Can I Move My 401(k) to a Gold IRA Without Penalty?

Yes. You can move your 401(k) to a Gold IRA without triggering the 10% early withdrawal penalty or the 20% mandatory federal tax withholding — but only if you use the right method.

That method is called a Direct Rollover, also referred to as a Trustee-to-Trustee Transfer. Here’s what it means in plain terms: your 401(k) administrator sends the funds directly to your new self-directed IRA custodian. The money never touches your personal bank account. That’s the legal shield that keeps the transaction penalty-free.

The IRS specifically designed the direct rollover to allow retirement account owners to move funds between qualified accounts without triggering a taxable distribution event. When the transfer is executed correctly, there’s nothing to withhold and no penalty to calculate.

There’s one important distinction to understand before you start. The standard direct rollover applies to funds in a former employer’s plan — the 401(k) you left behind when you changed jobs or retired. If you’re still employed and want to move your current employer’s 401(k), different rules apply. That scenario is called an “in-service distribution,” and it’s covered fully later in this article.

What this article covers: the correct way to execute a penalty-free rollover, the specific rules that govern it, what disqualifies the transaction, what happens during an indirect rollover and why it goes wrong, how to handle in-service distributions, and what ongoing ownership looks like after the transfer is complete.

The process is more straightforward than most people expect. Brighton Gold has walked customers through it since 2012. The goal here is to make sure you walk away knowing exactly what to expect — before you make a single phone call.

Last Updated: April 14, 2026

- What “Penalty-Free” Really Means — and Where Most People Go Wrong

- The Four-Step Path: From 401(k) to Physical Gold

- The Indirect Rollover: Why the Risk Is Real

- In-Service Distributions: Moving Funds While Still Employed

- Who This Process Is For — and Who It Isn’t

- After the Transfer: What Ongoing Ownership Looks Like

- Frequently Asked Questions

- The Bottom Line

What “Penalty-Free” Really Means — and Where Most People Go Wrong

The question most people are really asking isn’t “Can I move my 401(k) to a Gold IRA?”

It’s: “Can I do this without making a mistake that costs me?”

Here’s what most articles won’t tell you — the 10% penalty and the 20% federal withholding aren’t automatic. They’re the outcome of using the wrong method. Use the right one, and neither applies.

