How Are Private Depositories Audited and Insured in 2026?

Private depositories holding physical gold and silver are subject to independent third-party audits and institutional-grade insurance — structured examinations that confirm every ounce on record actually exists in the vault. These aren't courtesy checks. They're recurring, unannounced physical inventory reviews conducted by independent accountants and inspection firms, cross-referencing bar-specific serial numbers against documented custody records.

For owners holding metals inside a self-directed IRA, the rules are precise. Internal Revenue Code Section 408(m) defines which coins and bullion qualify for retirement accounts. The IRS requires those metals be stored at an approved depository — not at home, not in a personal safe. Keeping IRA-eligible metals outside an approved facility is treated as an immediate taxable distribution, subject to penalties.

On the insurance side, reputable depositories carry all-risk coverage — policies that explicitly protect against external theft, internal fraud, and unforeseen loss. Some state-regulated facilities insure deposited metals at 100% of market value. That's a documented policy requirement, not a marketing claim. Owners should confirm it directly before choosing a storage provider.

The Federal Trade Commission advises purchasers to ask whether independent third parties verify vault holdings — and whether insurance policies cover both external theft and internal fraud. That's the right question to ask.

Precious metals may appreciate, depreciate, or remain unchanged. What audits and insurance address isn't price — it's physical accountability. Knowing who holds your metals, under what terms, and with what verified documentation is the foundation of real ownership.

- Why Depository Oversight Is the Foundation of Physical Ownership

- How the Independent Audit Process Actually Works

- What 'All-Risk' Insurance Really Means for Stored Metals

- IRA-Specific Depository Requirements: What the IRS Mandates

-

Frequently Asked Questions

- How often are private precious metals depositories audited in 2026?

- What does 'all-risk' insurance actually cover in a gold depository?

- Are depository audits performed by internal staff or independent third parties?

- How does the IRS verify that depository storage remains compliant for Gold IRAs?

- What is the difference between depository-level insurance and a Lloyd's of London syndicate policy?

- What This Means for Your Metals — and Your Legacy

Why Depository Oversight Is the Foundation of Physical Ownership

Physical gold ownership means something specific. You hold a tangible asset — in your name, outside the paper financial system, with no intermediary standing between you and it. But that meaning collapses the moment the system protecting it goes unverified. A vault is only as trustworthy as the paper trail behind it.

That's the problem most buyers don't see until after the purchase. The metals exist. The receipt exists. But without independently verified records — audited documentation, bar-specific serial numbers, insurance that explicitly covers what it claims to cover — physical ownership is only as strong as someone else's word.

The Federal Trade Commission puts it plainly: ask whether independent third parties verify vault holdings — and whether the insurance policy explicitly covers external theft and internal fraud. Not fine print. The foundation. Every honest custody conversation starts there. For a grounded look at what that due diligence actually involves, start with secure storage for physical wealth.

The Difference Between Storing Gold and Owning It

There's a real difference between metals that are stored somewhere and metals that are genuinely owned. Storage is a location. Ownership is a verifiable legal claim — documented, audited, insured, and traceable to specific bars with specific serial numbers.

Institutional custody standards require custodians to track bar-specific serial numbers — documented, cross-referenced, and physically confirmed on a recurring basis by independent auditors. Your metals aren't just sitting in a room somewhere. They're catalogued against records that exist outside the depository's own books. That recurring, independent verification is what turns a storage receipt into something you can actually stand behind.

See Vaulted Storage for what institutional-grade custody actually requires. The documentation either exists or it doesn't. Most owners only find out which one it is when something goes wrong.

Why Most Buyers Never Ask the Right Custody Questions

Here's what actually happens at most purchase conversations. The buyer confirms the price. Reviews the product specs. Selects a storage tier. And never once asks who performs the audit, how often it happens, or whether the insurance policy covers internal fraud. Those questions don't surface until there's a problem — and by then, the answer matters a great deal.

That gap isn't the buyer's fault. Fear-first marketing keeps attention on crisis scenarios and price swings — not on the procedural rigor that makes a depository worth trusting. Brighton Gold takes the opposite position: the custody structure deserves exactly as much scrutiny as the metals inside it. 26 U.S.C. § 408 places specific legal obligations on custodians of retirement-held metals — and every owner has the right to ask whether those obligations are being met.

