Yes—you can roll over your 401(k) to a Gold IRA without paying taxes or penalties. The key is using a direct rollover, where funds transfer straight from your old plan to your new self-directed IRA. You never touch the money, so the IRS doesn’t treat it as a distribution.

Here’s the short version: request a direct rollover from your 401(k) administrator, open a self-directed IRA with a custodian that allows precious metals, and choose IRS-approved gold products once the funds arrive. Most customers complete the entire process in under two weeks. And once the funds arrive, you can start acquiring IRS-approved physical gold and silver right away.

The longer version—with every step, rule, and potential pitfall explained—is what we’ll cover below. By the end, you’ll know exactly how to move your retirement savings into physical gold while staying completely within IRS guidelines.

Understanding Direct vs. Indirect Rollovers [H2]

Before we go further, let’s get clear on terminology. The IRS uses specific words—and the differences matter.

Direct Rollover: The Recommended Path [H3]

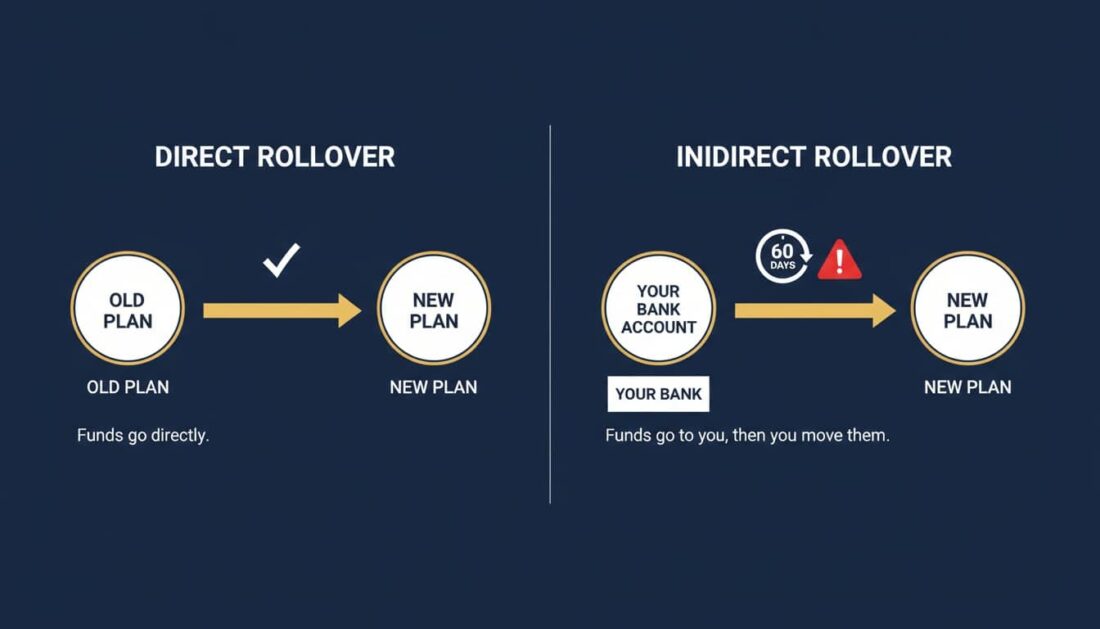

A direct rollover moves your 401(k) funds straight to your new Gold IRA. The transaction happens between custodians. You never see a check with your name on it.

Why does this matter?

- No withholding — Your employer doesn’t hold back 20% for taxes because you’re not receiving a distribution.

- No deadline pressure — There’s no 60-day window to worry about. The funds go directly where they belong.

- No annual limits — The IRS one-rollover-per-year rule applies to indirect IRA-to-IRA rollovers—not direct transfers from a 401(k).

According to IRS guidance on rollovers, this is the cleanest way to move retirement funds while keeping their tax-advantaged status intact.

Indirect Rollover: The Riskier Alternative [H3]

With an indirect rollover, your 401(k) plan pays you directly. You receive a check. Then you have exactly 60 days to deposit those funds into your new Gold IRA.

Here’s what makes this tricky:

- 20% mandatory withholding — Your employer must withhold 20% for federal taxes—even if you plan to roll over every dollar. To complete a full rollover, you’ll need to come up with that 20% from your own pocket, then claim it back when you file taxes.

- Hard 60-day deadline — Day 61 means the entire amount becomes taxable income. If you’re under 59½, add a 10% early withdrawal penalty on top of that. IRS Topic 413 explains these consequences in detail.

