Why Do Some Financial Advisors Discourage Gold IRAs? (The Real Reasons)

If you’ve ever brought up physical gold to a financial advisor — and been met with a frown, a dismissive comment, or a quick redirect to “something better” — you’re not alone. It’s one of the most common frustrations we hear from customers.

Here’s the short version: most financial advisors discourage Gold IRAs for three structural reasons — not because gold is a bad decision. Those reasons are compensation, custody, and training. The typical advisor earns fees based on the assets they manage. Physical gold sits outside their system. Their brokerage can’t hold it. And their education didn’t cover it.

That doesn’t make them dishonest. It makes them limited — by the tools they have and the system they work within.

The fact is, establishing a precious metals IRA is fully legal under Internal Revenue Code Section 408(m). Congress specifically carved out an exception for high-purity gold, silver, platinum, and palladium in retirement accounts. And with gold trading near $5,000 per ounce, the U.S. national debt surpassing $38.4 trillion, and central banks on a historic buying spree — understanding why your advisor might push back is more important than ever.

This article breaks down each of those three reasons in plain language. It’s not about blaming anyone. It’s about giving you the clarity to make your own informed decision — whether that means adding physical gold, staying the course, or doing both.

The difference between tangible ownership vs. digital exposure matters more today than it has in decades. Let’s walk through why.

The Compensation Gap — How Financial Professionals Get Paid

This is the reason most people never hear about — and it’s the most important one to understand. The way financial professionals get paid creates a natural blind spot when it comes to physical precious metals.

It’s not necessarily intentional. But when your entire business model is built around managing certain types of products, anything that falls outside that model becomes invisible — or inconvenient.

The AUM Fee Model and Physical Gold

The most common compensation structure in financial planning today is called Assets Under Management (AUM). Here’s how it works: your advisor charges a percentage — usually around 1% — of the total value they manage for you each year.

So if your advisor manages $500,000, they’re earning roughly $5,000 per year in fees. If that number grows to $750,000, their fee grows too. According to CNBC, approximately 72% of advisors received an AUM-based fee in 2024, with that number expected to climb to around 78% by 2026.

Here’s where physical gold creates a problem for that model.

When you move $50,000 into a self-directed Gold IRA, that $50,000 leaves your advisor’s managed accounts. It goes to a separate custodian. The advisor can no longer charge their AUM fee on that money. At 1%, that’s $500 per year in lost revenue — per customer.

Multiply that across dozens or hundreds of customers, and you start to see why there’s no incentive to bring up physical gold in the first place.

Commission-Based Products vs. Physical Metal

Advisors who work on a commission basis face a similar gap. They earn money when they sell financial products — mutual funds, annuities, insurance policies. These products come with built-in fees, loads, and trailing commissions.

Physical gold and silver? None of that applies. A gold coin doesn’t pay a trailing commission. A bar of silver doesn’t have a 12b-1 fee. When a customer buys physical metal through a precious metals dealer, the financial advisor earns nothing on that transaction.

This doesn’t mean every advisor who steers you away from gold is acting out of self-interest. Many genuinely believe the products they recommend are the best option. But the structure they operate within means physical gold never even enters the conversation — because it doesn’t fit the revenue model.

| Fee Model | How Advisor Earns | Works With Physical Gold? | Impact on Gold IRA Recommendation |

|---|---|---|---|

| AUM (% of managed assets) | Annual percentage of total managed value | No — gold leaves managed accounts | Strong disincentive to recommend |

| Commission-based | Upfront or trailing fees on product sales | No — no commissions on physical metal | No financial reason to suggest it |

| Fee-only (flat/hourly) | Fixed fee regardless of products chosen | Yes — fee isn’t tied to specific products | Most likely to give unbiased guidance |

| Hybrid (fee + commission) | Combination of AUM and product commissions | Partially — fee portion unaffected | Mixed incentives depending on structure |

The takeaway here isn’t that advisors are bad people. It’s that the system they work in has a built-in blind spot. And if you don’t know about that blind spot, you can’t evaluate their advice with full context.

