Gold IRA Scams: Red Flags and How to Protect Yourself (2026)

Here’s a surprise most people don’t realize until it’s too late — the biggest threat to your Gold IRA isn’t the market. It’s the dealer.

In 2026, predatory companies are charging 50% to over 100% in hidden markups on coins they label as “exclusive.” They’re promising you can legally store IRA metals at home — you can’t. They’re dangling “free silver” bonuses that are quietly baked into inflated prices. And they’re using fear-based sales tactics to pressure retirees into rushing decisions that affect decades of savings.

The good news? These scams follow the same playbook every time. Once you know the patterns, they’re easy to spot.

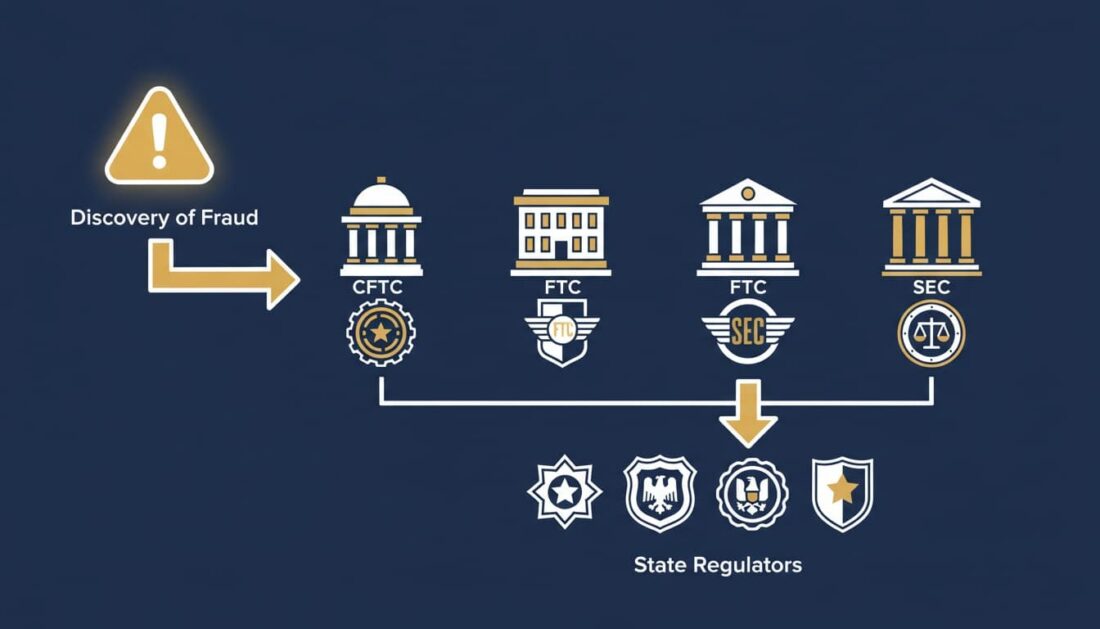

Federal agencies like the CFTC and SEC have been aggressively going after these companies. The enforcement cases they’ve brought — totaling hundreds of millions in penalties — tell you exactly what to watch for.

So what does a safe, compliant Gold IRA actually look like? And how do you tell the difference between a company that’s earning your trust and one that’s earning a commission?

That’s what this article covers. If you’ve been exploring the idea of identifying safe gold IRA practices — or you’re already comparing costs and wondering what’s fair — read this before you sign anything. Understanding gold IRA fee structures is one of the most important steps you can take to protect yourself.

The 5 Most Dangerous Gold IRA Scams Right Now

Not every scam looks the same. Some are loud — a cold call promising you’ll double your money. Others are quiet — a slightly inflated price you’d never catch unless you checked the spot rate yourself.

But the most damaging ones? They follow the same five patterns. And regulators have documented every one of them.

Here’s what we’re seeing today — and what you should know about each.

1. The “Home Storage” Myth

This one’s been around for years. And it’s still tripping people up.

Some companies advertise that you can keep your Gold IRA metals at home — usually through an LLC that you manage yourself. They make it sound simple and perfectly legal.