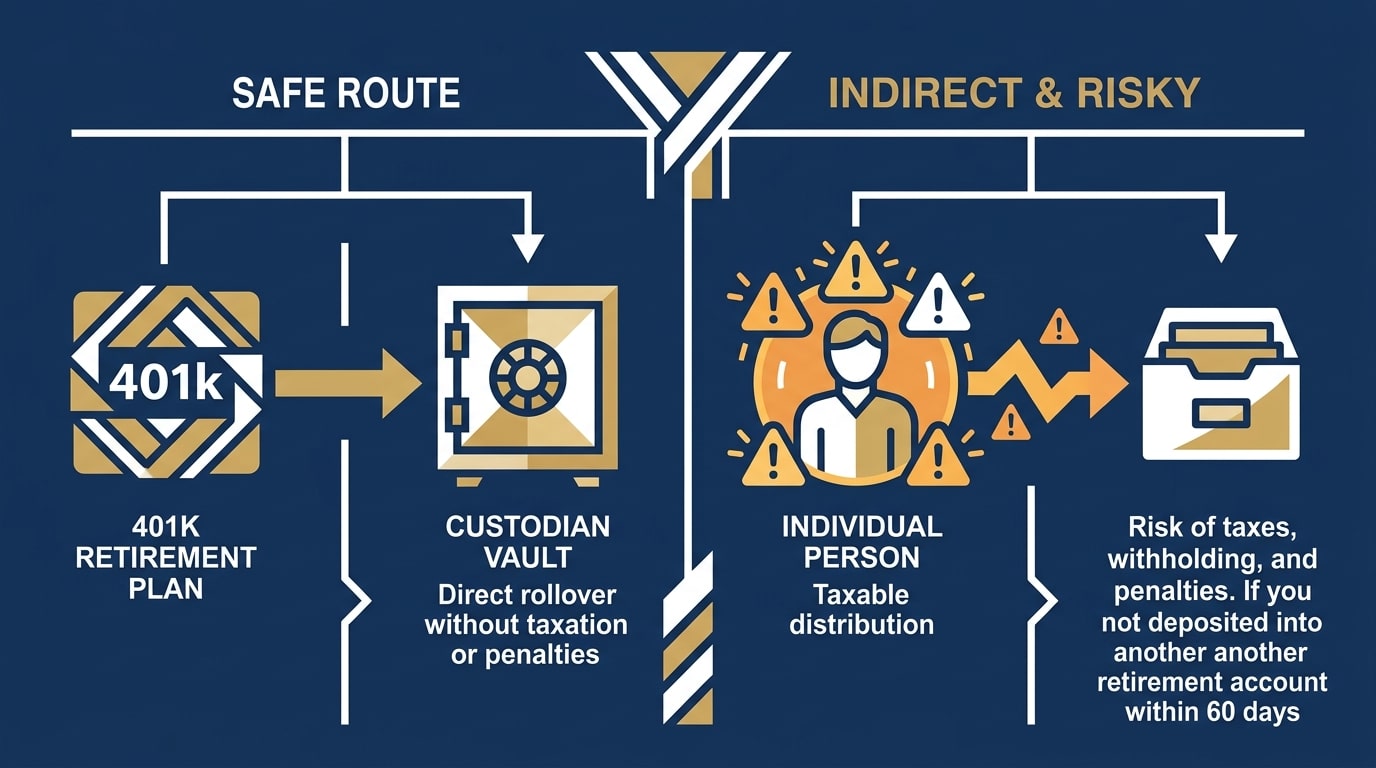

The Two Methods: Direct vs. Indirect

There are exactly two ways to move funds from a 401(k) into a self-directed IRA. The method you choose determines whether the transfer is penalty-free or taxable — and the difference isn’t subtle.

| Direct Rollover | Indirect Rollover | |

|---|---|---|

| How funds move | Administrator sends directly to new custodian — you never handle the money | Check issued to you first — you deposit it later |

| Tax withholding | None — transfer isn’t treated as a distribution | 20% mandatory federal withholding on the amount issued |

| IRS deadline | No deadline — funds move between institutions | 60 days from receipt to deposit the full original amount |

| Penalty risk | None when executed correctly | High — withheld amounts and missed deadlines both trigger penalties |

| Brighton Gold’s approach | Yes — the correct path | No — too many failure points |

The direct rollover is the right path. There’s no scenario where the indirect method offers a meaningful advantage over it.

The 20% Withholding Trap — What It Actually Looks Like

Here’s where the indirect rollover causes real damage — and it does so in a way that’s nearly invisible until it’s too late.

When a 401(k) administrator issues a check for an indirect rollover, they’re legally required to withhold 20% for federal taxes. So if your 401(k) holds $100,000, the check arrives for $80,000.

The problem — you must deposit the full $100,000 into the new account within 60 days to avoid a taxable event. Not just the $80,000 you received. The full amount. The missing $20,000 has to come from your own pocket.

Most people don’t have that cushion sitting around.

- $100,000 in your 401(k) — the check arrives for $80,000. The 20% goes to the IRS before you ever see it.

- 60 days to deposit the full original amount — not just the $80,000 received. The complete $100,000 must go in.

- The missing $20,000 must come from personal funds — if it doesn’t, the shortfall is treated as a taxable distribution immediately.

- Ordinary tax plus a 10% penalty — if you’re under 59½, both apply at once.

That’s a significant and avoidable cost. The direct rollover eliminates it entirely.

The Complexity Around This Topic Isn’t an Accident

The rollover process has a reputation for complexity it doesn’t deserve.

Custodian fees. IRS-approved metals lists. Storage requirements. Depository options. Most resources pile all of it on you at once — and leave you more confused than when you started.

We’ve seen this pattern for over a decade. A customer who feels overwhelmed is more likely to stall. More likely to accept terms they don’t fully understand. More likely to stay in the system they already know.

Our approach is the opposite. From a customer’s perspective, executing a penalty-free 401k rollover comes down to three decisions: open an account, request the transfer, select your metals. Everything else is handled on your behalf.

That clarity is the service — not complexity dressed up as expertise.

For those researching understanding gold IRA funding methods before making that first call, that guide covers both paths in detail.

Those considering Brighton Gold’s precious metals IRA structure will find a full overview of the account type, eligible metals, and how the No Fee IRA works.

