What Are the Hidden Fees in a Gold IRA for 2026? (Exposed)

In 2026, the hidden fees in a Gold IRA fall into three categories — and most dealers won’t volunteer any of them. The first is the dealer spread: the markup between the publicly quoted spot price of gold and the retail price you actually pay. It can run from 3% to 15%, and it’s rarely disclosed as a named line item. The second is custodial surcharges — wire fees, per-transaction processing charges, and termination costs buried in the fine print of your account agreement. The third is liquidity fees: what you pay when you sell, distribute, or close the account. For most customers, that day is twenty years away — which is exactly why it goes unasked.

Together, these three categories represent the total cost of Gold IRA ownership. Most marketing materials lead with the annual storage fee and stop there.

Here’s what a complete cost picture actually looks like. A standard Gold IRA with a flat-rate custodian runs approximately $200–$300 per year — setup ($50), annual administration ($100), and storage ($150). That part is straightforward. What isn’t disclosed on the same page is the spread. A 5% markup on a $250,000 purchase is $12,500 in day-one cost. A 10% spread on the same purchase is $25,000. Neither of those numbers appears as a line item on most dealer invoices. They’re embedded in the purchase price.

This article breaks down every fee category in a Gold IRA: what’s typical, what’s excessive, and what signals a dealer isn’t operating transparently. We cover the flat-fee versus scaled-fee debate, the “free silver” promotional structure, the fee audit checklist you should run before signing anything, and the one question most customers forget to ask until it’s too late.

Precious metals may appreciate, depreciate, or remain unchanged. Brighton Gold does not provide financial, tax, or legal advice. Consult your CPA or tax professional before making any decisions regarding your retirement accounts.

Why Hidden Fees Are the Real Story in Gold IRAs This Year

Most customers come in asking about fees. That’s the right instinct — but it’s usually aimed at the wrong number.

The annual fee is easy to find. It’s on the brochure. What’s harder to find — and what actually drives the total cost of ownership — sits in two places most customers never think to examine: the spread on every purchase and the exit costs that don’t appear until twenty years later. Understanding Gold IRA fee structures requires going beyond the annual summary line and into the mechanics of every transaction — including the ones that only surface when you’re ready to exit.

Here’s what we’re seeing today: the Gold IRA industry is one of the few financial spaces where marketing costs and customer costs are often the same number — just labeled differently.

Why Complexity in Fee Schedules Is Someone Else’s Revenue

A fee schedule that takes a spreadsheet to decode isn’t sophisticated. It’s strategic.

When the cost structure for a Gold IRA is buried across four documents — the custodian agreement, the dealer’s fee schedule, the storage contract, and the promotional offer terms — that complexity isn’t accidental. The harder it is for a customer to add up the numbers, the less pressure there is on any single number to be reasonable. Brighton Gold’s position on this hasn’t changed: a fee structure that requires an attorney to interpret is a fee structure designed to obscure costs, not communicate them.

Here’s what straightforward disclosure actually covers — and what you should expect before signing anything:

- Setup fee — One-time, typically $50. Covers account establishment with the custodian.

- Annual administration fee — Flat charge, typically $75–$150. Paid annually to the custodian for account maintenance and IRS reporting.

- Storage fee — Flat or percentage-based, typically $100–$150 annually. Paid to the IRS-approved depository.

- Dealer spread — The markup on your purchase price above spot. The largest variable cost — and the one most likely to be omitted from the fee summary.

- Wire transfer fee — $25–$50 per transaction. Standard in most custodian agreements. Appears in the account agreement, not the brochure.

- Liquidation or distribution fee — Charged when you sell metals or take an in-kind distribution. Range varies significantly by custodian.

If a dealer can’t walk you through each of those numbers before you sign — that’s already an answer.

The Three Fee Layers That Drive Total Cost

Here’s a way to think about it that most dealers won’t offer.

There are three separate cost events in a Gold IRA, and they don’t happen at the same time. The annual fee happens every year — predictable, manageable, and the one that gets the most attention in marketing. The spread happens at every purchase — a one-time cost that hits immediately and, on large accounts, is the largest dollar amount you’ll ever pay. The liquidity fee happens at the end — when you’re ready to sell, distribute, or close, and you’re meeting the fine print for the first time.