It’s not.

The IRS is clear — all precious metals in an IRA must be held by an approved custodian or depository. Not in your safe. Not in a bank box you control. An approved, third-party facility.

The 2021 McNulty Tax Court ruling removed any doubt. A couple stored about $411,000 in American Eagle coins — purchased through an IRA-owned LLC — in a safe at their home. The court ruled that taking physical possession counted as a taxable distribution of their entire IRA.

They ended up owing over $300,000 in back taxes and penalties.

The court even called the LLC vendor’s marketing a “questionable internet scheme.”

So if a dealer tells you home storage is legal — that’s not a gray area. That’s your signal to walk away.

2. Hidden and Excessive Markups

This is the scam that quietly drains the most money — and it’s almost invisible if you don’t know the baseline.

Here’s what “normal” looks like. Standard bullion coins — American Gold Eagles, Canadian Maple Leafs — typically carry dealer markups between 3% and 8% over the live spot price. That’s the standard cost of doing business.

Now here’s what “not normal” looks like.

In 2023, the SEC charged Red Rock Secured for telling customers their markups were 1% to 5%. The real number? As high as 130%. More than 700 people lost a combined $50 million.

And in late 2025, a federal court ordered Safeguard Metals to pay over $51 million after defrauding more than 450 customers — many of them retirement-aged — by selling silver coins at massively inflated, undisclosed markups.

How do you protect yourself? It’s straightforward. Before you purchase anything, look up the current spot price for that coin. Then ask the dealer — in writing — what their markup is. If the numbers don’t line up, or if they won’t answer, you’ve got your answer.

3. The “Exclusive” Coin Trap

This one’s sneaky — and it costs purchasers dearly.

Here’s how it plays out. A salesperson steers you away from standard bullion and toward “exclusive,” “limited edition,” or “semi-numismatic” coins. They’ll tell you these products are more valuable, more liquid, or better suited for your IRA.

That’s rarely true.

These coins often carry markups of 40% to 200% above their actual metal value. They’re harder to resell. And when you do try to sell, the dealer typically offers only the spot price — meaning you’ll never recover that premium.

What qualifies for an IRA? The IRS says gold must be at least 99.5% pure — with an exception for American Gold Eagles. Stick with widely recognized, IRS-approved bullion from government mints. American Eagles, Buffaloes, Maple Leafs. They’re liquid, fairly priced, and accepted everywhere.

If someone’s pushing anything described as “exclusive” for your retirement account — ask yourself who’s really benefiting from that recommendation.

4. High-Pressure Sales and Scare Tactics

“You need to move your money today.”

“This deal expires at midnight.”

“If you don’t act now, you could lose everything.”

Sound familiar? These aren’t market insights. They’re sales scripts.

The CFTC has warned about this repeatedly. Predatory companies use fear — about the dollar, about the economy, about government action — to push retirees into snap decisions. And the people making those calls aren’t licensed financial professionals. They’re salespeople, paid on commission.

A company that genuinely has your interests in mind won’t need to manufacture panic. They’ll give you time to think. They’ll encourage you to compare. They’ll answer your questions without rushing you.

That’s the difference between a company that earns your trust — and one that pressures you into giving it.

5. Misleading Buyback “Guarantees”

“We’ll buy it back anytime — guaranteed.”

Sounds reassuring, doesn’t it? But what does that actually mean?

In most cases, these “guarantees” have no specific price commitment, no binding terms, and plenty of fine print. The dealer isn’t promising to pay you fair market value. They’re not even promising the company will still be open when you’re ready to sell.

Some companies that heavily promoted buyback guarantees have simply shut their doors — leaving customers with no recourse and no one to call.

A buyback program can be a good sign. But only if it’s documented, transparent, and specific. Ask for the full terms in writing. What percentage of spot will they offer? Are there conditions? What happens if the company closes?

