Gold IRA Rollover vs. Transfer: What’s the Difference? (2026 Guide)

If you’ve been thinking about moving your retirement savings into physical gold, you’ve probably run into two terms — “rollover” and “transfer.”

They sound like the same thing.

They’re not. And choosing the wrong method could mean an unexpected tax bill, a missed deadline, or a penalty you didn’t see coming.

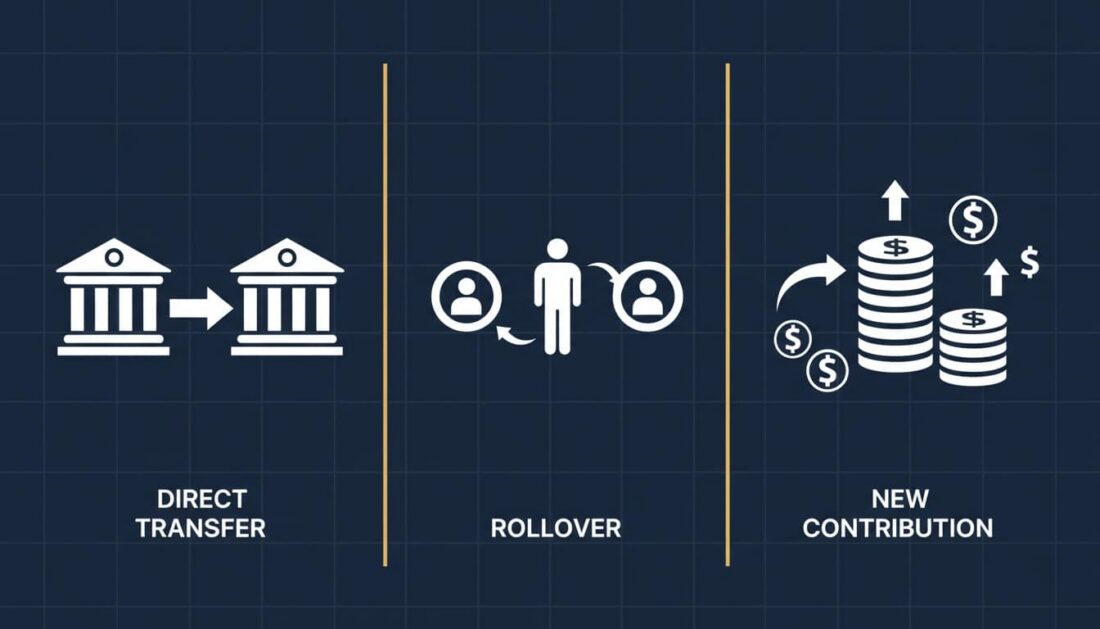

A Gold IRA transfer moves funds directly between two IRA custodians. The money never touches your hands. No taxes withheld. No deadlines. No annual limits.

A Gold IRA rollover moves funds from an employer plan — like a 401(k) or TSP — into a self-directed IRA. Depending on how it’s handled, it can come with a 60-day deadline, a 20% tax withholding, and a strict once-per-year rule.

So which one gives you the most control over how your money moves?

With gold trading above $5,000 per ounce in February 2026, the answer often comes down to speed, clarity, and tax efficiency. The right method is usually simpler than people expect — especially when you’re executing a precious metals IRA rollover with the right guidance.

Here’s what we’re seeing today.

The Quick Answer

| Direct Transfer | Direct Rollover | Indirect Rollover | |

|---|---|---|---|

| Best For | Moving an existing IRA into a Gold IRA | Moving a 401(k) or TSP into a Gold IRA | Last resort — when no direct option exists |

| Tax Risk | None | None | High — 20% withholding, 60-day deadline |

| Our Recommendation | First choice for IRA owners | First choice for employer plan holders | Avoid if possible |

How Each Method Actually Works

Most people use “rollover” and “transfer” interchangeably. The IRS doesn’t.

That distinction can mean the difference between a seamless, tax-free move — and an unexpected tax bill.

