Passing gold to your heirs requires more planning than passing a bank account or brokerage holdings. Gold coins and bars don’t come with beneficiary designation forms. There’s no automatic transfer at death. And without proper documentation, your family may not even know where to find them.

The good news is that inherited gold receives favorable tax treatment through what the IRS calls a “step-up in basis.” This single rule can eliminate decades of appreciation from your heirs’ tax bill entirely. But the benefit only applies if you structure the transfer correctly.

Here’s what you need to know: physical gold held outside an IRA typically passes through your will or trust. Gold held inside an IRA passes through beneficiary designations. Each path has different tax implications, different documentation requirements, and different timelines your heirs must follow.

For most families, leaving gold in your estate rather than gifting it during your lifetime provides the best tax outcome. We’ll explain why, walk through the specific rules for 2026, and cover everything your heirs need to know when the time comes.

This guide covers physical gold and silver coins, bars, and bullion, as well as Precious Metals IRAs held with approved custodians. The principles apply whether you own a few coins or a substantial collection.

Understanding the Step-Up in Basis: The #1 Tax Advantage for Inherited Gold

The step-up in basis is the single most important tax concept for anyone planning to leave gold to their heirs.

When someone inherits gold, the IRS resets the “cost basis” to the fair market value on the date of death. This is true whether the gold was purchased last year or fifty years ago.

How the Step-Up Works in Practice

Consider this example. Your grandfather bought a Gold American Eagle in 1985 for $400. At the time of his passing in 2026, that coin is worth $2,800. Under normal capital gains rules, selling the coin would trigger a $2,400 taxable gain.

But with inheritance, the rules change.

Your new cost basis becomes $2,800 — the value at the date of death. If you sell immediately for $2,800, you owe nothing. The entire fifty years of appreciation disappears from the tax calculation.

If you hold the coin and sell later for $3,200, you only owe capital gains tax on $400 — the appreciation that occurred after you inherited it.

This is why estate planners consistently recommend holding appreciated assets until death rather than gifting them during your lifetime. The step-up in basis can save your heirs thousands of dollars in taxes.

Why This Matters for Gold Specifically

Gold’s long-term price trajectory makes the step-up especially valuable.

Gold traded around $35 per ounce before 1971. It hovered between $300 and $500 through much of the 1980s and 1990s. Today, gold trades well above $2,000 per ounce. You can track current pricing in our weekly Gold Market Recap.

If you purchased gold decades ago, your heirs could be looking at enormous taxable gains without the step-up protection. With proper estate planning, that liability resets to zero.

The IRS classifies gold and other precious metals as collectibles, which means long-term capital gains are taxed at a maximum rate of 28 percent rather than the standard 15 or 20 percent for most assets. This higher rate makes the step-up in basis even more valuable for gold owners.

Gifting vs. Inheriting: A Side-by-Side Comparison

The difference between gifting gold during your lifetime and leaving it through your estate is significant. Here’s how the numbers work:

| Scenario | Original Purchase Price | Value at Transfer | Recipient’s Cost Basis | Capital Gain if Sold Immediately |

|---|---|---|---|---|

| Gift During Lifetime | $500 | $2,500 | $500 (carryover basis) | $2,000 taxable gain |

| Inheritance at Death | $500 | $2,500 | $2,500 (stepped-up basis) | $0 taxable gain |

The table illustrates why inheritance typically beats gifting from a tax perspective. When you gift gold, your original cost basis “carries over” to the recipient. They’re on the hook for all the appreciation that occurred during your ownership.

When they inherit, the slate wipes clean.

There are exceptions to this general rule, which we’ll cover in the section on annual gift tax exclusions. But for most families with appreciated gold, the step-up in basis is too valuable to forfeit through lifetime gifting.

The 2026 Estate Tax and Gift Tax Limits

For 2026, the federal estate and gift tax exemption stands at $15 million per individual, according to IRS Revenue Procedure 2025-32. Married couples can effectively shield $30 million from federal estate and gift taxes.

This means most families will not owe any federal estate tax on gold or other assets. Your heirs receive the full value of your gold holdings without federal estate tax reducing their inheritance.

