How Do I Calculate the Premium on Physical Gold Purchases?

The premium on physical gold is the cost charged above the current spot price. It’s the transparent cost of turning raw gold into something you can hold, store, and pass down — a tangible product with actual weight, provenance, and legal tender status.

The formula is straightforward: Total Price = (Spot Price per Ounce × Weight in Ounces) + Premium. The spot price is determined by the most active front-month futures contract on commodity exchanges like COMEX. The premium covers minting, fabrication, assaying, certification, distribution, shipping logistics, secure storage, insurance, and dealer operating costs.

Here’s what that means.

A one-ounce American Gold Eagle coin contains exactly one troy ounce of gold. It’s a 22-karat alloy — 91.67% gold, 3% silver, 5.33% copper — so the gross weight is 1.0909 troy ounces. That extra weight adds durability. The minting process adds security features, U.S. government backing, and liquidity in resale markets. All of that shows up in the premium.

Market conditions affect premiums. During peak stress in 2020, premiums on popular gold coins rose from a typical 5% to over 10-12%. High demand or supply chain disruptions push premiums higher. Larger gold bars carry lower per-ounce premiums than smaller coins — a 1-kilogram bar has lower fabrication costs per ounce than detailed coin designs.

Calculating the premium isn’t about outsmarting the dealer.

It’s about partnering with someone who explains it clearly upfront — what you’re paying for, why it costs what it does, and how the product you’re acquiring fits the role you need it to play. The clarity you need exists upfront — or it doesn’t exist at all.

- What the Premium Actually Represents

- The Formula Every Gold Buyer Should Know

- What Drives the Premium You Pay

- Why the Same Ounce of Gold Can Have Different Premiums

- How to Calculate the Premium on a Real Purchase

- Frequently Asked Questions

- What is a typical premium for a one-ounce American Gold Eagle coin?

- Why is the premium on a gold coin different from a gold bar of the same weight?

- Do I get the premium back when I sell my physical gold?

- How does dealer inventory affect the premium on gold products?

- Are gold premiums negotiable?

- Besides the premium, what other costs are involved in buying physical gold?

- Where This Leaves You

What the Premium Actually Represents

Before you can calculate anything, you need to know what you’re calculating — and most of the industry would rather keep that definition fuzzy.

The premium isn’t a fee tacked on because a dealer felt like it. It’s the measurable cost of turning a line item on a futures exchange into a physical asset you can hold. Manufacturing. Distribution. Business operations that keep the lights on. That distinction matters more than most articles admit.

When you buy a Gold American Eagle, you’re not buying paper gold or a share in a fund. You’re buying a coin that was minted by the U.S. Mint, assayed to verify its gold content, packaged, insured, shipped, and delivered to your door or a depository in your name. Every step in that chain costs money. The premium is how those costs get paid — and how the dealer stays in business to support you after the sale.

What the Spot Price Is (and Isn’t)

The spot price is the market price for immediate delivery of gold. It’s what gold trades for — right now — on commodity exchanges like COMEX, based on continuous electronic trading. That’s what you’ll see quoted on the current spot price of gold and every other live ticker.

Here’s what it isn’t: the price you’ll pay for a physical coin or bar. The spot price reflects futures contracts — agreements to buy or sell gold at a future date — not the cost of acquiring minted, certified, and deliverable metal today. The spot price is the floor. The premium is the difference between that floor and the real world.

Where the Spot Price Comes From

The gold spot price is determined by the most active front-month futures contract on COMEX, where price discovery happens through how gold futures contracts are traded electronically around the clock. It’s a global benchmark — the same number a buyer in New York and a buyer in Singapore both reference.