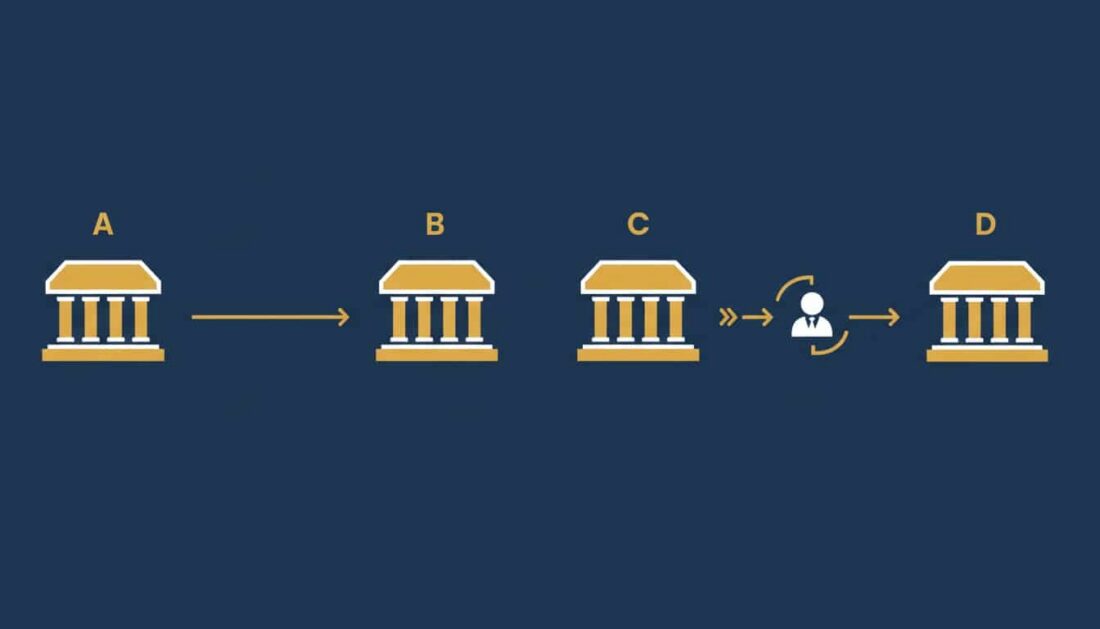

What Is a Gold IRA Transfer?

A transfer — sometimes called a “trustee-to-trustee transfer” — moves IRA funds directly from one custodian to another.

You never see the money. You never hold it. That’s the whole point.

In practice, here’s how it works:

- You contact your new self-directed IRA custodian — They provide a simple authorization form. You sign it. That’s your only step.

- Your current custodian sends the funds directly — The money moves electronically — or by check made payable to the new custodian. Not to you.

- Nothing to report to the IRS — Because the funds never hit your personal account, it’s not a taxable event. No Form 1099-R. No extra line items on your return.

The IRS has drawn this line clearly. A direct custodian-to-custodian transfer isn’t considered a rollover — and that means none of the rollover restrictions apply.

No 60-day deadline. No once-per-year limit. No withholding.