A customer with $300,000 in a Gold IRA who paid a 7% spread at purchase absorbed $21,000 in day-one cost. That same customer’s flat-rate custodian charges $250 a year. It takes eighty-four years of annual fees to equal what the spread cost in the first transaction.

Evaluating a Gold IRA by the annual fee while ignoring the spread is like judging the cost of a mortgage by the homeowner’s insurance premium. It’s a real number — it’s just not the biggest one on the table.

Breaking Down Every Fee in a Gold IRA

Every fee in a Gold IRA traces back to one of three parties: the custodian, the depository, or the dealer. Once you know who charges what — and when — the total cost picture stops being confusing.

| Fee Type | Typical Range | Who Charges It | When It Applies |

|---|---|---|---|

| Setup / Account Opening | $50 | Custodian | One-time, at account establishment |

| Annual Administration | $75–$150/year | Custodian | Annual recurring |

| Storage — Flat Rate | $100–$150/year | IRS-Approved Depository | Annual recurring, fixed regardless of balance |

| Storage — Scaled Rate | 0.5%–1.0% of holdings | IRS-Approved Depository | Annual, increases as account value grows |

| Dealer Spread | 3%–15% of purchase | Dealer | Per purchase transaction |

| Wire Transfer Fee | $25–$50 | Custodian | Per wire in or out |

| Liquidation / Distribution | $50–$150+ | Custodian or Dealer | At cash-out or in-kind distribution |

The spread and the liquidation fee are where the real cost lives. They’re also the two you’re least likely to find on the front page of any dealer’s website.

Dealer Spread — The First Number That Matters

The spread is simple in concept: it’s the gap between what gold costs on the open market and what you pay the dealer to put it in your IRA.

Spot price is public. Any financial news site shows it in real time. Retail price is set by the dealer — and the difference between the two is the spread. Per LBMA benchmark standards, institutional gold transactions reference published market prices. Retail IRA purchases carry a premium above that benchmark, which is legitimate — dealers have real operational costs. A 3%–5% spread on standard IRA-eligible bullion is industry-typical. When that number climbs above 8%–10% on common coins like the Gold American Eagle, it’s worth asking for a specific justification before anything is authorized.

The spread isn’t a scam. It’s a cost of doing business. What matters — the only thing that matters — is whether it’s disclosed before you commit.

- Watch for: Dealers who lead with spot price but don’t name the retail markup until the final paperwork

- Watch for: “Price match” guarantees with no specifics about which products or which dealers qualify

- Watch for: Multi-year purchase commitments that lock in a spread today on future transactions

Custodial Surcharges — The Line Items in the Account Agreement

The custodian agreement is where the secondary fees live. It’s also the document most customers scan rather than read.

Per FINRA’s disclosure requirements for retirement accounts, complete fee disclosure in self-directed retirement accounts is expected. Whether it’s proactively offered is another matter. Customers who don’t specifically ask for a complete, itemized fee schedule often don’t receive one — and they find these charges later:

- Wire transfer fee — $25–$50 per transaction, inbound and outbound

- Account termination fee — $100–$200 or more, charged if you close the account or transfer to another custodian

- In-kind distribution processing fee — Applied when you take physical possession of metals rather than selling

- Paper statement fee — A small per-statement charge for customers who prefer physical statements

- Excess contribution correction fee — Charged if an over-contribution to the IRA needs to be reversed

Ask for the complete fee schedule in writing. Review it before the account is opened, not after.