That benchmark reflects supply, demand, macroeconomic conditions, currency fluctuations, and geopolitical risk. What it doesn’t reflect is minting, fabrication, logistics, or dealer operating costs. Those show up in the premium — and they’re different for every product.

| Component | What It Covers | Example |

|---|---|---|

| Minting & Fabrication | Converting raw gold into a finished coin or bar with specific weight, purity, and design standards | A Gold American Eagle’s intricate design, security features, and alloy composition add production steps a simple cast bar doesn’t require |

| Assaying & Certification | Third-party verification of gold content and purity — the guarantee that what you’re holding is what the label says it is | IRA-approved coins must meet strict fineness standards; that verification process is baked into the premium |

| Distribution & Shipping | Secure logistics from mint to dealer to customer — insurance, tamper-evident packaging, tracked delivery | A one-ounce coin shipped to your door carries different handling costs than institutional bulk orders delivered to vaults |

| Dealer Operating Costs | Rent, staff, compliance, customer support, inventory carrying costs, and post-purchase service | The dealer who walks you through rollover questions six months after your purchase isn’t doing that for free |

| Market Liquidity Premium | Recognition and ease of resale — widely recognized products command tighter spreads when you sell | A Gold American Eagle is more liquid than a foreign coin or a generic round because buyers trust the U.S. Mint backing |

The Formula Every Gold Buyer Should Know

Total Price = (Spot Price per Ounce × Weight in Ounces) + Premium. That’s it. No industry jargon required.

Here’s how it works in practice. The spot price for gold is $2,050 per ounce. You’re buying a one-ounce American Gold Eagle coin. The premium is $85. Your total cost is ($2,050 × 1) + $85 = $2,135.

That $85 premium covers everything between the futures contract and the physical coin in your hand — minting, certification, distribution, insurance, and the dealer’s operating margin.

The premium isn’t a mystery to solve or a fee to resent.

It’s the transparent cost of owning something real. When a dealer obscures that calculation or races you to the bottom on price, they’ve already told you what they think of the relationship. The clarity you need exists upfront — or it doesn’t exist at all.

Understanding the definition of a financial premium means recognizing it’s not a markup designed to confuse you. It’s the measurable cost of bringing a physical product to market.

The calculation itself is simple math. The decision about who you buy from is where the real work happens.

| Scenario | Spot Price | Total Price | Premium (Dollars) | Premium (%) |

|---|---|---|---|---|

| 1 oz Gold Eagle (spot $2,050, premium $85) | $2,050 | $2,135 | $85 | 4.1% |

| 1 oz Gold Eagle (spot $2,200, premium $90) | $2,200 | $2,290 | $90 | 4.1% |

| 1 oz Gold Buffalo (spot $2,050, premium $95) | $2,050 | $2,145 | $95 | 4.6% |

| 10 oz Gold Bar (spot $2,050, premium $70/oz) | $2,050 | $20,700 | $700 | 3.4% |

| 1 oz Gold Eagle (market stress, spot $2,050, premium $200) | $2,050 | $2,250 | $200 | 9.8% |

What Drives the Premium You Pay

The premium isn’t arbitrary. It’s the sum of specific, identifiable costs that any transparent dealer can break down for you on the spot.

Most dealers bury these costs in jargon or use them as an excuse to pad margins.

Brighton Gold does the opposite. We explain what drives the premium, show how it breaks down, and let you decide if the value matches the cost. Here’s what you’re paying for.

Minting and Fabrication

Minting and fabrication cover the physical work of turning raw metal into a finished product. For a coin like the Gold American Eagle, that means striking a 22-karat alloy — 91.67% gold, 3% silver, 5.33% copper — into a coin with security features, detailed design, and U.S. government backing.

A one-ounce Gold Eagle weighs 1.0909 troy ounces because of that alloying process. The extra weight adds durability and longevity.

Assaying and certification verify the gold content and purity before the product reaches you. That verification is what makes a U.S.-minted coin immediately recognizable and liquid in resale markets.

You’re not just buying gold. You’re buying provenance.

How the U.S. Mint prices its products reflects production realities — raw material costs, operational overhead, and demand. The premium you pay includes what the dealer paid to acquire minted products from the source.

