What Are the IRS Rules for IRA-Approved Gold?

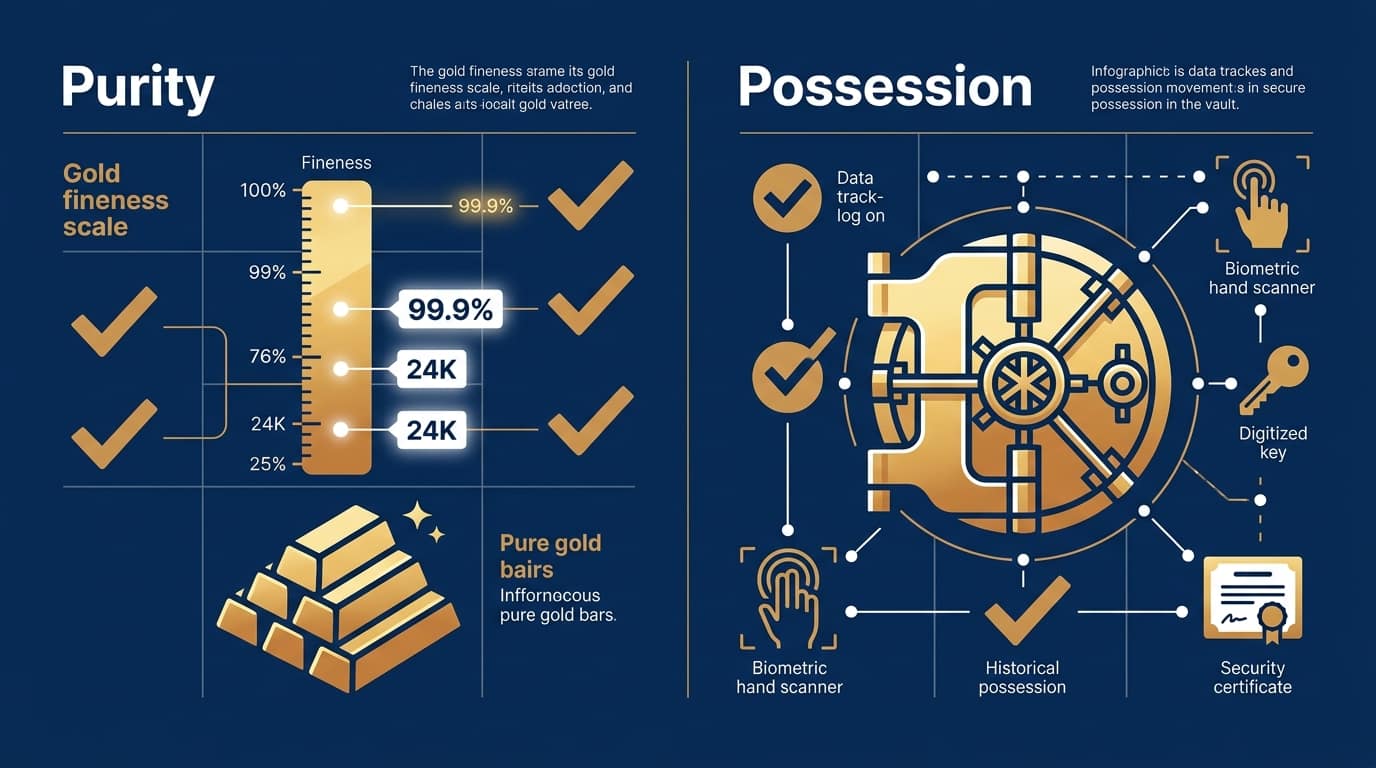

The IRS rules for IRA-approved gold come down to two requirements. First, purity — most gold products must meet a minimum fineness of .995 (99.5% pure), as established under IRC Section 408(m)(3). Second, possession — the gold must be held by an IRS-approved trustee or custodian and stored at a licensed depository. If either requirement fails, the IRS treats the metals as a taxable distribution of the account.

