How Do I Set Up a Gold IRA? (Step-by-Step Checklist)

Setting up a Gold IRA is a four-step process: choose a self-directed IRA custodian, fund the account, select your IRS-approved metals, and arrange depository storage. Most customers complete all four steps in two to three weeks. No trips to a vault. No complicated paperwork that requires a lawyer. A concierge team coordinates most of the process between the custodian and the depository — your primary job is making three decisions.

Here’s what those decisions are, and what the IRS actually requires at each stage.

Step 1 is choosing a qualified SDIRA custodian — a financial institution authorized by the IRS to hold alternative assets inside a retirement account. Banks and traditional brokerages don’t do this. You need a self-directed specialist.

Step 2 is funding the account. You can fund it through a direct rollover from an existing IRA or 401(k), an institution-to-institution transfer, or a new cash contribution subject to the annual limits set by IRS Publication 590-A. Each funding method has different IRS rules and timelines — those differences matter more than most people realize.

Step 3 is selecting your metals. Not every gold product qualifies. The IRS requires a minimum purity of 99.5% for gold held inside an IRA. U.S.-minted coins like the Gold American Eagle and Gold Buffalo meet those standards and are among the most commonly held products.

Step 4 is storage. Physical gold inside a retirement account must be held by an IRS-approved depository — not at home, not in a bank safe deposit box. That’s not a guideline. It’s a compliance requirement with real tax consequences if ignored.

The rest of this article covers each step in detail — including the funding traps most people walk into, the IRS rules that trip up first-time buyers, and what the process looks like when it’s done right.

What the Industry Doesn’t Tell You About This Process

Here’s a question worth asking before you read another word about Gold IRAs: why does a four-step process have a reputation for being complicated?

It’s not the IRS rules. Those are documented and consistent.

It’s not the custodians. They do this for a living.

It’s not the metals themselves. U.S.-minted gold coins are straightforward to confirm and acquire.

The process of establishing a precious metals IRA is genuinely simple — two to three weeks, four steps, and one point of contact who coordinates the rest. What makes it feel overwhelming is an industry that benefits from keeping it that way.

That’s worth naming before we get into the steps.

Why the Complexity Is a Feature — for Them

When a process feels complicated, something else happens: you start looking for someone to lean on.

That’s not an accident. It’s how a lot of financial services firms build customer dependency — layer enough jargon on top of a simple process and suddenly you need an expert, a guide, a manager, and a quarterly review. What used to be a direct decision becomes an ongoing relationship you’re paying for.

Gold IRA rollovers are one of the clearest examples we see. The mechanics of a direct rollover are three institutional steps. The IRS rules are publicly available in IRS Publication 590-A. The custodian and the dealer handle most of the coordination. Most of what feels like a “complicated process” is jargon sitting on top of a simple one — and in our view, using jargon to signal expertise is the opposite of service.

We do it differently. Before anything is signed, Brighton Gold’s team walks you through exactly what’s going to happen — in plain language, at whatever pace you need.

- Identifying safe gold IRA practices starts before you choose a custodian — knowing what a red flag looks like is the first filter.

- Understanding gold IRA fee structures is part of that same first conversation — the total cost of ownership isn’t always where you expect to find it.

Precious metals may appreciate, depreciate, or remain unchanged. What shouldn’t be uncertain is how clearly you understand the process before you’re in it.

What “Concierge” Means When It’s Real

The word gets used loosely in this industry. Here’s what it actually means in practice.

When you begin working with Brighton Gold, our team coordinates directly with the custodian and the depository on your behalf. You’re not managing three separate institutional relationships. You have one point of contact — someone who keeps you informed at each stage, handles the communication between institutions, and answers your questions as they come up.

Before the sale. Through the transfer. After delivery.

That’s support at every stage of ownership. And it’s the difference between a transaction and a relationship that stays useful long after the paperwork is done.

The 4-Step Process, Broken Down

Every Gold IRA follows the same four steps — in the same order, with the same IRS requirements at each one. What varies is who’s coordinating the logistics on your behalf.

Here’s what each step actually involves.

