How Do I Transition My Gold from Home Storage to a Professional Vault?

Transitioning physical gold from home storage to a professional vault comes down to four steps: inventory your holdings, select a custodian and depository, ship with insured transit logistics, and confirm receipt and establish ongoing access. Each step moves privately held bullion from a domestic setting into an institutional-grade environment — fully insured, independently audited, and eligible for a self-directed Precious Metals IRA.

The process starts with a written inventory of every coin, bar, and round you own. Weight, purity, condition — all of it documented. That record becomes the chain of custody that follows your metals from your door to the vault.

From there, you select an IRS-approved custodian and depository. Under Internal Revenue Code Section 408(m), IRA-eligible precious metals must be held by an approved trustee. Home storage doesn't satisfy that requirement — regardless of how secure the safe is.

Shipping is handled through insured transit carriers that specialize in high-value commodity logistics. Metals are packed to professional standards, assigned a declared value, and covered by transit insurance for the full journey. Once the depository verifies the shipment against your inventory, you receive confirmation and gain access through the custodian's reporting systems.

Precious metals may appreciate, depreciate, or remain unchanged. The decision to move them into professional custody isn't about price performance — it's about ownership structure. Home storage carries real liabilities: limited insurance coverage, no IRA eligibility, reduced liquidity when it's time to sell or transfer. Professional vaulting removes each of those frictions without surrendering a single ounce of ownership.

The gold doesn't change. Its situation does.

- Why Home Storage Creates Hidden Liabilities

- What a Professional Vault Actually Provides

- The Step-by-Step Transition Process

- Who This Process Is Right For — and Who It Isn't

-

Frequently Asked Questions About Transitioning Gold to a Vault

- Is it legal to transition privately stored home gold into a professional depository?

- How does professional vaulting protect gold from home storage security liabilities?

- What are the specific steps required to physically pack and ship gold to a vault?

- How does third-party transit insurance work during a home-to-vault gold transition?

- Can I transition my home-stored gold into an IRA-compliant vault system?