The Four-Step Path: From 401(k) to Physical Gold

If you’re ready to do this correctly, the process follows a clear sequence.

Nathaniel Cross, Director of Research at Brighton Gold, puts it this way: the customer’s job is to initiate and confirm. The custodians and administrators handle the mechanics.

Here’s what that actually looks like.

Step 1 — Open a Self-Directed IRA

A standard IRA held at a brokerage can’t hold physical precious metals. You need a self-directed IRA (SDIRA) — specifically, one with a custodian approved to hold alternative assets like physical gold, silver, platinum, and palladium.

The SDIRA custodian acts as the compliance gatekeeper. They ensure the account meets IRS requirements under IRS Publication 590-A, including asset eligibility and reporting standards.

- Choose a qualified custodian — Per SEC Rule 206(4)-2, physical assets in qualified accounts must be held by an approved custodian. This isn’t a preference — a non-qualified arrangement can invalidate the account entirely.

- Complete the application — Name, identification, beneficiary designation. Most customers complete this in under 30 minutes.

- Receive your account number — You’ll need this for the next step.

Customers who want a full walkthrough of how to set up a Gold IRA — from account selection through first purchase — will find the complete sequence covered there.

Step 2 — Request a Direct Rollover from Your 401(k) Administrator

This is the step where the penalty-free protection is established.

You contact your 401(k) plan administrator and request a Direct Rollover — a Trustee-to-Trustee Transfer. That specific framing matters.

- Submit the Letter of Authorization (LOA) — Your SDIRA custodian provides this. You submit it to the 401(k) administrator. It instructs them to wire the funds directly to the new custodian — not to you.

- Specify the destination account — The LOA includes your SDIRA account number and the custodian’s wire instructions.

- Confirm the transfer type in writing — Get it on record as a direct rollover, not a distribution. This triggers zero withholding on the administrator’s end.

The funds never touch your personal account. That’s the legal protection. No timing. No deposits. No 60-day clock.

Step 3 — Funds Are Wired to the New Custodian

Once the administrator processes the LOA, the funds go directly to your SDIRA custodian. Transfer timelines vary by plan — typically 5 to 15 business days.

During this window, the funds are in transit. No metals have been purchased yet. That’s normal.

- Track the transfer — Your SDIRA custodian confirms when the funds arrive and are credited.

- No deadline pressure — Because no check was issued to you, there’s no 60-day window and no penalty exposure during transit.

Step 4 — Select IRS-Approved Metals

Once the funds are credited, you select what to purchase. The IRS sets specific purity standards for metals held inside a retirement account.

| Metal | Minimum Purity | Common IRS-Approved Examples |

|---|---|---|

| Gold | 99.5% | Gold American Eagle, Gold American Buffalo, certain gold bars |

| Silver | 99.9% | Silver American Eagle, Silver American Buffalo |

| Platinum | 99.95% | Platinum American Eagle, approved bars |

| Palladium | 99.95% | Palladium American Eagle, approved bars |

U.S.-minted products are the standard at Brighton Gold. Provenance, purity, and liquidity all matter to serious owners — and U.S.-minted coins deliver on all three.

Customers researching choosing IRS-approved gold coins will find a breakdown of eligible options — including the Gold American Eagle and Gold American Buffalo — with details on why each qualifies.

The metals are purchased through the dealer and held in your name at an IRS-approved depository. Your property. Not the custodian’s. Not the dealer’s.

The Indirect Rollover: Why the Risk Is Real

The indirect rollover is a legal option. It exists in the IRS rulebook.

It’s also one of the most consistent ways to turn a straightforward retirement account transfer into a costly — and in many cases irreversible — mistake.

Understanding exactly how it fails before you start any rollover conversation is worth your time.