Step 1 — Choose a Self-Directed IRA Custodian

Your current brokerage almost certainly can’t do this.

Traditional IRAs at firms like Fidelity, Schwab, or Vanguard are “directed” accounts — meaning the custodian controls what assets are available. Physical gold isn’t on that menu. A precious metals IRA requires a self-directed custodian: a bank, credit union, or non-bank trust company that’s been authorized by the IRS to hold alternative assets inside a retirement account.

What to look at when you’re evaluating custodians:

- IRS authorization — This should be confirmed directly. Don’t accept marketing copy as verification. Ask.

- Fee structure — Setup fees, annual maintenance fees, and sometimes asset-based fees that grow with your holdings. Understanding gold IRA fee structures before anything is signed is the difference between a surprise and a plan.

- Depository partnerships — Not all custodians work with the same approved facilities. This matters for your segregated storage options.

- Purchase timelines — Once funds are settled, how quickly can the custodian execute a metals order? Ask this question before you open the account.

Brighton Gold works with established SDIRA custodians and walks you through the options during your complimentary consultation — including how the No Fee Precious Metals IRA for the lifetime of the account works on qualified purchases.

Step 2 — Fund the Account

There are three ways to move money into a new SDIRA. Each one has a different set of IRS rules, and getting this step right protects everything that comes after it.

- Direct IRA-to-IRA transfer — The funds move institution-to-institution. You never receive a check. No tax withholding. No 60-day deadline. For most customers with existing IRAs, this is the cleanest path.

- 401(k) direct rollover — Possible in most cases, but usually only from a former employer’s plan. Current employer plans have more restrictions. We cover this in detail in moving your 401(k) to a Gold IRA without penalty.

- Annual cash contribution — Subject to IRS annual limits, which adjust periodically based on cost-of-living adjustments. Check IRS Publication 590-A for the current numbers. Owners aged 50 and over are eligible for catch-up contributions on top of the standard limit.

| Funding Method | Withholding Risk | IRS 60-Day Rule | Best For |

|---|---|---|---|

| Direct IRA-to-IRA Transfer | None | Not applicable | Customers with existing IRAs |

| Direct Rollover (401k) | None if direct | Not applicable | Former employer plan holders |

| Indirect Rollover | 20% withheld by plan | Yes — 60 days to redeposit | Rarely recommended — see Section 3 |

| Annual Cash Contribution | None | Not applicable | New contributions within IRS limits |