The questions aren't complicated. Is the audit conducted by an independent third party — not internal staff? Does the insurance policy name the specific risks it covers, including internal fraud? Are bar-level serial numbers tracked against custody records you can request? Asking those three things before choosing a depository is the difference between informed ownership and a well-intentioned assumption you'll only test under pressure.

| Oversight Layer | Who Is Responsible | What It Verifies | How Often |

|---|---|---|---|

| Independent Physical Audit | Third-party accountant or inspection firm — no affiliation with the depository | Physical presence of every bar and coin against documented custody records; bar-specific serial numbers confirmed | Recurring basis, including unannounced examinations |

| Chain of Custody Documentation | Depository custodian, with oversight by independent auditors | Bar-level serial number tracking from deposit through ongoing storage; continuity of ownership records | Maintained continuously; cross-referenced at each audit cycle |

| All-Risk Insurance Coverage | Depository's insurer, confirmed by policy documentation | Explicit protection against external theft, internal fraud, and unforeseen loss — coverage boundaries verified by the owner | Policy reviewed at renewal; owners should confirm coverage scope before depositing metals |

| IRS Custodian Compliance (IRA holders) | IRS-approved custodian responsible for maintaining regulatory eligibility | That metals meet eligibility standards and remain in an approved facility — not held personally by the account owner | Ongoing; verified at account establishment and monitored through the life of the IRA |

| Owner Verification Rights | The metals owner — exercised through direct inquiry before and after purchase | Whether third-party audits are conducted, whether insurance explicitly names covered risks, and whether records are accessible upon request | Before selecting a depository; periodically throughout ownership |