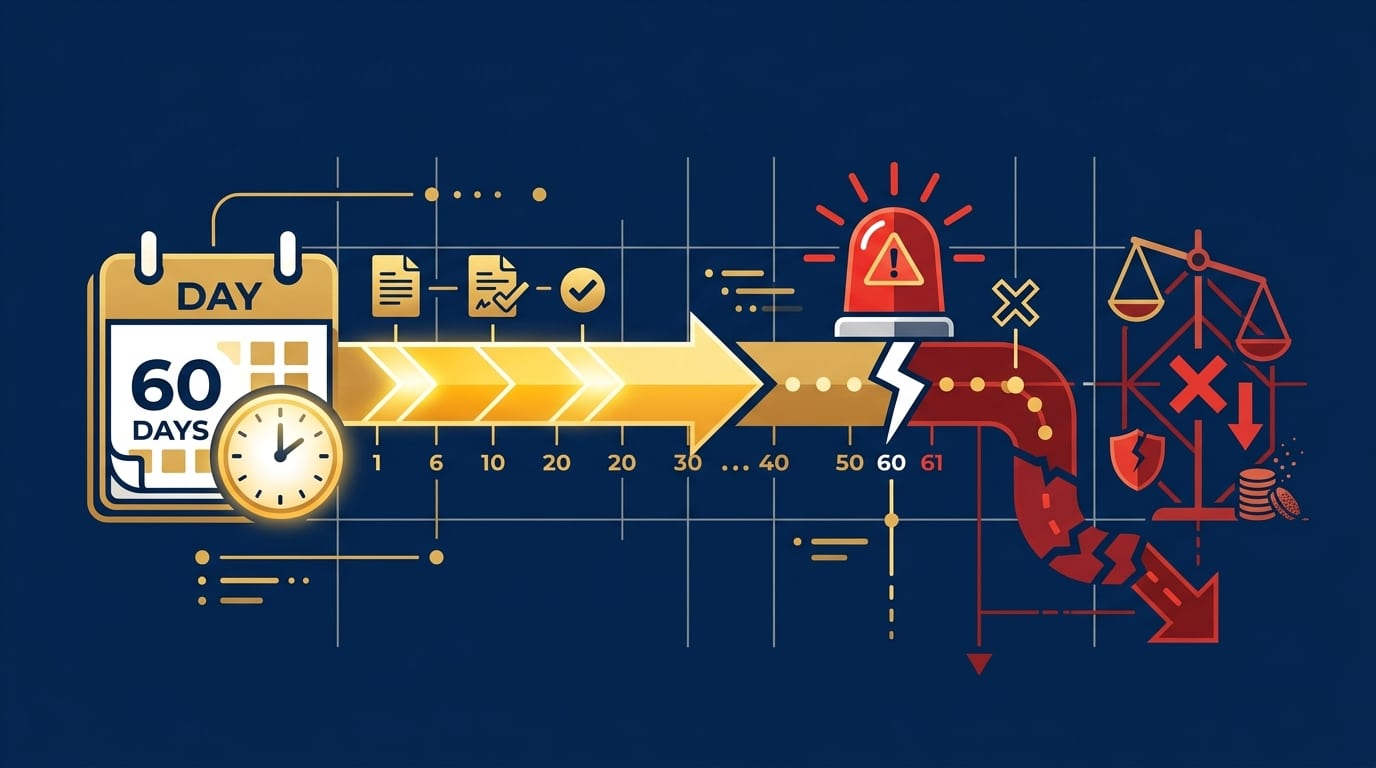

Why the 60-Day Rule Is a Deadline, Not a Safety Net

Under IRS Publication 590-A, if you receive a distribution from a retirement account and want to treat it as a rollover, you have 60 days to deposit it into another qualified account.

That sounds workable. Here’s what actually happens:

- Your 401(k) administrator issues a check payable to you — not to the custodian

- 20% is withheld automatically for federal taxes

- You have 60 days to deposit the full original amount — including the withheld 20% — into the new account

- Deposit only the 80% you received — the missing 20% is treated as a taxable distribution immediately

Rollover guidance under IRS Notice 2026-13 updated safe harbor explanations for retirement distributions under SECURE 2.0 — but the 60-day rule and the 20% mandatory withholding mechanism remain fully in effect.

The math works against most people. And that’s before the deadline becomes a factor.

What Happens When the 60-Day Window Closes

Miss the deadline — the entire distributed amount becomes a taxable distribution. No grace period. No negotiation.

- Ordinary tax on the full distributed amount at your current marginal rate

- A 10% early withdrawal penalty if you’re under 59½

- No correction available once 60 days pass — barring a narrow IRS hardship waiver process that most people don’t qualify for

The IRS does allow a self-certification procedure for certain missed deadlines. The qualifying reasons are limited and require documentation. It’s a narrow exception — not a safety net. Don’t plan around it.