Annual Gift Tax Exclusion for 2026

The annual gift tax exclusion remains at $19,000 per recipient for 2026. This allows you to give up to $19,000 worth of gold to any number of people each year without filing a gift tax return or using any of your lifetime exemption.

Married couples can combine their exclusions through “gift splitting,” effectively giving $38,000 per recipient annually.

Here’s how you might use this strategically:

- Give one Gold American Eagle ($2,800 value) to each grandchild annually — well under the limit

- Transfer several coins to adult children each year without tax consequences

- Systematically reduce your estate over time if you’re approaching the exemption threshold

Important note: Even when using the annual exclusion, your heirs receive your original cost basis on gifted gold. They lose the step-up benefit. This makes strategic sense only in specific situations, such as when gold has minimal appreciation or when reducing estate size is a priority.

When Federal Estate Tax Applies

Federal estate tax only becomes a concern when total estate value exceeds $15 million for individuals or $30 million for married couples. The tax rate on amounts above the exemption is 40 percent.

If your estate includes gold as part of holdings that exceed these thresholds, consult an estate planning attorney about strategies such as:

- Irrevocable trusts designed for estate tax reduction

- Family limited partnerships

- Charitable giving structures

- Strategic lifetime gifting programs

For the vast majority of gold owners, federal estate tax is not a concern. The exemption levels are high enough that the step-up in basis and proper documentation are far more important than estate tax planning.

State Estate and Inheritance Taxes

Federal rules don’t tell the whole story. Several states impose their own estate or inheritance taxes with significantly lower exemption thresholds.

States like Massachusetts and Oregon have estate tax exemptions under $2 million. Six states currently levy inheritance taxes paid by the beneficiary rather than the estate.

If you live in a state with estate or inheritance taxes, your gold holdings could trigger state-level liability even when federal taxes don’t apply. Check with an estate attorney in your state to understand local requirements.

Physical Gold: Documentation and Transfer Strategies

Physical gold presents unique estate planning challenges. Unlike bank accounts or brokerage holdings, there’s no central registry tracking ownership. No automatic transfer mechanism. No death notification to a custodian.

Your heirs need to find the gold, prove ownership, and establish its value. Without proper documentation, any of these steps can fail.

The “Shoebox Problem”

We call it the shoebox problem because it happens more often than you’d expect. Someone passes away with gold coins hidden in a closet, safe, or safe deposit box — and nobody knows they exist.

Sometimes the gold is found years later during an estate sale. Sometimes it’s never found at all.

Other times, family members know gold exists but can’t locate it. They search the house, find an empty safe, and wonder if someone took it or if it was moved years ago.

Even when found, disputes arise. Multiple heirs may claim they were promised specific pieces. Without documentation, these arguments become family fractures.

Preventing the shoebox problem requires action today:

- Create a detailed inventory with descriptions, purchase information, and current storage location

- Store the inventory with your estate planning documents — not with the gold itself

- Inform your executor or trustee about the gold’s existence and location

- Update your inventory whenever you buy, sell, or move metals

Creating a Comprehensive Gold Inventory

Your inventory should include enough detail for heirs to identify, locate, value, and claim each item. At minimum, document:

| Information Type | Details to Record |

|---|---|

| Item Description | Type (coin, bar, round), weight, purity, year, mint mark |

| Purchase Information | Date purchased, dealer name, purchase price, receipt location |

| Current Location | Home safe combination, bank safe deposit box address and key location, depository account number |

| Authentication | Grading certificates, assay documentation, original packaging |

| Instructions | Preferred distribution among heirs, any items with sentimental significance |

Store this inventory in multiple secure locations. Your estate attorney should have a copy. Your executor should know where to find it. Consider a fireproof document safe for one copy and secure digital storage for another.

Review and update the inventory annually. Gold acquisitions, sales, and storage changes should be reflected immediately.

Working with Depositories and Storage Facilities

If you store gold with a third-party depository, the transfer process differs from home storage. Depositories maintain detailed records and typically have established procedures for estate transfers.

Contact your depository to understand their requirements. Most will need:

- Death certificate

- Letters testamentary or letters of administration from probate court

- Completed beneficiary claim forms

- Identification for the heir or executor

Brighton’s concierge team can help customers navigate this process with their depository when the time comes. Having records organized in advance makes the transfer significantly smoother.