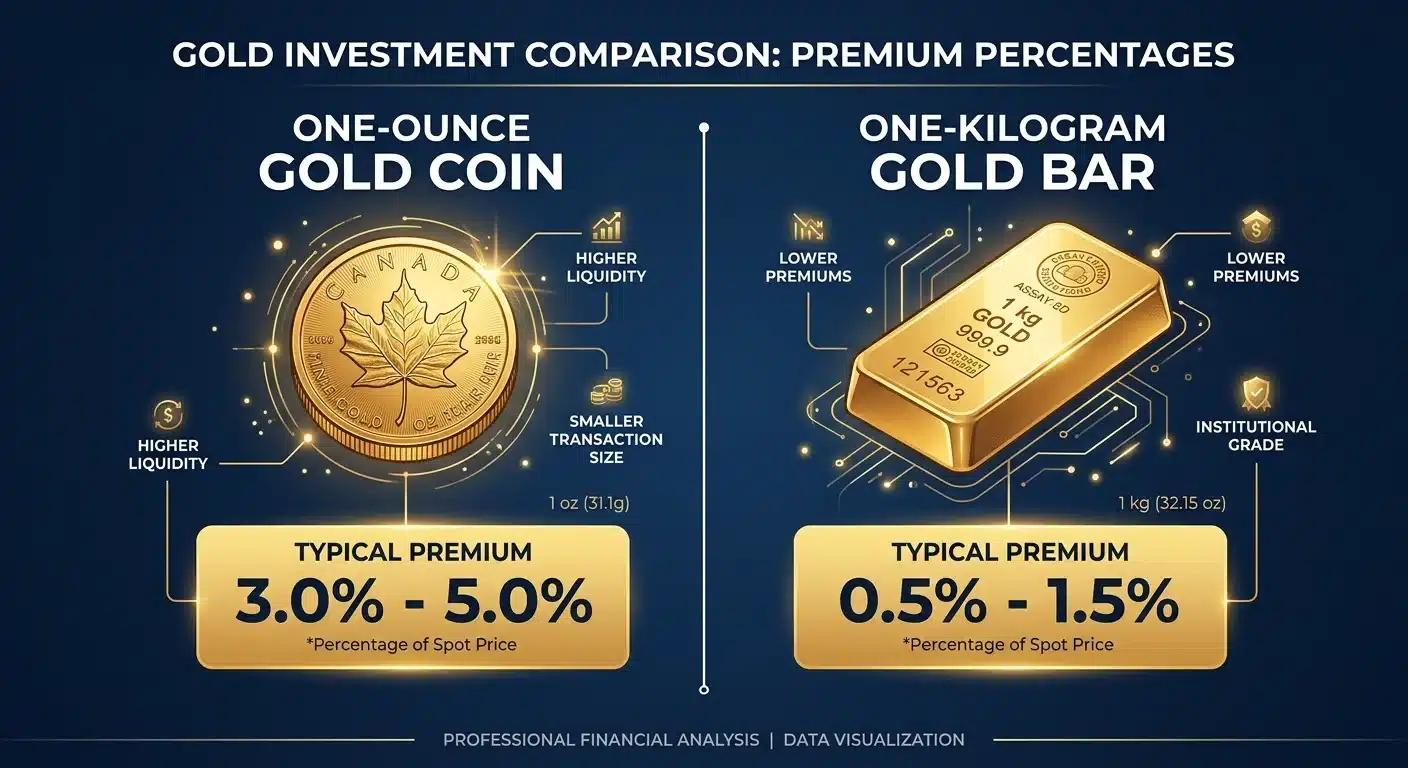

Smaller coins carry higher per-ounce premiums than larger bars because the design and strike process doesn’t scale with weight. A 1-ounce coin costs more to produce per ounce than a 10-ounce bar.

Distribution, Shipping, and Insurance

Distribution, shipping, and secure storage aren’t invisible costs. They’re measurable line items.

Physical gold doesn’t appear at your door. It’s packaged, insured, transported through secure channels, and — if you’re using a depository — vaulted under your name in a facility with insurance coverage that reflects the actual value of the holdings.

Insurance alone is a recurring cost for any dealer holding inventory. Supply chain disruptions, fuel costs, and carrier premiums all feed into the final premium you see.

During periods of high demand or stress — like 2020 — these costs spike, and premiums rise. That’s not price gouging. That’s the market passing real costs through to the transaction.

Dealer Margin and Operating Costs

Dealer operating costs include everything that keeps the business running — staff, compliance, customer support, systems, and the capital to maintain inventory.

A dealer who answers questions six months after your purchase isn’t doing that for free. That support is baked into the margin.

Here’s the question most articles skip: do you want the cheapest dealer, or the one who’ll still be around — and still care — when you need to sell?