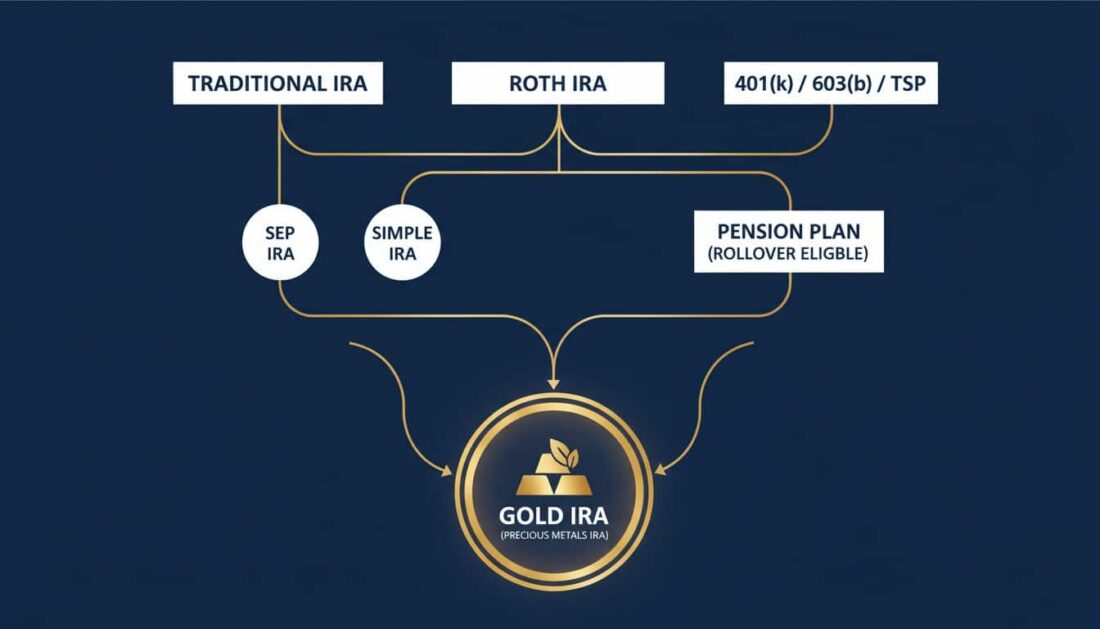

If you already have a Traditional IRA, SEP IRA, or another self-directed IRA — a transfer is almost always the cleanest path to a Gold IRA.

What Is a Gold IRA Rollover?

A rollover typically moves funds from an employer-sponsored plan — a 401(k), 403(b), TSP, or 457(b) — into an IRA.

There are two types. They work very differently.

- Direct rollover — Your plan administrator sends the funds straight to your new Gold IRA custodian. You never receive the money personally. No taxes withheld. This is the most common — and most recommended — method for executing a penalty-free 401k rollover.

- Indirect rollover — Your plan administrator cuts a check to you. You now have 60 days to deposit the full amount into a new retirement account. And if it comes from an employer plan, they’re required to withhold 20% for federal income taxes — even if you plan to roll over every dollar.

That 20% withholding is where most people run into trouble.

Say your 401(k) distribution is $100,000. You’ll only receive $80,000. To complete the rollover and avoid taxes, you’d need to come up with that missing $20,000 from your own pocket.

You’d get the withheld amount back when you file your return — but only if the full rollover was completed on time.

What happens if you miss that 60-day window? The IRS treats the entire amount as taxable income. And if you’re under 59½, you could be looking at an additional 10% early withdrawal penalty on top of it.

That’s a steep price for a paperwork mistake.

The One-Per-Year Rule: Why This Catches People Off Guard

There’s one IRS rule that trips up more people than almost anything else when it comes to moving retirement funds.

And it only applies to indirect rollovers.

How the 12-Month Clock Works

Since 2015, the IRS has limited you to one indirect IRA-to-IRA rollover every 12 months. That’s not per account — it’s across all your IRAs combined. Traditional, Roth, SEP, SIMPLE — they all count together.

And the 12-month clock starts on the date you receive the distribution.

Not the date you roll it over. Not January 1st of the following year.

Here’s a quick example. You take an IRA distribution on March 1, 2026, and roll it over on April 15. When can you do another indirect rollover? Not April 16, 2027 — it’s March 2, 2027. Twelve months from the original distribution.

A new calendar year doesn’t reset anything. The clock is strict.

Where did this rule come from? A 2014 Tax Court case — Bobrow v. Commissioner. Before that decision, the restriction applied per IRA. Now it applies per person — regardless of how many accounts you own.

What This Means If You Own a Gold IRA

If you’ve done an indirect IRA-to-IRA rollover in the past 12 months, you can’t do another one without tax consequences.

A second indirect rollover during that window? It gets treated as a taxable distribution — and could trigger the 10% early withdrawal penalty.

But here’s the part most people miss — direct trustee-to-trustee transfers aren’t subject to this rule at all. You can do as many direct transfers as you need in a single year. There’s no cap.

That’s one of the biggest reasons Brighton — and most experienced precious metals dealers — recommend a direct transfer whenever the option’s available.

Side-by-Side: How the Three Methods Compare

Sometimes a table tells the story better than paragraphs can.

