Can I Store My Gold IRA at Home? (IRS Rules & Risks)

No — you cannot legally store your Gold IRA metals at home.

The IRS requires all IRA-held precious metals to be in the physical possession of a qualified trustee or custodian. That’s not a gray area or an open question — it’s written directly into federal law. Taking personal possession of your IRA gold — whether in a home safe, a personal bank safe deposit box, or through a structure marketed as a “Checkbook IRA” or “Home Storage IRA” — is treated by the IRS as a taxable distribution. The full fair market value of your IRA becomes ordinary income in the year possession transfers. For those under 59½, a 10% early withdrawal penalty stacks on top.

The 2021 McNulty v. Commissioner ruling by the U.S. Tax Court removed whatever ambiguity some dealers had been using to sell this idea. The court rejected the argument that an IRA LLC structure allowed the taxpayer to hold her IRA gold personally without triggering a distribution. Personal possession — in any form — violates the custodial requirement. The taxpayer’s result: a six-figure tax bill.

Here’s what’s worth understanding before going any further: the marketing for “Home Storage IRAs” sounds like a control story. More access. More independence. Less middleman. For customers who value self-reliance and are skeptical of institutions, that pitch lands. But the appeal of the pitch has no effect on what the IRS will do when it reviews your account.

This article covers what federal law actually requires, why the Checkbook IRA structure fails under IRS scrutiny, how IRS-approved depositories protect your tax-deferred status, and what your options look like if you want genuine access to physical metals — legally. If you have a specific tax situation, your CPA or tax professional is the right person to consult. What follows is education — not legal or tax advice.

Where the “Home Storage” Idea Comes From

The “Home Storage IRA” didn’t come from nowhere. It came from dealers who built a pitch around something customers already want — direct control over what they own.

The pitch works because the instinct behind it is legitimate. The problem is that the structure being sold to satisfy that instinct isn’t legal — and the people most harmed by it aren’t the dealers promoting it.

Here’s where to look, and why it matters before you make any decisions.

The Checkbook IRA Marketing Playbook

The structure goes like this.

A promoter encourages you to form a Limited Liability Company (LLC) owned by your IRA. The IRA custodian transfers your account funds into that LLC. You — as the LLC’s manager — purchase physical gold and store it personally, often at home or in a private safe deposit box.

The theory: the LLC owns the gold, not you. You’re just the manager. So personal possession doesn’t count as a distribution.

IRC Section 408(m)(3) says otherwise — directly. The statute requires IRA precious metals to be held in the “physical possession of a trustee.” A trustee is a bank, a federally-insured credit union, or another entity the IRS has approved to administer IRAs. A customer-owned LLC isn’t on that list. The individual still controls the gold. That’s the exact problem the LLC structure was supposed to eliminate — and it doesn’t.

There’s a broader point worth making: the Checkbook IRA structure isn’t categorically illegal. It has legitimate applications in some self-directed IRA contexts. But using it to achieve home storage of precious metals is specifically where it becomes non-compliant. Most promoters don’t draw that line for you. That’s why identifying safe gold IRA practices matters before anything is signed.

What to watch for in a Checkbook IRA pitch:

- “You maintain full control” (the problem, not the benefit) — “Full control” over IRA assets is how the IRS defines constructive receipt. This phrase is doing exactly what it sounds like — and not in your favor.

- “The LLC owns it, not you” (rejected by the courts) — The McNulty ruling addressed this framing directly. Nominal LLC ownership didn’t protect the taxpayer from a full taxable distribution. The court looked at who actually controlled the gold.

- “This is a common strategy” (frequency isn’t compliance) — Popularity doesn’t create a legal defense. The IRS enforces the statute regardless of how widely a non-compliant structure is marketed.

- “Skip the depository fees” (a false economy) — Any savings from bypassing an approved depository disappear the moment the IRS treats your account as a distribution. The real cost isn’t the depository fee.

Why “Control” Is the Selling Point — and the Problem

It’s worth being honest about why this pitch resonates.

Customers who’ve spent decades building what they have don’t love the idea of handing their physical gold to a third party. What if the depository has a problem? What if access gets complicated? What if the institution itself becomes part of the instability they’re trying to get outside of?

Those aren’t irrational questions. They’re the right questions to ask about the institutions you work with.