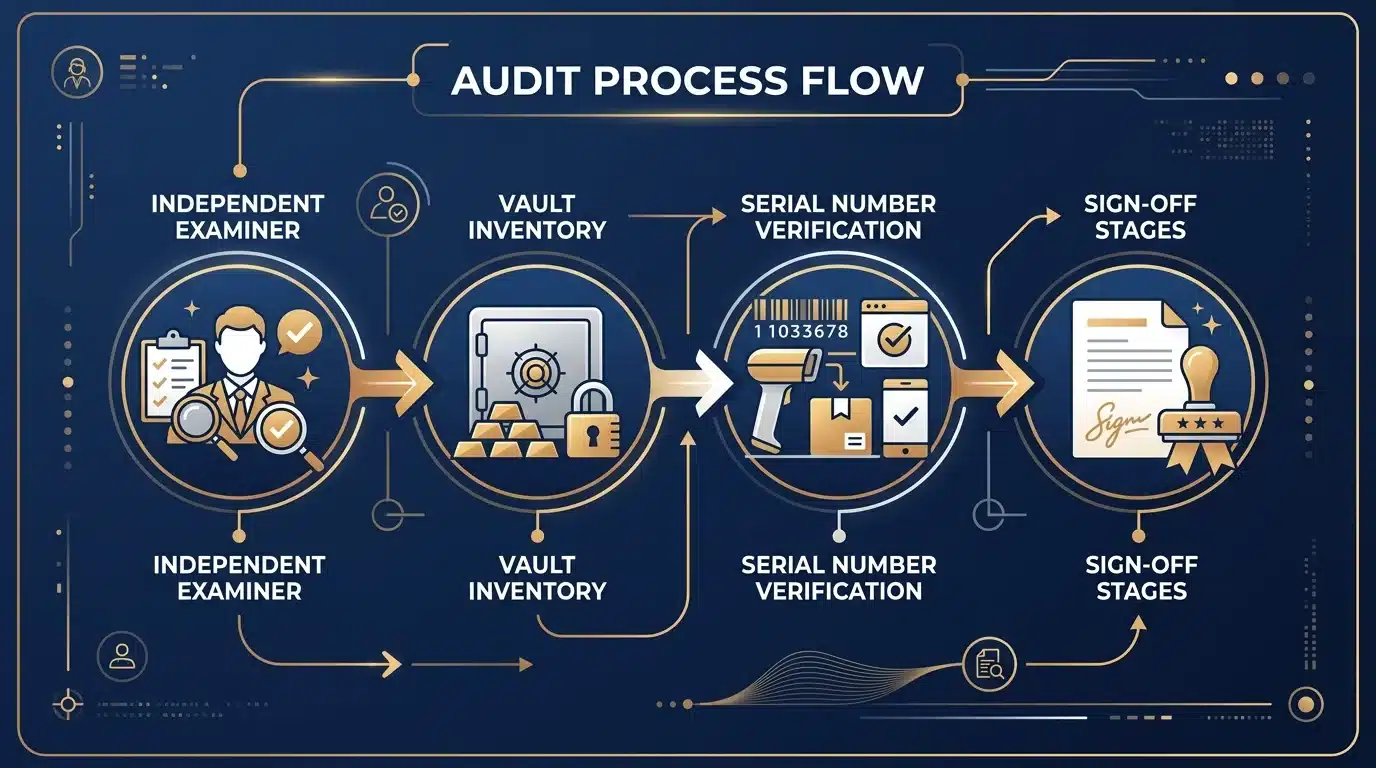

How the Independent Audit Process Actually Works

What gets verified in an audit is more specific than most owners expect. And the specifics are exactly what matter.

Independent audits are conducted by outside accounting firms and inspection professionals — not internal staff. That distinction matters.

The auditor's job is to confirm that the physical assets documented on the depository's books actually exist in the vault, bar by bar. That's not a general inventory sweep. It's a verification run against specific records — one bar, one serial number, one documented entry at a time.

The legal expectations for independent custody verification are unambiguous: qualified custodians must demonstrate that physical assets match documented records through structured, recurring examination.

Audit documentation doesn't describe a vault — it proves one. There's a meaningful difference. A well-written custody agreement tells you what should be there. An independent audit tells you what is.

Surprise Exams and Why They Matter

The most important word in depository auditing is surprise.

Scheduled audits let custodians prepare. Unannounced ones test what's actually there — on an ordinary Tuesday, not a rehearsed inspection day.

Qualified custodians must undergo a surprise annual audit conducted by an independent public accountant. That word — surprise — isn't procedural decoration.

It's the only mechanism that prevents a custodian from presenting a curated snapshot of holdings that looks clean on inspection day but doesn't reflect day-to-day reality. The exam checks the actual physical existence of customer assets against books and records. What's claimed has to match what's physically present. Not approximately. Exactly.

For owners, this comes down to one thing: a depository can't stage what it doesn't know is coming.

What they say is there has to actually be there.

Bar-Level Serial Tracking and Chain of Custody

Physical gold auditing doesn't operate at the vault level. It operates at the bar level.

Custodians must establish a transparent chain of custody that tracks bar-specific serial numbers — meaning every individual piece of metal held in a compliant facility has its own documented identity. Not a category. Not a weight class. A specific bar, with a specific number, tied to a specific record.

That bar-level record is what connects the audit to you specifically. When an independent auditor walks a vault, they're cross-referencing physical inventory against serial-number logs in custody records — not spot-checking a pile, matching individual bars to individual entries.

How metals are held directly affects how that tracking works. It's worth understanding segregated and non-segregated storage before choosing a facility, because the structure of your account determines exactly how traceable your specific metals are.

That's what the chain of custody means in real terms: a documented, traceable record that follows a specific bar from deposit through every audit.

A vault full of gold isn't the same as a vault full of your gold. Serial tracking is what makes that distinction real — and verifiable.

Why the Industry Default Leaves Buyers Guessing

Most depository marketing communicates security in the vaguest possible terms. High-security facilities. State-of-the-art vaults. Ironclad insurance.

None of that is necessarily false. But it tells an owner exactly nothing — not the audit frequency, not who performs it, not what the insurance policy actually covers, not whether a surprise exam has ever taken place.

That's the industry default: reassurance sold in place of documentation. And it holds together fine — right up until something goes wrong.

Regular physical audits are a baseline for risk management and asset verification. Not a premium feature. Not a differentiator. A baseline. But they're rarely what a storage provider leads with, because reassurance is an easier pitch than showing your audit schedule.

Brighton Gold's position is direct: the custody structure deserves the same scrutiny as the metals inside it.