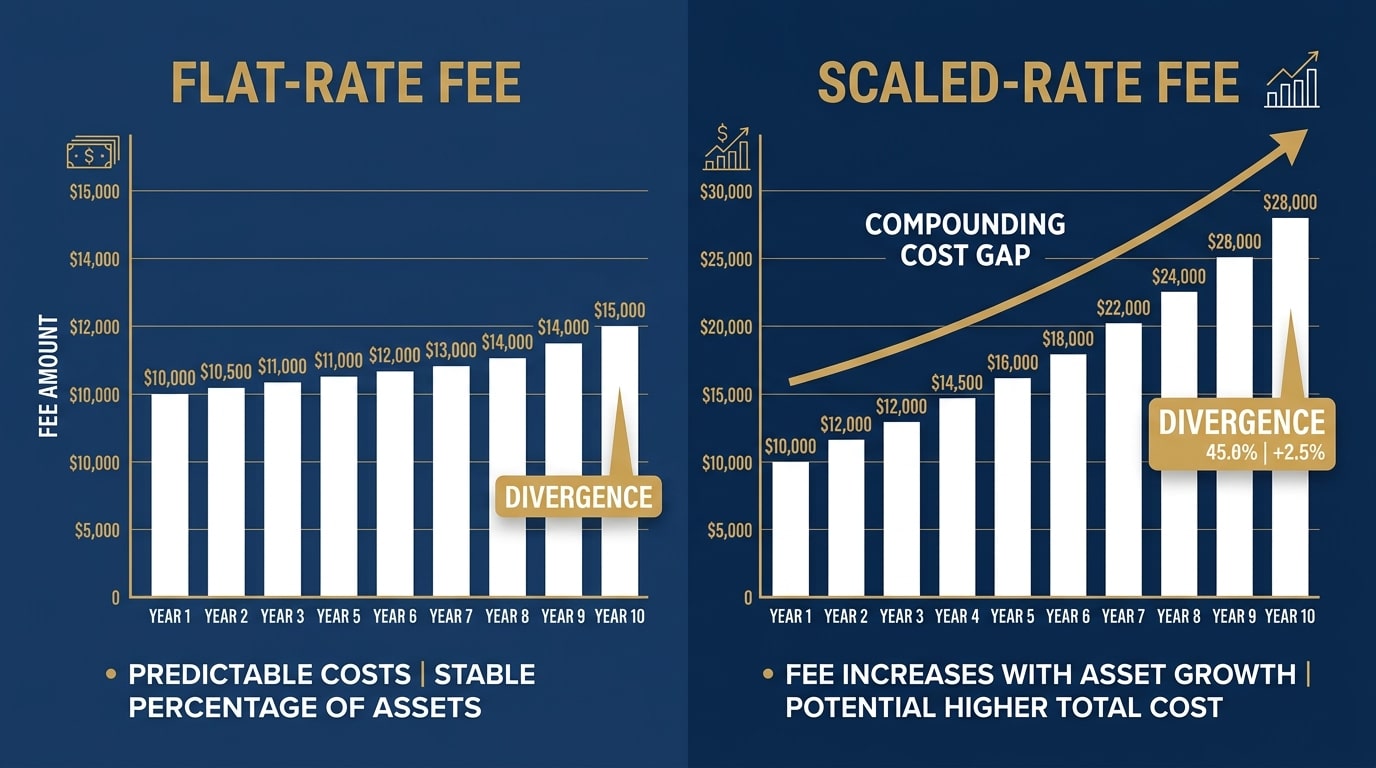

Storage Fees — Why Flat Rate vs. Scaled Rate Changes the Long-Term Math

Storage fees go to the IRS-approved depository that holds your metals. Two structures exist — and the difference between them compounds significantly over time.

Flat rate means you pay a fixed annual charge — typically $100–$150 — regardless of how large the account grows.

Scaled (percentage-based) means you pay a percentage of total holdings — typically 0.5%–1% — every year. As the account grows, so does the fee.

On a $100,000 account, a 0.5% scaled fee is $500/year. On a $400,000 account — possible if metals appreciate — that same rate is $2,000/year. A flat-rate structure stays at $150. For customers with large balances, that’s not a minor difference. It’s a number worth confirming before the account is opened, not after the structure is locked in.

Segregated vs. Commingled Storage

Storage also comes in two types — and both are IRS-compliant.

- Commingled storage: Your metals are held with other customers’ metals of the same type. You own a documented claim by weight and product category — not specific physical units. Lower annual cost, typically $100–$125.

- Segregated storage: Your specific coins or bars are stored separately with individual identification. You have a direct claim to those exact units. Higher annual cost — typically $150–$200 or more — but provides a cleaner ownership trail for customers with estate planning priorities.

For customers who want to understand the full picture before committing to a storage structure, understanding gold IRA storage rules covers what IRS compliance requires of approved depositories and what the ownership documentation looks like under each arrangement.