Step 3 — Select Your IRS-Approved Metals

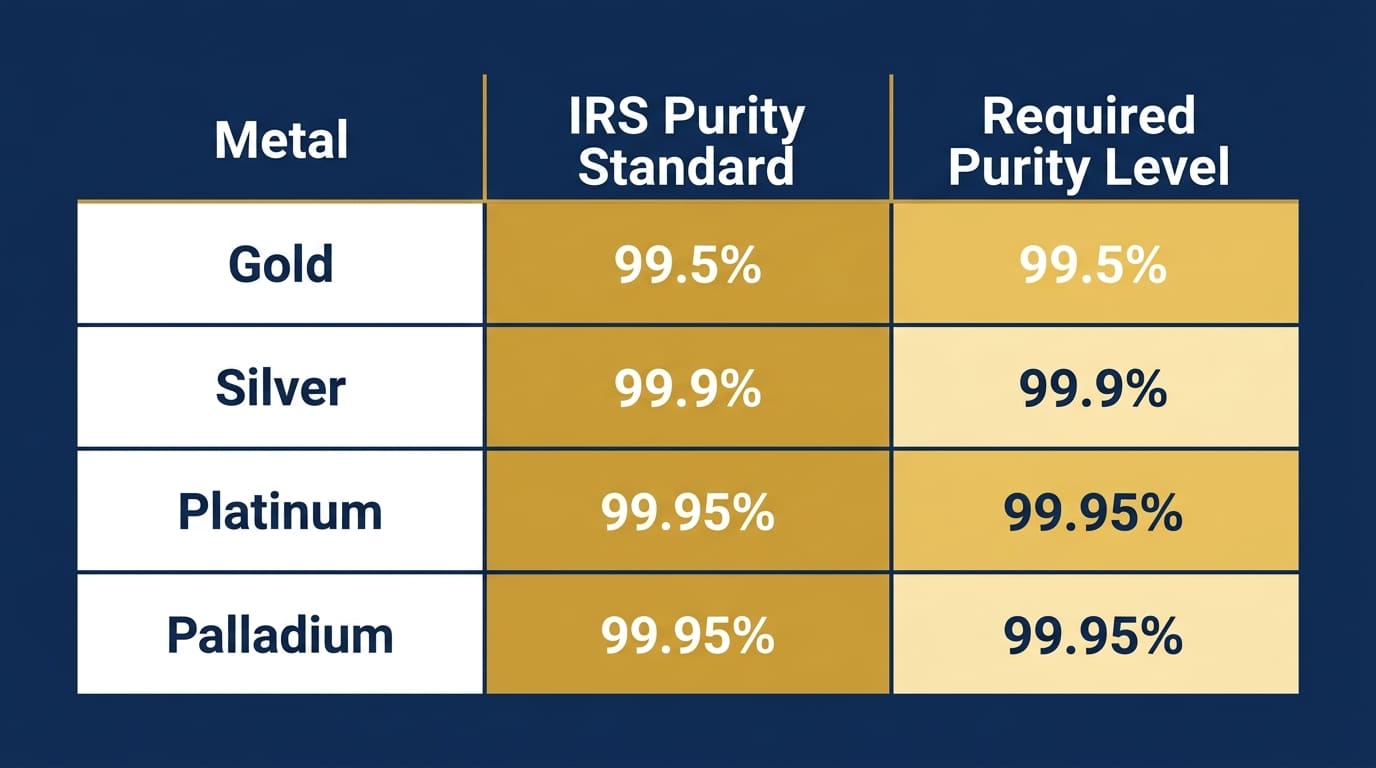

Not every gold product qualifies for an IRA. The IRS is specific: gold must meet a minimum fineness of .995 (99.5% pure). Silver requires .999. Platinum and palladium both require .9995.

| Metal | Minimum Purity | Common IRA-Approved Products |

|---|---|---|

| Gold | 99.5% (.995) | Gold American Eagle, Gold American Buffalo |

| Silver | 99.9% (.999) | Silver American Eagle, Silver American Buffalo |

| Platinum | 99.95% (.9995) | Platinum American Eagle |

| Palladium | 99.95% (.9995) | Palladium American Eagle |

The U.S. Mint produces both the Gold American Eagle and the Gold American Buffalo — the two most commonly held IRA gold products. The Eagle is technically 22-karat, but Congress specifically authorized it for IRA use because the U.S. government guarantees its one-troy-ounce gold content. The Buffalo is .9999 fine and qualifies on purity alone.

For most owners, U.S.-minted coins are the standard. Not because foreign alternatives are always disqualified — but because provenance, purity guarantees, and long-term liquidity favor American-made products in a way that’s hard to replicate offshore. If you want a deeper look at which coins make sense and why, choosing IRS-approved gold coins breaks it down.

Step 4 — Arrange Depository Storage

Physical gold inside a retirement account cannot be stored at home.

Not in a safe. Not in a safe deposit box. Not through an LLC or a trust arrangement. It must be held at an IRS-approved depository — a secure, audited, insured facility built specifically for precious metals custody.

This is not optional. An account holder who takes personal possession of IRA-held metals triggers an immediate taxable distribution — the full fair market value of those metals, treated as if it were withdrawn that day. Add taxes and potential early-withdrawal penalties if you’re under 59½ and you’re looking at a significant unplanned tax event. The understanding gold IRA storage rules guide covers how depository custody works and what your options are.

Most custodians work with established facilities like Delaware Depository or Brinks Global Services. You’ll typically choose between segregated storage — your metals held separately, identified specifically as yours — and commingled storage, where holdings are pooled. Segregated is the cleaner option for most owners.

Rollovers, Transfers, and the 20% Withholding Trap

This is where most people make a costly mistake — and it happens before a single ounce of gold is purchased.

