — year after year, regardless of whether your metals gained or lost value. Over 20 years, that’s a minimum of $5,000 and potentially $12,000 or more paid directly out of your retirement account in fees alone.

A No Fee Precious Metals IRA eliminates those costs entirely — for the lifetime of the account — on qualified purchases. Not for a promotional window. Not for the first year. For life.

Financial industry research consistently shows that even modest annual fees — in the range of 1 to 2 percent — can significantly erode a retirement account’s value when compounded over 20 years. The math doesn’t change because the product is physical gold instead of equities. Fees are fees. And $400 per year is $400 per year that isn’t staying in your account, holding its value, or passing to your heirs.

For retirees managing Required Minimum Distributions — now triggered at age 73 under current IRS rules — every dollar retained in the account matters. Eliminating recurring fees keeps more of your holdings in your hands, and less in the hands of an administrative system built around institutional convenience rather than owner outcomes.

This article covers how standard gold IRA fees are actually structured, what the No-Fee model means in concrete terms, the legacy math over 10 to 20 years, and who this type of account is — and isn’t — designed for.

The Real Cost of Gold IRA Fees in Retirement

The fee question doesn’t come up at the front of most precious metals IRA conversations. It shows up later — after the account is open, after the metals are purchased, after the first annual statement arrives.

That timing isn’t accidental.

Understanding gold IRA fee structures before anything is signed is the step most dealers don’t rush you toward. Here’s why that matters — and what the standard model actually looks like when you examine it directly.

How the Standard Gold IRA Fee Model Is Built

Most precious metals IRAs carry at least three separate recurring charges. They don’t always get explained together. They don’t always show up on the same line of the same document. But they add up — every year — for as long as the account stays open.

- Annual account administration fee ($100–$300) — Charged by the custodian for maintaining the self-directed IRA. This fee applies regardless of account activity, account size, or price movement. The account can sit unchanged for 12 months and the fee still runs.

- Annual storage fee ($100–$300) — Charged by the depository for physically holding your metals. Some depositories use a flat fee structure. Others charge a percentage of total account value — which means the fee grows as your metals grow.

- Setup or account opening fee ($50–$250) — A one-time charge applied at account establishment. Not universal, but common enough to plan for.

- Transaction fees ($25–$100 per trade) — Applied each time metals are purchased or sold within the account. These stack on top of the annual charges — they don’t replace them.

Not every custodian charges all four. But most charge at least the first two — and the first two alone can run $200 to $600 per year, every year, for the lifetime of the account.

| Fee Type | Typical Annual Range | Standard Model | Brighton No-Fee Model |

|---|---|---|---|

| Administration Fee | $100–$300 | Yes — annual | $0 for life |

| Storage Fee | $100–$300 | Yes — annual | $0 for life |

| Setup Fee | $50–$250 (one-time) | Common | Often waived |

| Transaction Fee | $25–$100 per trade | Common | Varies by transaction |

Why the Standard Fee Model Fails Long-Term Owners

Here’s the honest version of how the standard fee model works: it runs whether or not your metals moved.

Whether or not you made a transaction. Whether or not the account grew.

The clock doesn’t pause for flat markets. It doesn’t adjust when things get rough. It just runs — quietly, automatically, every year — until the account is closed or transferred somewhere else.

The real cost isn’t only what the fees charge. It’s what that money stops being able to do inside the account.

FINRA’s investor education guidance makes this arithmetic plain: even modest annual fees compound against an account over a long holding period. A $400 annual drag over 20 years isn’t $8,000 gone. It’s $8,000 gone — plus every dollar that money could have represented had it stayed in the account the whole time.

The model isn’t broken because the charges are outrageous. It’s broken because the fees are invisible to most customers until the account is already open — and by then, the commitment is already made.

Brighton Gold’s view is direct: recurring annual fees are a structural problem, not a necessary cost of holding physical metals. The No Fee Precious Metals IRA for the lifetime of the account was built to eliminate that problem — not reduce it, not discount it for a promotional period, but eliminate it entirely on qualified purchases.

That’s a different design than most of this industry operates on.

What “No Fee for Life” Actually Means

“No fee” is one of the more loosely used phrases in the precious metals IRA space. It shows up as a first-year rate. It shows up as a promotional window with an expiration date. It shows up in terms that quietly convert back to standard fees after a grace period the customer may not have registered.

Brighton Gold’s No Fee Precious Metals IRA for the lifetime of the account isn’t any of those things.