Liquidity Fees — The Cost You Won’t Face for Twenty Years

This is the fee most customers never ask about. It’s also the one that catches them off guard.

When you’re ready to sell metals held in a Gold IRA — or take an in-kind distribution of the physical metals themselves — costs arrive from multiple directions at once. The custodian charges a liquidation or distribution processing fee. The dealer’s buyback price typically sits below spot — the reverse of the purchase spread, applied on the way out. In-kind distributions carry shipping and insurance on top of processing.

The BBB documents a consistent pattern of complaints in the precious metals IRA category: customers surprised by what it costs to exit — not customers who were misled about the annual fee. The entry costs and exit costs are different numbers. A transparent dealer discusses both. Brighton Gold does not guarantee buybacks or fixed resale pricing — resale values depend on market conditions. But the policy should be in writing before anything is signed, not surfaced when you call to sell.

The “Free Silver” Trap and How Promotional Pricing Works

“Free silver” is one of the most searched phrases in the Gold IRA space. It’s also one of the most reliably misunderstood.

There’s no such thing as a promotional loss leader in a commissioned transaction environment. Every bonus is funded somewhere. The question is just whether it’s funded by the dealer — as a genuine customer acquisition cost — or by the customer through a higher spread on their own purchase.

How Promotional Offers Shift the Real Cost

Here’s how the most common structure works. A dealer offers “up to $10,000 in free silver” with a qualifying IRA purchase. The customer sees a bonus. What actually happens is that the spread on the primary gold purchase runs 8%–12% rather than the 3%–5% a transparent dealer would charge. The silver isn’t free. The customer funded it — through their own markup — and received a worse net position than a no-bonus deal at a lower spread would have produced.

Some dealers use promotional offers as genuine acquisition costs — marketing spend applied to the customer’s benefit. We’re not suggesting every bonus offer is a trap. The distinction is disclosure: can the dealer tell you what spread you’re paying before the promotional value is factored in?

- Before accepting any bonus offer, ask: “What is the spread on my gold purchase — calculated separately from the promotional metals?”

- Compare the full transaction: The relevant number is total cost paid minus spot value received — across all metals, including the bonus

- Get the buyback terms on promotional metals: Bonus silver sometimes carries different resale terms than primary IRA holdings — confirm before accepting

Flat-Rate vs. Scaled-Rate Custodian — What It Costs Over Time

For large-balance customers, the custodial fee structure isn’t a detail — it’s a decision with a significant dollar figure attached.

| Flat-Rate Custodian | Scaled-Rate Custodian (0.75%) | |

|---|---|---|

| Annual Fee at $100,000 | $250/year | $750/year |

| Annual Fee at $250,000 | $250/year | $1,875/year |

| Annual Fee at $500,000 | $250/year | $3,750/year |

| 10-Year Total at $500,000 | ~$2,500 | ~$37,500 |

| Fee Behavior | Fixed regardless of balance | Grows as account grows |

On a $500,000 account over a decade, the gap between a flat-rate and a scaled-rate custodian is more than $35,000 — before the spread on any purchases is counted.

Brighton Gold’s No Fee Precious Metals IRA for the lifetime of the account on qualified purchases eliminates custodial and storage fees at the structural level. Not as a first-year waiver. Not as a promotional rate that reinstates in month thirteen. That distinction is worth understanding when comparing offers.

Who This Isn’t For

One thing worth saying directly: Brighton Gold isn’t the right fit for everyone — and the fee structure conversation is a good place to figure out which side of that line you’re on.

If your primary goal is to buy metals today and sell in six to twelve months when the price moves — a precious metals IRA isn’t the right vehicle, and Brighton Gold isn’t the right dealer. IRA accounts are governed by IRS distribution rules, custodian processes, and fee structures built for long-term ownership. They’re not short-term trading instruments. Using them as one costs more in fees, and the structure works against you at every turn.

Brighton Gold doesn’t forecast price movements, doesn’t weigh in on optimal purchase timing, and doesn’t provide recommendations based on anticipated market conditions. We educate on the ownership process and walk customers through it directly.

If that’s not the kind of relationship you’re looking for — that’s a useful thing to know before you open an account.