Before choosing a depository, ask who performs the audit — and whether they're truly independent. Ask how often it happens. Ask whether the insurance policy names the specific risks it covers. These aren't complicated questions. They're just the ones the industry has made it quietly easy to skip.

| Audit Type | Who Conducts It | Frequency | What Is Verified | Regulatory Basis |

|---|---|---|---|---|

| Surprise Annual Audit | Independent public accountant — not depository staff | Unannounced, at least annually | Physical existence of customer assets against books and records | SEC custody rule requirements for qualified custodians |

| Bar-Level Physical Inventory | Third-party inspection professionals | Concurrent with surprise audit cycle | Serial number of each bar cross-referenced against custody records | Good Delivery standards and custodial chain of custody obligations |

| Chain of Custody Verification | Independent auditors with access to serial-number logs | Ongoing — triggered by deposits, withdrawals, and audit cycles | Traceable record confirming each specific bar remains present and accounted for | Custodial documentation standards for IRA-eligible metal storage |

| Internal Compliance Review | Depository's own compliance or operations team | Periodic — frequency set by facility protocol | Reconciliation of internal records against physical inventory before third-party examination | Facility-level operational standards |

| Regulatory Examination | Government or state oversight authority (where applicable) | As scheduled by the governing regulatory body | Adherence to licensing conditions, insurance coverage, and security protocols | State bullion depository statutes and applicable federal oversight frameworks |

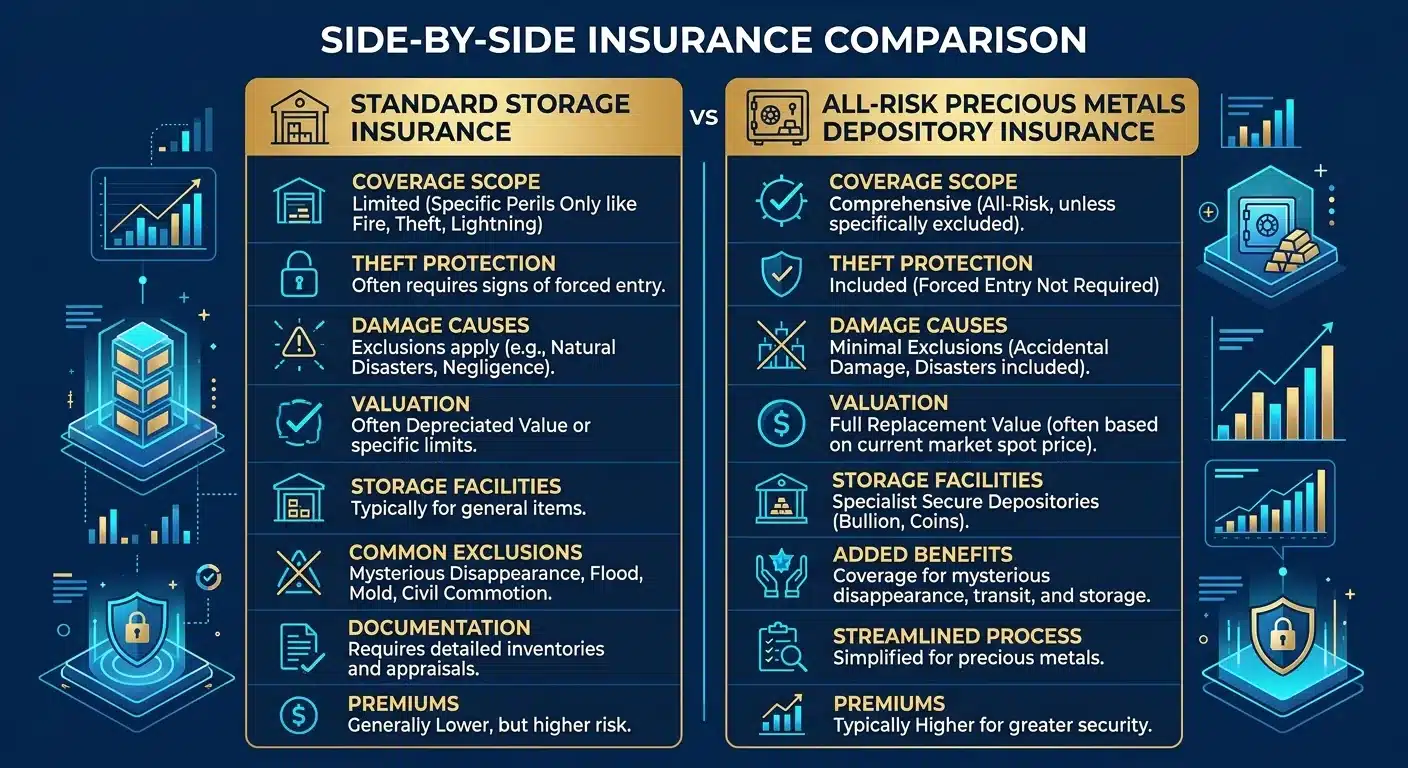

What 'All-Risk' Insurance Really Means for Stored Metals

Audits confirm your metals exist. Insurance answers what happens when something goes wrong anyway. Those are two different questions — and most buyers only ask one.