The One-Rollover-Per-Year Rule

There’s a second constraint that catches people who use the indirect method repeatedly.

The U.S. Tax Court ruling in Bobrow v. Commissioner established that the one-rollover-per-year rule applies across all of a taxpayer’s IRAs in aggregate — not per individual account. Take an indirect rollover from any IRA in a 12-month window, and no other indirect rollover from any other IRA is permitted in that same period.

This rule doesn’t apply to direct Trustee-to-Trustee transfers.

One more reason to avoid the indirect method altogether.

For those comparing executing a precious metals IRA rollover to a standard IRA transfer, that guide covers both paths mechanically.

In-Service Distributions: Moving Funds While Still Employed

One of the most common questions we hear — and one of the most misunderstood areas of rollover rules — is whether you can move your current employer’s 401(k) to a Gold IRA while you’re still on payroll.

The short answer: sometimes yes. But the rules are different, and eligibility depends entirely on your specific plan.

What an In-Service Distribution Is — and Who Qualifies

An in-service distribution allows an active employee to take a distribution — or in some cases, execute a rollover — from their current employer’s 401(k) while still employed.

Not all plans allow it. The option lives in your plan document — the specific rules your employer’s 401(k) has adopted. If the plan doesn’t permit it, the option doesn’t exist regardless of your age or account balance.

- Age threshold — Most plans that permit in-service distributions require the participant to be at least 59½. Some plans allow earlier access under narrow hardship criteria, but 59½ is the standard threshold for penalty-free eligibility.

- Plan permission required — Even at the eligible age, the plan must explicitly allow in-service distributions. This isn’t automatic.

- Your employer’s personal approval isn’t required — If the plan permits them, you don’t need your manager’s sign-off or HR’s blessing. You need the plan administrator’s cooperation — not your employer’s opinion on the matter.

| Situation | Rollover Available? | Key Condition |

|---|---|---|

| Former employer plan, any age | Yes | Standard direct rollover rules apply |

| Current employer plan, under 59½ | Usually No | Narrow hardship exceptions only; plan-specific |

| Current employer plan, 59½ or older | Often Yes | Plan must explicitly permit in-service distributions |

| Roth 401(k) to Roth IRA | Yes | No taxable event; same direct rollover mechanics apply |

What to Confirm Before You Start Anything

Think you qualify? Start with documentation — not the application.

- Request your Summary Plan Description (SPD) — This document outlines every rule governing your plan, including in-service distribution eligibility and any restrictions on partial transfers.

- Get confirmation in writing — Before any paperwork is initiated, get written confirmation of your eligibility from the plan administrator. A verbal “you should be fine” won’t protect you if the terms are different.

- Have your SDIRA open before you request the distribution — Delays in account setup can create timing complications. Be ready before you make the call.

For those working through the depository and custodian setup that follows a distribution, understanding gold IRA storage rules covers what to expect on the other side.

Who This Process Is For — and Who It Isn’t

The direct rollover process works. It’s legal, well-documented, and used by a significant number of retirement account owners every year.

But it’s not right for every situation — and being upfront about that is how Brighton Gold operates.

This Is Not for Speculators

If you’re looking at a 401(k) rollover to a Gold IRA because you think gold prices are headed higher and you want to capture that move — this process isn’t designed for that goal, and Brighton Gold isn’t the right partner for it.

We don’t forecast prices. We don’t time markets. We don’t provide recommendations on when to buy or sell. Precious metals may appreciate, depreciate, or remain unchanged — and we say that plainly, every time, because customers deserve to hear it before anything is signed.

The behavior we’re describing — specifically:

- Looking for price forecasts or market timing guidance — Brighton Gold doesn’t provide that. No one reliably can.

- Evaluating a Gold IRA based on near-term price movement expectations — metals for a six-month trade and metals for long-term ownership are two fundamentally different decisions.

- Wanting someone to tell you whether “now” is the right time to buy — that question has no honest answer we can give.

The owners who get the most from this process aren’t asking whether gold will go up. They’re asking how to hold something real — something outside the paper financial system, not dependent on a bank’s solvency or a government’s printing decisions.

If you’re looking for a short-term trade — metals today, a sale in six months when the price moves — Brighton Gold isn’t your best option, and we’d tell you that directly.