If they can’t answer those questions, that “guarantee” isn’t worth much.

| Scam Type | How It Works | How to Protect Yourself |

|---|---|---|

| Home Storage IRA | Dealer claims you can legally store IRA metals at home via LLC | IRS requires approved custodian storage; McNulty ruling confirmed this |

| Hidden Markups | Dealer quotes low markup but charges 50-130%+ above spot | Check live spot price; demand written fee disclosure before purchasing |

| “Exclusive” Coin Trap | Salesperson pushes high-premium coins with inflated markups | Stick with standard, IRS-approved bullion from recognized government mints |

| High-Pressure Sales | Fear-based urgency tactics to force immediate decisions | Legitimate dealers give you time; no real deal requires a same-day commitment |

| Fake Buyback Guarantees | Promises to repurchase metals with no binding commitment | Get buyback terms in writing; verify specific pricing and conditions |

Why This Matters More Than Ever in 2026

Here’s what we’re seeing today — and why the risks are higher than they’ve been in years.

Record Gold Prices Are Creating Urgency

When gold prices climb — as they have recently — people who’ve been thinking about precious metals start to feel like the window’s closing. That urgency is natural.

But it’s also exactly what predatory dealers exploit.

They position themselves as the shortcut. They say, “Prices are only going up — act now.” And because the market does feel urgent, people let their guard down.

The reality? Record prices don’t mean you need to rush. They mean you need to be more careful about who you work with and what you pay. A transparent dealer won’t create false pressure — they’ll give you the clarity and space to make a confident decision on your own timeline.

AI Deepfakes and Fake Celebrity Endorsements

This is a newer threat — and it’s growing fast.

Scam companies are now using AI-generated videos and fabricated celebrity endorsements to make themselves look credible. A familiar face in a commercial doesn’t mean that person actually endorsed the company. And even when the endorsement is real, it just means someone got paid to appear in an ad.

It says nothing about the company’s pricing, compliance record, or how they’ll treat you after the sale.

How do you cut through it? Focus on the things that actually matter — their track record, their pricing transparency, and their complaint history. Not their commercials.

Regulators Are Sounding the Alarm

Federal enforcement in the precious metals space has ramped up significantly. In late 2025 alone, the CFTC — working alongside 30 state regulators — secured the $51 million judgment against Safeguard Metals for defrauding over 450 retirement-aged customers.

Another ongoing case — against TMTE Inc., operating as Metals.com — alleges $185 million in fraud targeting elderly purchasers with markups of 100% to 300%.

These aren’t one-off situations. They’re part of a pattern that federal agencies are actively working to stop.

What does that mean for you? It means the scams are real. The consequences for bad actors are real. And your due diligence is the most important protection you have.

How to Spot a Bad Actor Before They Touch Your Savings

Knowing the scams is helpful. But knowing how to identify a bad actor before they get anywhere near your savings — that’s what actually keeps you safe.

The warning signs are consistent. And the questions that expose them aren’t complicated.

Red Flags Worth Memorizing

You don’t need a law degree for this. You just need to know what to listen for.

- Unsolicited contact — A company calls, emails, or mails you out of the blue with a Gold IRA pitch? That’s one of the CFTC’s most commonly cited warning signs. Proceed with extreme caution.

- Pressure to decide today — “This window is closing” or “We only have a few spots left” — these are sales scripts, not market realities. Gold doesn’t run out of stock.

- No written fee schedule — If a dealer can’t put their full fee breakdown on paper — markups, storage fees, custodial fees, transaction fees — that should end the conversation.

- Pushing “rare” or “collectible” coins for your IRA — IRA-approved coins are standard bullion products from recognized mints. If someone’s steering you toward “exclusive” or “proof” coins, they’re almost certainly earning a bigger commission.

- Promises of growth or protection — Precious metals may appreciate, depreciate, or remain unchanged. Anyone promising otherwise either doesn’t understand what they’re selling — or they’re counting on you not understanding it.

- “Free” silver or gold bonuses — Nothing in precious metals is free. Those costs are hidden somewhere else in the transaction.

Five Questions That Separate Good Dealers from Bad Ones

Before you commit to anything, ask these five questions. A company that deserves your business will answer every one of them — clearly and in writing.

- What’s your exact markup over the current spot price for this specific coin?