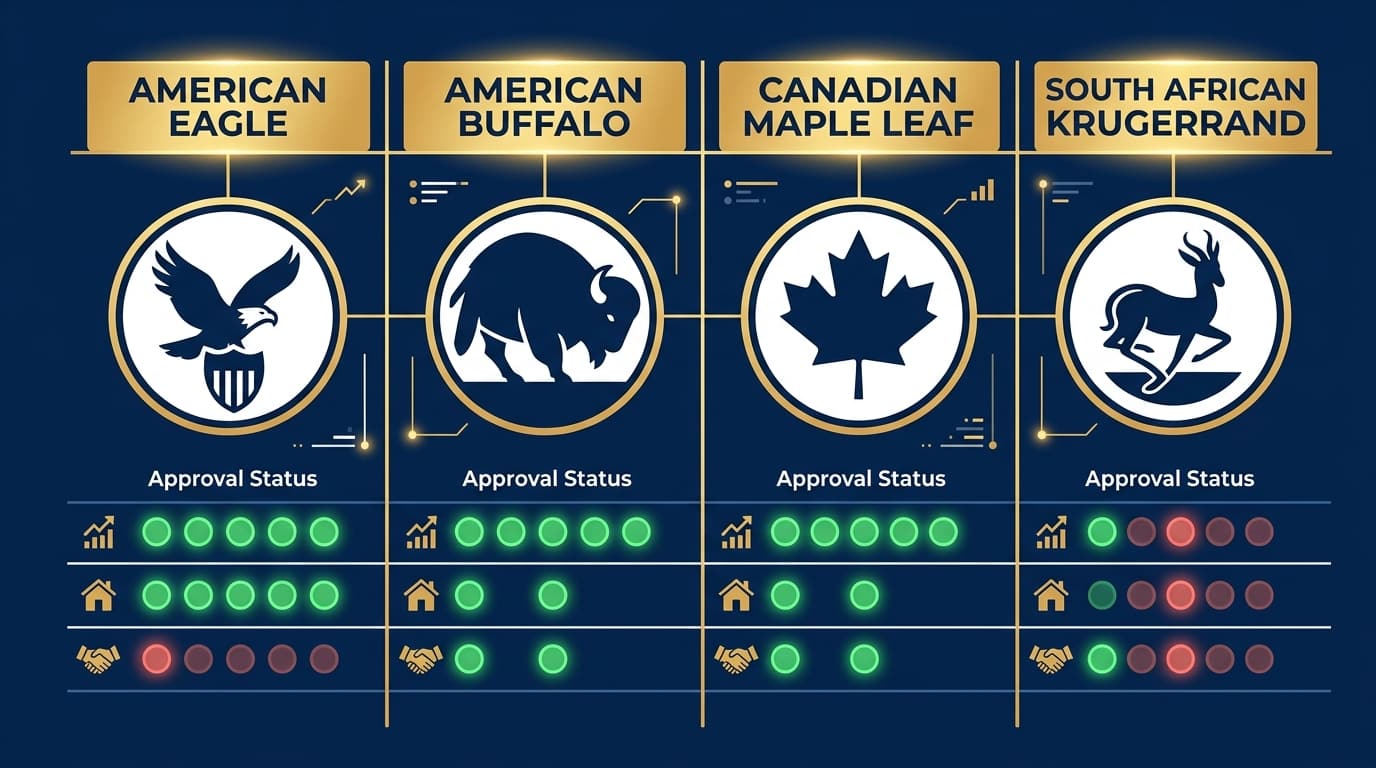

There is one notable exception to the purity floor: the American Gold Eagle, which is approved at 91.67% purity (22 karat) because it’s a U.S. legal tender coin specifically exempted by statute. No other 22-karat gold coin receives that same exemption.

The rules aren’t complicated. What makes them feel complicated is the way they’re often presented — buried in fineness charts, custodian requirements, and storage logistics that arrive all at once without context. Strip that away and what you have is this: buy IRS-eligible gold, hold it in an approved account, and store it at an authorized depository. That’s the framework.