This Is Not a Substitute for Tax or Legal Guidance

A Gold IRA rollover is a retirement account transfer — not a tax strategy, not a cash flow shelter, and not a replacement for working with a licensed CPA or tax professional.

Brighton Gold doesn’t provide financial, tax, or legal guidance. That’s not a disclaimer buried in fine print. It’s how we’re structured — and how we’ve operated since 2012.

If you have questions about the specific tax implications of your rollover — the account type, the RMD exposure, the timing relative to other IRA activity — those belong with your CPA.

Brighton Gold explains the mechanics. Your tax professional handles the strategy.

For those who’ve raised concerns about whether Gold IRA providers are legitimate and how to tell the trustworthy ones from the bad actors, identifying safe gold IRA practices addresses the most common red flags directly.

And for a broader view of how a Gold IRA transfer works — the full picture from application through metal acquisition — that guide covers the complete sequence.

After the Transfer: What Ongoing Ownership Looks Like

Getting the funds into your self-directed IRA is the mechanics.

What comes after is ownership — and that’s where most of the real questions actually live.

Most of the anxiety around the rollover process isn’t about the transfer itself. It’s about what follows: the depository, the statements, the fees, the RMD exposure. These are legitimate things to understand before you start — not questions to figure out after.

Storage and Depository Requirements

Physical metals held in a self-directed IRA can’t be stored at home. Not in a personal safe. Not in a safe deposit box. This isn’t a preference — it’s a legal requirement.

Per SEC Rule 206(4)-2, physical assets in qualified accounts must be maintained by a qualified custodian or their approved depository. Storing IRA-held metals yourself — even temporarily — is treated as a distribution. Taxes and penalties apply immediately.

- The depository holds your metals in your name — You’re the owner. The depository is the physical custodian of the property, not the beneficial owner.

- Segregated vs. commingled storage — Most IRS-approved depositories offer both. Segregated storage means your specific coins or bars are held separately under your name. Commingled means equivalent weights are tracked but not individually assigned.

- Annual fees apply — Storage isn’t free, and cost structures vary by depository and storage type. Understanding gold IRA fee structures breaks down what to budget for — setup, annual custodian, storage, and transaction costs — before anything is signed.

Required Minimum Distributions from a Gold IRA

If you’re 73 or older, Required Minimum Distributions (RMDs) apply to traditional IRA balances — and a self-directed Gold IRA is no exception.

RMDs from a Gold IRA can be satisfied two ways.

A cash distribution — a portion of the metals is sold, and the proceeds are distributed. Or an in-kind distribution — physical metals equal to the RMD amount are delivered to you directly.

The in-kind option matters to customers who want to maintain physical possession as part of their legacy planning. Receiving the actual coins — not a cash equivalent — keeps the metals in hand.

- RMD calculation requires fair market valuation — The metals must be independently valued at year-end to establish the RMD amount.

- Coordinate early — Depositories and custodians need time to process RMD requests. Waiting until December creates pressure that doesn’t need to exist.

- Your CPA handles the strategy — RMD timing, sequencing across multiple accounts, tax implications — these are tax-specific decisions. Brighton Gold supports the mechanics. Strategy is your CPA’s call.

Brighton Gold’s broader educational resources — guides on depository options, custodian selection, and ongoing account management — are all available through Brighton Gold’s learning center.

Frequently Asked Questions

What is the 60-day rule for a Gold IRA rollover — and why does it matter?

The 60-day rule applies only to indirect rollovers — situations where the retirement account funds are paid out to you first rather than transferred directly between custodians.

If your 401(k) administrator issues a check in your name, you have 60 days to deposit the full original amount — including the 20% that was withheld — into a qualified account. Miss that window, and the entire amount is treated as a taxable distribution. That triggers ordinary tax on the full balance, plus a 10% penalty if you’re under 59½.

The direct rollover — Trustee-to-Trustee Transfer — eliminates the 60-day clock entirely. The funds never reach your account, so no deadline applies.

The 60-day rule isn’t a cushion. It’s a hard deadline with permanent consequences. The simplest way to avoid it is to never trigger it in the first place.

Can I move just part of my 401(k) to a Gold IRA, or does it have to be the full balance?

Partial rollovers are permitted. You are not required to move the entire 401(k) balance into a self-directed IRA.