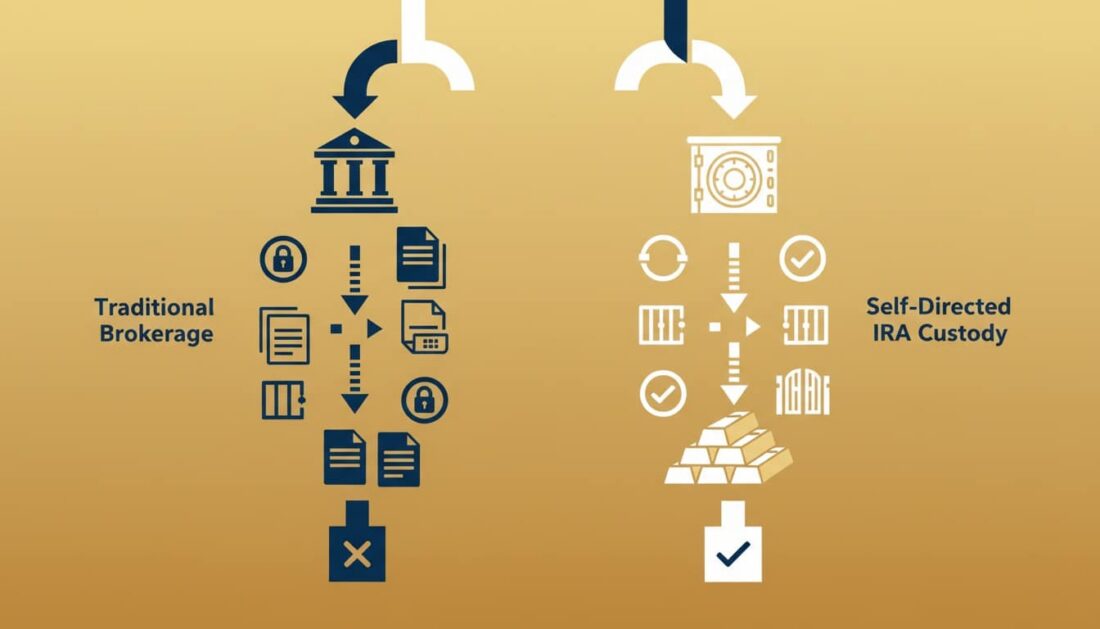

The Custody Problem — Why Brokerages Can’t Hold Physical Gold

Even if your financial advisor wanted to help you acquire physical gold inside a retirement account, their brokerage probably can’t do it. This isn’t a matter of willingness — it’s a structural limitation built into the regulatory framework.

Understanding this “custody gap” is essential to evaluating any advice you receive about precious metals.

What the SEC Custody Rule Actually Says

The SEC’s Custody Rule (Rule 206(4)-2) requires that registered financial advisors maintain assets with “qualified custodians” — typically banks, broker-dealers, or trust companies.

Here’s the catch: the current rule applies to “funds and securities.” Physical gold isn’t a security. It’s a tangible asset. And most qualified custodians at major brokerages — Fidelity, Schwab, Vanguard, Merrill Lynch — are set up to hold digital records of paper-based products. They don’t have vaults. They don’t have depository relationships. They aren’t equipped to take physical possession of a gold coin.

The SEC even proposed expanding its custody framework in February 2023 to cover physical assets like precious metals, real estate, and commodities — acknowledging that the existing rules weren’t designed for these types of holdings. But even that proposal recognized that physical assets often “cannot be recorded and maintained in a manner in which a qualified custodian can maintain possession.”

In plain language? The regulatory system wasn’t built for gold. And your advisor is operating inside that system.

Self-Directed IRAs: The Bridge Between Systems

This is where self-directed IRAs come in. A self-directed IRA uses a specialized trust company — one that’s been approved to hold physical assets — as your custodian. The gold itself is stored in an IRS-approved depository, not at your house and not in your advisor’s office.

It’s a parallel structure. Your traditional retirement accounts stay with your current advisor. Your physical gold sits with a self-directed custodian. Both are legal, both are tax-advantaged, and both serve different purposes.

The FINRA, SEC, and NASAA joint alert on self-directed IRAs does warn about fraud risks in the self-directed space — and those warnings are legitimate. Scam promoters have used self-directed IRAs to lure people into fraudulent schemes. But the alert also makes clear that self-directed IRAs themselves are not the problem. The problem is unscrupulous operators.

That’s why identifying safe gold IRA practices matters so much. Working with a reputable dealer, a licensed custodian, and an approved depository eliminates the risks that regulators are rightly concerned about.

| Traditional Brokerage IRA | Self-Directed Gold IRA |

|---|---|

| Custodian holds paper-based products | Custodian holds physical precious metals |

| Advisor manages and earns AUM fees | Advisor has no role in the Gold IRA |

| Limited to what the brokerage offers | Broader range of IRS-approved assets |

| Easy to rebalance digitally | Requires physical purchase and depository storage |

| Subject to market performance of paper products | Subject to spot price of physical gold and silver |

The point isn’t that one system is better than the other. It’s that they exist in separate worlds — and most advisors only have access to one of them.