- Your Gold Hasn't Changed — Its Situation Has

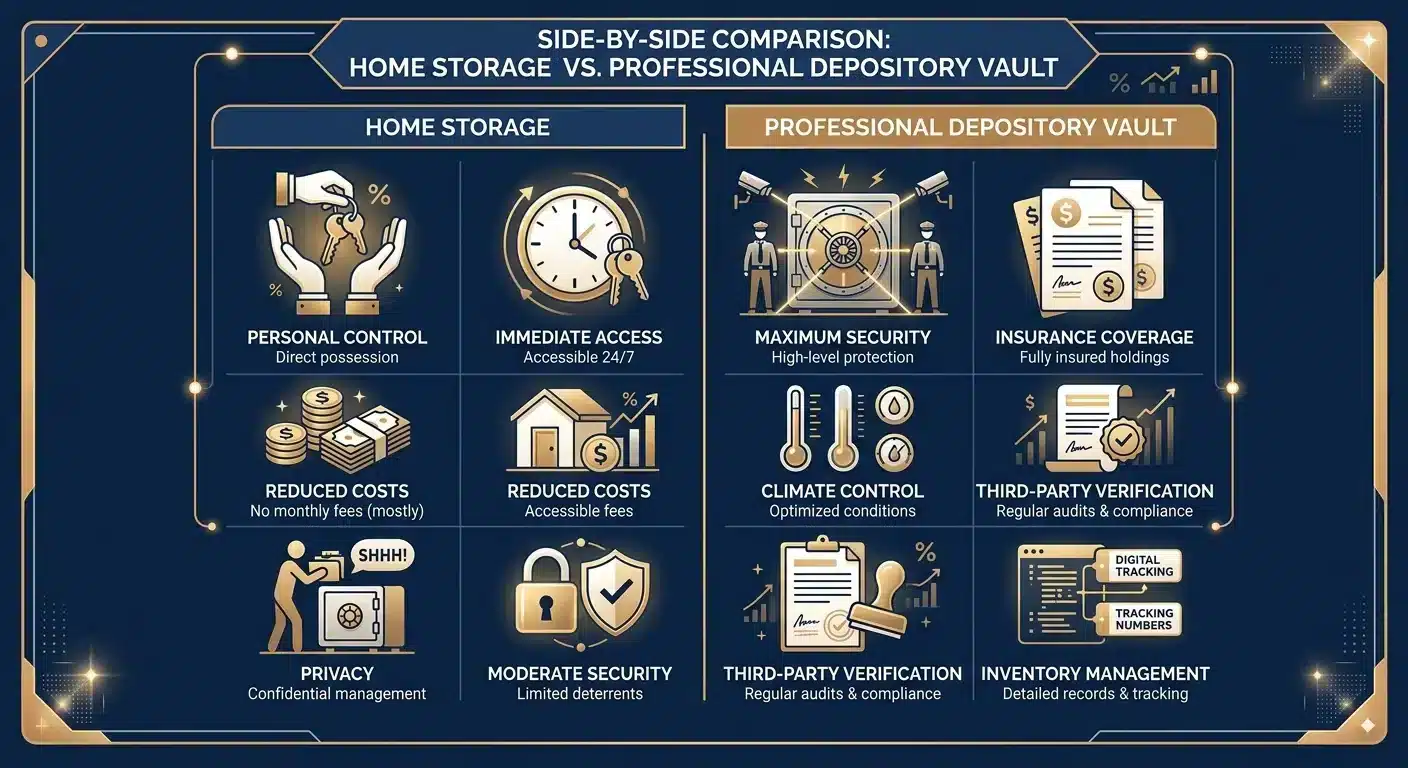

Why Home Storage Creates Hidden Liabilities

Gold in a home safe feels secure. Tangible, close, yours. But feeling secure and being institutionally recognized as secure are not the same thing — and that gap is where most home storage strategies quietly fall apart.

Home storage creates three friction points that don't disappear because the safe is bolted to the floor: limited insurance coverage, zero IRA eligibility, and reduced liquidity when it's time to sell or transfer. These aren't edge-case risks. They're structural — built into the nature of private domestic storage itself. Understanding physical wealth protection risks starts with recognizing that proximity to your metals isn't the same as security around them.

The numbers make the direction clear. Gold demand reached 4,899 tonnes in 2023 — with central banks alone acquiring 1,037 tonnes of that total. That level of institutional participation isn't coincidence. Serious gold ownership has migrated toward professional custody. Home storage keeps you on the outside of that ecosystem. gold demand reached 4,899 tonnes

Why the 'Safe at Home' Assumption Fails

Read your homeowner's policy carefully — most owners don't until after something goes wrong. Standard homeowner and renter insurance places strict sub-limits on precious metals. That cap is often a fraction of what a real bullion holding is worth. A modest theft limit offers no meaningful protection for a serious position. The policy isn't built for gold. It's built for furniture.

The CFTC's consumer warnings on precious metals schemes specifically flag non-compliant home storage configurations as a zone of elevated legal and financial risk. And the concern isn't just theft. It's the entire framework of documentation, custodianship, and regulatory standing that home storage doesn't provide. Without an approved custodian in the chain, your metals exist outside any institutional verification system. That invisibility has real consequences — in an IRA context, in an estate context, and the moment you try to liquidate.

That last point matters most for anyone with retirement savings in mind. Home-stored metals — no matter how pure, no matter how carefully documented — don't qualify for an IRA. Under Internal Revenue Code Section 408(m), the IRS requires an approved trustee to hold those assets. That's not a technicality. It's a hard disqualification. What secure vaulted storage delivers is a resolution to all three friction points at once: proper insurance coverage, institutional documentation, and a direct path to IRA-compliant custody when that's the direction you want to go.

| Risk Category | Home Storage Exposure | Professional Vault Protection |

|---|---|---|

| Insurance Coverage | Standard homeowner or renter policies impose strict sub-limits on precious metals — often far below the actual value of a substantial bullion holding | Professional depositories carry comprehensive, purpose-built insurance coverage scaled to the full declared value of stored metals |

| IRA Eligibility | Home-stored metals do not satisfy IRS requirements regardless of purity, documentation, or security measures in place — they are categorically excluded from IRA custody | Approved depositories meet IRS trustee requirements under Internal Revenue Code Section 408(m), making professional vault storage the only path to IRA-compliant precious metals ownership |

| Liquidity and Transferability | Privately stored metals exist outside institutional verification systems, creating friction and delays when it comes time to sell, transfer, or establish provenance with a dealer | Vault-held metals carry continuous chain-of-custody documentation and institutional verification, supporting faster, cleaner transactions when you choose to act |

| Documentation and Chain of Custody | Home storage relies entirely on personal records — receipts, photos, written logs — with no independent third-party verification of what you hold or its condition | Professional custodians maintain independent, auditable records of every holding, weight, purity, and condition — documentation that travels with the metals and satisfies institutional standards |

| Regulatory Standing | Non-compliant home storage configurations carry elevated legal and financial risk, particularly when marketed as IRA-eligible — a category the CFTC specifically flags in its consumer protection guidance | Institutional custody places metals within a fully regulated framework, with licensed custodians and approved depositories providing the legal standing that home storage cannot replicate |

| Audit and Verification Access | Owners of home-stored metals have no independent verification mechanism — there is no third party to confirm holdings, condition, or weight outside of personal record-keeping | Vault-held metals are subject to independent audits, and owners can request formal verification of their holdings through the custodian's reporting systems at any time |

What a Professional Vault Actually Provides

Home storage answers one question: where is it?

Professional vaulting answers everything else — what it's worth on paper, whether it qualifies for an IRA, how fast it can be liquidated, and whether a counterparty will accept it without hesitation.

That's the difference between gold that works for you and gold that simply sits.