What “Qualified Purchase” Means — and Why It Matters

The fee waiver applies to qualified purchases. That’s the condition — and it’s the only condition.

- Qualified accounts carry permanent zero-dollar administration and storage fees for the lifetime of the account. Not a discounted rate. Not a rebate applied somewhere else in the structure. The fees are gone — and they stay gone.

- There’s no expiration date on the waiver. No grace period. No conversion to market-rate fees after year one. The commitment holds for the full duration of the ownership relationship.

- The complimentary consultation is where we walk through whether you qualify, what the account structure looks like, and what the process involves — before anything is signed or decided.

We believe that transparency here matters. A business model built around long-term customer value doesn’t need fine print to survive scrutiny. Identifying safe gold IRA practices starts with this: clear terms that hold up when you read them directly, without a deadline attached to pressure the decision.

| Feature | Standard Custodial Model | Brighton No-Fee Model |

|---|---|---|

| Administration fee | $100–$300 per year | $0 — lifetime |

| Storage fee | $100–$300 per year | $0 — lifetime |

| Fee duration | Ongoing / permanent | Eliminated — permanently |

| Time-limited offer | N/A | No — this isn’t a promotion |

| Qualification required | No | Yes — qualified purchase |

Why Most Dealers Can’t — or Won’t — Match This

There’s a reasonable question underneath this: if zero fees are sustainable, why doesn’t everyone offer them?

The answer is structural. The annual fee model isn’t just industry convention — it’s a revenue line built into how most dealers operate after the initial acquisition is complete.

Per SEC regulatory guidance on custodial arrangements, charging for account maintenance and safekeeping is legal, standard, and normalized across the industry. Most dealers have no structural reason to step away from a recurring revenue stream that runs automatically year after year.

Brighton Gold built a different model.

The No Fee IRA isn’t a promotion. It’s a structural commitment to long-term customer value that most competitors can’t or won’t replicate.

The assumption that all precious metals dealers operate on the same basic terms — and that the difference is just in which coins they carry — is worth examining directly. It isn’t true. And for customers holding a 10 to 20-year account, the difference between “fee-lite” and “fee-zero” isn’t cosmetic.

The fee structure is the relationship. Ours is built to create value for the owner across the full life of the account — not extract from it annually while they wait.

The Legacy Math — How Zero Fees Change the Retirement Calculation

The math on fee elimination isn’t complicated. It’s just not something most dealers put in front of you before the account is opened.