- Can you give me a complete, written fee schedule — storage, custodial fees, transaction fees — all of it?

- What’s your buyback policy? Can I see the terms in writing?

- Which IRS-approved depository will hold my metals — and how do I verify that on my own?

- Are your salespeople licensed to offer financial guidance, or are they paid on commission?

If you get vague answers, pushback, or deflection on any of these — that tells you everything you need to know about how that company operates.

| Legitimate Dealer | Fraudulent Dealer |

|---|---|

| Provides written fee schedule before purchase | Avoids discussing fees or gives verbal-only estimates |

| Recommends standard IRS-approved bullion | Pushes “exclusive” or high-premium coins |

| Gives you time to compare and decide | Creates urgency with fear-based tactics |

| Transparent about markups over spot price | Hides markups or quotes misleading percentages |

| Works with recognized IRS-approved depositories | Promotes home storage or vague storage arrangements |

| Encourages you to consult your CPA or tax professional | Dismisses the need for outside guidance |

| Has a verifiable BBB record and complaint history | Has no track record or multiple unresolved complaints |

How to Verify a Gold IRA Company Before You Sign Anything

Trust shouldn’t be assumed. It should be earned — and verified.

The tools to do it are free, publicly available, and take about five minutes. Here’s a simple three-step process you can run through before transferring a single dollar.

Step 1: Check Their Complaint and Regulatory History

Start with the Better Business Bureau.

Look up the company. Read the complaints — not just the rating. Pay attention to patterns. One or two complaints can happen to any business. But a string of unresolved disputes about pricing, delivery, or high-pressure tactics? That’s a pattern.

Then check your state’s securities regulator. The North American Securities Administrators Association keeps a directory of state regulators who can tell you if a company is registered — and whether any enforcement actions have been filed.

If you’re evaluating risks of precious metals ownership, this step is non-negotiable. Five minutes of homework can save you thousands.

Step 2: Demand a Written Buy/Sell Spread

The buy/sell spread is the gap between what you pay for a coin and what the dealer will pay you when you sell it back.

This one number tells you more about a dealer’s integrity than anything else on their website.

Ask for it in writing. Then compare it to the current spot price. A spread of 3% to 8% on standard bullion is reasonable. Anything north of 15% on widely traded coins like American Eagles or Maple Leafs? That deserves a hard look — and probably a second opinion.

And if the dealer says “it depends” without giving you specifics — that’s not transparency. That’s evasion.

Step 3: Cross-Reference Coin Prices with Live Spot Rates

Before you buy anything, check the live spot price. It’s the current market value per troy ounce — and it’s publicly available from dozens of sources.

Then do the math.

If gold’s trading at $2,800 an ounce and a dealer’s quoting $4,200 for a one-ounce coin — that’s a 50% markup. Far outside the standard range.

Tools like FMVgold.com can help you track fair market values and see whether a dealer’s pricing is in line with the broader market.

This step takes two minutes. And it’s the single most effective way to catch an inflated price before it costs you.

| Verification Step | What to Check | Where to Check |

|---|---|---|

| Complaint and regulatory history | BBB rating, unresolved disputes, state enforcement actions | BBB.org, state securities regulator, NASAA |

| Buy/sell spread | Written disclosure of markup and buyback pricing | Request directly from the dealer — in writing |

| Live spot price comparison | Dealer price vs. current market value per troy ounce | FMVgold.com, Kitco, APMEX, or any live metals tracker |

]

What a Legitimate Gold IRA Actually Looks Like

It’s easy to focus on what’s wrong. But knowing what the process should look like — when it’s done right — gives you something to compare against.

And the truth is, a legitimate Gold IRA is surprisingly straightforward.

The Process, Step by Step

- Choose a reputable dealer — One with transparent pricing, a verifiable BBB history, and a clear fee schedule. They should work with recognized, IRS-approved custodians and depositories.

- Open a self-directed IRA — Your dealer coordinates with an approved custodian to set up the account. Most customers complete this in a few business days. Wondering about timelines? Here’s a closer look at executing a precious metals IRA rollover.