This article covers what that framework actually looks like in practice. You’ll learn which coins and bars qualify — and why — which products don’t meet the standard, what “trustee possession” means and why it matters as much as purity, and what happens when the wrong coin ends up in an IRA.

The IRS rules haven’t changed at their core. What has changed is how much confusion surrounds them — and how much of that confusion is avoidable.

The IRS Standard: Two Things That Determine IRA Eligibility

Here’s what most people get wrong from the start — they go looking for a list when what they actually need is a framework.

The list matters. It’s further down. But the framework is what prevents a costly mistake. When something goes wrong — wrong coin, wrong storage arrangement — the framework tells you why. The list just tells you that it happened.

Two criteria determine eligibility. Both are required. Neither is flexible.

Criterion One: Purity

The number is .995.

That’s the minimum fineness — 99.5% pure gold — the IRS requires for most gold bullion and coins, as specified in IRS Publication 590-A. It exists to draw a clean line between two different categories: metal you’re acquiring for its gold content, and metal whose value comes from its age, rarity, or historical significance.

Those two categories are treated very differently. And you need to know which one you’re in before anything moves.

The one exception is the American Gold Eagle — 22 karat, 91.67% pure. Congress carved it out specifically in the Taxpayer Relief Act of 1997. No other 22-karat coin got the same pass. A Krugerrand is also 22 karat. It doesn’t qualify.

- Gold bullion bars (.995 minimum fineness) — Must come from a national government mint or an approved refiner, assayer, or manufacturer. The floor is fixed.

- Gold coins (.9999 for most) — Most qualifying coins are 24 karat. The Gold American Eagle is the sole statutory exception at 22 karat.

- Proof coins — Proof versions of eligible coins can qualify — but only in original, undamaged condition with the certificate of authenticity intact.

Criterion Two: Possession

Purity clears one hurdle. Most people don’t realize there’s a second one — and it has nothing to do with the coin itself.

Under IRC Section 408(m)(3), IRA-owned physical gold must be in the physical possession of an IRS-approved trustee or custodian. That means a bank, trust company, or entity specifically approved by the IRS. The metals are then stored at a licensed depository — a facility equipped and legally designated to hold IRA assets.

This isn’t optional language. It’s structural.

The metals stay in your name. Ownership is yours. But custody runs through the approved trustee — and the gold lives at the depository, not at your address.

A precious metals IRA is built around this exact structure. Understanding it before you open an account is what prevents the most common — and most expensive — mistakes.

| IRS Compliance Requirement | What It Means | Consequence of Failure |

|---|---|---|

| Minimum fineness (.995 for bullion) | Gold must be at least 99.5% pure (Eagle exempted at 91.67%) | Product treated as prohibited collectible |

| Authorized mint or producer | Must come from a national government mint or approved refiner | Product disqualified regardless of purity |

| Trustee/custodian possession | Held by IRS-approved custodian, not the IRA owner | Entire account treated as distributed |

| Licensed depository storage | Stored at approved facility (not home, not bank safe deposit box) | Same taxable distribution result |

Why the Industry Makes This Harder Than It Is

Those two requirements took about a minute to read.

So why does this feel like a maze?

Some of it is the subject matter — tax code, custodian requirements, depository logistics. None of it is vocabulary most people use day to day. But a meaningful part of the confusion doesn’t happen by accident. Parts of the precious metals industry benefit from complexity. Dense language, layered caveats, the persistent implication that you can’t navigate this without specialized guidance at every turn — it creates dependency. And dependency is a business model.

We believe simplicity is the real value. Our job isn’t to be indispensable. It’s to show you that the maze mostly isn’t there.

What we’ve found: most customers who arrive overwhelmed aren’t struggling with the rules themselves. They’re struggling with how the rules were delivered to them — all at once, stripped of context, mixed in with things that don’t apply to their situation.