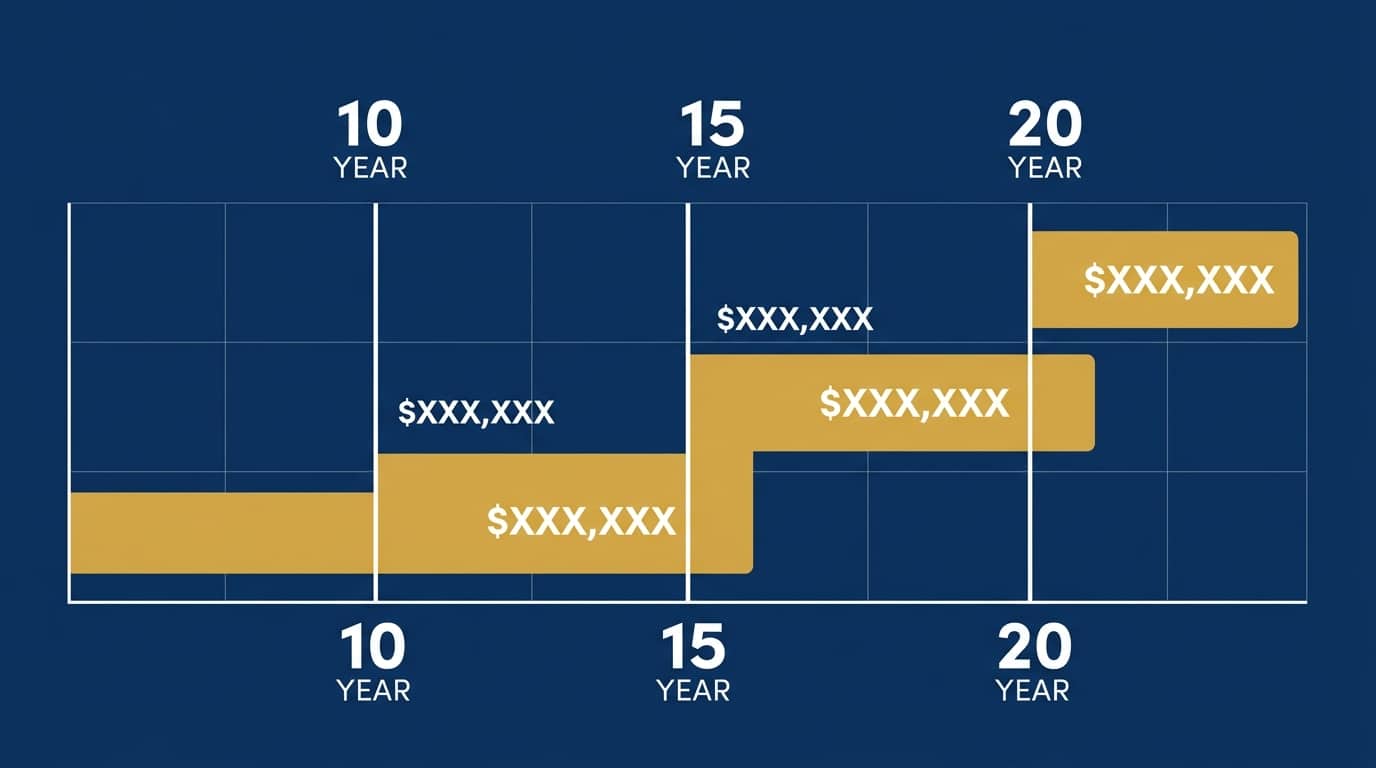

Here’s what $400 per year — a conservative figure for combined administration and storage fees — actually costs across a 10, 15, and 20-year retirement holding period. Not projections. Arithmetic.

Cumulative Fee Drag vs. Zero-Fee Retention

| Holding Period | Standard Model ($400/yr) | No-Fee Model | Retained by Owner |

|---|---|---|---|

| 10 years | $4,000 paid out | $0 | $4,000 |

| 15 years | $6,000 paid out | $0 | $6,000 |

| 20 years | $8,000 paid out | $0 | $8,000 |

| 20 years ($600/yr avg) | $12,000 paid out | $0 | $12,000 |

These numbers assume flat fees — no increases, no rate changes. That’s the conservative scenario.

In reality, storage fees tied to account value don’t stay flat. They rise as the value of gold rises. With gold at current price levels per World Gold Council market data, accounts with meaningful holdings face proportionally higher percentage-based storage costs every year the account is open.

Fee elimination isn’t just a dollar-for-dollar trade. It’s also protection against that escalation — the part of the standard model most dealers don’t put on paper for you until after the account is funded and the relationship is already established.

What does $8,000 retained over 20 years mean in real terms? It means $8,000 that stayed in the account — still representing an ownership position in physical metals — rather than $8,000 paid out in overhead that produced no ownership benefit. Passed to a beneficiary, it’s $8,000 that exists rather than $8,000 that was quietly extracted, one annual charge at a time.

That’s not a marketing claim. That’s arithmetic applied to a fee structure most customers never see side by side.

RMDs, Tax Planning, and the No-Fee Advantage

Under current IRS Publication 590-B rules, Required Minimum Distributions from retirement accounts — including Gold IRAs — begin at age 73. The amount is calculated each year against account value and IRS life expectancy tables.

Here’s how that intersects with the No-Fee model:

- Every dollar paid in fees reduces the account base from which RMDs are calculated. A smaller account value means a smaller distribution base — and those dollars aren’t being distributed. They’re gone, paid out in administrative overhead.

- No-Fee accounts retain more year over year. More of your holdings stay intact through the holding period. That means a larger ownership position at distribution time — and more flexibility in how the distribution process unfolds.

- Distribution from a Precious Metals IRA — whether through liquidation or in-kind transfer — runs through custodian coordination. A clean, no-fee account structure reduces the administrative friction around that process.

For those working through executing a precious metals IRA rollover from an existing 401(k) or traditional IRA — starting with a no-fee structure from the opening of the account captures every year of that advantage from day one.

Brighton Gold does not provide financial, tax, or legal advice. For the ordinary tax liability on distributions from a Precious Metals IRA, work with a CPA or tax professional who can account for your specific situation.

Who This Account Is For — and Who It Isn’t

The No Fee Precious Metals IRA isn’t for everyone. That’s worth saying before anything else.

Most of the resources at the Brighton Gold Learning Center are built around that kind of upfront clarity — the process, the expectations, and who the relationship actually works for — before any decision gets made.