The mistake is treating home storage as the answer to them.

Home storage doesn’t resolve institutional risk — it creates a more immediate, more certain problem in front of the hypothetical one. The IRS doesn’t wait for a financial crisis to enforce the custodial requirement. A single audit that finds non-compliant storage triggers a distribution of your entire account value before any crisis ever materializes.

For customers focused on understanding gold IRA rules, here’s the core truth: the tax benefit and the custodial requirement are part of the same structure. You can’t keep one and discard the other. They come together — or not at all.

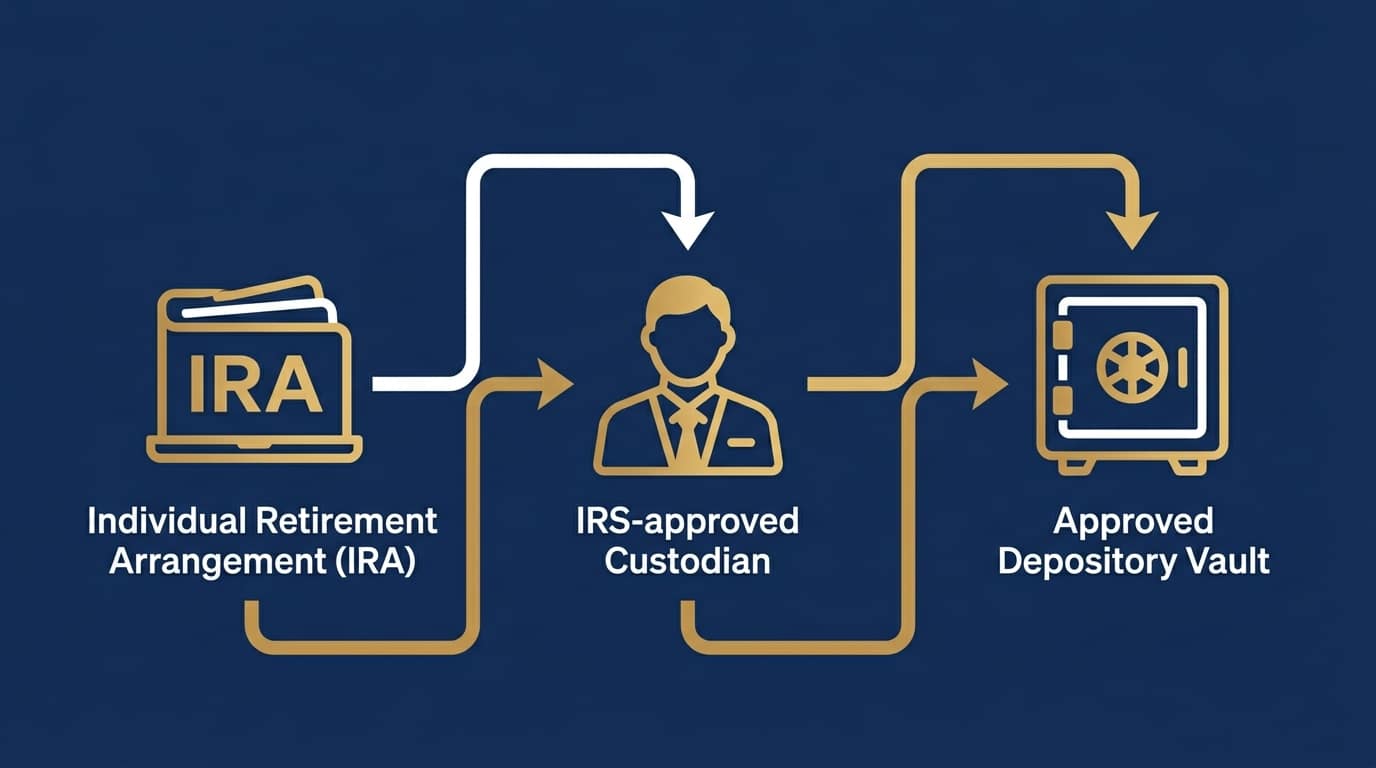

What Federal Law Actually Requires

The rules governing Gold IRA storage aren’t complicated. Two conditions. One covers the metals themselves. The other covers where they have to be.

Home storage fails the second condition. Completely. Here’s what the law actually says — and what it means in practice.