- Fund the account — Through a direct rollover, transfer, or new contribution. A direct rollover moves funds straight from one retirement account to another — the money never touches your hands. That’s the cleanest approach.

- Purchase IRS-approved metals — Standard bullion coins and bars that meet IRS purity requirements. Gold must be at least 99.5% pure (with the American Gold Eagle exception). Your dealer should explain exactly what you’re buying, what it costs, and why.

- Metals ship to an approved depository — Stored in your name, in a segregated or non-segregated account, at a facility that’s insured and regularly audited.

That’s it. No home storage. No secret LLCs. No “exclusive” coins with hidden premiums. Just a clean, compliant transaction — with support at every stage of ownership.

What Ongoing Support Should Look Like

The purchase shouldn’t be the end of the relationship. It should be the beginning.

A quality dealer provides regular account statements. Access to market updates and educational resources. Responsive customer service when you have questions. And a clear, documented process for when you’re ready to sell or take a distribution.

If a dealer goes quiet after the sale, that’s a sign they were more interested in the commission than in you.

Some financial professionals even question Gold IRAs entirely — and honestly, it’s often because they’ve seen what happens when companies disappear after the transaction. The answer isn’t to avoid Gold IRAs. It’s to work with a dealer who stays present — before, during, and long after the purchase.

That’s what concierge service actually means.

What to Do If You’ve Already Been Scammed

Maybe you’ve already made a purchase and something doesn’t feel right. Or maybe you’re just now doing the math and the numbers aren’t adding up.

Either way — there are concrete steps you can take.

Report It to Federal and State Agencies

You’ve got several options — and using more than one increases the chances of action.

- CFTC — File at cftc.gov/complaint or call 866-366-2382. The CFTC’s whistleblower program offers rewards of 10% to 30% of sanctions collected in successful cases.

- FTC — Report fraud at reportfraud.ftc.gov. The FTC uses complaint patterns to build enforcement cases.

- SEC — If your situation involved retirement account misrepresentation, file at sec.gov/tcr.

- State regulators — Contact your state’s securities commissioner or attorney general. The Safeguard Metals case involved 30 states working together — state-level complaints carry real weight.

Pull Together Your Documentation

Gather everything you have — transaction agreements, fee disclosures, marketing materials, emails, and recorded calls if you’ve got them.

If you never received a written fee schedule — or if what you were told verbally doesn’t match the paperwork — that’s worth noting in your complaint. These details become evidence.

Talk to a Professional

If you’ve taken a significant loss, it’s worth speaking with a securities attorney or your CPA. They can help you understand your options — and the tax implications of unwinding a bad transaction.

Precious metals may appreciate, depreciate, or remain unchanged. That’s normal market reality. But if your losses came from undisclosed markups, misrepresentation, or outright fraud — that’s not a market issue. That’s a regulatory one. And there are agencies built to address it.

Frequently Asked Questions

Can I store my Gold IRA gold at home legally?

No. And this one isn’t a gray area.

The IRS requires all Gold IRA metals to be held by an approved custodian or depository. Not in your home. Not through an LLC you manage yourself.

The 2021 McNulty Tax Court ruling settled this definitively. A couple stored American Eagle coins — purchased through an IRA-owned LLC — in a personal safe. The court ruled that taking possession counted as a taxable distribution. They owed over $300,000 in taxes and penalties.

The court called the home storage marketing a “questionable internet scheme.” Any company saying otherwise is either uninformed or deliberately misleading you.

What’s a normal markup for Gold IRA coins?

For standard bullion — American Gold Eagles, Canadian Maple Leafs, American Buffaloes — you’ll typically see markups between 3% and 8% over the spot price.

That’s the normal range.

If a dealer’s quoting 20%, 50%, or anything above 15% on widely traded bullion, that’s well above market norms. Always check the live spot price yourself and calculate the markup before committing.

For a more detailed breakdown of what you should expect to pay, Brighton’s guide to understanding gold IRA fee structures covers it in detail.

Are “exclusive” or “limited edition” coins better for IRAs?

No. They’re almost always worse.