Establishing Fair Market Value at Death

The IRS defines fair market value as “the price at which property would change hands between a willing buyer and a willing seller, neither being under any compulsion to buy or sell, and both having reasonable knowledge of relevant facts.”

For standard bullion coins and bars, fair market value is straightforward. Check the spot price of gold on the date of death, apply typical dealer premiums, and document the calculation.

For numismatic or rare coins, professional appraisal may be necessary. The value depends on condition, rarity, and collector demand rather than metal content alone.

Keep documentation of your fair market value calculation. The stepped-up basis is only as good as the supporting paperwork. If the IRS challenges your valuation, you’ll need records showing how you determined the date-of-death value.

The executor may also elect an “alternate valuation date” — six months after death — if it reduces both estate value and estate tax liability. This option only applies when federal estate tax is owed and the election benefits the estate. See IRS Publication 559 for detailed guidance on executor responsibilities.

Gold IRA Inheritance: The SECURE Act 10-Year Rule

Gold held inside an IRA follows different inheritance rules than physical gold held outside retirement accounts. The SECURE Act of 2019 fundamentally changed how non-spouse beneficiaries receive inherited IRAs, and those rules now apply to Gold IRAs as well.

Beneficiary Designations: Your Primary Estate Planning Tool

For Gold IRAs, beneficiary designations control who receives the account — not your will.

This is a critical distinction. Even if your will says your Gold IRA goes to your daughter, the account will transfer to whoever is named on the beneficiary form with your custodian.

Review your beneficiary designations regularly. Life changes such as marriage, divorce, births, and deaths should trigger an immediate review. Outdated designations are among the most common estate planning failures.

Your Gold IRA custodian maintains these forms. Contact them to verify current designations, add contingent beneficiaries, and ensure documentation is complete.

Spouse vs. Non-Spouse Beneficiaries

The rules differ significantly depending on whether a spouse or non-spouse inherits your Gold IRA.

Surviving Spouse Options:

- Roll the inherited IRA into their own IRA — treating it as their own account

- Keep it as an inherited IRA with distributions based on their life expectancy

- Take a lump sum distribution (triggering full taxation)

Spouses have the most flexibility. They can defer required distributions until they reach RMD age, extend distributions over their lifetime, and even name new beneficiaries.

Non-Spouse Beneficiary Options:

Under the SECURE Act rules, most non-spouse beneficiaries must fully distribute inherited IRA assets within 10 years of the original owner’s death. This applies to adult children, grandchildren, siblings, and other individual beneficiaries.

The 10-year rule eliminates the previous “stretch IRA” strategy that allowed beneficiaries to take small distributions over their lifetime.

Understanding the 10-Year Distribution Requirement

The 10-year rule requires complete distribution of the inherited IRA by December 31 of the tenth year following the original owner’s death.

However, the rule has nuances:

If the original owner died before reaching their Required Beginning Date for RMDs, beneficiaries can take distributions in any amount at any time during the 10-year window. They could wait until year 10 and take everything at once.

If the original owner died after beginning RMDs, beneficiaries must take annual required minimum distributions during years 1 through 9, then empty the account in year 10. This interpretation was confirmed in IRS final regulations taking effect in 2025.

The key point for Gold IRA owners: your heirs will face ordinary income tax on distributions, regardless of timing. The metals don’t need to be sold within the IRA, but removing them from the IRA wrapper triggers taxation at their fair market value.

Eligible Designated Beneficiaries: Exceptions to the 10-Year Rule

Certain beneficiaries are exempt from the 10-year requirement and can still stretch distributions over their life expectancy:

- Surviving spouses

- Minor children of the account owner (until age 21, then 10-year rule applies)

- Disabled individuals

- Chronically ill individuals

- Individuals not more than 10 years younger than the deceased owner

If your intended beneficiary falls into one of these categories, consult with your custodian and a tax professional about documentation requirements and distribution options.

Gold IRA Distribution Strategies for Heirs

When heirs receive a Gold IRA, they have decisions to make about timing and form of distributions.