IRC Section 408(m)(3) — The Exact Legal Standard

IRC Section 408(m)(3) is the federal statute that governs precious metals held in IRAs. Two conditions for tax-deferred status:

- Fineness requirements (what metals qualify) — Gold must meet a minimum purity of .995 fine for most coins and bars. There’s a statutory exception for certain U.S.-minted coins — including the Gold American Eagle — which carries a .9167 fine purity but is explicitly approved by law.

- Trustee physical possession (where the metals must be) — The metals must be in the “physical possession of a trustee.” This is the condition home storage violates, regardless of any LLC structure or ownership arrangement placed around it.

What qualifies as a trustee? IRS Publication 590-A defines it: a bank, an insured credit union, or another entity that’s demonstrated to the IRS’s satisfaction that it can properly administer an IRA. A customer-controlled LLC doesn’t qualify — regardless of how it’s titled.

The rule holds regardless of how ownership appears on paper. Metals at your home, in your personal safe deposit box, or in any facility where you have unilateral access all fail the trustee possession test.

What McNulty v. Commissioner Settled

The McNulty v. Commissioner case is the one dealers who promote home storage tend not to mention by name.

Here’s what happened. The taxpayer held gold coins in her home safe through an LLC owned by her self-directed IRA. Her argument: the LLC — not her personally — was the legal owner. The U.S. Tax Court, in its November 2021 ruling, rejected this completely.

The court found that the taxpayer, as LLC manager, had unrestricted personal access to the coins. That level of access is “unfettered control.” Unfettered control constitutes constructive possession. And constructive possession is treated identically to physical possession under IRS rules.

The outcome: the full value of her IRA was treated as a taxable distribution in the year she stored the coins at home. Combined with the resulting tax liability, the financial damage ran into six figures. The LLC provided no protection — because the court was looking at actual control, not the name on the title.

What the ruling confirmed:

- The LLC structure does not change who has functional control over IRA assets.

- “Constructive possession” — the ability to access assets without independent institutional authorization — is enough to trigger a distribution.

- The IRS was enforcing the plain meaning of the statute. Not a technicality. Not an obscure interpretation.

| Distribution Scenario | Tax Treatment | Early Withdrawal Penalty (Under 59½) |

|---|---|---|

| Home storage discovered during IRS audit | Full IRA fair market value treated as taxable distribution in the year possession was established | +10% of full account value |

| Checkbook IRA / LLC home storage, any age | Full IRA fair market value treated as distribution in year metals were taken possession of | +10% if under 59½ |

| Voluntary correction (prior to audit) | CPA-advised resolution — potentially reduced exposure | Varies — professional guidance required |

| Compliant depository storage | No current tax event — IRA status preserved | Not applicable |

If you’re currently in a home storage arrangement and haven’t filed amended returns — don’t wait. A conversation with a CPA who specializes in self-directed IRAs is the right first move. Not watching to see if an audit arrives.

Constructive Receipt — Even a Key Can Trigger a Distribution

Here’s the part of the law that catches most people off guard.

Constructive receipt doesn’t require you to physically hold the gold. It means you have the ability to access and control it at will — with nothing independent stopping you.

Under IRS interpretation, even holding a key to a safe or having solo access to a facility where your IRA metals are stored can establish constructive receipt. If there’s no independent institutional control between you and the metals, you effectively possess them — regardless of how the ownership documents read.

This is why the structural design of an approved depository is as important as its physical security. IRS-approved depositories operate under dual-control access protocols. No individual — including the account owner — can access the metals without independent custodian authorization. That independent layer is what separates compliant storage from constructive possession.

The question worth asking about any proposed storage arrangement: “What stops me from walking in and taking the gold right now?” If the answer is only a lock you control — that’s not enough. For a full breakdown of how compliant depositories are structured, understanding gold IRA storage rules covers the access control and authorization requirements in detail.