The Training Gap — Modern Portfolio Theory and What Gets Left Out

Beyond compensation and custody, there’s a third factor that shapes how financial advisors view gold — and it starts long before they meet their first customer.

Most financial professionals are trained in what’s called Modern Portfolio Theory (MPT). It’s the foundation of virtually every financial planning certification in the United States. And while it’s a solid framework for constructing balanced, risk-adjusted strategies, it has a significant blind spot when it comes to physical gold.

What Financial Professionals Learn (and Don’t Learn)

Modern Portfolio Theory — developed in the 1950s by economist Harry Markowitz — emphasizes building a mix of paper-based products that work together to manage risk. The entire framework is built around things like expected returns, standard deviations, correlation coefficients, and dividend yields.

Physical gold doesn’t fit neatly into this model. It doesn’t produce earnings. It doesn’t pay a quarterly dividend. And its value isn’t derived from a company’s balance sheet.

So when advisors study for their Series 7, Series 66, or CFP certification, physical precious metals rarely come up. The curriculum focuses on securities, money markets, mutual funds, ETFs, and insurance products — all things that produce income, can be managed digitally, and fit within the AUM compensation structure.

That’s not a conspiracy. It’s just how the education pipeline works. If the tools you’re trained on don’t include physical gold, you’re unlikely to recommend it — even if it might genuinely help your customer.

The “Gold Doesn’t Pay Dividends” Argument

This is probably the most common pushback you’ll hear: “Gold is a dead asset. It just sits there. It doesn’t earn anything.”

It’s technically true that gold doesn’t produce income. But that argument misunderstands what gold is designed to do.

Gold isn’t meant to compete with dividend-paying products. It’s meant to protect purchasing power — especially during periods of inflation, currency devaluation, and economic instability.

And the data supports that purpose. According to World Gold Council research, gold has outpaced both U.S. consumer prices and Treasury bill rates since 1971. In years when inflation ran between 2% and 5%, gold’s price increased an average of 8% per year. During periods of higher inflation, those numbers went even higher.

The intrinsic value of precious metals isn’t measured in quarterly earnings reports. It’s measured in what your dollar buys today versus what it bought ten years ago — and whether you’ll still have access to your wealth when the system gets rocky.

When someone says “gold doesn’t pay dividends,” the real question to ask is: “What’s the dividend on peace of mind?”

What the Law Actually Says About Gold in Retirement Accounts

One of the most powerful responses to advisor resistance is simple: the law is on your side. Physical gold in retirement accounts isn’t a loophole, a workaround, or a gray area. It’s specifically authorized by the Internal Revenue Code.

IRC Section 408(m) — The Exception That Makes Gold IRAs Legal

The IRS treats most tangible personal property as “collectibles” — and collectibles are generally prohibited from being held in IRAs. That includes art, antiques, stamps, and most coins.

But Section 408(m)(3) carves out a specific exception for certain precious metals that meet strict purity standards. The Taxpayer Relief Act of 1997 expanded these provisions, making it clear that Congress intended for Americans to have access to physical gold and silver inside their retirement accounts.

This isn’t obscure tax trivia. It’s settled law that’s been in place for nearly three decades. If your advisor tells you “you can’t put gold in an IRA,” that’s simply not accurate.

Purity Standards and IRA-Approved Products

Not all gold qualifies. The IRS requires specific fineness standards:

- Gold — Must be at least 99.5% pure (0.995 fineness)

- Silver — Must be at least 99.9% pure (0.999 fineness)

- Platinum — Must be at least 99.95% pure (0.9995 fineness)

- Palladium — Must be at least 99.95% pure (0.9995 fineness)

The one notable exception? The American Gold Eagle. Despite not meeting the standard 99.5% purity threshold (it’s 91.67% gold by weight), Congress specifically exempted it by name. That’s how intentional this legislation was — they even addressed individual coin types.