How the Three Methods Stack Up

| Feature | IRA Transfer | Direct Rollover | Indirect Rollover |

|---|---|---|---|

| Fund Source | Existing IRA to new IRA | Employer plan (401k, TSP, 403b) to IRA | Employer plan or IRA to you, then to IRA |

| Who Handles the Funds | Custodian to custodian | Plan administrator to custodian | You receive the check personally |

| Tax Withholding | None | None | 20% mandatory (employer plans) or 10% default (IRAs) |

| 60-Day Deadline | No | No | Yes — strict |

| One-Per-Year Limit | No limit | Not subject to IRA limit | Yes — one per 12 months (IRA-to-IRA) |

| IRS Reporting | Not required | Form 1099-R issued | Form 1099-R issued |

| Risk Level | Lowest | Low | Highest |

| Typical Timeline | 1–3 weeks | 1–4 weeks | Varies (plus your 60-day window) |

The short version? Request a direct transfer for IRA-to-IRA moves. Request a direct rollover for employer plans. And treat an indirect rollover as a last resort — not a first choice.

Which Method Fits Your Situation?

Not every account works the same way. Here’s a simple way to think through it:

- You have a Traditional IRA or self-directed IRA at another custodian — A direct transfer is the simplest path. No withholding, no limits, no deadline.

- You’re leaving a job and have a 401(k) or TSP — Ask your plan administrator for a direct rollover to your new Gold IRA custodian. Make sure the check is payable to the custodian — not to you.

- You want temporary access to the funds — An indirect rollover technically gives you possession for up to 60 days. But the risks are real. This should be a last resort.

Brighton’s concierge team handles the coordination between custodians and plan administrators — so you’re not chasing paperwork between institutions on your own.

Why the Speed of Your Move Matters Right Now

Gold has moved fast this year.

The metal crossed $5,000 per ounce for the first time in history in late January. It reached an all-time high near $5,595. And as of mid-February 2026, it’s trading around $5,040 — up more than $2,100 from a year ago.

When prices move that quickly, the method you choose to fund your Gold IRA isn’t just a paperwork decision. It’s a timing decision.

Why Direct Transfers Help You Get Positioned Faster

A direct transfer between custodians typically takes one to three weeks. Once the funds arrive, you can purchase IRS-approved metals right away.

An indirect rollover? That introduces delays. Waiting for a check. Depositing it. Waiting for the new custodian to process your contribution. All while the 60-day clock is running — and gold prices are moving.

In a market where prices can swing $100–200 in a single session, that extra time carries real weight.

What’s Driving Gold Prices in 2026

Here’s what we’re seeing right now:

- Central bank buying stayed historically elevated — According to the World Gold Council, central banks purchased 863 tonnes of gold in 2025 — well above the 2010–2021 annual average of 473 tonnes. Poland alone added 102 tonnes. Brazil re-entered the market for the first time since 2021.

- Total global gold demand crossed 5,000 tonnes for the first time — The total value reached a record $555 billion in 2025, driven by gold-backed ETF inflows of 801 tonnes, per World Gold Council data.

- De-dollarization pressures keep building — Reserve managers around the world are moving away from U.S. dollar-denominated holdings — and that trend is providing long-term structural support for gold.

Does that mean gold will keep going up? Not necessarily. Precious metals may appreciate, depreciate, or remain unchanged — that’s always the reality.

But it does explain why so many Americans are looking to secure their retirement savings in physical metals right now. And why the speed and tax efficiency of that move matters.

What You Can Do: How to Fund Your Gold IRA Step by Step

Whether you’re moving an existing IRA or rolling over a 401(k), the process follows the same basic path.

It’s more straightforward than most people expect.