The purity standard takes a few minutes to understand. The possession requirement takes another few. Where guidance actually matters — custodian selection, depository relationship, product sourcing — that’s where Brighton Gold adds real value. Decoding the rules? That’s the easy end.

The Approved List: Which Gold Coins and Bars Qualify

The U.S. Mint produces the two gold coins that define the IRA-eligible standard in this country: the Gold American Eagle and the Gold American Buffalo.

Both qualify. Both are U.S.-minted. They’re the products Brighton Gold works with most — not because the approved list ends there, but because provenance, purity, and liquidity matter to owners thinking in years and decades, not quarters.

Here’s the full picture.

IRA-Approved Gold Coins and Bullion

| Product | Country | Fineness | IRA Status | Notes |

|---|---|---|---|---|

| Gold American Eagle | United States | .9167 (22k) | ✓ Approved | Statutory exemption — only 22k coin that qualifies |

| Gold American Buffalo | United States | .9999 (24k) | ✓ Approved | Meets standard fineness requirement |

| Canadian Gold Maple Leaf | Canada | .9999 (24k) | ✓ Approved | Meets fineness; not U.S.-minted |

| Austrian Gold Philharmonic | Austria | .9999 (24k) | ✓ Approved | Meets fineness; not U.S.-minted |

| Australian Gold Kangaroo | Australia | .9999 (24k) | ✓ Approved | Meets fineness; not U.S.-minted |

| PAMP Suisse Gold Bars | Switzerland | .9999 (24k) | ✓ Approved | Approved refiner; meets fineness |

| Credit Suisse Gold Bars | Switzerland | .9999 (24k) | ✓ Approved | Approved refiner; meets fineness |

| South African Krugerrand | South Africa | .9167 (22k) | ✗ NOT Approved | No statutory exemption; fails fineness test |

| Pre-1933 U.S. Gold Coins | United States | Varies | ✗ NOT Approved | Classified as collectibles regardless of fineness |

| Gold Jewelry | N/A | Varies | ✗ NOT Approved | Collectible by definition; no IRA exception |

| Numismatic/Commemorative Coins | Various | Varies | ✗ NOT Approved | Value based on rarity, not metal content |

If you’re weighing the Eagle against the Buffalo — the fineness difference, the composition, what each one means in practical IRA use — the guide to choosing IRS-approved gold coins is worth working through before you decide.

For a broader look at which coins fit what long-term owners are actually trying to accomplish, the full resource on choosing IRS-approved gold coins covers the complete range.

The American Gold Eagle Exception — What 22k Gets Right

The Gold Eagle is 22 karat. That’s 91.67% gold — well below the .995 floor that governs everything else on the approved list.

So why does it qualify?

When Congress wrote the Taxpayer Relief Act of 1997, the Eagle was already the United States’ flagship legal tender gold coin. Excluding it from IRA eligibility while approving foreign .9999 coins would have been a strange result. So the statute includes a specific carve-out — the Eagle qualifies, in all four denominations, regardless of its fineness.

That exemption doesn’t extend to other 22-karat coins. Not even close.

The Krugerrand is also 22 karat. It doesn’t qualify — because there’s no statutory carve-out for it. There’s no general 22-karat rule. There’s one exemption, written for one product. Everything else holds to the .995 floor.

- Gold Eagle (approved) — 22 karat, statutory exemption, U.S. legal tender, all four denominations

- Krugerrand (not approved) — 22 karat, no exemption, fails the IRA fineness test

- Gold Buffalo (approved) — 24 karat, meets the standard fineness requirement directly

- Pre-1933 U.S. coins (not approved) — classified as collectibles regardless of gold content or American origin

That last one surprises people. The assumption that “old U.S. gold” must be IRA-approved — because it’s American — doesn’t hold. Age and historical significance push a coin into the collectibles category. The IRS doesn’t make exceptions for patriotic intent.

The Possession Rule: Why Where You Store It Matters as Much as What You Buy

Most people researching IRA-eligible gold spend most of their time on the approved list.