Strategic considerations:

- Spreading distributions over the 10-year period may keep heirs in lower tax brackets

- Taking distributions in years with lower income can minimize tax impact

- Taking in-kind distributions (actual metals rather than cash) is possible with most custodians

- Converted metals become physical gold outside the IRA, held with a new cost basis equal to the distribution value

For heirs who want to continue holding gold, taking in-kind distributions allows them to receive the actual metals. Once distributed, the gold is theirs to hold, sell, or pass on as they choose.

Brighton assists families navigating inherited Gold IRA distributions. Our concierge team can explain options, connect heirs with custodians, and provide guidance on next steps.

Estate Planning Documents for Gold Owners

A complete estate plan for gold owners includes several essential documents. Each serves a specific purpose in ensuring your gold transfers smoothly and according to your wishes.

Will or Trust: Directing Your Gold

Your will or revocable living trust specifies who receives your physical gold and how it should be divided.

For a Will:

- Gold passes through probate before reaching heirs

- Court supervision ensures proper distribution

- Process is public record

- Timeline varies by state but often takes months

For a Revocable Living Trust:

- Gold owned by the trust avoids probate

- Distribution can occur immediately after death

- Process remains private

- Successor trustee manages the transfer

Many gold owners prefer trusts for privacy and speed. Probate records are public, meaning anyone can see what you owned and who received it. Trusts keep this information confidential.

If you use a trust, ensure your gold is properly titled in the trust’s name or that the trust is named as beneficiary of any depository accounts.

Letter of Instruction: Practical Guidance

A letter of instruction supplements your legal documents with practical information that helps your executor and heirs.

This is where you record:

- Safe combinations and key locations

- Depository account numbers and contact information

- Location of purchase records and inventory

- Instructions for finding gold stored at home

- Guidance on dealers you’ve worked with

- Preferences for distribution among heirs

Unlike your will, the letter of instruction is not a legal document. But it’s often the most useful document for heirs trying to locate and manage inherited gold.

Store copies with your estate planning attorney, your executor, and in a location your family can access.

Power of Attorney: Managing Gold During Incapacity

A durable power of attorney allows someone you trust to manage your gold if you become incapacitated.

Without this document, your family may need court intervention to access or sell gold if you cannot manage your own affairs. The process is time-consuming and expensive.

Ensure your power of attorney specifically mentions authority over precious metals, safe deposit boxes, and storage accounts. Generic language may not be sufficient for some institutions.

Beneficiary Designations: Keeping Them Current

We’ve mentioned beneficiary designations for Gold IRAs, but they apply elsewhere too.

If you have a depository account, check whether beneficiary designations are available. Some depositories allow transfer-on-death arrangements that bypass probate.

Review all beneficiary designations annually and after major life events. Common triggers include:

- Marriage or divorce

- Birth or adoption of children or grandchildren

- Death of a named beneficiary

- Changes in family relationships

Outdated designations create conflict and may result in unintended recipients. A few minutes of annual review prevents significant problems.

Tax Reporting for Inherited Gold

Heirs who inherit gold need to understand their tax reporting obligations — both at the time of inheritance and when they eventually sell.

At the Time of Inheritance

Good news first: Receiving inherited gold does not trigger income tax. You don’t report the inheritance on your tax return simply because you received it.

Federal estate tax, if owed, is paid by the estate — not by individual heirs. And for estates under the $15 million threshold, no federal estate tax applies.

State inheritance taxes work differently. In states that impose them, heirs may owe tax on what they receive. Rates and exemptions vary by state and sometimes by relationship to the deceased.

Establishing and Documenting Your Basis

Your most important task after inheriting gold is documenting your stepped-up cost basis.

Obtain or create records showing:

- The date of death

- Fair market value of each gold item on that date

- How fair market value was determined (spot price, dealer quotes, professional appraisal)

- Any estate documents confirming the valuation

Keep these records indefinitely. When you eventually sell — whether that’s next year or thirty years from now — you’ll need documentation supporting your cost basis.

The IRS can challenge your basis if you lack adequate records. Without proof, they may assert a basis of zero, making your entire sale price taxable.