The Fee Audit Checklist — Three Steps Before You Sign

Here’s what we tell every customer who’s evaluating a Gold IRA: before you sign anything, run three checks. They take less than an hour. They surface every number that matters.

Most customers don’t do this because no one tells them it’s possible. It is.

Step 1 — Request the Buyback Policy in Writing

Ask for the buyback policy as a written document before any paperwork is signed. Not a verbal overview. Not a sentence in an email. A document.

A complete policy answers:

- Whether the dealer is obligated to repurchase metals from you, or whether buyback is at their discretion

- What price basis applies when they make a buyback offer — spot price, a percentage below spot, or something else

- Whether the terms cover all IRA-eligible products or only specific coins and bar types

- What the process covers — required documentation, timelines, shipping and insurance responsibilities

Brighton Gold does not guarantee buybacks or fixed resale pricing. That’s an honest answer. What to watch for is a dealer who does guarantee buyback pricing — without a written document behind it. That guarantee may look very different when you actually need it.

For customers evaluating custodians at the same time, a review of top-rated Gold IRA custodians for 2026 covers which custodians include buyback facilitation in their service agreements and how that process typically unfolds in practice.

Step 2 — Verify the Annual Storage Rate Is Flat, Not Scaled

Before the account is opened, ask two direct questions:

- “Is the annual storage fee flat or percentage-based?”

- “Does that fee increase if the value of my account increases?”

If the answer is percentage-based, do the ten-year math at your expected account value. Compare it against a flat-rate alternative. That’s the conversation that saves large-balance customers tens of thousands of dollars — and it almost never happens without the customer initiating it.

Also worth confirming: does the storage fee go directly to the depository, or does it pass through the custodian? Both structures are legitimate. But you should know which one you’re dealing with — because custodians who pass through depository fees with markup are adding a cost that doesn’t appear anywhere in the storage fee line.

Understanding gold IRA storage rules gives you the foundation to evaluate these questions accurately — including what IRS regulations require of approved depositories and how the ownership documentation differs between storage types.

Step 3 — Calculate the Spread Before Committing

This is the most important number in the entire transaction — and it requires a direct conversation, not a brochure.

Ask: “What is the purchase price per ounce on this product, and what is today’s spot price?”

Divide the markup by the spot price. That percentage is your spread.

- Under 5% on standard IRA-eligible bullion — typical and reasonable

- 5%–8% — higher, but potentially justified on specialized or lower-availability products

- Above 8% on standard IRS-approved gold coins — ask for specific justification before proceeding

A dealer who won’t name that number before you authorize the purchase is telling you something. Transparent operations don’t need to hide it.

Reviewing the full process for executing a precious metals IRA rollover before any fee conversation is also worth the time. Understanding the full transaction sequence — what gets authorized at each step and when each cost triggers — puts you in a much stronger position when you’re asking these questions.

Frequently Asked Questions

How much should a Gold IRA cost in fees each year?

A standard Gold IRA with a flat-rate custodian typically runs $200–$300 per year in combined administration and storage fees. That’s a reasonable baseline for a transparent, compliant account. The spread on your purchase is separate — and on large accounts, it’s a much larger dollar amount than any annual fee you’ll ever pay.

What is the dealer spread and how is it calculated in 2026?

The dealer spread is the difference between the spot price of gold and the retail price the dealer charges for a specific coin or bar. To calculate it: (Retail Price − Spot Price) ÷ Spot Price × 100. A Gold American Eagle might carry a 4%–6% spread over spot depending on market conditions and dealer pricing. What we’ve found is that the customers who ask for this calculation upfront — before authorizing anything — are the ones who make the most grounded decisions. Any dealer who won’t provide it before the purchase closes is not operating transparently.

Are there hidden fees for rolling over a 401(k) to a Gold IRA?

The direct rollover itself typically doesn’t carry a fee — it’s a custodian-to-custodian transfer that the IRS does not tax or penalize when executed correctly. Per IRS Publication 590-A, a properly executed direct rollover from a qualifying retirement plan to an IRA does not trigger a taxable distribution event. Always confirm the mechanics with your CPA or tax professional before initiating.