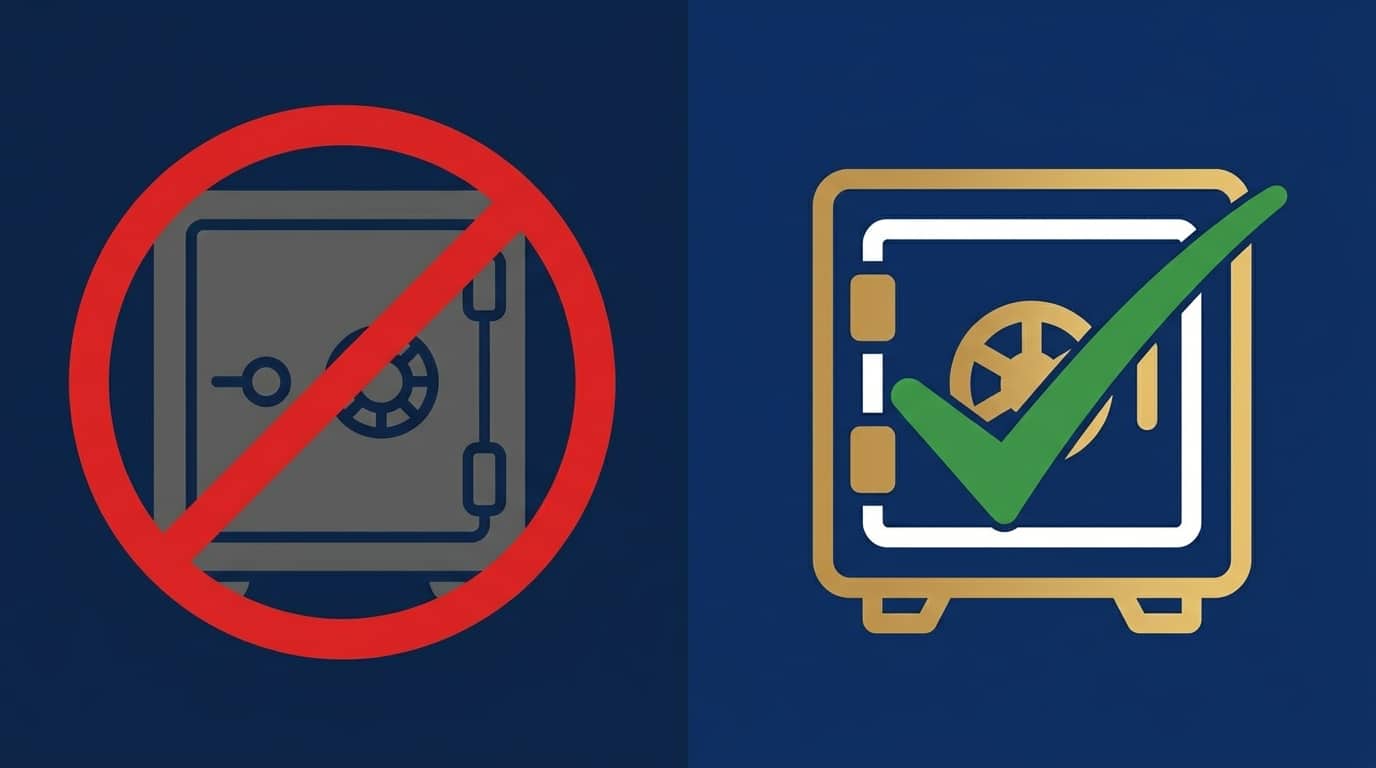

Home Storage vs. IRS-Approved Depository — Side by Side

A lot of content frames this as “control vs. compliance” — as though the two options trade off something real.

They don’t. One path keeps your IRA intact. The other ends it. Here’s how they actually compare.

| Factor | Home Storage (Prohibited) | IRS-Approved Depository (Compliant) |

|---|---|---|

| IRS Standing | Immediate taxable distribution | Tax-deferred status preserved |

| Legal Basis | Violates IRC Section 408(m)(3) | Compliant with IRC Section 408(m)(3) |

| Tax Consequence | Full account value treated as taxable distribution | No current tax event |

| Early Withdrawal Penalty | 10% if under age 59½ | Not applicable |

| Physical Security | Home safe or personal facility | Class 3 vault with institutional-grade infrastructure |

| Insurance Coverage | Homeowner’s policy (typically inadequate for metals) | Institutional coverage — often $1B+ aggregate |

| Access Control | Unilateral — creates constructive receipt | Dual-control — custodian authorization required |

| Audit Risk | High — IRS enforcement is active in this area | Low — full documentation and receipt trail maintained |

The comparison that actually matters isn’t “home storage vs. depository.” It’s “taxable distribution vs. continued IRA.”