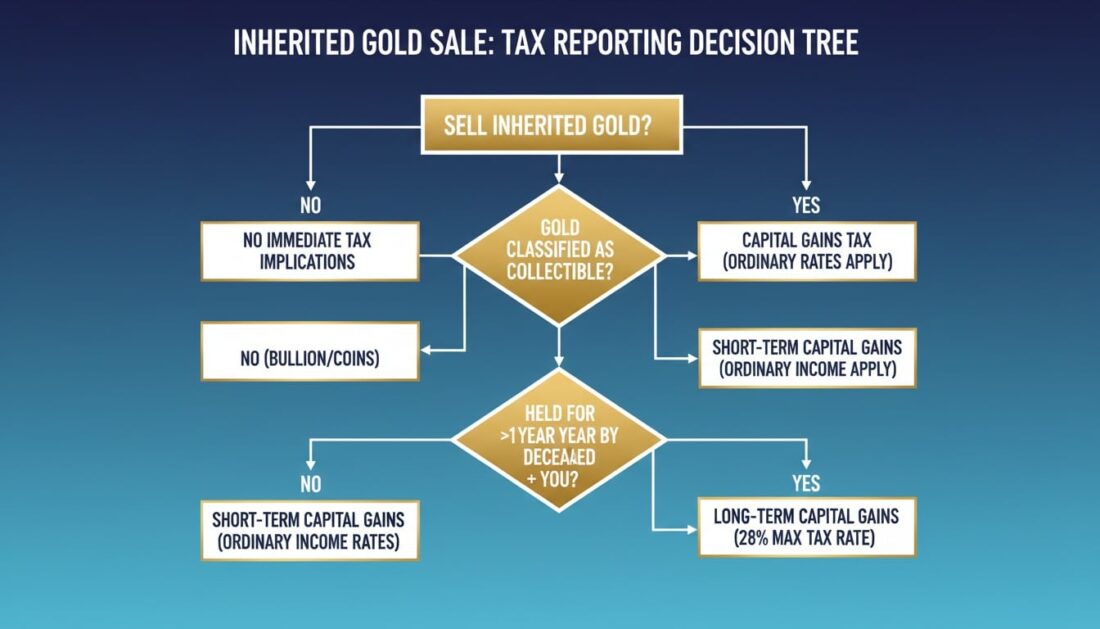

When You Sell: Capital Gains Reporting

Selling inherited gold triggers capital gains tax on any appreciation above your stepped-up basis.

Key points for reporting:

- Report sales on Schedule D (Form 1040)

- Detail transactions on Form 8949

- Calculate gain as sale price minus stepped-up basis

- Apply the 28 percent maximum rate for collectibles

Inherited assets are automatically treated as long-term for capital gains purposes, regardless of how long you personally held them. This provides the more favorable long-term rate rather than short-term ordinary income rates.

If you sell at a loss — meaning the gold declined in value after you inherited it — the loss can offset other capital gains or up to $3,000 of ordinary income annually.

The 28 Percent Collectibles Rate

The IRS classifies gold as a collectible, which carries a maximum capital gains rate of 28 percent rather than the standard 15 or 20 percent for most assets.

This doesn’t mean you’ll automatically pay 28 percent. The actual rate depends on your overall taxable income:

| Your Marginal Tax Bracket | Rate on Collectible Gains |

|---|---|

| 10% or 12% | Your marginal rate (10% or 12%) |

| 22% or higher | 28% maximum |

Lower-income heirs may pay less than 28 percent on gold sales. Higher-income heirs hit the 28 percent ceiling.

This is another reason the step-up in basis matters so much. Every dollar of pre-inheritance appreciation that the step-up eliminates is a dollar that won’t be taxed at this elevated rate.

Frequently Asked Questions

Do my heirs pay taxes when they inherit my gold?

Heirs generally do not owe income tax simply for receiving inherited gold. Federal estate taxes only apply if the total estate exceeds $15 million in 2026. However, when heirs sell the gold, they may owe capital gains tax on any appreciation above the stepped-up basis value established at the date of death.

The stepped-up basis eliminates taxes on appreciation that occurred during your lifetime. Only gains occurring after inheritance become taxable when sold.

What is the step-up in basis for inherited gold?