If you’re funding a new SDIRA by moving money out of a 401(k) or existing IRA, there are two paths. One of them can cost you 20% of your retirement savings on the way to your new account. The other costs nothing and takes the same amount of time.

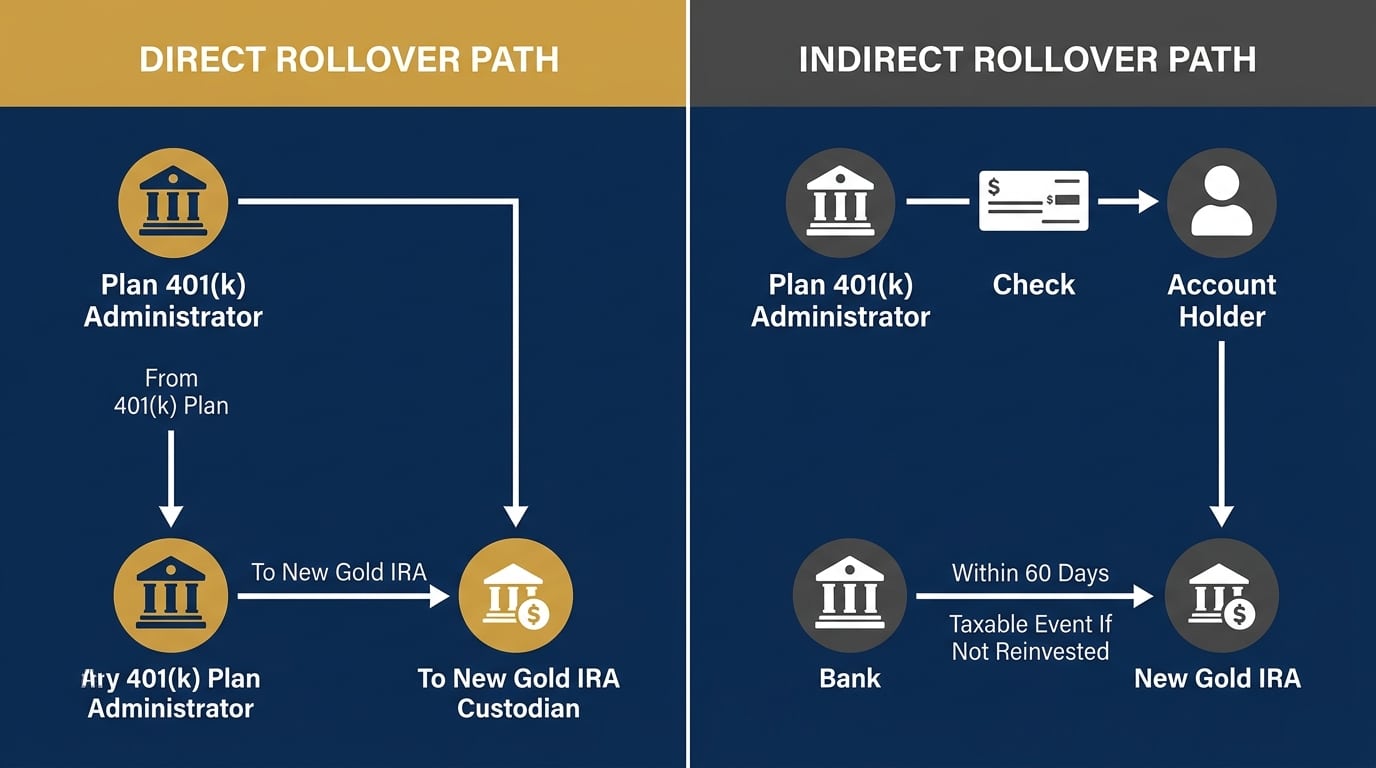

Direct vs. Indirect: The Decision That Changes the Tax Outcome

A direct rollover — sometimes called an institution-to-institution transfer — means the funds move from your old custodian straight to your new one. You never receive a check. The IRS treats the movement as a non-event: no withholding, no 60-day deadline, no tax consequence.