When it comes to acquiring U.S.-minted gold coins for a retirement account, the American Gold Eagle remains the most popular choice precisely because of this explicit congressional approval.

| Metal | Minimum Purity | Popular IRA-Approved Products | Congressional Authority |

|---|---|---|---|

| Gold | 99.5% (exception: American Gold Eagle) | American Gold Eagle, Canadian Maple Leaf, Gold Buffalo | IRC 408(m)(3)(A) and (B) |

| Silver | 99.9% | American Silver Eagle, Canadian Silver Maple Leaf | IRC 408(m)(3)(B) |

| Platinum | 99.95% | American Platinum Eagle, Canadian Platinum Maple Leaf | IRC 408(m)(3)(B) |

| Palladium | 99.95% | Canadian Palladium Maple Leaf | IRC 408(m)(3)(B) |

Understanding these standards is part of evaluating risks of precious metals ownership — and it’s exactly the kind of detail a traditional advisor may not know, simply because it falls outside their training and their system.

Evaluating Your Current Guidance — A 3-Step Framework

Now that you understand the three structural reasons behind advisor resistance — compensation, custody, and training — you can evaluate the advice you’re receiving with clearer eyes.

This isn’t about confrontation. It’s about asking the right questions so you can make your own decision with confidence.

Step 1 — Identify the Custody Gap

Ask your financial advisor a straightforward question: “Can your firm hold physical gold or silver in my retirement account?”

If the answer is no — and for most major brokerages, it will be — that tells you something important. It doesn’t mean the advisor is wrong about everything else. But it does mean their recommendations are limited to what their system can accommodate.

Understanding gold IRA fee structures on the self-directed side will help you compare apples to apples. Self-directed IRA custodians charge annual account fees, storage fees, and sometimes transaction fees. These are real costs, and they’re worth understanding before you move forward.

Step 2 — Review the Fee Structure

Ask: “How are you compensated, and does that change if I move a portion of my retirement into a self-directed IRA?”

If your advisor charges AUM fees, any money that moves out of their management reduces their income. That’s not accusatory — it’s just math. Understanding this dynamic helps you weigh their advice more objectively.

A fee-only advisor who charges a flat rate regardless of where your money sits is more likely to give you unbiased guidance on physical gold. If that’s not your current setup, it’s still valuable to get a second opinion from someone without a direct financial stake in the answer.

Step 3 — Analyze the Protection Strategy

Ask: “What’s your plan for protecting my purchasing power if the dollar continues to lose value?”

This is the question that gets to the heart of why people consider gold in the first place. With the U.S. national debt exceeding $38.4 trillion and the CBO projecting $1.9 trillion annual deficits, the question of dollar stability isn’t theoretical anymore.

If your advisor’s only answer involves paper-based products denominated in dollars, that’s a single-system approach. Adding physical precious metals — held outside the banking system, in a tangible form you actually own — introduces a fundamentally different layer of protection.

That’s not fear-based thinking. That’s common sense.

| Evaluation Step | Key Question | What the Answer Reveals |

|---|---|---|

| 1. Identify the Custody Gap | “Can your firm hold physical gold in my IRA?” | Whether their system can even support what you’re asking |

| 2. Review the Fee Structure | “How does my decision to add gold affect your compensation?” | Whether a financial incentive is influencing the recommendation |

| 3. Analyze the Protection Strategy | “What’s your plan for dollar devaluation?” | Whether your current strategy accounts for currency risk |

Frequently Asked Questions

Do financial advisors make money on Gold IRAs?

Most traditional financial advisors do not earn ongoing fees or commissions on physical gold held in a self-directed IRA. Because physical precious metals sit outside the advisor’s managed accounts, they can’t charge their standard AUM percentage — which typically runs around 1% annually. This creates a structural gap in compensation that doesn’t exist with paper-based products.

That gap doesn’t mean advisors are acting in bad faith. But it does mean that their recommendations naturally gravitate toward the products they can manage and earn from. Understanding this is the first step toward evaluating the advice you receive about gold with full transparency.

Is it true that gold is a “dead asset” because it pays no interest?

Gold doesn’t produce dividends or interest — that’s accurate. But calling it a “dead asset” misses the purpose entirely.

Gold functions as wealth protection, not income generation. According to the World Gold Council, gold has averaged approximately 8% in annual returns since 1971, outpacing both U.S. inflation and Treasury bill rates over the same period.

The “no yield” argument compares gold to income-producing instruments without accounting for gold’s primary role: preserving purchasing power during periods of currency devaluation and economic uncertainty. Precious metals may appreciate, depreciate, or remain unchanged depending on market conditions.

Can my current Merrill Lynch or Fidelity advisor manage my Gold IRA?