The step-up in basis resets the cost basis of inherited gold to its fair market value on the date of the original owner’s death. This means if gold was purchased for $500 and is worth $2,500 at death, the heir’s new basis is $2,500. If they sell immediately for $2,500, there is no taxable gain.

This is the single most valuable tax benefit for inherited gold. It can eliminate decades of appreciation from the tax calculation entirely.

Is it better to gift gold now or leave it in my will?

In most cases, leaving gold in your will provides better tax treatment for your heirs. Inherited gold receives a step-up in basis to fair market value at death, potentially eliminating decades of appreciation from taxation. Gifted gold retains your original cost basis, meaning heirs could owe capital gains on all appreciation since your purchase.

The exception is when you want to reduce a taxable estate or when gold has not appreciated significantly since purchase. Consult with an estate planning professional about your specific situation.

How do I pass my Gold IRA to my children?

Name your children as beneficiaries on your Gold IRA account. Under SECURE Act rules, non-spouse beneficiaries must generally withdraw all funds within 10 years of your death. The metals do not need to be sold within the IRA, but they must be distributed from the IRA wrapper, triggering ordinary income tax on the fair market value at distribution.

Review beneficiary designations regularly to ensure they reflect your current wishes.

What is the capital gains tax rate on inherited gold?

The IRS classifies gold as a collectible, subject to a maximum long-term capital gains rate of 28 percent. However, heirs only pay tax on gains above the stepped-up basis. If they sell shortly after inheriting, there may be little or no gain to report.

Lower-income heirs may pay less than 28 percent based on their marginal tax bracket.

How do I document my gold for my heirs?

Create a detailed inventory listing each item with purchase date, price, dealer name, and current storage location. Store copies with your estate planning documents and share access information with your executor. Include safe combinations, depository contact information, and any authentication certificates.

Update the inventory whenever you buy, sell, or relocate metals. Review it annually as part of your estate planning checkup.

What happens if my heirs cannot find my gold?

Physical gold without documentation or known location may be lost, disputed among family members, or claimed by the state as unclaimed property. Creating a clear inventory, informing your executor, and including specific instructions in your estate plan prevents this common problem.

Don’t assume family members know about or can locate your gold. Explicit documentation saves significant stress during an already difficult time.

Can I give gold to my grandchildren without paying gift tax?

Yes. The annual gift tax exclusion for 2026 is $19,000 per recipient. You can give up to $19,000 worth of gold to each grandchild without filing a gift tax return. Married couples can give $38,000 per grandchild by combining their exclusions through gift splitting.

Remember that gifted gold carries over your original cost basis rather than receiving a step-up. Consider the tax implications before choosing gifting over inheritance.

Conclusion

Passing gold to your heirs requires attention to details that most financial assets don’t demand. The combination of physical possession, favorable tax treatment, and specialized IRA rules means estate planning for gold deserves specific focus.

The step-up in basis remains your most powerful tool. For most families, leaving gold through your estate rather than gifting it during your lifetime provides the best tax outcome for heirs.

Proper documentation — including a detailed inventory, clear storage instructions, and current beneficiary designations — prevents the common problems that derail gold transfers. Take time now to create and maintain these records.

Brighton does not provide tax or legal advice. The information in this guide is educational only. Consult your CPA, estate attorney, or tax professional for guidance specific to your situation. Precious metals may appreciate, depreciate, or remain unchanged in value.

Ready to Protect Your Legacy?

If you’re thinking about how your gold fits into your overall estate plan, you’re not alone. Most customers we work with have questions about documentation, storage options, and how to make things as straightforward as possible for their families.

That’s why we offer a complimentary consultation to walk you through your options — including our No Fee Precious Metals IRA, which covers custodial fees for the lifetime of the account on qualified purchases. (Subject to minimum purchase requirements; ask your representative for details.)

We’ll show you exactly:

- How the No Fee IRA works and whether you qualify

- The difference between U.S.-minted coins and foreign alternatives

- What to expect from the purchasing and delivery process

- How to roll over or transfer existing retirement funds

- What ongoing support looks like after your purchase

Learn About the No Fee IRA — no obligation, just actionable insights you can use whether you work with us or not.

Your family’s financial legacy deserves the same careful planning you’ve applied to building it.