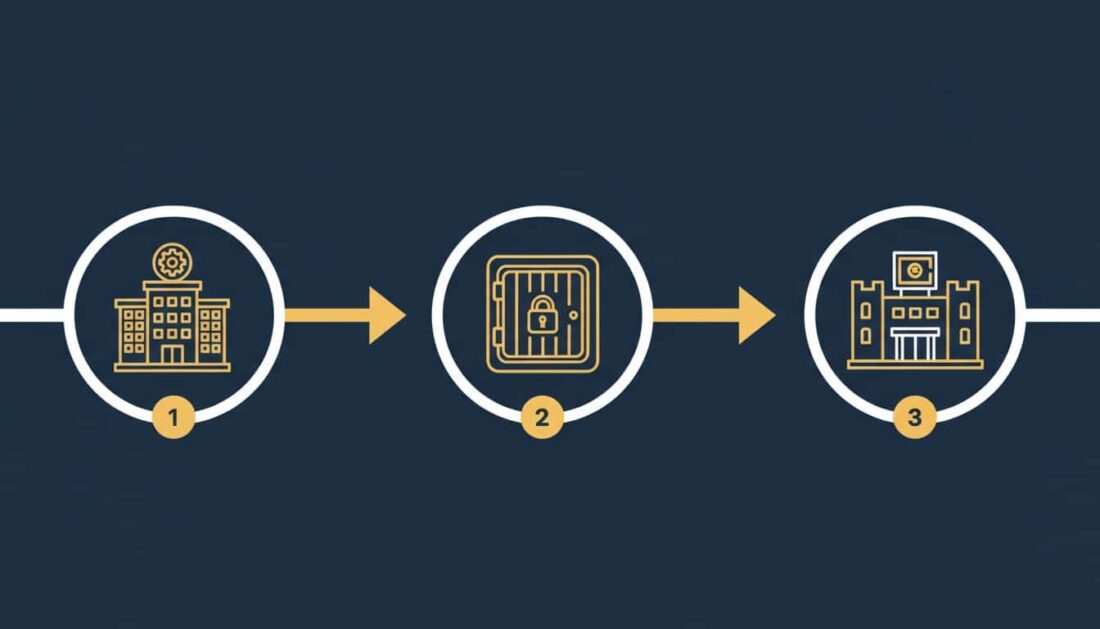

Step 1: Open a Self-Directed IRA

A standard IRA at a bank or brokerage won’t allow precious metals. You’ll need a self-directed IRA with a custodian that specifically permits physical gold and silver.

What does the custodian actually do? They hold the account, process transactions, and handle IRS compliance. They don’t provide financial guidance — that’s not their role.

Brighton works with established, IRS-approved custodians to make the account setup seamless.

One thing worth knowing — for 2026, the IRS allows contributions of up to $7,500 to an IRA, or $8,600 if you’re 50 or older, per IRS guidance.

But here’s what surprises people — rollovers and transfers don’t count against those limits. You can move any amount from an existing retirement account without it affecting your annual contribution cap.

Step 2: Initiate the Transfer or Rollover

This is where the method you choose matters most.

- For IRA-to-IRA transfers — Contact your new custodian and complete a transfer authorization form. They handle the rest directly with your current custodian. You don’t need to call anyone else.

- For 401(k) or employer plan rollovers — Contact your plan administrator and request a direct rollover to your new self-directed IRA custodian. The one detail that matters most? Make sure the check is payable to the custodian — not to you. That single step avoids the 20% withholding entirely.

Brighton’s team walks customers through the exact paperwork for their specific account type and custodian combination. No guesswork.

Step 3: Select and Purchase IRS-Approved Metals

Once the funds land in your self-directed IRA, you can work with your precious metals dealer to select your products.

Not every gold or silver product qualifies for IRA inclusion. The IRS requires minimum purity levels:

- Gold — 99.5% purity (0.995 fine)

- Silver — 99.9% purity (0.999 fine)

U.S.-minted products like the Gold American Eagle and Silver American Eagle are the most commonly held IRA-eligible coins.

After purchase, the metals ship directly to an IRS-approved depository — you don’t take personal possession while they’re inside the IRA.

Most customers complete the entire process — from opening the account to purchasing metals — in one to three weeks when using a direct transfer or direct rollover.

Wondering which metals are right for your situation? Brighton’s team can help you choose the best gold coins for new owners based on your goals.

Four Mistakes That Can Cost You When Moving Retirement Funds

Even with the best intentions, small missteps during a rollover or transfer can create real headaches.

Here are the ones we see most often — and how to avoid them.

Mistake 1: Requesting a Check When a Direct Transfer Would’ve Worked

This is the most common one.

Some people ask their current custodian for a distribution check — without realizing they could’ve had the funds sent directly to their new Gold IRA custodian.

The moment that money hits your personal account, you’ve started the 60-day clock. And you may have triggered tax withholding.