The premium reflects more than the product. It reflects the relationship. Brighton Gold’s concierge model exists because customers who feel informed and supported make better decisions and stay. The margin isn’t there to squeeze one transaction. It’s there to fund the support that lasts the lifetime of your ownership.

| Cost Component | What It Includes | Impact on Premium |

|---|---|---|

| Minting & Fabrication | Striking, alloying, quality control, security features, design complexity | Higher for coins with intricate designs; lower for simple cast bars |

| Assaying & Certification | Purity testing, weight verification, chain-of-custody documentation | Built into government-minted products; minimal for private mint rounds |

| Distribution & Shipping | Secure transport, packaging, carrier insurance, fuel costs, logistics infrastructure | Rises during supply chain disruptions or periods of high demand |

| Secure Storage & Insurance | Vault fees, inventory insurance, depository agreements, security protocols | Ongoing cost for dealers holding inventory; passed through to customers |

| Dealer Operating Costs | Staff, compliance, customer support, systems, capital requirements, post-purchase service | Reflects the relationship model — transactional dealers minimize this; concierge models build it in |

Why the Same Ounce of Gold Can Have Different Premiums

Not all gold products are created equal — and the premium reflects that.

Two one-ounce gold products can have wildly different premiums — and both can be legitimate.

The difference isn’t one dealer overcharging and another playing fair. It’s the form of the product, the market conditions when you buy, and whether inventory is sitting on shelves or backordered.

Knowing what drives the difference is how you make a decision based on value, not just who quotes the lowest number today.

Product Form and Size

A one-ounce American Gold Eagle coin doesn’t cost the same as a one-ounce gold bar — even though they both contain the same amount of gold.

The coin carries a higher premium. The minting process is more demanding. The design detail is finer. The product carries U.S. government backing and instant liquidity. A simple cast bar doesn’t have those features — and it doesn’t cost as much to produce.

Larger bars carry lower per-ounce premiums than smaller coins. A 1-kilogram bar has lower fabrication costs per ounce than a 1-ounce coin because the fixed costs of assaying, handling, and certification get spread across more ounces.

If your goal is to acquire the most gold for the lowest total premium, larger bars make sense. If your goal is liquidity, divisibility, or resale recognition, coins justify the higher premium.

Here’s the question most price-shoppers skip: what role does this product need to play?

A 10-ounce bar is harder to sell in small increments than ten 1-ounce coins. A Gold Eagle is easier to authenticate and resell than a foreign-minted round most buyers have never heard of.

The premium isn’t just the cost to acquire the product today — it’s the cost of what that product does for you when you need it to perform. The process of buying gold should include that conversation upfront, not after you’ve already committed.

Market Conditions and Availability

Market conditions affect premiums — and those conditions change.

During peak market stress in 2020, premiums on popular gold coins rose from a typical 5% to over 10-12%. High demand, supply chain disruptions, and inventory shortages push premiums higher.

When everyone wants the same product at the same time, the premium reflects that scarcity.

Supply and demand dynamics for physical gold operate independently of the spot price.

The spot price tracks futures contracts — paper gold. Physical gold premiums track real-world availability — minted inventory, dealer stock levels, shipping bottlenecks, and regional demand spikes.

A dealer with deep inventory can offer tighter premiums during high-demand periods. A dealer scrambling to restock can’t — and the premium reflects that reality.

The premium isn’t a mystery to solve or a fee to resent — it’s the transparent cost of owning something real.

When a dealer obscures that calculation or races you to the bottom on price, they’ve already told you what they think of the relationship. The clarity you need exists upfront — or it doesn’t exist at all.

Brighton Gold’s approach is straightforward: explain what drives the premium, show you the components, and let you decide if the product fits the role you need it to play. That’s the conversation — not who quoted the lowest number on a single product on a single day.

| Product Type | Typical Premium Range | Why the Difference |

|---|---|---|

| 1-ounce American Gold Eagle coin | 5% – 12%+ | Higher fabrication costs per ounce due to intricate design and minting process; premiums spike during market stress or supply shortages |

| Popular coins during high-demand periods (e.g., 2020 market stress) | 10% – 12%+ | Market conditions like high demand or supply chain disruptions cause premiums to increase significantly |

How to Calculate the Premium on a Real Purchase

You’ve got the concept. You’ve got the drivers. Now let’s walk through the calculation with real numbers.