No. Major brokerages like Merrill Lynch, Fidelity, Charles Schwab, and Vanguard are not structured to hold physical precious metals. The SEC’s Custody Rule requires that advisors maintain assets with “qualified custodians,” and most traditional custodians only handle funds, securities, and paper-based products.

A Gold IRA requires a self-directed IRA custodian — a specialized trust company approved to hold physical assets in IRS-compliant depositories. This is a separate account from your traditional brokerage IRA, and it operates under the same tax-advantaged rules.

Why do advisors recommend Gold ETFs instead of physical gold?

Gold ETFs stay within the advisor’s managed accounts. That means they can charge their standard AUM fee, monitor the position digitally, and rebalance without any logistical complexity. Physical gold, by contrast, requires a self-directed custodian, an approved depository, and sits outside the advisor’s fee structure entirely.

For many advisors, recommending an ETF keeps the relationship — and the revenue — intact. That doesn’t mean ETFs are bad. But understanding the difference between tangible ownership and digital exposure helps you make a more informed decision about which approach fits your goals.

An ETF is a paper claim on gold held by a financial institution. Physical gold in a self-directed IRA is metal you own, stored in a vault with your name on it. Those are fundamentally different things.

What percentage of my retirement should be in physical gold?

There’s no universal answer — it depends on your situation, your goals, and your comfort level. Many precious metals specialists suggest that somewhere between 5% and 20% of retirement holdings in physical gold or silver can provide meaningful protection without over-concentrating in a single area.

Precious metals may appreciate, depreciate, or remain unchanged depending on market conditions. Consult your CPA or tax professional for guidance specific to your situation.

Brighton does not provide financial, legal, or tax advice. A complimentary consultation can help you evaluate what makes sense based on your unique circumstances.

Is a Gold IRA legal?

Yes — completely. Internal Revenue Code Section 408(m)(3) specifically permits certain precious metals in IRAs, including gold bullion meeting 99.5% purity standards, American Gold Eagles, and other IRS-approved coins. The Taxpayer Relief Act of 1997 expanded these provisions further.

A Gold IRA is fully legal, tax-advantaged, and subject to the same contribution limits and distribution rules as any traditional or Roth IRA.

How do I move money into a Gold IRA without upsetting my current advisor?

You don’t have to move everything. Many customers start with a partial rollover — transferring a portion of an existing IRA or 401(k) into a self-directed Gold IRA while keeping the rest with their current advisor.

A direct rollover (trustee-to-trustee transfer) avoids penalties and taxes entirely. You can frame the conversation simply: “I’d like to move a portion of my retirement into physical metals for protection. This doesn’t change our relationship — it adds another layer.”

Most advisors will understand, even if they don’t actively support it.

The Bigger Picture

Understanding why some financial advisors discourage Gold IRAs isn’t about finding villains. It’s about recognizing the system — and making sure the system is working for you, not the other way around.

Your advisor may be a smart, well-intentioned professional. They may genuinely believe that the products they recommend are the best available. But if their system can’t hold physical gold, their fees don’t apply to physical gold, and their training didn’t cover physical gold — you’re getting advice from an incomplete perspective.

The solution isn’t to fire your advisor. It’s to broaden your perspective. Add a precious metals specialist to the conversation. Ask the hard questions. And make sure the person guiding your retirement has the full picture — not just the part their system can profit from.

With the national debt growing by $8 billion per day, central banks buying gold at record levels, and the dollar’s purchasing power under constant pressure — the case for holding something tangible, something outside the paper system, has never been stronger.

That’s not an opinion. That’s what the data says.

Ready to See What a Gold IRA Looks Like for Your Situation?

If you’ve been thinking “this all makes sense, but I don’t have time to figure it out on my own,” you’re not alone. Most customers we work with felt the same way before they realized how straightforward the process can be with the right guidance.

That’s why we offer a complimentary consultation to walk you through your options — including our No Fee Precious Metals IRA, which covers custodial fees for the lifetime of the account on qualified purchases.

We’ll show you exactly:

- How the No Fee IRA works and whether you qualify

- The difference between U.S.-minted coins and foreign alternatives

- What to expect from the purchasing and delivery process

- How to roll over or transfer existing retirement funds

- What ongoing support looks like after your purchase

Learn About the No Fee IRA — no obligation, just actionable insights you can use whether you work with us or not.

Your advisor gives you one perspective. We’ll give you the rest. Because when it comes to your retirement, you deserve the full picture — not just the parts that fit inside someone else’s fee structure.