Most customers exploring understanding gold IRA funding methods ask exactly this — whether they can move a portion while leaving the rest in the original plan. The answer is yes, with one caveat: your 401(k) plan document governs whether partial distributions are allowed. Some plans require a full distribution upon separation from service. Confirm the terms with your plan administrator before initiating anything.

Does my current employer have to approve the rollover?

If you’re rolling over a former employer’s 401(k), your current employer has no involvement. The transfer is between your old plan administrator and your new SDIRA custodian.

If you’re still employed and attempting an in-service distribution, the question shifts to the plan itself — not your employer personally. You don’t need your manager’s sign-off. But the plan document must explicitly permit in-service distributions. If it doesn’t, the option isn’t available regardless of how your employer feels about it. Start with your Summary Plan Description.

Is there a difference between a “Direct Rollover” and a “Trustee-to-Trustee Transfer”?

These terms are often used interchangeably — and for most practical purposes, they describe the same fundamental mechanic: funds moving directly between financial institutions without the account owner ever handling the money.

The technical distinction is narrow. “Direct Rollover” typically refers to movement from a qualified plan (like a 401(k)) into an IRA. “Trustee-to-Trustee Transfer” technically describes movement between two IRAs. Both produce the same result: no withholding, no 60-day window, no penalty exposure when executed correctly.

What matters is the outcome, not the label. If the funds never arrive in your personal account, the transaction is protected.

What does a 401(k)-to-Gold-IRA rollover actually cost?

There are several cost layers to understand before you start:

- SDIRA setup fee — A one-time fee charged by the custodian to open the account. Varies by provider.

- Annual custodian fee — Ongoing administrative fee for maintaining the SDIRA. Varies by custodian and account balance.

- Storage fee — Charged by the depository for holding the physical metals. Segregated storage typically costs more than commingled.

- Transaction fee — Charged per purchase or sale of metals within the account.

Brighton Gold offers a No Fee Precious Metals IRA for the lifetime of the account on qualified purchases. That structure eliminates several cost layers that other arrangements carry. For a full line-item breakdown of what to budget across all fee categories, understanding gold IRA fee structures covers each one specifically.

What if I already have an existing IRA — can I still roll my 401(k) into a separate Gold IRA?

Yes. An existing IRA does not prevent you from opening a self-directed IRA and funding it via rollover from a separate 401(k). The accounts are treated independently for rollover purposes.

One important note: the one-rollover-per-year rule established in Bobrow v. Commissioner applies to indirect rollovers across all IRAs in aggregate — not per account. If you use the direct method for all transfers, this limitation doesn’t affect you.

If you’re also considering moving funds from an existing traditional IRA rather than a 401(k), the mechanics differ slightly. How a Gold IRA transfer works covers the IRA-to-IRA path and how it compares to the 401(k) rollover process outlined here.

The Bottom Line

Moving a 401(k) to a Gold IRA without penalty isn’t complicated. It requires one correct decision at the start — use the direct rollover — and then following each step in order.

The penalty and the withholding aren’t inevitable. They’re the outcome of using the wrong method. The Trustee-to-Trustee Transfer removes both risks from the equation entirely.

What this process gives you isn’t a price movement guarantee. Precious metals may appreciate, depreciate, or remain unchanged — and anyone who tells you otherwise isn’t being straight with you. What it gives you is ownership — tangible, physical, held in your name — outside the paper financial system. For customers who’ve spent decades building what they have, that distinction carries real weight.

Brighton Gold has walked customers through this since 2012. The mechanics haven’t changed. The clarity we provide around them has only gotten stronger. If you want to know whether this fits where you are, a conversation is the right next step.

If you’ve been thinking about moving part of your retirement savings into something tangible — and you’re not sure where your specific situation fits — you don’t have to figure that out alone.

Most customers who reach Brighton Gold have already done the research. What they’re looking for is someone who’ll walk through the details of their rollover directly, without a sales pitch and without pressure.

That’s exactly what our complimentary consultation covers — including how the No Fee Precious Metals IRA for the lifetime of the account works and whether you qualify based on what you’re currently holding.

Explore the No Fee IRA Structure

The window to act thoughtfully is open. Not because urgency is the point — but because clarity costs nothing, and decisions made from a clear position hold up better over time.