The formula is Total Price = (Spot Price per Ounce × Weight in Ounces) + Premium. The math isn’t the hard part. Finding the inputs is. Knowing what you’re looking at when you do is harder still.

Step 1: Find the Current Spot Price

The spot price comes from commodity exchanges like COMEX. It’s based on the most active front-month futures contract. Price discovery happens through continuous electronic trading, and the number you see is the market’s best estimate of what gold for immediate delivery is worth right now.

That means the number you see on Kitco, the World Gold Council, or your dealer’s website isn’t arbitrary. It’s the real-time reference point for the underlying gold value.

Where you check matters less than when. The spot price moves constantly during trading hours.

If you’re calling a dealer to lock in a purchase, ask them what spot price they’re using for the quote. If you’re buying physical gold for home delivery, the dealer should reference the current spot price of gold at the time they generate your invoice — not the price from yesterday or an estimate from earlier in the week.

Transparency starts here.

Step 2: Determine the Total Purchase Price

This is the all-in number the dealer quotes you. The actual dollar amount you’ll pay to complete the transaction. It includes the gold’s intrinsic value plus the premium.

Most dealers display this as a single line: “One-ounce Gold American Eagle — $2,135.” That’s your total purchase price. It’s not hidden. It’s not broken out unless you ask.

Here’s where the concierge difference shows up.

A dealer who wants you informed will show you the spot price, the premium, and how they add up to the total — before you commit. A dealer who wants you transacting will quote the total and move on.

Brighton Gold’s approach is the former. You see the calculation. You understand what you’re paying for. You decide if it makes sense.

Step 3: Calculate the Premium

Subtract the intrinsic gold value from the total purchase price.

Using the earlier example: spot price is $2,050. You’re buying one ounce. Total price quoted is $2,135. The calculation is $2,135 − ($2,050 × 1) = $85.

That $85 is the premium. The cost above spot that covers minting, distribution, insurance, dealer margin, and everything else that brought the physical product to you.

The premium isn’t arbitrary. It’s measurable.

And when a dealer can’t or won’t walk you through that math, you’ve learned something about the relationship. The premium you’re willing to pay should reflect the product you’re acquiring and the support you’re receiving — not just the lowest number someone shouted at you over the phone.

Step 4: Express the Premium as a Percentage

Divide the dollar premium by the intrinsic gold value. Multiply by 100.

Using the same example: ($85 ÷ $2,050) × 100 = 4.15%. That percentage lets you compare premiums across dealers and products. A 1-ounce coin at 4.15% versus a 10-ounce bar at 2.8%.

The percentage is the normalized cost of acquisition.

But here’s the part most price-comparison articles miss: the lowest percentage premium isn’t always the best deal.

A dealer offering a 3% premium on a product you’ve never heard of — with no buyback commitment, no post-purchase support, and no transparency about resale liquidity — isn’t offering value. They’re offering a number.

The premium reflects the product and the relationship. Both matter when you’re holding something for the long term.

| Step | Action | Example Calculation |

|---|---|---|

| 1. Find the Current Spot Price | Check a real-time pricing source (Kitco, World Gold Council, your dealer’s quote). The spot price is the baseline — the market price for immediate delivery of gold. | Spot price = $2,050 per ounce |

| 2. Identify the Total Purchase Price | This is the all-in dollar amount the dealer quotes you for the product. It includes the gold’s intrinsic value plus the premium. | Total purchase price = $2,135 |

| 3. Calculate the Intrinsic Gold Value | Multiply the spot price by the weight in troy ounces. For a one-ounce coin, this is straightforward. | Intrinsic value = $2,050 × 1 = $2,050 |

| 4. Subtract to Find the Dollar Premium | Subtract the intrinsic gold value from the total purchase price. The difference is the premium — the cost above spot. | Premium = $2,135 − $2,050 = $85 |

| 5. Calculate the Percentage Premium | Divide the dollar premium by the intrinsic gold value, then multiply by 100. This gives you the normalized premium as a percentage. | Percentage premium = ($85 ÷ $2,050) × 100 = 4.15% |

Frequently Asked Questions

The calculation is simple — but the same handful of questions come up every time.

Most aren’t about the math. They’re about whether what you’re paying for makes sense for the role you need gold to play.