The Right Owner for a No-Fee Precious Metals IRA

Customers who get the most from this structure share a few consistent characteristics.

- They’re planning to hold — not flip. The lifetime fee waiver compounds in value the longer the account stays open. Customers intending to hold metals for 10 to 20 years capture the full benefit of zero annual costs. Customers expecting to liquidate within a few years see less of that advantage materialize.

- They want a clean, simple ownership structure. A well-structured precious metals account shouldn’t require constant attention — or produce annual fee invoices. You acquire the metals. They’re held at an IRS-approved depository. That’s where the relationship lives. Without a recurring cost attached to it every year.

- They’re building something to pass on. The No-Fee model appeals to owners thinking about legacy — not short-term price movement. An extra $8,000 to $12,000 retained over 20 years doesn’t disappear into overhead. It stays in the account until it passes to whoever you’ve named.

- They want to understand understanding gold IRA storage rules — including what it costs, where the metals sit, and what it means when that cost is zero.

- They’re drawn to U.S.-minted products. Customers choosing IRS-approved gold coins like the Gold American Eagle appreciate that provenance, purity, and long-term liquidity matter — and that our concierge approach includes guidance on exactly those decisions.

This Isn’t the Right Account for the Speculator

One thing worth being direct about: Brighton Gold isn’t the right fit for every customer — and the No Fee IRA isn’t built to be.

If the first thing you want to know is where gold prices are heading over the next six months — this account isn’t built around that question.

Brighton Gold doesn’t forecast prices. We don’t time markets. We don’t make recommendations about when to buy or sell based on where prices might move next. That’s not a limitation — it’s an honest description of what we do and don’t do.

If the goal is a trading account — acquiring metals today, selling when the price shifts, cycling positions based on short-term price movement — the No Fee IRA’s long-term ownership structure isn’t designed for that. The qualified purchase requirement and the ownership orientation both exist specifically to serve customers who plan to hold something tangible over time. Not customers looking to speculate on near-term price activity.

Brighton Gold also isn’t the right fit for the customer who leads every conversation with spread and moves on if someone else’s number is lower. We’re not the cheapest option in this market. The value is in the structure, the service, and a fee model that works in your favor for the full life of the account — not just the day it opens.

Precious metals may appreciate, depreciate, or remain unchanged. We say that directly — every time — because customers who stay with us went in with that expectation already set.

If clarity, stability, and an ownership experience without annual fees attached sounds like what you’re after — we’re worth a conversation.

Frequently Asked Questions

How much can a retiree save with a No-Fee IRA for life?

Most customers in a standard custodial account pay between $200 and $600 per year in combined administration and storage fees. Over a 20-year retirement horizon, that’s $4,000 to $12,000 paid directly out of the account — and that’s assuming flat fees.

If storage fees are percentage-based and tied to account value, the total climbs higher as the underlying value of your metals grows. Brighton Gold’s No Fee Precious Metals IRA eliminates those costs entirely on qualified purchases — so at $400 per year retained over 20 years, that’s $8,000 that stays with the owner instead of covering overhead that produces no ownership benefit. For a full breakdown of the charges most dealers don’t put front and center, the guide to what hidden fees in a gold IRA actually look like is worth reviewing before any account is opened.

Is “No Fee for Life” too good to be true?

That’s a fair question — and it deserves a direct answer.

The no-fee model works because Brighton Gold’s business isn’t structured around the annual fee stream. The standard industry model treats custodial fees as a revenue line that runs indefinitely. We treat the long-term ownership relationship as the value instead — which means the fee structure is built to support the customer over time, not extract from them year after year.

The waiver applies to qualified purchases. That’s the full condition — no expiration, no conversion to market-rate pricing after a grace period, no fine print clause designed to walk it back. Identifying safe gold IRA practices starts with exactly this kind of direct evaluation: are the terms clear, are they consistent, and does the company’s record support them? Brighton Gold has been in operation since 2012, holds an A+ BBB rating, and maintains a AAA BCA rating. The no-fee commitment isn’t new — it’s the model the company was built around.

Does the No-Fee IRA include storage costs at the depository?

Yes. Both administration and storage fees are waived under the No Fee Precious Metals IRA for the lifetime of the account on qualified purchases.

The depository holds Brighton Gold customer metals in an IRS-approved, insured facility. The storage fee that most custodians charge annually — typically $100 to $300 — is part of what the No-Fee model eliminates. Not a reduced rate. Not a credit applied elsewhere. Zero. For the life of the account.