An indirect rollover means the old custodian cuts a check — made out to you. The moment that happens, the IRS requires the plan administrator to withhold 20% for federal taxes. You get 80 cents of every dollar. Now you have 60 days to deposit 100% of the original balance — including the 20% that was withheld — into the new account.

If you can’t cover that gap out of pocket, the withheld amount becomes a taxable distribution. Income taxes are owed on it. If you’re under 59½, a 10% early withdrawal penalty applies on top of that.

A direct rollover eliminates the problem entirely. It’s not a workaround — it’s the IRS-designed method for exactly this situation. For customers moving 401(k) funds specifically, moving your 401(k) to a Gold IRA without penalty walks through the process step by step.

What the IRS Safe Harbor Rules Give You

The IRS requires plan administrators to provide written rollover explanations before any distribution is processed. Updated requirements under SECURE 2.0 era guidance — including IRS Notice 2026-13 — are designed specifically to protect retirement account holders from the withholding trap described above.

That explanation is your right — not a favor. If you haven’t received one, ask for it before anything moves.

- You’re entitled to a written explanation of your rollover options before any funds are distributed. Request it. Read it carefully.

- The 60-day redeposit deadline is firm. The IRS does allow waivers in specific hardship situations — natural disaster, hospitalization, death of a family member — but ordinary delays don’t qualify.

- You’re allowed one indirect rollover per 12-month period across all of your IRAs combined. Not per account. Per person. Most customers never need an indirect rollover. But knowing the rule prevents a costly mistake if you ever end up in that situation.

Brighton Gold does not provide tax, legal, or financial advice. Consult your CPA or tax professional before initiating any distribution or rollover.

What the IRS Actually Requires — and What Happens If You Get It Wrong

Two IRS rules trip up more first-time Gold IRA buyers than any others. One is about what metals are eligible. The other is about where they live after you own them.

Getting either one wrong doesn’t result in a warning. It results in a tax bill.

Purity Standards, Approved Products, and the Collectibles Line

The IRS separates IRA-eligible precious metals from “collectibles” — and collectibles are prohibited from IRA ownership entirely. If you buy a collectible inside an IRA, it’s treated as a deemed distribution at the moment of purchase.

What counts as a collectible? Coins that don’t meet purity thresholds. Rare or numismatic coins valued for scarcity rather than metal content. Precious metals not produced by a national government mint or an accredited refinery.

What the IRS requires for IRA-approved gold covers the full approved product list in detail. The headline rules:

- Gold American Eagles qualify despite being 22-karat — Congress carved out a specific exemption for them.

- Gold American Buffalos are .9999 fine — they qualify on purity with room to spare.

- Foreign coins may or may not qualify depending on purity and where they were produced. Provenance matters.

- Numismatic coins don’t qualify, regardless of how much gold they contain.

Every product sold through Brighton Gold is confirmed IRS-eligible before the order is placed. That’s not an added service — it’s a standard part of how we work.

The Home Storage Myth — and What U.S. Tax Court Said About It

There’s a piece of misinformation that keeps circulating online: the idea that you can store IRA-held gold at home using something called a “home storage IRA” or “checkbook IRA” structure.

The U.S. Tax Court settled this in McNulty v. Commissioner. An account holder stored IRA-owned gold coins at home — through an LLC — and the court ruled it triggered a fully taxable distribution. The fair market value of those metals was treated as if it had been withdrawn on the day they were taken into personal possession. Combined with taxes and penalties, the resulting bill exceeded $300,000.

IRS Publication 590-A is plain on this: IRA assets must be held by a qualified trustee or custodian. The structure of the arrangement — LLC, trust, or otherwise — doesn’t change that requirement.

If a provider is marketing home storage as a legal IRA strategy, that’s not a gray area. Walk away.

Brighton Gold uses IRS-approved depositories. That’s not a policy preference. It’s a compliance requirement we treat as non-negotiable.

Who This Is For — and Who It Isn’t

A Gold IRA works well for a specific kind of retirement owner. It’s not the right fit for everyone — and we’d rather say that directly than let someone start a process that doesn’t serve them.

The customers Brighton Gold works best with share a few things in common:

- They’re at or approaching retirement, and they want to hold something tangible alongside their existing accounts — not replace them entirely.