- One-per-year limitation — For IRA-to-IRA rollovers, the IRS limits you to one per 12-month period across all your accounts.

Why This Matters [H3]

The direct rollover removes almost all the ways things can go wrong.

No scrambling to meet deadlines. No withholding to make up. No risk of accidentally triggering a taxable event.

For most customers, this is the obvious choice. The process is seamless, and the outcome is exactly what you’d expect: your retirement savings move from one tax-advantaged account to another—without the IRS taking a cut along the way.

| Method | Tax Withholding | Time Limit | Annual Limit | Risk Level |

|---|---|---|---|---|

| Direct Rollover | None | None | Unlimited | Low |

| Indirect Rollover | 20% withheld | 60 days | One per year (IRA-to-IRA) | Higher |

| IRA Transfer | None | None | Unlimited | Low |

Is Your 401(k) Eligible for Rollover? [H2]

Not every 401(k) can be rolled over right away. Your options depend on one main factor: your employment status with the company that sponsors the plan.

If You’ve Left the Company [H3]

Good news. Once you’ve separated from service—whether through retirement, a job change, or a layoff—your 401(k) is fully portable.

You can roll it over to a Gold IRA at any time. No waiting period. No age requirement.

Many people have old 401(k) accounts sitting with former employers. Sometimes they forget about them entirely. These accounts are ideal candidates for consolidation into a self-directed IRA where you have more control—and more options.

If you’re not sure whether you have an old account somewhere, the Department of Labor’s Abandoned Plan Search can help you track it down.

If You’re Still Employed [H3]

This is where it gets more nuanced.

Rolling over your 401(k) while still working for the sponsoring company is called an in-service distribution. Federal law allows it—but your plan doesn’t have to offer it.

Common eligibility rules for in-service rollovers include:

- Age 59½ threshold — Many plans only permit in-service rollovers after you reach this age.

- Years of participation — Some plans require five years as an active participant before you can access funds.

- Account seasoning — Certain plans allow rollovers only for money that’s been in the account for at least two years.

- Contribution type restrictions — Your plan might allow rollovers from employer match or profit-sharing accounts—but not from your salary deferrals.

You’ll find these details in your plan’s Summary Plan Description (SPD). Your HR department or plan administrator can provide a copy.

What You Can Do [H3]

If in-service rollovers aren’t available, you’re not stuck. You simply wait until you leave the company—and in the meantime, you can start researching your options.

Identify a Gold IRA provider you trust. Understand the products available. Get positioned so you’re ready to move quickly when the time comes.

The Step-by-Step Rollover Process [H2]

Here’s exactly what the process looks like from start to finish. Most customers complete everything within two weeks—sometimes faster.

Step 1: Choose Your Precious Metals Provider [H3]

Start by selecting a company that specializes in Gold IRAs and retirement rollovers.

This is the team that will guide you through the process, answer your questions, and help you select IRS-approved products once your account is funded.

What to look for:

- Experience with 401(k) rollovers — They should understand IRS regulations and common pitfalls.

- Clear pricing — No hidden fees, no pressure tactics, no last-minute surprises.

- Concierge service — Support at every stage of ownership, not just at the point of sale.

- Established custodian relationships — A provider with strong custodian partnerships makes the process more seamless.

Brighton Gold, for example, offers a relationship-first approach. We walk customers through each step—from initial consultation through delivery to the depository—and we remain available long after the transaction is complete.