If you already have an IRA — even at a completely different institution — ask about a direct transfer first. Every time.

Mistake 2: Not Accounting for the 20% Withholding

If your 401(k) plan administrator sends you a check instead of sending it straight to your new custodian, they’re required to withhold 20% for federal taxes.

What does that actually mean?

On a $200,000 distribution, you’d only receive $160,000. To roll over the full amount and avoid taxes, you’d need to come up with $40,000 from your own pocket — then wait for a refund at tax time.

The simplest way to avoid this? Request a direct rollover where the check goes straight to your new custodian. No withholding. No scramble.

Mistake 3: Violating the One-Per-Year Rule

If you’ve done an indirect IRA-to-IRA rollover in the past 12 months and try another one, the second distribution becomes fully taxable.

There’s no waiver for this — Congress hasn’t extended relief for one-per-year violations.

Here’s the key distinction — direct transfers and direct rollovers from employer plans aren’t subject to this limit. Only indirect IRA-to-IRA rollovers count.

Mistake 4: Trying to Move Gold You Already Own Into an IRA

This one surprises a lot of people.

The IRS doesn’t allow you to transfer gold bars, coins, or rounds that you already own into an IRA. All precious metals inside an IRA must be purchased through the custodian and shipped directly to an approved depository.

Why? It comes down to purity verification and chain-of-custody documentation.

If you already hold physical gold outside of a retirement account, that’s perfectly fine. It simply exists as a separate position alongside your IRA holdings.

The Tax Picture: What Gets Reported and What Doesn’t

Understanding the tax side gives you clarity on why the method you choose matters — not just today, but at tax time.

Transfers: Nothing to Report

A direct trustee-to-trustee transfer between IRAs doesn’t generate a Form 1099-R.

You don’t report anything on your tax return. As far as the IRS is concerned, the funds simply moved from one custodian to another. No distribution happened.

It’s about as clean as it gets.

Direct Rollovers: Reported, But Not Taxed

When you do a direct rollover from an employer plan, the plan administrator issues a Form 1099-R showing the distribution.

But because the funds went straight to your new custodian, you report it on your return as a non-taxable rollover. Your new custodian issues a Form 5498 confirming receipt.

No taxes owed. No penalties. Just paperwork.

Indirect Rollovers: Reported — and Potentially Taxed

An indirect rollover generates a 1099-R. If you complete the rollover within 60 days, you report it as non-taxable.

But miss that deadline — even by one day — and the IRS treats the full amount as taxable income for that year.

For employer plans, the 20% mandatory withholding adds another layer on top of that.

| Transaction Type | Form 1099-R? | Taxable? | Form 5498? |

|---|---|---|---|

| Direct Transfer | No | No | No |

| Direct Rollover | Yes | No (if completed properly) | Yes |

| Indirect Rollover | Yes | No (if within 60 days) / Yes (if missed) | Yes (if completed) |

This is why working with an experienced precious metals dealer matters. Brighton coordinates directly with custodians and plan administrators to make sure everything’s handled correctly from the start — so you’re not sorting through reporting questions later.

How Brighton’s Concierge Service Simplifies the Process

Here’s what we hear most often from people considering a Gold IRA — it’s not the concept that feels complicated.

It’s the coordination.

Moving funds between institutions. Choosing the right custodian. Selecting IRA-eligible metals. Making sure every IRS rule is followed at every step.

That’s exactly what Brighton’s concierge service was built to handle.

What Brighton Handles for You

Brighton’s approach is built around support at every stage of ownership — not just the point of sale. Here’s what that looks like during the funding process:

- Custodian selection and account setup — Brighton works with established, IRS-approved custodians and helps customers open the right type of self-directed IRA for their situation. No confusion over which forms to file or which custodian fits best.

- Transfer and rollover coordination — The team handles communication between your current custodian or plan administrator and the receiving institution. You’re not chasing paperwork between offices.

- Product selection guidance — Once funds arrive, Brighton helps you evaluate IRS-approved products — whether that’s U.S.-minted coins, bars, or a combination that fits your goals. Every option is explained in plain terms.