- They’re thinking in years, not quarters. They’re not looking for a price pop. They’re looking for stability.

- They know that precious metals may appreciate, depreciate, or remain unchanged. That’s not a concern for them — it’s a baseline they’ve already accepted.

- They want a process they understand, answers that are honest, and a team that’s still reachable after the paperwork is done.

- They’re not here because someone scared them into it. They’ve thought this through.

The Speculator — Who This Relationship Isn’t Built For

One thing worth saying clearly: Brighton Gold isn’t the right fit for everyone.

If you’re here because you think gold prices are about to move and you want to get positioned before they do — we’re probably not your best option.

If you want someone to tell you that gold is guaranteed to go up, or that now is the perfect moment to buy — we can’t help you with that. No one can. Precious metals prices aren’t predictable, and any dealer who suggests otherwise isn’t being straight with you.

Brighton Gold does not forecast prices. We do not time the market. We do not make buying or selling recommendations. Our team informs, guides, and supports — they do not direct financial decisions. If you need someone to tell you what to do with your money, you need a licensed financial planner, not a precious metals dealer.

If the goal is a short-term trade — in today, out in six months — this isn’t the relationship for that.

What we’re good at is working with customers who want to hold something real for the long haul. If that’s where you are — and you want to understand what happens when you eventually retire and need to access those holdings — understanding gold IRA distribution options is the next read worth your time.

The learning center exists for the customer who wants the full picture before they commit to anything. That’s the customer this relationship is built for.

Frequently Asked Questions

How long does it actually take to set up a Gold IRA?

Most customers complete the full process — from opening the SDIRA to having metals held at an approved depository — in two to three weeks.

Here’s what that window typically looks like: the SDIRA application is completed online and is usually approved within one to three business days. Funding a direct rollover or transfer adds another five to ten business days, depending on how quickly the transferring institution processes the outgoing request. Once funds are confirmed settled, the metal purchase order is executed. Shipping and vault acceptance at the depository adds a final few business days on top of that.

The process moves faster today than it did even a few years ago — most applications and transfer forms are now handled digitally. That said, 401(k) transfers tend to move more slowly than IRA-to-IRA transfers, and the originating custodian’s internal processing speed is the variable most people underestimate when they’re planning a timeline.

Can I use a 401(k) from a current employer to fund a Gold IRA?

In most cases, no — not while you’re still employed there.

Most employer 401(k) plans don’t allow in-service distributions or rollovers to outside accounts for active employees. That’s a plan-level restriction, not an IRS prohibition — so the answer depends on what your specific plan allows.

The exception is if your plan offers an “in-service withdrawal” provision, which some plans permit after a certain age — typically 59½. Your plan documents or plan administrator can confirm whether that option exists.

Once you’ve left the employer, rolling a 401(k) into a Gold IRA through a direct rollover is straightforward. Moving your 401(k) to a Gold IRA without penalty covers the mechanics and compliance rules in full detail.

Brighton Gold does not provide tax or legal advice. Consult your CPA or tax professional about your specific plan’s terms before initiating any rollover.

What are the IRS purity standards for gold inside a retirement account?

Gold held inside an IRA must meet a minimum fineness of .995 (99.5% pure). The IRS specifies this in the tax code governing IRA-eligible precious metals.

The Gold American Eagle is a notable exception — it’s 22-karat (.9167 fine) but was specifically authorized by Congress for IRA inclusion. The Gold American Buffalo, at .9999 fine, exceeds the standard and qualifies on purity alone.

Foreign coins and rounds may qualify if they meet the purity threshold and are produced by a recognized national government mint or accredited refinery. But whether something technically qualifies and whether it’s practical to hold inside an IRA aren’t always the same question — liquidity, verifiability, and custodian acceptance all factor in. For a full look at approved products and what to consider, see choosing IRS-approved gold coins.

What happens if I store IRA gold at home by mistake?

The IRS treats it as a taxable distribution — immediately.

The moment IRA-held metals come into your personal possession, the fair market value of those metals is treated as if you withdrew that amount from the IRA. You owe income tax on that amount at your ordinary rate. If you’re under 59½, you also owe a 10% early withdrawal penalty.