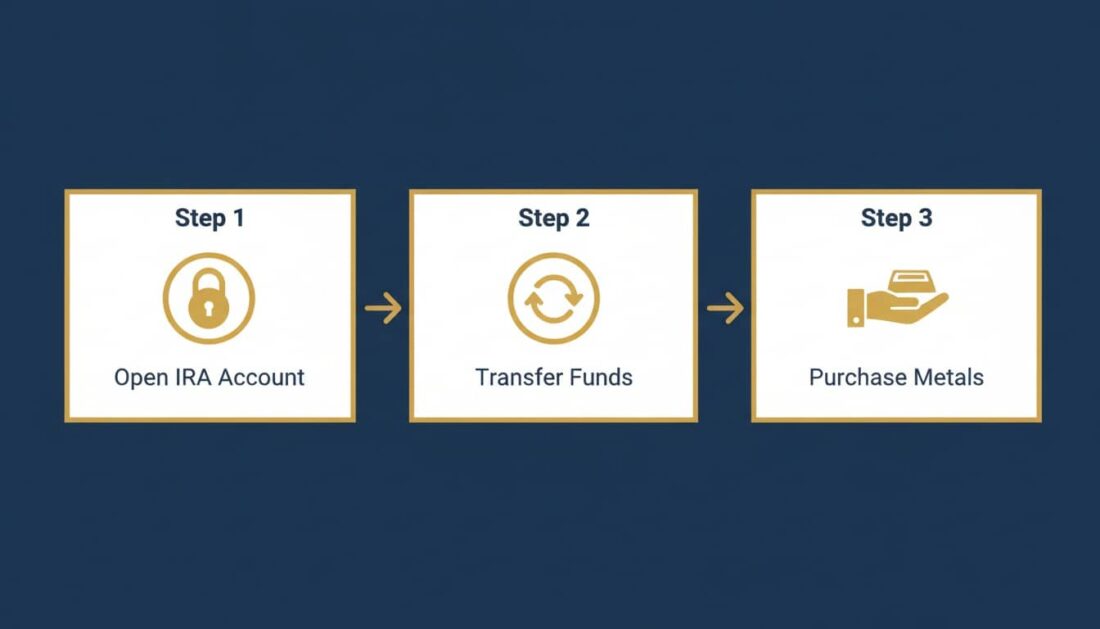

Step 2: Open Your Self-Directed IRA [H3]

Your Gold IRA must be held by an IRS-approved custodian that allows physical precious metals. Most traditional brokerages don’t offer this because they don’t handle tangible assets.

Self-directed IRA custodians specialize in alternative holdings: precious metals, real estate, private equity. Your precious metals provider will typically recommend custodians they work with regularly.

Opening the account is straightforward:

- Complete the application (10-15 minutes)

- Provide a government-issued ID

- Designate beneficiaries

- Sign custodial agreements

You’ll choose between a Traditional Gold IRA or a Roth Gold IRA based on your current account type. Traditional 401(k) funds roll into a Traditional IRA. Roth 401(k) funds roll into a Roth IRA.

Step 3: Initiate the Direct Rollover [H3]

Contact your 401(k) plan administrator and request a direct rollover. You’ll complete distribution paperwork that specifies:

- The amount to roll over (partial or full balance)

- Your new custodian’s name and address

- Your new IRA account number

- Instructions to make the check payable to your custodian “FBO” (for the benefit of) your name

Your new custodian can provide a letter of acceptance confirming they’re ready to receive the funds. Some plan administrators require this before processing.

The IRS rollover chart confirms that 401(k) plans can roll directly into Traditional IRAs—and Roth 401(k) accounts can roll into Roth IRAs.

Step 4: Wait for the Funds to Arrive [H3]

Most direct rollovers complete within 10 to 14 business days. Some plans take longer.

During this period:

- Keep records of all communications with your former plan administrator

- Confirm with your new custodian when funds are received

- Don’t worry if the timeline extends slightly—processing delays are common

Once the money arrives in your self-directed IRA, you’re ready to acquire precious metals.

Step 5: Select IRS-Approved Precious Metals [H3]

Work with your precious metals provider to choose products that meet IRS requirements. Not all gold qualifies—the IRS has specific purity and sourcing standards.

We’ll cover the eligible products in detail in the next section. For now, the key point is this: your provider should make this easy. They should clearly explain what qualifies, what doesn’t, and why certain products make more sense for your situation than others.

Step 6: Arrange Secure Storage [H3]

IRS regulations require your Gold IRA metals to be stored in an approved depository—not at home, not in a safe deposit box.

You’ll choose between two options:

- Segregated storage — Your metals stored separately from other customers’ holdings. Higher security, higher cost ($100-$300/year).

- Non-segregated storage — Your metals pooled with other customers’ holdings of the same type. Lower cost ($50-$150/year).

Major approved depositories include Delaware Depository (Wilmington, DE) and Brink’s Global Services (Los Angeles, Salt Lake City, New York).

Rollover Timeline Overview [H3]

| Stage | What Happens | Typical Timeframe |

|---|---|---|

| Account Setup | Open self-directed IRA, complete paperwork | 1-2 business days |

| Rollover Request | Submit distribution forms to 401(k) administrator | 1-3 business days |

| Fund Transfer | 401(k) custodian processes and sends funds | 7-14 business days |

| Metal Purchase | Select and acquire IRS-approved precious metals | 1-2 business days |

| Depository Delivery | Metals shipped to secure storage facility | 5-7 business days |

| Total | From start to metals in storage | 2-4 weeks |

Which Precious Metals Qualify for Your Gold IRA? [H2]

The IRS doesn’t allow just any gold or silver in a retirement account. There are strict purity standards—and purchasing the wrong products could disqualify your entire IRA. These requirements come from IRC Section 408(m)(3), which specifies exactly which metals qualify.