What Compliant Storage Actually Provides

Facilities like Delaware Depository and Brinks Global Services — two of the most widely used IRS-approved depositories in the precious metals IRA industry — operate at a level no home setup can match.

Class 3 vault construction. Around-the-clock monitoring. Multi-layer access controls. Institutional insurance coverage on the full value of stored metals. These aren’t premium features — they’re baseline operating standards for qualifying facilities.

But the physical security isn’t the main reason to use an approved depository. The main reason is that it’s the only structure that lets you hold IRA metals without triggering a distribution.

That said, the security is meaningful on its own terms. A home safe offers a fire rating, a lock, and whatever your homeowner’s policy will cover — which typically has hard limits on precious metals and requires a specific rider for even partial coverage. An approved depository is a different category of protection entirely — not a better version of the same thing.

For customers who have real concerns about institutional risk — depositories failing, access complications — here’s what to evaluate rather than defaulting to home storage:

- Financial backing and certification — Is the depository fully capitalized? COMEX or LBMA certification is a meaningful indicator of operational standards.

- Audit frequency and transparency — Are independent audits conducted? Are the results available to account owners?

- Segregated vs. commingled storage — Segregated storage keeps your specific metals separately identified. Commingled pools them with other holdings. Both are compliant; the distinction matters to some owners.

- Insurance coverage specifics — What’s covered, to what limit, and under what circumstances? Don’t assume — ask.

For everything on selecting the right depository, that guide covers the full evaluation criteria. Precious metals may appreciate, depreciate, or remain unchanged. What doesn’t change: how you store them within an IRA determines whether the IRA continues to exist.

How the IRS Verifies Storage

The IRS doesn’t operate on the honor system here. There’s a documented verification trail for IRA precious metals:

- Custodian recordkeeping — Your IRA custodian maintains records of which metals are held, where, and in whose name. Those records are subject to IRS review.

- Depository receipts — Approved depositories issue formal receipts confirming possession. These receipts are part of the custodial documentation trail.

- Form 5498 filing — Custodians report the fair market value of your IRA assets — including physical metals — annually on Form 5498. Discrepancies between reported values and actual holdings raise audit flags.

- Physical vault confirmation — In an audit, the IRS can and does request verification that metals are physically present at the depository location reported.

A home safe produces none of this. It creates exactly the kind of evidentiary gap an audit is designed to surface.

Who This Article Isn’t For

One thing worth saying directly — because this topic sometimes draws readers who aren’t actually interested in long-term IRA ownership.

If your interest in home storage is about keeping metals accessible for a quick sale when prices move — if the goal is trading positions, not long-term ownership — this article, and Brighton Gold, aren’t the right fit.

We don’t forecast prices. We don’t time the market. We don’t offer trading recommendations.

Brighton Gold works with customers who want to hold something real for the long term. People who value physical ownership, clarity, and control over their financial picture — not the ability to liquidate on a 48-hour window.

If active trading is the goal, an IRA structure isn’t what you’re looking for in the first place. The custodial and distribution rules that govern IRAs exist for long-term retirement accumulation — they’re not built for frequent transactions. Comparing a Gold IRA to direct physical ownership covers that distinction in full — including when direct ownership outside an IRA structure actually makes more sense for certain owners.

If long-term ownership inside a tax-deferred account is the goal, the custodial requirement isn’t an obstacle. It’s the mechanism that makes the tax benefit possible. That distinction is what separates customers who get lasting value from a Gold IRA from those who don’t.

The Questions Owners Ask Most

A few questions come up reliably once customers understand the storage rules. Here’s what the answers actually look like.

“What About a Safe Deposit Box at My Bank?”

A personal safe deposit box at your bank isn’t an IRS-approved storage solution for IRA metals — with one specific exception.

If the bank itself is the IRA custodian and holds the box under its institutional control, the arrangement can work. But the key distinction is who controls access. A safe deposit box rented in your personal name — at any bank, even one where you’ve had accounts for decades — gives you the key. You walk in, open the box, and access the contents without anyone else’s authorization. That’s constructive receipt. Same legal problem as a home safe.