This is not a technicality. The U.S. Tax Court ruled on this directly in McNulty v. Commissioner, where an account holder stored IRA gold coins at home through an LLC structure — and was hit with a tax bill exceeding $300,000. No storage method, LLC structure, or checkbook arrangement changes the underlying rule: IRA assets must be held by a qualified trustee or custodian.

If you encounter anyone marketing a “home storage IRA” as a legal structure, treat it as a significant red flag about that provider’s compliance posture.

Do I need a financial professional to set up a Gold IRA?

No. A financial professional is not a required part of the process.

What you need is a self-directed IRA custodian, an IRS-eligible precious metals dealer, and access to an approved depository. Brighton Gold’s team coordinates between all three on your behalf — you don’t have to manage three separate institutional relationships yourself.

That said, a licensed financial planner, CPA, or tax professional can be valuable for thinking through whether a Gold IRA fits your broader retirement picture, what percentage of your retirement savings makes sense to hold in physical metals, and how the tax treatment of a rollover interacts with your other accounts. Brighton Gold doesn’t provide that advice — we refer customers to their qualified professionals for those decisions.

Evaluating institutional bias against gold covers why some financial professionals actively discourage Gold IRAs — and what’s worth considering when you hear that advice.

What does it actually cost to hold a Gold IRA?

The cost structure for a Gold IRA typically includes a one-time account setup fee, annual custodian maintenance fees, and depository storage fees that are charged either as a flat rate or as a percentage of the assets held.

The full fee picture matters before you open an account — because what looks like a competitive spread on the metal purchase can be offset by ongoing annual costs that vary significantly between custodians. Understanding gold IRA fee structures breaks down what to look for, what questions to ask, and what Brighton Gold’s No Fee Precious Metals IRA for the lifetime of the account on qualified purchases actually means for your total cost of ownership.

Brighton Gold holds an A+ BBB rating and AAA BCA rating. We’re transparent about the full cost picture before anything is signed.

What happens to my Gold IRA when I retire?

When you reach retirement age and begin taking distributions from a Gold IRA, you have two options: take the metals as a physical distribution (the metals are shipped to you), or liquidate the metals first and take a cash distribution.

Required minimum distributions (RMDs) begin at age 73 under current IRS rules, and they apply to Gold IRAs the same as they do to traditional IRAs. The RMD amount is based on the fair market value of your account. Because precious metals prices fluctuate, the fair market value of the metals at the time of the RMD calculation determines the required distribution amount.

Planning ahead for how you’ll handle RMDs and distributions is part of the broader ownership picture. Understanding gold IRA distribution options walks through the mechanics in detail.

The Bottom Line

Here’s what we’ve seen, working with customers through this process: the hardest part of setting up a Gold IRA usually isn’t the process itself. It’s finding someone who will walk you through it without making it feel like a sales pitch.

Physical gold and silver exist outside the paper financial system. That distinction means something — not because of any single economic event, but because holding something real that you own outright, that’s audited and insured, and that no bank can freeze or dilute is a fundamentally different kind of ownership than a statement balance. Precious metals may appreciate, depreciate, or remain unchanged. What doesn’t change is what you hold and where it lives.

The four steps in this guide are the same for every customer. The difference is who coordinates them — and how clearly you understand each one before you commit. If you’ve read this far and the process still makes sense for where you are, the next step is a direct conversation. Not a brochure. A conversation.

If you’ve been thinking about moving part of your retirement savings into something tangible, you don’t have to piece this together on your own.

The questions that come up most often — what a rollover actually costs, whether your 401(k) qualifies, what the real difference is between a direct and indirect transfer — are exactly what Brighton Gold’s complimentary consultation is built to answer. Before anything is signed. With no pressure attached to any of it.

Brighton Gold’s team will walk you through how the process works, what the No Fee Precious Metals IRA for the lifetime of the account looks like on qualified purchases, and whether any of it fits where you are right now.

The window to act clearly is open. Not because of urgency — because the time you spend unclear is time you’re not holding something you feel good about.