Here’s what you need to know.

Gold Standards [H3]

Gold must be at least 99.5% pure (0.995 fineness) to qualify for IRA ownership.

There’s one important exception: the American Gold Eagle. Despite containing only 91.67% gold (22 karat), Congress specifically exempted this coin under the Taxpayer Relief Act of 1997. A one-ounce American Gold Eagle still contains exactly one troy ounce of pure gold—the coin simply weighs more because it includes copper and silver for durability.

At Brighton Gold, we focus primarily on U.S.-minted products like the Gold American Eagle. These coins carry the backing of the United States government for weight, content, and purity.

Eligible Gold Products [H3]

| Product | Purity | Mint | Notes |

|---|---|---|---|

| American Gold Eagle | 91.67% (22k) | U.S. Mint | Congressional exemption, most recognized |

| American Gold Buffalo | 99.99% (24k) | U.S. Mint | First 24k coin from U.S. Mint |

| Canadian Gold Maple Leaf | 99.99% (24k) | Royal Canadian Mint | Advanced security features |

| Austrian Gold Philharmonic | 99.99% (24k) | Austrian Mint | Europe’s best-selling gold coin |

| Gold Bars | 99.5%+ | COMEX/NYMEX-approved refiners | Lower premiums on larger sizes |

Silver, Platinum, and Palladium [H3]

Your Gold IRA can hold other precious metals too. The purity requirements vary by metal:

- Silver (99.9% pure) — American Silver Eagles, Canadian Silver Maple Leafs, qualifying silver bars

- Platinum (99.95% pure) — American Platinum Eagles, qualifying platinum bars

- Palladium (99.95% pure) — Canadian Palladium Maple Leafs, qualifying palladium bars

For a deeper look at silver options, see our guide on the best silver coins for purchasers.

What Doesn’t Qualify [H3]

The IRS explicitly prohibits certain items:

- Collectible and numismatic coins — Coins valued for rarity or condition rather than metal content don’t qualify. The IRS treats these as collectibles.

- Gold jewelry and gold-plated items — These don’t meet purity requirements.

- Foreign coins below purity standards — Some foreign coins contain gold but don’t meet the 99.5% threshold.

- Bars from non-approved refiners — Bars must come from COMEX, NYMEX, or LBMA-approved sources.

The bottom line: Work with a provider that specializes in IRA-approved products. If something doesn’t qualify, you want to know before you buy—not after.

As with any acquisition, precious metals may appreciate, depreciate, or remain unchanged based on market conditions. Resale values depend on the market at the time of sale.

Understanding the IRS Rules That Keep You Penalty-Free [H2]

The IRS has clear rules for retirement rollovers. Follow them, and your funds stay tax-advantaged. Break them—even accidentally—and you could face unexpected taxes, penalties, or worse.

Here’s what matters most.

The 60-Day Rule [H3]

If you receive funds directly (indirect rollover), you have exactly 60 calendar days to deposit them into a qualifying IRA.

Miss the deadline, and the IRS treats the entire amount as a taxable distribution.

If you’re under 59½, add a 10% early withdrawal penalty.

There’s no grace period. Day 61 is too late.

The IRS may waive this deadline in limited situations—financial institution errors, hospitalization, natural disasters—but you’d need to apply for relief. For complete details, see IRS Publication 590-A. Why take the risk when a direct rollover avoids the issue entirely?

The One-Rollover-Per-Year Rule [H3]

Since 2015, the IRS has limited indirect IRA-to-IRA rollovers to one per 12-month period. This applies across all your IRAs—not per account.

But here’s the good news: this rule doesn’t apply to 401(k)-to-IRA rollovers.

And it doesn’t apply to direct rollovers or transfers at all.

If you’re moving money from a former employer’s 401(k) to a Gold IRA using the direct method, you’re in the clear.

Contribution Limits Don’t Apply to Rollovers [H3]

The standard IRA contribution limits ($7,000 for 2024, or $8,000 if you’re 50+) apply to new contributions only—not rollovers.

You can roll over $50,000, $500,000, or more in a single transaction. There’s no cap.