The term 'all-risk' sounds airtight. That's the design. But the real answer lives in the policy language — and the policy language isn't always what the brochure implies. The FTC is direct about this: buyers must review insurance policies to confirm they explicitly cover external theft and internal fraud. Those two categories aren't automatically included in every contract. Most people don't find out which ones are missing until it's too late to matter.

There's a clear standard. Regulated, state-administered depositories insure deposited metals at 100% of market value. Not 100% for institutional clients. For every account holder. That's the baseline every owner should be measuring a storage provider against — before signing anything.

What All-Risk Coverage Actually Protects

At its most rigorous, all-risk coverage means the insurer accepts full financial liability for stored metals across a defined range of loss scenarios. External theft is the obvious one — a physical breach, metals removed from the vault. Internal fraud is the one that actually keeps institutional risk managers up at night. And it's the one most buyers never think to ask about.

Internal fraud means a depository employee — or the depository itself — misrepresents, misappropriates, or fails to account for your holdings. A policy that covers external theft but excludes internal fraud is protecting against the less likely scenario. The IRS regulatory framework places specific obligations on custodians, but regulatory compliance and insurance coverage are two separate layers. A depository can be IRS-compliant and still leave you exposed. Both layers have to hold.

The FTC is specific: ask whether coverage includes both external theft and internal fraud. Ask that before you sign a storage agreement. Not after a claim. That answer is part of what documented ownership actually means.

The Coverage Gap No One Talks About

Here's what doesn't get said clearly: 'all-risk' is a label. The exclusions are what make it real. Those two things are rarely identical — and the difference lives in the fine print most owners never read.

The gap lives in the exclusions. Natural disaster damage, government confiscation scenarios, and certain categories of internal loss show up as carved-out exceptions in standard commercial policies — not in the headline coverage summary, but in the pages no one reads. An owner who hasn't seen the actual policy can't know which risks are covered and which are left open. That's why chain of custody documentation matters: an audit without adequate insurance leaves gaps in accountability. Insurance without audited records leaves the same gaps from the other direction.

The standard isn't complicated. Deposited metals insured at 100% of market value. Coverage that explicitly names external theft and internal fraud as covered events — in writing, in the policy, not in the sales pitch. If those specifics aren't there, the gap is real. And it won't reveal itself until it's too late to close it.

Who This Arrangement Is Not For

This level of institutional rigor isn't the right fit for everyone. That's worth saying plainly.

If you want the lowest-cost option with minimal documentation and no oversight overhead, a fully audited, fully insured depository is more than you're looking for. The fees reflect the infrastructure — independent audits, bar-specific serial tracking, all-risk insurance at 100% of market value. That structure exists for long-term ownership. It's not built for short-term convenience, and it doesn't pretend to be.

Brighton Gold works with owners who want the full picture before any metals move — custody structure, audit frequency, insurance scope, all of it. Precious metals may appreciate, depreciate, or remain unchanged. What institutional-grade storage provides isn't a performance guarantee. It's verifiable accountability: documented, audited, and insured at every stage of ownership. That's what a lasting family legacy is actually built on.

| Coverage Type | What It Protects Against | Who Typically Carries It | Key Verification Step |

|---|---|---|---|

| External Theft | Physical removal of metals by a third party through a security breach or robbery | Most regulated depositories carrying commercial vault insurance | Confirm the policy explicitly names external theft as a covered event — not implied by 'all-risk' language alone |

| Internal Fraud | Misrepresentation, misappropriation, or failure to account for holdings by a depository employee or operator | Institutional-grade depositories with comprehensive all-risk coverage; often absent from standard commercial policies | Ask directly whether internal fraud is named in the policy — it's the most operationally realistic risk and the one most commonly excluded |

| Natural Disaster Damage | Physical loss or damage caused by fire, flood, earthquake, or other environmental events | Varies widely by facility and insurer; may appear as a standard inclusion or a specific exclusion depending on policy language | Request the exclusions list in writing — disaster scenarios are a common carve-out in commercial storage policies |

| Government or Regulatory Action | Seizure, confiscation, or restriction of stored assets by a government authority | Typically excluded from standard commercial insurance products; not a covered event under most depository policies | Review the policy's exclusions section specifically for governmental action language before signing a storage agreement |

| Full Market Value Coverage | Ensures the insured value reflects current market pricing, not a fixed or depreciated valuation at time of policy issue | State-administered and institutional depositories operating under rigorous oversight standards | Verify that coverage is pegged to current market value — not a fixed ceiling set at deposit — so the insured amount keeps pace with holdings |