That makes sense. The coin question is concrete — it has a right answer.

The possession requirement is where the more expensive mistakes happen. And it gets far less attention than it deserves.

Understanding gold IRA storage rules isn’t optional. It’s the structural requirement that determines whether your metals are inside the IRA or effectively outside it — regardless of which coin you chose.

What “Trustee Possession” Actually Means

The IRS requires IRA-held physical gold to be in the physical possession of an IRS-approved trustee or custodian. That comes directly from IRS Publication 590-A and IRC Section 408(m)(3).

In practice:

- An approved custodian — a bank, trust company, or IRS-approved non-bank entity — holds legal custody of the metals on behalf of the IRA.

- An authorized depository stores the metals in a segregated or pooled vault. The depository is a separate institution from the custodian. That’s where the gold physically lives — not at your home, not in a safe deposit box you control.

- You own the metals through the IRA — titled in the IRA’s name, held by the custodian, stored at the depository. Your ownership is real. Your physical access is not.

The IRS draws a hard line between beneficial ownership — which you have — and physical possession — which you don’t.

The moment that line blurs, the metals are treated as distributed from the account. The full market value becomes taxable in the year it happens. Under 59½, a 10% early withdrawal penalty applies on top.

This isn’t a technicality. It’s the explicit design of the law.

The Home Storage Myth — Why the “Checkbook IRA” Approach Fails

There’s a structure that circulates in parts of the self-directed IRA world called the “Checkbook IRA” or “LLC IRA.”

Here’s how it’s typically pitched: form an LLC owned by your IRA, appoint yourself as the manager, store IRA gold at home — because technically the LLC is holding it, not you personally.

It doesn’t work. The legal record isn’t close.

The Tax Court addressed this directly in McNulty v. Commissioner (2021). When an IRA owner serves as LLC manager and has unfettered access to the metals, the court held that the metals are in the constructive possession of the IRA owner — not an approved trustee. The entire account was treated as distributed. The owners faced tax liability on the full account value, plus penalties.

The “Checkbook IRA” isn’t a gray area waiting to be tested. It was tested. It lost.

Brighton Gold doesn’t work with customers pursuing home storage structures. We don’t recommend custodians who facilitate them. The risk to the account is real. It’s also not correctable once the distribution is recognized.