Most banks don’t offer custodial precious metals storage for self-directed IRAs. An IRS-approved precious metals depository is the practical, standard-compliant solution for the overwhelming majority of Gold IRA owners.

| Storage Structure | Access Control | IRS Compliance Status |

|---|---|---|

| Home safe | Account owner — unilateral | Prohibited — taxable distribution |

| Personal safe deposit box | Account owner holds key | Prohibited — constructive receipt |

| Safe deposit box held by custodian-bank (bank as trustee) | Custodian institution — controlled | Potentially compliant — custodian must control access |

| IRS-approved precious metals depository | Dual control — custodian + depository | Compliant — meets IRC 408(m)(3) standard |

“Why Do Some Dealers Still Advertise Home Storage?”

This is the right question to ask — and asking it is the right instinct.

Two reasons explain why some dealers still run this pitch.

First, it converts. Customers who value self-reliance respond to “keep your gold close” messaging. Some dealers prioritize the conversion over the customer’s long-term compliance picture.

Second — and this is the part that matters — the consequences of home storage fall on the customer, not the dealer. The dealer collects the commission. The customer is the one who gets audited.

We believe customers deserve to know that dynamic before anything is signed. No marketing claim — however confident — changes what IRC Section 408(m)(3) says. A dealer promising full IRA tax benefits alongside home storage is making a promise the IRS won’t honor.

For the warning signs that separate compliant guidance from commission-first promotion, the guide on identifying gold IRA red flags covers what to look for before any agreement is signed.

“Can I Take Physical Possession When I Retire?”

Yes — and this is the answer to the control question that home storage is trying to solve illegally.

Once you reach age 59½, you can request an In-Kind Distribution — a direct physical transfer of your IRA metals from the depository to you. At that point, the metals leave the IRA structure. They’re yours. No custodian. No storage requirements. No IRS restrictions on how or where you keep them.

The distribution is a taxable event — the fair market value of the metals at the time of transfer carries a tax liability. But once that obligation is satisfied, ownership is complete and unconditional.

This is also the legitimate path for customers who worry about institutional access in a future crisis. You don’t have to compromise your IRA’s tax-deferred status during the accumulation years to end up with direct physical possession in retirement. You accumulate with the tax structure intact — and take possession on your timeline, legally, when it makes sense for you.

The mechanics, timing, and planning considerations for executing a precious metals IRA distribution are covered in that guide in full — including how to sequence distributions to manage the resulting tax liability across multiple years.

What a Compliant Transition Looks Like

If you’re currently storing IRA metals at home — or if you’ve been operating under a Checkbook IRA structure for precious metals storage — here’s what moving toward compliance typically involves:

- Step 1: Get a qualified tax professional involved immediately (this is the non-negotiable first move) — Whether a taxable distribution has already been triggered is a legal and tax determination that requires professional assessment. The sooner a CPA who specializes in self-directed IRAs is in the conversation, the more options typically remain open. Don’t attempt to correct this without professional guidance.

- Step 2: Establish a compliant self-directed IRA custodial account (the structural foundation) — A qualified self-directed IRA custodian sets up the right account structure and can connect you with IRS-approved depositories. The custodian handles the paperwork. You choose the depository.

- Step 3: Transfer the metals under proper custodial supervision (not a self-move) — The transfer needs formal documentation. Metals must move from your possession to the custodian’s with the transfer properly recorded. Your CPA and custodian manage the mechanics. Your job is to initiate the process.

Proactive correction consistently produces better outcomes than waiting for an audit. The IRS enforcement record in this area is active. A self-initiated correction typically results in significantly fewer consequences than one discovered during a formal review.

For the full picture on what a compliant Gold IRA costs to maintain — custodian fees, depository fees, and what to watch for in fee structures — understanding gold IRA fee structures covers what to expect and where to ask hard questions.

Frequently Asked Questions

Is a “Checkbook IRA” a legal way to store gold at home?

No. The U.S. Tax Court addressed this directly in McNulty v. Commissioner (2021). A Checkbook IRA structure — where the account owner manages an LLC that holds the metals personally — does not satisfy the custodial requirement under IRC Section 408(m)(3). The court found that unrestricted personal access through LLC management constitutes constructive receipt, and the taxpayer’s full IRA value was treated as a taxable distribution. The LLC wrapper provided zero protection under enforcement.

What is the penalty for storing Gold IRA metals at home?