- Ongoing support after purchase — Need to track the fair market value of your holdings? Want to add to your position? Have questions about what happens when it’s time to take distributions? Brighton’s team stays available long after the initial acquisition.

If you’re looking for clarity on gold IRA fee structures before making a decision, Brighton’s complimentary consultation is a good place to start.

Getting Started

The consultation is free, and there’s no obligation. Brighton’s team will walk you through your specific situation — whether you’re comparing methods, choosing a custodian, or just exploring whether a Gold IRA makes sense for your goals.

Most customers say the same thing afterward: “I wish I’d done this sooner.”

Special Situations: Roth Accounts, TSPs, and Inherited IRAs

Not every retirement account follows the same rules when it comes to moving into a Gold IRA.

Here are a few situations that come up regularly — and what you need to know about each.

Roth IRA to Roth Gold IRA

You can transfer funds from an existing Roth IRA to a self-directed Roth IRA that holds physical metals.

Same transfer rules apply — no taxes, no limits, no deadlines.

The one thing to confirm? Make sure your new custodian supports both Roth accounts and precious metals. Not all of them do.

Thrift Savings Plan (TSP)

Active-duty military and federal employees can roll over TSP funds into a Gold IRA — but only after separation from service (or, in some cases, after reaching age 59½ while still employed).

The good news? The TSP processes direct rollovers to IRAs. So the funds can go straight to your Gold IRA custodian — no withholding, no middleman.

Inherited IRAs

Inherited IRAs have their own set of distribution rules — and the SECURE Act changed them significantly.

You can transfer an inherited IRA to a new custodian that holds metals. But you can’t roll inherited funds into your own personal IRA unless you’re the surviving spouse.

The Required Minimum Distribution (RMD) rules depend on your relationship to the original owner and when they passed. If you’ve inherited a retirement account and want to explore your options, consult your CPA or tax professional for guidance specific to your situation.

SEP and SIMPLE IRAs

Both SEP and SIMPLE IRA funds can be transferred to a self-directed Gold IRA.

One important detail for SIMPLE IRAs — there’s a two-year waiting period from your first contribution before you can move funds to a non-SIMPLE IRA without penalty.

Once that window passes, the same transfer rules apply.

If you’re weighing whether a Gold IRA fits into your broader retirement picture, Brighton’s guide on evaluating gold IRA advantages and disadvantages walks through the practical considerations.

What Happens After the Funds Arrive

Once your transfer or rollover is complete and the funds have settled, the next step is selecting and purchasing your metals.

Most customers find this is the easiest part of the entire process.

Metal Selection

Brighton’s team walks you through available products, current pricing, and how each option fits within IRA rules.

Most customers make their selections within a few business days of the funds arriving.

Common IRA-eligible products include:

- Gold American Eagles — The most widely recognized U.S.-minted gold coin. Produced by the U.S. Mint since 1986 — trusted, liquid, and easy to value.

- Gold American Buffalos — 24-karat (.9999 fine) gold coins that meet the highest purity standard for IRA inclusion.

- Silver American Eagles — The most popular silver coin in the world, with .999 fine purity and strong recognition.

- IRA-eligible bars — Gold and silver bars from approved refiners (NYMEX/COMEX-approved or nationally recognized) that meet minimum fineness requirements.

After purchase, the metals ship directly from the dealer to the IRS-approved depository associated with your custodian. You’ll receive confirmation of delivery and can track your holdings through the custodian’s portal.

Storage Options

IRA-held metals must be stored in an IRS-approved depository. You can’t keep them at home or in a personal safe while they’re inside the IRA.

Most custodians offer two options:

- Segregated storage — Your metals are stored separately from other customers’ holdings — individually identified and inventoried. Many owners prefer this for the added peace of mind and control.

- Non-segregated (commingled) storage — Your metals are stored alongside other customers’ identical products. You’re entitled to the same type and quantity — just not necessarily the same specific coins or bars.

Brighton can help you understand the differences and explore distribution options for when the time comes to take possession.

Frequently Asked Questions

What is the difference between a direct and indirect gold IRA rollover?

A direct rollover moves funds straight from your employer plan to your Gold IRA custodian. You never touch the money. No taxes withheld. No 60-day deadline to worry about.