IRA-Specific Depository Requirements: What the IRS Mandates

Audits and insurance tell you how a depository operates. The IRS tells you whether it's legally allowed to hold your metals at all.

For owners with self-directed retirement accounts, custody isn't a preference — it's a legal requirement. Internal Revenue Code Section 408(m) defines which coins and bullion qualify for IRA inclusion. It also mandates where those assets must be held. The line between a compliant depository and a non-compliant one isn't about quality. It's about legal standing.

That's what separates IRA-held metals from metals purchased for direct delivery. Both represent physical ownership. But only one carries an IRS compliance obligation — governing custody from the moment of acquisition through every audit, every year the account stays open.

Why Home Storage Is Not an Option

Here's where people get burned: the IRS doesn't grade your home safe. Storing IRA-eligible gold at home is treated as an immediate taxable distribution — penalties included. That's not a technicality buried in fine print. It's the enforcement mechanism. Remove the metals from an approved depository, and the IRS treats the account as if you cashed it out.

This is one of the most expensive misunderstandings in the precious metals space. Holding your own metals sounds like the ultimate form of ownership — and some corners of the industry have historically blurred the line between physical possession and IRA-compliant custody. Those aren't the same thing. Not even close. For a plain-language breakdown of how that confusion spreads, see the home storage IRA misconception.

Physical possession of IRA-held metals triggers immediate tax consequences — it doesn't matter how secure your home setup is. The IRS doesn't evaluate personal storage quality. The rule is structural: IRA metals must reside in an approved depository. Full stop. For owners working through that decision, the learning center offers plain-language guidance on how IRA-compliant custody actually works.

IRS-Approved Metals and Purity Standards

Not every gold product qualifies for a self-directed IRA. The IRS sets specific purity and form requirements, and the IRA contribution framework — grounded in Internal Revenue Code Section 408(m) — determines which assets custodians are permitted to hold. Gold bullion must hit a minimum purity of 99.5% fine gold. Below that threshold, the metal doesn't qualify. It doesn't matter how it's stored or who holds it.

Standard Good Delivery gold bars must weigh between 350 and 430 fine troy ounces. Those aren't arbitrary numbers — they're the institutional benchmark that connects private depository holdings to globally recognized custody standards. A bar that doesn't meet the spec doesn't meet the standard.

Product selection isn't a separate decision from custody. Metals that don't meet IRS purity and form requirements can't be held in a compliant depository for IRA purposes. Precious metals may appreciate, depreciate, or remain unchanged. What the eligibility standards ensure is that what you hold is exactly what institutional-grade custody is built to receive, verify, and audit.

How Custodians and Depositories Work Together

In an IRA structure, the custodian and the depository do different jobs — and you need both. The custodian is the IRS-approved financial institution administering the account: handling documentation, processing transactions, keeping the records clean. The depository is the physical facility holding the metals. One manages the paper. The other manages the vault. Neither replaces the other.

That separation creates two independent layers of accountability. The custodian maintains the account record. The depository maintains the physical inventory. When those two records are reconciled by an independent auditor, that's when the paper trail connects to the vault. A vault is only as trustworthy as the paper trail behind it — and the custodian-depository relationship is where that trail begins.

Brighton Gold works with owners to make this structure clear before anything is signed. The custodian you choose and the depository they work with are both part of the ownership decision — not administrative afterthoughts. Understanding how those two institutions interact is what turns IRS compliance from a paperwork burden into a foundation you can actually rely on. That's where real ownership starts.

| Metal Type | Minimum Purity Requirement | IRS-Approved Examples | Good Delivery Standard |

|---|---|---|---|

| Gold Bullion Bars | 99.5% fine gold minimum | LBMA Good Delivery bars | 350–430 fine troy ounces; 99.5% minimum purity |

| IRA Custodian-Held Metals (all eligible types) | Purity and form requirements per IRC Section 408(m) | Must reside in an IRS-approved depository — no personal custody permitted | Personal custody triggers immediate taxable distribution |

Frequently Asked Questions

Some questions don't show up in a standard walkthrough. They're the ones owners ask after they've already read the basics — and still aren't satisfied.