The IRS treats non-compliant personal possession as a taxable distribution in the year it occurs. The full fair market value of your IRA is treated as a taxable distribution for that tax year — subject to your standard tax rate. For account owners under age 59½, a 10% early withdrawal penalty also applies to the full distribution amount. For a six-figure IRA, the combined federal and state tax liability can eliminate a significant portion of the account’s accumulated value in a single year.

Can I store my IRA gold in a bank safe deposit box?

Only if the bank functions as your IRA custodian and holds the safe deposit box under its institutional control — not in your personal name. A box you rent personally, with a key in your possession, creates constructive receipt — the same legal problem as home storage. Most banks don’t offer custodial precious metals storage for self-directed IRAs. If you’re uncertain about a specific arrangement, that question belongs to your CPA before any action is taken.

Why do some gold companies still advertise home storage IRAs?

Because the marketing converts — and the legal consequences fall on the customer, not the dealer. Some companies promote Home Storage or Checkbook IRA structures knowing that the IRS will treat personal possession as a distribution. The dealer earns the commission either way. Understanding that dynamic before signing anything is important. For a clear picture of what compliant guidance actually looks like — and how to distinguish it from commission-first marketing — what are the IRS-approved gold requirements covers the compliance side in detail.

How do IRS-approved depositories protect my metals?

Approved depositories operate with institutional-grade physical security — Class 3 vault construction, 24/7 monitoring, and insurance designed specifically for high-value precious metals. More important for IRA compliance is the dual-control access structure: no individual — including the account owner — can access stored metals without independent custodian authorization. That structure is what satisfies the trustee possession requirement under federal law. Regular independent audits and formal depository receipts also create the documentation trail that supports your IRA’s ongoing tax-deferred status.

Can I take physical possession of my gold when I retire?

Yes — through an In-Kind Distribution. Once you reach age 59½, you can request that your Gold IRA metals be physically transferred to you directly from the depository. The distribution is a taxable event — the fair market value of the metals at the time of transfer carries a tax liability — but once that’s satisfied, the metals are your outright personal property. No ongoing custodial or storage requirements apply. For the full process, timing, and planning options, that guide covers the mechanics in full.

How does Brighton Gold approach the storage question?

Brighton Gold’s team walks customers through every step of the Gold IRA process — including custodian selection and depository options — as part of the complimentary consultation. We work with IRS-approved custodians and connect customers with compliant storage facilities. We don’t provide tax or legal advice — that’s your CPA’s role. What we handle is making the process clear so you can move forward with confidence rather than uncertainty. The Brighton Gold learning center has additional guides on IRA mechanics, approved metals, and physical delivery options.

The Bottom Line on Home Storage

The Home Storage IRA isn’t a bold move. It’s a tax trap that keeps getting repackaged with professional-sounding language.

The law is settled. The case law is settled. The IRS enforcement record is settled. Personal possession of IRA-held precious metals — regardless of how the ownership is structured on paper — triggers a taxable distribution. That outcome isn’t hypothetical. It doesn’t depend on an audit. It occurs in the year possession is established.

What customers who value self-reliance are actually after is something real they own outright — physical metals outside the paper financial system, held in their name, accessible to them and their family. That’s a legitimate goal. It’s achievable. But within a tax-deferred IRA, the path runs through a compliant custodian and an approved depository — not around them.

The In-Kind Distribution at retirement is the moment when IRA metals become fully, legally, personally yours — no institutional requirements attached. That’s not a workaround. That’s how the structure is designed to work. Accumulate with tax deferral intact. Take physical possession on your terms, on your timeline, when it makes sense.

A compliant depository isn’t giving up control. It’s the mechanism that makes the tax benefit possible — so that when you do take possession, it’s a deliberate decision, not a forced one.

If you’ve spent time researching Gold IRA storage and you’re still not sure which information to trust — that’s a reasonable place to be.

Brighton Gold’s complimentary consultation walks through your specific situation: what you currently have, what you’re trying to protect, and whether a Precious Metals IRA with compliant storage makes sense for where you are. No pressure. No pitch. Just a clear conversation — including how the No Fee IRA works and whether you qualify.

The window to get clarity is open now — not because of urgency, but because the longer a non-compliant structure sits unaddressed, the fewer options remain when it’s reviewed.