An indirect rollover sends the funds to you first. If it comes from an employer plan, your plan administrator must withhold 20% for federal taxes. You then have 60 days to deposit the full original amount — including the withheld portion, from your own pocket — into your new Gold IRA.

Which path gives you more control? In almost every case, it’s the direct rollover.

Can I do a gold IRA transfer from a Roth 401(k) in 2026?

Yes — but Roth 401(k) funds can only roll into a Roth IRA, not a Traditional IRA.

If your self-directed IRA custodian offers Roth accounts and permits precious metals, you can do a direct rollover from a Roth 401(k) into a Roth Gold IRA. Because those contributions were already taxed, the direct rollover is tax-free.

Consult your CPA or tax professional to confirm your eligibility.

Does the IRS 60-day rule apply to a direct gold IRA transfer?

No. The 60-day rule only applies to indirect rollovers — situations where you personally receive the funds before redepositing them.

A direct trustee-to-trustee transfer has no deadline because the money moves between custodians without ever passing through your hands.

That’s one of the main reasons experienced precious metals dealers recommend transfers over indirect rollovers.

How many times a year can I transfer funds between Gold IRAs?

There’s no limit on direct trustee-to-trustee transfers per year. The IRS one-per-12-month rule only applies to indirect (60-day) IRA-to-IRA rollovers.

You could transfer IRA funds between custodians multiple times in the same month — as long as each transfer is handled directly between institutions.

What happens if I miss the 60-day rollover deadline for physical gold?

The IRS treats the distribution as taxable income. If you’re under 59½, you may also owe a 10% early withdrawal penalty on top of that.

There are hardship waivers available under Revenue Procedure 2020-46 for qualifying circumstances — hospitalization, natural disasters, or errors by a financial institution.

But these aren’t automatic. The safest approach? Avoid the 60-day rule entirely by requesting a direct rollover or transfer.

Are there fees for rolling over a 401(k) to a Gold IRA?

The rollover itself typically doesn’t carry a fee from the IRS. But there may be fees from your existing plan administrator — like a distribution or processing charge — and from your new Gold IRA custodian for account setup, annual maintenance, and storage.

Brighton offers a No Fee Precious Metals IRA on qualified purchases, which covers custodial fees for the lifetime of the account.

It’s always worth asking about the full fee schedule before initiating any move.

Can I transfer gold bars I already own into a new Gold IRA?

No. The IRS doesn’t allow you to move personally held precious metals into an IRA.

All metals inside a Gold IRA must be purchased through the custodian and delivered directly to an IRS-approved depository. This ensures every item meets IRS purity requirements and chain-of-custody standards.

If you already own physical gold or silver, those holdings can exist outside your IRA as a separate cash-purchase position. Brighton supports both IRA and direct-delivery purchases.

The Takeaway: Making the Right Decision for Your Situation

The difference between a Gold IRA rollover and a transfer comes down to three things — where the money starts, how it moves, and what the IRS requires along the way.

For most people, a direct transfer (IRA to IRA) or a direct rollover (employer plan to IRA) is the simplest, safest, and fastest way to move retirement funds into physical precious metals.

An indirect rollover has its place — but the withholding, the 60-day deadline, and the once-per-year limit make it the least forgiving option.

You don’t have to figure this out alone. And you don’t have to rush.

The right move is the one you understand completely before you make it.

If you’re looking at establishing a precious metals IRA for the first time, start with the basics and build from there.

Ready to Take the Next Step?

If you’re thinking “this all makes sense, but I don’t have time to figure it out on my own,” you’re not alone. Most customers we work with felt the same way before they realized how straightforward the process can be with the right guidance.

That’s why we offer a complimentary consultation to walk you through your options — including our No Fee Precious Metals IRA, which covers custodial fees for the lifetime of the account on qualified purchases.

We’ll show you exactly:

- How the No Fee IRA works and whether you qualify

- The difference between U.S.-minted coins and foreign alternatives

- What to expect from the purchasing and delivery process

- How to roll over or transfer existing retirement funds

- What ongoing support looks like after your purchase

Learn About the No Fee IRA — no obligation, just actionable insights you can use whether you work with us or not.

Your retirement savings took decades to build. The way you move them should reflect that same level of care.