“Exclusive” coins often carry markups of 40% to 200% — and when you go to sell, the dealer typically only offers the spot price. That gap? That’s money you’ll never recover.

Stick with widely recognized, IRS-approved bullion from government mints. They’re liquid, fairly priced, and universally accepted.

If a salesperson is pushing you toward anything called “exclusive” or “limited edition” — ask yourself who that really benefits.

How do I report a Gold IRA scam to the government?

You’ve got several options — and you can use more than one.

CFTC: cftc.gov/complaint or call 866-366-2382. Whistleblowers can earn 10-30% of sanctions.

FTC: reportfraud.ftc.gov

SEC: sec.gov/tcr

State regulators: Contact your state’s securities commissioner or attorney general.

NASAA: The North American Securities Administrators Association can connect you with your local regulator.

Filing a complaint helps regulators spot patterns — and build the cases that protect everyone.

Why do some gold companies offer “free silver” bonuses?

Because the cost is baked into the markup on your primary purchase.

If a company’s offering $10,000 in “free” silver, that $10,000 is almost certainly recovered through inflated prices on the gold you’re buying. It’s a marketing tactic — not generosity.

A transparent dealer lets their pricing speak for itself. They don’t need gimmicks to earn your business.

What should I look for in a legitimate Gold IRA company?

Start with the basics. A verifiable Better Business Bureau record. Transparent, written fee schedules. IRS-approved storage with recognized depositories.

Beyond that — look for a company that gives you time. That encourages you to consult your CPA or tax professional. That doesn’t rely on fear to close a sale.

The best dealers earn your trust through clarity and patience — not pressure. If you’re still getting familiar with the terminology used in this industry, Brighton’s glossary is a good place to start.

What is a dealer buyback guarantee — and can you trust it?

A buyback guarantee means the dealer promises to repurchase your metals down the road.

But “guarantee” can mean very different things depending on the fine print. Some programs are legitimate and well-documented. Others are vague promises — no binding terms, no price commitment, no accountability if the company folds.

Get the full terms in writing before you rely on any buyback promise. And verify that the company’s been around long enough to actually honor it.

Are celebrity endorsements of gold companies trustworthy?

A celebrity in a commercial means someone got paid. That’s it.

It doesn’t tell you anything about the company’s pricing, their compliance record, or how they’ll treat you after the sale. Some of the companies with the biggest ad budgets have faced federal enforcement actions.

And with AI-generated deepfake endorsements becoming more common in 2026, you can’t even be sure the celebrity actually participated.

Focus on what matters — pricing, transparency, complaint history, and how the company treats you when you ask tough questions. Not who’s in their TV spot.

Conclusion

Protecting your savings from Gold IRA scams doesn’t take specialized knowledge. It takes the right questions, a few minutes of free research, and the willingness to walk away from anyone who won’t give you straight answers.

The patterns are consistent. Excessive markups. Home storage myths. “Exclusive” coin traps. High-pressure sales. Misleading buyback promises. These are the same tactics that show up in every major enforcement case — and federal agencies are going after them more aggressively than ever.

Your retirement savings represent decades of hard work. You deserve a process that’s transparent, compliant, and backed by a team that stays present long after the paperwork is signed.

The right dealer will welcome your questions — not dodge them.

Ready to explore Gold IRA ownership the right way?

If you’re thinking “this all makes sense, but I don’t have time to figure it out on my own,” you’re not alone. Most customers we work with felt the same way before they realized how straightforward the process can be with the right guidance.

That’s why we offer a complimentary consultation to walk you through your options — including our No Fee Precious Metals IRA, which covers custodial fees for the lifetime of the account on qualified purchases.

We’ll show you exactly:

- How the No Fee IRA works and whether you qualify

- The difference between U.S.-minted coins and foreign alternatives

- What to expect from the purchasing and delivery process

- How to roll over or transfer existing retirement funds

- What ongoing support looks like after your purchase

Learn About the No Fee IRA — no obligation, just actionable insights you can use whether you work with us or not.

Your retirement savings deserve transparency, not tactics. Let’s start with a conversation.