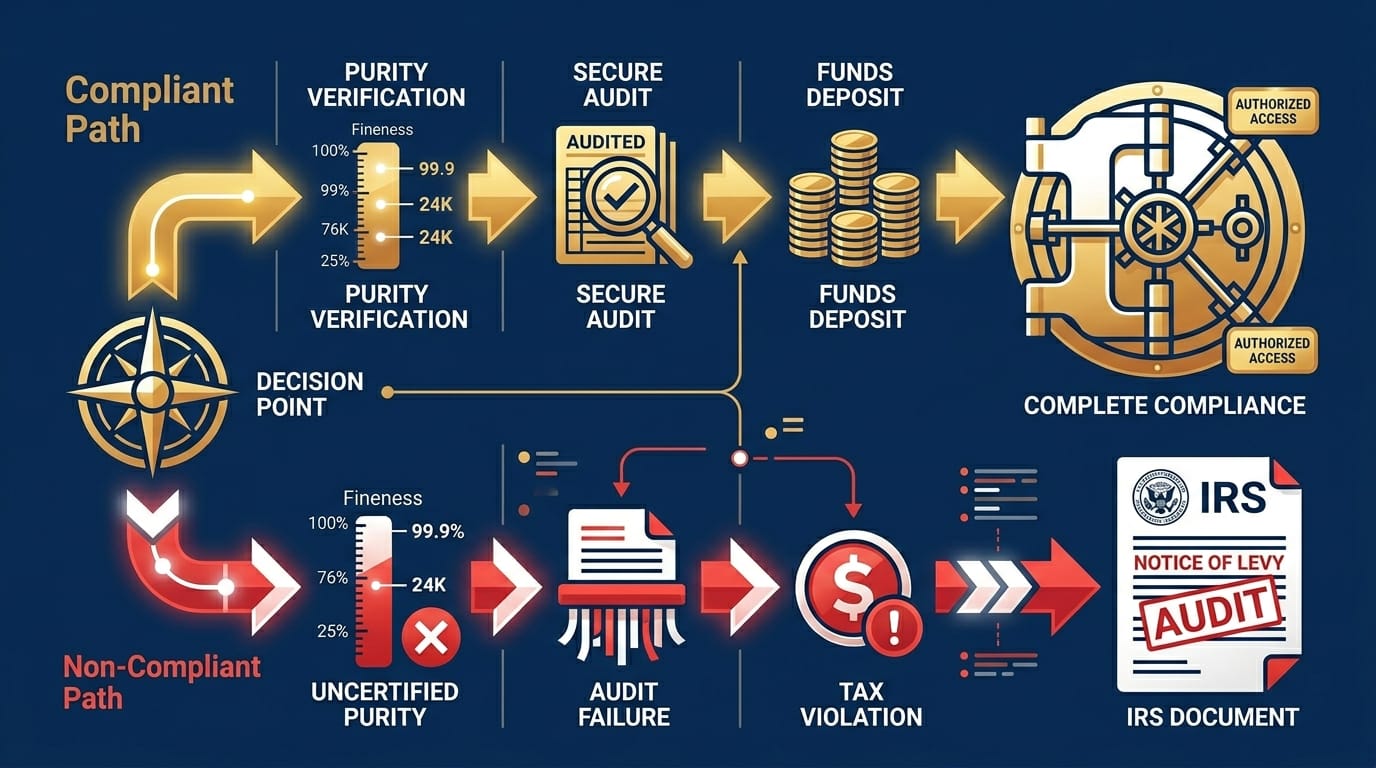

What the compliant path actually looks like:

- IRA established with an IRS-approved self-directed custodian

- Custodian purchases the metals on behalf of the IRA

- Metals ship directly to an approved depository — never to the owner

- Owner receives account statements confirming holdings — not physical delivery

- Storage fees paid from the IRA or directly by the owner to the depository

That’s the structure. Straightforward when you follow it.

If you’re still in the setup phase, the walkthrough on executing a precious metals IRA rollover covers custodian selection and the funding steps in detail.

The Collectibles Trap: How Owners End Up With a Taxable Distribution Without Realizing It

The fineness floor gets most of the attention. It’s a number. You can verify it before you buy.

The collectibles prohibition is where the more costly mistakes live — and it’s the rule that catches people who think they’ve already done their research.

Under IRS rules, using IRA funds to purchase a prohibited collectible triggers a distribution of the purchase amount in the year it happens. The metals don’t have to leave the account. The transaction itself is the taxable event.

How the Collectibles Rule Works

Before 1997, the IRS classified all physical gold as a collectible — prohibited inside IRAs alongside artwork, stamps, gems, and rare coins. The Taxpayer Relief Act of 1997 created a carve-out for qualifying bullion and specific government-minted coins. Everything that didn’t make that cut stayed in the collectibles category.

That category still covers:

- Pre-1933 U.S. gold coins — regardless of gold content or American origin

- Rare or numismatic coins where market value exceeds metal value

- Gold jewelry, medallions, and rounds from unapproved manufacturers

- Coins and bars below the .995 fineness standard — with the Eagle exception

- Any product from a mint or refiner not approved by the IRS

The question isn’t “is this physical gold?” It’s whether this specific product meets the statutory requirements of IRC Section 408(m)(3). If the answer is no — and IRA funds were used — the purchase amount is treated as a distribution and taxed in that year.

| Scenario | IRS Treatment | Tax Consequence |

|---|---|---|

| Buy .9999 Gold Buffalo in IRA, store at licensed depository | Fully compliant | No tax event |

| Buy Gold Eagle in IRA, store at licensed depository | Fully compliant (Eagle exemption) | No tax event |

| Buy Krugerrand in IRA (any storage) | Prohibited collectible | Distribution — taxable in year of purchase |

| Buy Pre-1933 U.S. gold coin in IRA | Prohibited collectible | Distribution — taxable in year of purchase |

| Buy approved gold coin, store at home | Possession violation | Full account treated as distributed |

| Buy approved gold, store in personal bank safe deposit box | Possession violation | Full account treated as distributed |

What Happens If the Wrong Coin Gets Into an IRA

The outcome isn’t a warning letter.