This is especially important for customers with substantial 401(k) balances. You don’t need to roll over in stages.

Storage Requirements [H3]

Your Gold IRA metals cannot be stored at home.

The IRS requires all precious metals in an IRA to be held by an approved depository. Taking personal possession—even briefly—constitutes a distribution.

That means:

- Taxes on the full value

- 10% penalty if you’re under 59½

- Loss of tax-advantaged status

Some companies advertise “home storage” Gold IRAs using LLC structures. The IRS has not approved these arrangements, and promoters have faced enforcement actions. Don’t take the risk.

Common Mistakes That Trigger Penalties [H2]

Knowing what can go wrong helps you steer clear of costly errors. These are the mistakes we see most often—and how to avoid them.

Missing the 60-Day Deadline [H3]

This is the most common reason rollovers fail.

The check arrives. Life gets busy. Before you know it, two months have passed.

The consequence: The entire amount becomes taxable income—plus a 10% early withdrawal penalty if you’re under 59½.

The solution: Use a direct rollover. No deadline to miss.

Not Replacing the 20% Withholding [H3]

With an indirect rollover, your employer withholds 20% for taxes—even if you plan to roll over every penny.

Here’s how that plays out:

You have a $100,000 401(k). You request an indirect rollover. Your employer sends you a check for $80,000 (withholding $20,000). To complete a full rollover, you must deposit $100,000 into your new IRA within 60 days.

Where does the extra $20,000 come from? Your pocket.

If you only deposit the $80,000 you received, the IRS treats the missing $20,000 as a taxable distribution.

The solution: Direct rollover. No withholding, no shortfall.

Purchasing Non-Approved Metals [H3]

Some dealers push high-commission numismatic coins that don’t qualify for IRA ownership. They profit from inflated markups—and you’re left with products that can’t go in your retirement account.

The consequence: If non-approved metals end up in your IRA, the IRS may disqualify the account entirely.

The solution: Work with a provider that specializes in IRA-eligible bullion—not collectibles. Ask questions. Get clarity before you buy.

Attempting Home Storage [H3]

We touched on this earlier, but it’s worth repeating.

Taking personal possession of IRA metals—for any reason—triggers a taxable distribution. The “home storage IRA” promoted by some companies has not been approved by the IRS.

The consequence: Taxes, penalties, and loss of tax-advantaged status.

The solution: Use an IRS-approved depository. There’s no legitimate workaround.

For questions about your specific tax situation, consult your CPA or tax professional for guidance tailored to your circumstances.

Comparison: Mistake Consequences [H3]

| Mistake | Tax Consequence | Penalty | Additional Risk |

|---|---|---|---|

| Missing 60-day deadline | Full amount taxable | 10% if under 59½ | Permanent loss of tax-deferred status |

| Not replacing 20% withholding | Shortfall taxable | 10% if under 59½ | Reduced rollover amount |

| Purchasing non-approved metals | Potential account disqualification | Varies | Loss of IRA status |

| Home storage | Full amount taxable | 10% if under 59½ | Possible additional IRS penalties |

What to Expect After Your Rollover [H2]

Once your funds arrive and you’ve acquired your metals, here’s what ongoing ownership looks like.

Account Statements [H3]

Your custodian will send regular statements showing:

- Your account value based on current spot prices

- Details of metals held in storage

- Any transactions during the statement period

- Fees charged to the account

For tax purposes, the custodian reports your account to the IRS annually. You won’t receive a 1099 unless you take a distribution.

Required Minimum Distributions [H3]

Like any Traditional IRA, your Gold IRA will eventually require minimum distributions. Current rules require RMDs to begin by April 1 of the year after you turn 73. For complete distribution rules, see IRS Publication 590-B.

You can satisfy RMD requirements by:

- Selling metals within the IRA and taking a cash distribution

- Taking an “in-kind” distribution of physical metals (the metals are shipped to you)

With an in-kind distribution, you take possession of the actual metal. You’ll owe income tax on the distribution value, but no penalty applies if you’re over 59½.

Selling and Liquidity [H3]

Your Gold IRA metals can be sold at any time. Your provider coordinates with the depository to verify holdings and complete the transaction. Proceeds are deposited back into your IRA.

Brighton Gold offers repurchase options for metals originally purchased through our program. Having an established relationship simplifies the process when you’re ready to sell.

For current market conditions and pricing trends, visit our Gold Market Recap.

Ongoing Support [H3]

This is where the right provider makes a real difference.