Here’s what we hear.

What is a typical premium for a one-ounce American Gold Eagle coin?

There’s no fixed number. Premiums shift based on product, dealer, and market conditions.

What you see depends on demand, inventory, and market stress. During peak stress in 2020, premiums on popular coins jumped from the usual range to over 10-12%. That’s not the norm. That’s what happens when supply tightens and everyone wants the same product at once.

If a dealer won’t explain where their premium sits and why, you’re not having the right conversation.

Why is the premium on a gold coin different from a gold bar of the same weight?

Fabrication cost per ounce.

1-ounce coins cost more per ounce to produce than a 1-kilogram bar. The design, minting process, and security features all add cost. You’re not just paying for the gold — you’re paying for the work that turned raw metal into a finished product.

Bars are simpler. Coins aren’t.

That difference shows up in the premium — and in the liquidity and resale recognition when you move it later.

Do I get the premium back when I sell my physical gold?

No. The premium isn’t refundable.

When you sell, you’re paid based on spot price at that time and the dealer’s buyback terms. The premium you paid covered minting, fabrication, shipping, insurance, and dealer margins — costs that don’t reverse when you decide to sell.

What you get back depends on market conditions when you’re ready to move.

The premium was the cost of acquiring something real. It doesn’t come back — it was never meant to.

How does dealer inventory affect the premium on gold products?

Inventory levels influence pricing — sometimes significantly.

When a dealer has limited stock and high demand, premiums rise. When supply is strong and demand is steady, premiums stabilize. Straightforward supply-and-demand mechanics applied to a physical product with real production and storage costs.

That’s why shopping for the absolute lowest premium on a given day doesn’t tell you much.

The dealer who’s cheapest today isn’t always the dealer who’s transparent tomorrow.

Are gold premiums negotiable?

Sometimes. Not always.

Large purchases or established relationships sometimes open the door for pricing conversations. But if you’re chasing negotiation as the primary strategy, you’ve already shifted the focus from clarity to transaction.

Here’s what matters more: is the dealer explaining the premium upfront, breaking down what it covers, and showing you where your total cost sits relative to spot?

If that transparency isn’t there before you ask, negotiating a lower number doesn’t fix the problem.

Besides the premium, what other costs are involved in buying physical gold?

Shipping, insurance, and secure storage — if you’re holding it in a vault rather than taking delivery.

The premium covers minting, fabrication, assaying, certification, distribution, and dealer operating costs. But getting the product to you or storing it safely adds another layer. Those costs are separate line items in a transparent transaction.

If a dealer isn’t walking you through every cost before you commit, you’re not getting the full picture.

And without the full picture, you’re not making an informed decision.

Where This Leaves You

You know the formula. You know what drives the premium. You know how to run the calculation.

What you do with that clarity is up to you.

The premium isn’t negotiable. It’s the cost of owning something real — minted, assayed, shipped, insured, and backed by a dealer who answers the phone when you sell.

The math is simple. The decision is yours.

What separates a smart acquisition from a regrettable one isn’t chasing the lowest premium. It’s evaluating whether the premium reflects the product, the liquidity, and the support you’ll need over time.

A dealer who explains the calculation upfront — shows you the components, lets you decide based on value instead of pressure — isn’t being generous. That’s the relationship that lasts.

Brighton Gold’s concierge model exists for customers who want to understand what they’re paying for, why they’re paying it, and what they’re getting in return. That’s not a sales tactic. That’s the baseline.

The premium calculation isn’t complicated. What matters is whether you’re working with someone who walks you through it without turning it into a pressure pitch.

The clarity you need exists upfront — or it doesn’t exist at all.

If you’re ready to buy gold with that kind of transparency, Brighton Gold can walk you through setting up a Precious Metals IRA or acquiring physical gold for delivery. It starts with a conversation about what fits your situation — not a race to the bottom on spread.

The premium reflects the product and the support. Both matter when you’re holding something for the long term.

You know the formula now. You’ve seen what drives the spread. You understand what you’re paying for — and why. If you’re ready to move forward with that clarity, Brighton Gold offers a complimentary consultation to walk you through your options. No pressure. No race to the bottom on price. Just the full picture before you sign anything. The clarity you need exists upfront — or it doesn’t exist at all.