It’s a taxable event — recognized the moment the transaction happens, not when it’s discovered.

If IRA funds are used to purchase a prohibited collectible, the purchase amount is treated as a distribution in that tax year. You’ll owe ordinary tax liability on the amount. Under 59½, the 10% early withdrawal penalty applies on top. The metals — the ones that triggered the distribution — are outside the IRA now. They belong to you personally. The tax has already landed.

There’s no reversal mechanism. Once the distribution is recognized, it’s recognized. You can’t re-contribute the metals or undo the transaction retroactively.

This is why pre-purchase verification matters — confirming with your custodian that a specific product meets IRS standards before any funds move. Custodians vary in how carefully they do that screening, and that variance has real consequences. Identifying safe gold IRA practices and understanding gold IRA fee structures — including fees that aren’t always disclosed upfront — are both worth working through before you fund an account.

This Isn’t the Right Path for Everyone

One thing worth being direct about.

If you’re approaching this as a short-term trade — buy now, sell when the price moves, out in six months — a Gold IRA isn’t the right structure. The IRA framework creates friction around short-term access by design. That friction protects the account’s tax-deferred status. It’s not a flaw. But it makes the structure a poor fit for anyone thinking in quarters instead of years.

And if you’re looking for price forecasts, market timing guidance, or a guarantee that gold is headed up — Brighton Gold isn’t your fit. No legitimate dealer can offer that. Precious metals may appreciate, depreciate, or remain unchanged. Anyone claiming otherwise is making a promise they can’t back.

Brighton Gold works with customers who want to hold something real for the long term. People who aren’t chasing price activity — they want clarity, process integrity, and support at every stage of ownership.

If that describes where you are, executing a penalty-free 401k rollover is a natural next step to understand.

If it doesn’t — that’s worth knowing before you’re inside a structure that doesn’t match your goals.

Frequently Asked Questions

Is 22-Karat Gold Allowed in an IRA?

The short answer is: only one 22-karat gold coin qualifies, and that’s the American Gold Eagle.

Congress wrote a specific statutory exemption for the Gold Eagle into the Taxpayer Relief Act of 1997. That exemption doesn’t travel. The Krugerrand is also 22 karat — not approved. No general 22-karat rule exists. If a dealer tells you 22-karat gold is “fine for IRAs” without citing the Eagle specifically, that’s incomplete information — and acting on it triggers a taxable distribution. The IRS compliance structure exists independently of price activity. Both realities are in play.

Can I Put Gold Bars From a Private Refinery in My IRA?

Private refinery bars can qualify — but not all of them do.

The .995 fineness floor applies. So does the producer requirement — the bar must come from a national government mint or a refiner, assayer, or manufacturer that meets IRS standards. PAMP Suisse, Valcambi, and Credit Suisse are among the well-known approved producers. Unknown or unapproved manufacturers don’t qualify regardless of what the bar says about its purity.

Confirm approval status with your custodian before any purchase. If they can’t confirm it — the bar doesn’t go in the account.

Why Are South African Krugerrands Not IRA-Approved?

Two reasons, working together.

First, the Krugerrand is 22-karat (91.67% gold) — below the .995 floor. Second, Congress didn’t include a carve-out for it in the 1997 legislation the way it did for the Gold Eagle. The Eagle’s approval at 22 karat is a specific statutory exemption, not a general rule. The Krugerrand is one of the first globally recognized bullion coins in the world. Market reputation and IRS eligibility are different things — the statute doesn’t follow market popularity.