What can carry costs: the new account setup fee (typically $50), the spread on your first purchase, and occasionally a wire transfer fee if the originating custodian charges for outbound transfers. Identifying safe Gold IRA practices starts with mapping which cost belongs to which stage of the rollover — and getting written confirmation that no early distribution penalty applies to your specific transfer type.

Is “free silver” really free or is it a marketing tactic?

In most cases, it’s a marketing tactic — and a transparent dealer will acknowledge that plainly.

“Free silver” offers are typically funded through a higher spread on the primary gold purchase. Whether the deal is actually favorable depends on whether the total cost of the transaction — purchase price minus spot value across all metals received — compares better than a no-bonus deal at a lower spread. The question to ask before accepting any bonus offer: “What spread am I paying on my gold purchase, separate from the promotional metals?” A dealer who can’t answer that question directly isn’t one operating in your interest.

What is the difference between segregated and commingled Gold IRA storage?

Commingled storage holds your metals alongside other customers’ metals of the same type. You have a documented ownership claim by weight and product type — not to specific physical units. Annual cost is lower, typically $100–$125.

Segregated storage holds your specific coins or bars separately with individual identification. Your claim is to those exact units. Annual cost is higher — typically $150–$200 or more. For customers with estate planning priorities or a strong preference for direct, documented ownership, that premium is often worth it. For customers who prioritize cost efficiency over documentation specificity, commingled is compliant and commonly used.

How do I avoid excessive fees on a Gold IRA in 2026?

Three steps: ask for the spread percentage before any purchase is authorized. Confirm the annual storage fee is flat-rate rather than scaled. Request the buyback policy in writing before signing anything.

Recognizing Gold IRA fee red flags is the other half of the answer — knowing how to identify a deceptive fee structure makes a transparent one easy to recognize by contrast. A dealer who answers all three of those questions upfront and without hesitation is a dealer operating with your interests in view.

Can a customer avoid custodial fees entirely?

Yes — under qualifying program structures. Brighton Gold’s No Fee Precious Metals IRA for the lifetime of the account on qualified purchases eliminates custodial and storage fees at the structural level. This isn’t a first-year waiver. It applies for the full lifetime of the account on qualifying purchases.

What the No Fee structure doesn’t eliminate is the dealer spread — a separate cost that should still be disclosed and calculated before any purchase is authorized. Fee program or not, every purchase carries a spread. What differs is whether that spread is presented as a known number before you commit. Evaluating institutional bias against gold — examining that context as part of the larger decision helps put fee concerns in proper perspective.

The Takeaway on Gold IRA Fees in 2026

The “hidden fee” conversation is really a disclosure conversation — and it shouldn’t be complicated.

The fees aren’t secret. They’re legal. They exist in documents you’re given to sign. What makes them “hidden” is that no one hands you a plain-English summary before you decide — and some dealers benefit from the gap between what customers know going in and what they find out later.

Here’s what transparency means in practice: a dealer who names the spread before you authorize the purchase. A custodian whose fee schedule fits on one page. A buyback policy that exists as a written document — not a verbal assurance from someone on a call. A storage fee that stays flat regardless of how the account grows.

Four cost categories. That’s the whole picture. Spread on purchase, annual custodial fee, storage fee, liquidation terms. Any dealer who can explain all four in plain language before you sign has nothing to hide — and that’s the only kind of relationship worth building for twenty years.

Precious metals may appreciate, depreciate, or remain unchanged. Brighton Gold’s position on that reality is direct: customers who go in with a complete cost picture — including the downside — make better decisions. Not every customer who works through these numbers will decide a Precious Metals IRA is right for them. That’s a good outcome, not a bad one. It’s also the only outcome that builds a long-term relationship worth having.

If you’ve worked through the fee picture in this article and want to see how it applies to your specific situation — account size, product selection, custodian structure — that’s what our complimentary consultation covers.

We’ll show you how the spread is calculated on the products you’re considering, run the ten- and twenty-year cost comparison between flat-rate and scaled-rate structures, and give you a full picture of total cost before any commitment is made.

The Learning Center has additional resources on every aspect of precious metals ownership — from account setup and storage to long-term planning and beyond.

Fee transparency isn’t a feature worth advertising. It’s the baseline every owner deserves — and it should exist before you sign, not after.