At Brighton Gold, we believe in support at every stage of ownership—not just at the point of sale. Questions come up. Markets shift. Circumstances change.

You deserve a team that’s available when you need them. That’s the concierge experience we’re known for.

Frequently Asked Questions [H2]

Can I roll over my 401(k) to a Gold IRA without paying taxes? [H3]

Yes. A direct rollover is not a taxable event.

The funds transfer directly between custodians. You never take possession. The IRS doesn’t treat it as a distribution—so no taxes apply.

This is the recommended method for exactly this reason. Your retirement savings maintain their tax-deferred status, and you can start acquiring IRS-approved precious metals as soon as the funds arrive.

What is the 60-day rule for Gold IRA rollovers? [H3]

If you choose an indirect rollover, the IRS gives you 60 days to deposit the funds into your new Gold IRA.

Miss the deadline—even by one day—and the entire amount becomes taxable income. If you’re under 59½, add a 10% early withdrawal penalty.

The clock starts when you receive the funds. Weekends and holidays count. This is why most customers choose the direct rollover instead.

Can I roll over my 401(k) while still employed? [H3]

It depends on your plan.

Some 401(k) plans allow in-service rollovers after age 59½ or after meeting certain participation requirements. Others restrict rollovers until you leave the company.

Check your Summary Plan Description or ask your HR department. If in-service rollovers aren’t available, you can still plan ahead—research your options now so you’re ready to move when you separate from service.

What types of gold qualify for a Gold IRA? [H3]

The IRS requires gold to be at least 99.5% pure.

The exception: American Gold Eagles (91.67% gold) are specifically permitted by Congress.

Eligible products include American Gold Eagles, American Gold Buffalos, Canadian Gold Maple Leafs, Austrian Philharmonics, and gold bars from approved refiners.

Numismatic or collectible coins do not qualify. When in doubt, ask your provider before purchasing.

How long does a 401(k) to Gold IRA rollover take? [H3]

Most direct rollovers complete within 10 to 14 business days.

The timeline depends on your former employer’s processing speed. Once funds arrive, you can purchase metals immediately. Those metals typically reach the depository within another 5-7 business days.

Can I store my Gold IRA metals at home? [H3]

No.

IRS regulations require all Gold IRA assets to be held in an approved depository. Storing at home—even briefly—constitutes a distribution, triggering taxes and potential penalties.

Don’t be misled by “home storage IRA” promotions. The IRS has not approved these structures.

What fees are involved in a Gold IRA rollover? [H3]

Typical fees include:

- Account setup: $50-$300 (one-time)

- Annual custodian fees: $80-$300

- Storage fees: $100-$300 (varies by storage type)

Brighton Gold offers a No Fee IRA on qualified purchases that covers custodial fees for the lifetime of the account. This significantly reduces your ongoing costs compared to standard arrangements.

Is there a limit on how much I can roll over? [H3]

No.

Rollover contributions are not subject to annual IRA contribution limits. You can roll over your entire 401(k)—whether that’s $50,000 or $5 million—in a single transaction.

The standard contribution limits only apply to new cash contributions.

Taking the Next Step [H2]

Rolling over your 401(k) to a Gold IRA doesn’t have to be complicated.

The direct rollover method keeps it simple. Your funds move between custodians. No taxes withheld. No deadlines to track. No penalties to worry about.

The result: tangible ownership of physical gold, held inside a tax-advantaged retirement account.

For customers who want something they can see and touch—something outside the traditional financial system—this is the path to get there.

The key is working with a team that understands both the IRS requirements and the practical steps involved. A team that offers clarity when you have questions. A team that remains available long after the initial transaction.

That’s what we do at Brighton Gold.

Ready to Explore Your Options?

If you’re considering moving part of your retirement savings into physical gold or silver, the first step is a conversation—not a commitment.

Brighton Gold offers a complimentary consultation to walk you through your options, including our No Fee Precious Metals IRA that covers custodial fees for the lifetime of the account on qualified purchases.

We’ll show you exactly:

- How the No Fee IRA works and whether you qualify

- The difference between U.S.-minted coins and foreign alternatives

- What to expect from the rollover and purchasing process

- How to transfer funds from your existing 401(k) or IRA

- What ongoing support looks like after your purchase

Learn About the No Fee IRA — no obligation, just actionable insights you can use whether you work with us or not.

Your retirement savings represent decades of work. Understanding your options helps you move forward with clarity and confidence.