These are the sharper questions Brighton Gold hears from owners who've done the research and want specifics, not reassurance.

How often are private precious metals depositories audited in 2026?

The baseline: a surprise annual audit by an independent public accountant. That's the standard for qualified custodians — and it's unannounced by design, so there's no time to stage a clean inventory.

Some state-regulated facilities add extra unannounced third-party reviews on top of that. Frequency depends on the depository and its regulatory framework.

Don't take the depository's word for it. Ask directly — and get the answer confirmed in writing.

What does 'all-risk' insurance actually cover in a gold depository?

At a well-run depository, all-risk coverage insures metals at 100% of market value. That policy should explicitly name external theft and internal fraud as covered events.

Here's what it doesn't automatically include: natural disaster scenarios, government confiscation, and certain categories of internal loss.

The label says "all-risk." The policy language decides what that actually means. Read it. Don't assume coverage because the name sounds complete.

Are depository audits performed by internal staff or independent third parties?

Independent third parties. That's the standard for qualified custodians — a surprise annual audit by an independent public accountant.

Internal staff verifying their own inventory isn't a check. It's a record. The point of a surprise exam is that the depository doesn't see it coming. The auditor shows up and verifies that customer assets on the books actually exist in the vault.

Internal reviews happen too. But they don't replace that external layer, and any depository that conflates the two deserves a harder question.

How does the IRS verify that depository storage remains compliant for Gold IRAs?

The IRS doesn't walk vaults. Its enforcement is structural.

Under Internal Revenue Code Section 408(m), IRA-eligible metals must be held in an approved depository. Store them at home instead, and the IRS treats it as an immediate taxable distribution — with penalties on top.

Compliance isn't verified by an auditor showing up. It's enforced by the tax cost of getting it wrong. The IRS doesn't need to inspect the vault. The rules make non-compliance expensive enough to be self-policing.

What is the difference between depository-level insurance and a Lloyd's of London syndicate policy?

Depository-level insurance is the facility's own commercial policy — covering metals on the premises under that depository's specific terms. A Lloyd's of London syndicate policy is a specialized underwriting arrangement, typically offering higher coverage limits or broader risk categories than a standard commercial product.

The practical difference is scope and ceiling.

A reputable depository insures metals at 100% of market value regardless of which structure backs the coverage. So the underwriter's name matters less than most owners think. What matters is whether the policy is explicit, verified in writing, and names the specific risks it actually covers. Ask for documentation. If the depository hesitates, that's your answer.

What This Means for Your Metals — and Your Legacy

Every layer of this system points to the same truth: physical gold ownership is only as real as the institutional infrastructure behind it.

Audits confirm what's in the vault. Insurance defines what happens if something goes wrong. IRS compliance determines whether the whole structure has legal standing.

These aren't bureaucratic obstacles. They're what separates a metal bar in a room from documented, verifiable wealth — the kind that holds up under scrutiny, outlasts market cycles, and means something when it's time to pass it down.

A vault is only as trustworthy as the paper trail behind it.

That's not a cautionary note. It's the standard that makes physical ownership worth holding.

When audit records are clean, insurance scope is explicit, and the custodian and depository reconcile independently — what you have isn't just gold in a room. You have a documented chain of accountability that survives market cycles, political uncertainty, and time. Not price performance. Verifiable, transferable ownership. The kind a lasting family legacy is actually built on.

Precious metals may appreciate, depreciate, or remain unchanged. What institutional-grade oversight provides isn't a promise about value — it's clarity about possession.

Brighton Gold works with owners who want that clarity before anything moves: custody structure understood, audit frequency confirmed, insurance scope reviewed in writing.

That's what it means to own something real. And the only question worth asking now is whether the documentation behind your metals is strong enough to prove it.

You now know what to ask. The harder question is whether your current setup can actually answer it — the audit schedule, the insurance scope, the custody chain, all of it.

Brighton Gold offers a complimentary consultation to walk you through exactly that. Not a sales pitch. Not a product demo. A straight conversation about whether your storage structure holds up.

Learn About the No Fee IRA

Most people walk away from that conversation with more clarity than they expected. That's the point.