Does the IRS Allow Proof Gold Coins in Retirement Accounts?

Proof versions of IRS-eligible coins generally qualify — with conditions.

The coin must stay in its original mint packaging, with the certificate of authenticity intact and the coin undamaged. Any evidence of removal from the sealed case — or handling consistent with collectible use — can shift the coin into the prohibited category. Most custodians treat proof coins with extra scrutiny for exactly this reason. Once that sealed case is opened, the compliance argument weakens fast.

What Happens If I Accidentally Buy a Prohibited Coin With IRA Funds?

The IRS treats the purchase amount as a distribution in the year the transaction occurs.

Intent doesn’t factor in. The amount is treated as distributed — ordinary tax liability applies in that year, plus the 10% penalty if you’re under 59½. The metals leave the IRA permanently. There’s no mechanism to reverse it. Pre-purchase verification with your custodian isn’t paperwork — it’s the line between a clean transaction and a taxable one.

How Does the IRS Define “Fineness” for Gold Bullion?

Fineness is the proportion of pure gold in a coin or bar, expressed as a decimal.

A fineness of .995 means 99.5% pure gold. A fineness of .9999 means 99.99%. The IRS sets the floor at .995 for bullion bars and most gold coins — with the Gold American Eagle as the sole statutory exception at .9167. Fineness and karat measure the same thing differently: karat as a fraction of 24, fineness as a decimal. Both answer the same question — how much of this product is actually gold.

Can I Move an Existing 401(k) Into a Gold IRA Without Tax Consequences?

Yes — if the transfer is done correctly through a direct rollover.

A direct rollover sends funds from your 401(k) straight to the new self-directed IRA custodian — the money never passes through your hands. No taxable event. No penalties. An indirect rollover — where the check comes to you first — introduces a mandatory 20% withholding and a 60-day window to complete the transfer. Miss that window, and the full amount becomes taxable. Consulting your CPA or tax professional before initiating is the right call for tax-specific questions about your situation. The mechanics and what to confirm with your plan administrator are covered in the walkthrough on executing a penalty-free 401k rollover.

The Bottom Line on IRS Gold IRA Rules

The framework isn’t complicated. Two requirements — purity and possession — govern everything. A defined list of qualifying products covers the gold coin and bullion landscape. A clear custody structure connects the custodian to the depository to the owner.

What makes this feel complicated is noise. The Checkbook IRA pitch. Home storage arrangements that don’t hold up in court. Vague assurances that “any physical gold” works inside an IRA. None of it survives contact with the actual statute.

The possession requirement is where most costly mistakes happen — not the coin selection. Owners who understand the fineness floor but skip the custody structure end up in a taxable distribution they didn’t see coming and can’t walk back.

Brighton Gold’s position is clear: U.S.-minted products are our standard. The Gold American Eagle and the Gold American Buffalo represent the cleanest, most liquid path for customers looking for IRS-compliant gold in a retirement account. Not because foreign alternatives don’t qualify — some do — but because provenance, recognized purity, and established domestic liquidity matter to owners thinking in decades, not quarters.

Precious metals may appreciate, depreciate, or remain unchanged. The compliance structure operates independently of that. Both are real. Getting the structure right is what makes everything else work. For more on the full landscape of precious metals IRA options, the learning center is the right place to continue.

If you’ve spent time understanding the IRS rules — you’re already ahead of most people who own gold inside a retirement account.

The harder question isn’t whether the rules make sense. It’s whether your specific situation holds up against them. Your account structure. Your custodian. The products you’re looking at. Those are the details worth a direct conversation — before anything moves.

Brighton Gold offers a complimentary consultation to work through exactly that. We’ll walk you through the compliance framework as it applies to your situation — including how the No Fee Precious Metals IRA works and whether you qualify.

Check Your IRA Compliance Picture

Getting the structure right from the beginning costs nothing. A taxable distribution you didn’t see coming costs considerably more than that.