The mechanics of how depository storage actually works — segregated versus commingled options, insurance coverage, and how distribution is handled when the time comes — are worth understanding before any account is opened. The details matter more than most customers realize until they need them.

How do 2026 RMD rules affect a No-Fee Gold IRA?

Under IRS Publication 590-B, Required Minimum Distributions from a Gold IRA begin at age 73. The RMD amount is calculated each year based on account value and IRS life expectancy tables — the same methodology that applies to traditional IRAs.

The No-Fee advantage runs through that calculation directly. A standard model charging $400 annually reduces the account base before distributions begin — those dollars are gone, not distributed. The No-Fee model retains them, which means a larger ownership position at distribution time and more flexibility in how the process unfolds. Brighton Gold does not provide financial or tax advice. Work with a CPA or tax professional on the ordinary tax liability associated with distributions from your Precious Metals IRA.

What defines a “qualified purchase” for the lifetime fee waiver?

A qualified purchase refers to a metals acquisition that meets Brighton Gold’s account threshold at the time the IRA is opened. The specific threshold is discussed during the complimentary consultation — because it depends on the type of rollover, transfer, or direct purchase being executed.

The clearest path to that answer is a direct conversation. No obligation. No sales process running in the background. Just a clear picture of whether the account structure makes sense for where you are.

Is a No-Fee IRA better for larger or smaller retirement accounts?

Both benefit — but the math favors larger accounts most when storage is percentage-based rather than flat.

For smaller accounts, a flat fee of $400 per year still represents meaningful annual overhead relative to account size. Eliminating it entirely means 100% of the holdings stay in the account — nothing leaves to cover administration. For larger accounts with percentage-based storage, the advantage compounds more significantly. A 0.5% to 1% annual fee on a $150,000 account runs $750 to $1,500 per year — and climbs higher as gold’s value rises. The No-Fee model removes that escalation permanently, which is why the advantage grows in absolute dollar terms the larger and longer-held the account is.

How does this compare to just holding physical gold outside an IRA?

The comparison between a No-Fee IRA and direct physical ownership outside a retirement account comes down to account structure, IRS compliance, tax treatment, and how you intend to manage legacy.

Home storage of IRA-designated metals isn’t permitted under IRS rules — attempting it triggers distribution treatment and potential tax penalties. The question of which makes more sense — a Gold IRA or physical gold for retirement protection depends on your tax situation, your ownership goals, and how you plan to handle distribution when the time comes. What the No-Fee model does is remove cost as a variable in that comparison — which often simplifies the decision more than people expect.

The Takeaway: The Fee Structure Is the Relationship

Here’s what this comes down to: every precious metals IRA in this market holds metals at an IRS-approved depository. The metals are similar. The storage facilities are similar. What’s not similar — and what most customers don’t examine closely enough before opening an account — is the fee structure they’re agreeing to carry for the next 10 to 20 years.

The standard model bills you every year. It bills you when the metals hold flat. It bills you when the market moves against you. It bills you until the account closes — regardless of what the account did or didn’t do in the years it was open.

The No Fee Precious Metals IRA for the lifetime of the account is built on a different premise entirely. The fee isn’t deferred. It isn’t discounted. It isn’t promotional. It’s eliminated — because a model built around the long-term owner shouldn’t extract from them annually while they wait.

Precious metals may appreciate, depreciate, or remain unchanged. That’s the honest answer to anyone who asks about price direction — and it’s the answer Brighton Gold leads with, every time. What the No-Fee model removes from the equation isn’t market uncertainty. It’s the one cost that was guaranteed to run against you regardless of what the market did.

Over 20 years, that’s $8,000 to $12,000 that stays where it belongs. In the account. With the owner. Available to pass on.

That’s the case for lifetime fee elimination. Not as a discount. As a design principle — and the only model Brighton Gold offers.

If you’ve been evaluating precious metals IRA options and the fee question keeps coming back — you’re asking the right question.

Most custodial models are built around ongoing fee revenue. Brighton Gold’s No Fee Precious Metals IRA was built around something different: that the relationship with a long-term owner should create value across the full life of the account — not extract from it annually while the metals sit.

A complimentary consultation walks you through the qualification threshold, the account structure, and whether the No-Fee IRA fits your situation — based on what you’re holding, what you’re protecting, and what ownership actually looks like for you.

The fee question doesn’t have to stay open. The clearest way to resolve it is a direct conversation — no obligation, no pressure, just the most complete picture Brighton Gold can give you of what this looks like for your retirement.