An approved depository delivers four things no home setup can replicate: institutional-grade insurance covering the full declared value, independent third-party auditing, recognized chain-of-custody documentation, and direct eligibility for IRA-compliant custody.

That's not a premium add-on. It's the operating standard of every accredited vault in the country.

It's also the foundation behind the Brighton Gold concierge vaulting model — built so owners don't have to work through that infrastructure alone.

The ounces don't change. What changes is the institutional standing of those ounces.

That standing determines insurability, liquidity, and IRA eligibility. Precious metals may appreciate, depreciate, or remain unchanged — but the structure around them shapes how much of that value you can actually access when it matters.

Same gold. Different situation entirely.

IRA Compliance and the Custody Requirement

IRA eligibility isn't something a vault adds to your metals. It's a legal standard the vault's custodian satisfies on your behalf.

Under Internal Revenue Code Section 408(m), IRA assets held in precious metals must be in the physical possession of an IRS-approved trustee or custodian. Self-custody — no matter how secure the arrangement feels — doesn't meet that standard.

There's no workaround. There's no documentation that makes home storage IRA-compliant.

That requirement exists for a reason. Retirement assets held independently, audited by a third party, documented inside a recognized regulatory framework — that's the structure the IRS is enforcing.

A high-quality safe doesn't change that. A solid insurance rider doesn't change that. Meticulous personal records don't change that. The metals are yours. But the IRS doesn't recognize home storage as compliant for retirement account purposes — full stop.

The gap isn't about trust in you as an owner. It's about whether the custody structure meets a defined legal standard.

For anyone wondering whether existing holdings can move into an IRA-eligible vault structure, Brighton Gold's educational resource center covers the custodian selection process in detail.

But here's the short version: once your metals are in an approved depository under an IRS-recognized custodian, the compliance question resolves. What was previously ineligible becomes eligible.

Not because the metal changed. Because the custody structure finally matches what the law requires.

| Feature | Home Storage | IRS-Approved Depository |

|---|---|---|

| Insurance Coverage | Sub-limits under standard homeowner or renter policies — often far below actual bullion value | Full declared value covered under institutional-grade vault insurance |

| IRA Eligibility | Not eligible — home custody does not satisfy IRS trustee requirements regardless of security measures | Fully eligible — depository operates under an IRS-approved custodian framework |

| Chain of Custody Documentation | Personal records only — no independent verification or institutional recognition | Independently audited records maintained by the depository and custodian |

| Liquidity on Sale or Transfer | Buyers and institutions may require re-assay or independent verification before accepting | Recognized chain of custody documentation accepted directly by institutional buyers |

| Third-Party Auditing | None — holdings exist outside any institutional verification system | Regular independent audits confirm holdings, weight, and purity on record |

| Regulatory Standing | Outside any recognized regulatory or compliance framework | Fully documented within an established custodial and regulatory structure |

The Step-by-Step Transition Process

The 'why' is settled. Here's the 'how.'

Four steps. Each one simpler than most owners expect.

- Document and inventory your holdings

- Choose your vault and custodian

- Pack and ship with insured transit logistics

- Confirm receipt and establish ongoing access

Step 1: Document and Inventory Your Holdings

Before anything moves, you need a written record of everything you own. Every coin, bar, and round — documented by denomination, weight, purity, mint year, and condition.

This isn't paperwork for its own sake. It's the chain of custody that travels with your metals from your home to the vault.

Professional depositories verify contents against your paperwork at intake. If the numbers don't match, the shipment stalls — and so does everything that follows.

Get the inventory right upfront. That record travels with your metals for as long as you own them.

Photograph everything before it's packed. Serial numbers on bars. Edge markings on coins. Anything that makes one piece distinguishable from another.

That detail isn't bureaucratic caution — it's what makes the chain of custody defensible at every stage that follows.

Step 2: Choose Your Vault and Custodian

Here's a distinction most people miss: you're choosing two things, not one.

The depository is the physical facility — the vault where your metals live. The custodian is the legally recognized entity that holds title on behalf of your account. Related decisions, but separate ones. And under Internal Revenue Code Section 408(m), the custodian isn't optional for any IRA-eligible holding. It's the legal structure that makes compliance possible at all.

Not all depositories operate at the same standard — and the differences matter. Look for segregated storage, meaning your metals held separately rather than pooled with other customers' holdings. Full-value insurance coverage. Independent third-party auditing on a regular schedule.

The transition physical gold process Brighton Gold supports connects customers directly to vetted custodians and approved depositories. You don't have to evaluate each option from scratch.

Central banks and institutional buyers have been moving sustained gold demand into exactly these kinds of professional custody structures. That's not coincidence.

When you choose an approved depository and custodian, you're entering the same framework that governs serious gold ownership at every scale.

Step 3: Pack and Ship with Insured Transit Logistics

Shipping physical gold is not the same as shipping a package. Treat it like one and you're exposed.

This step requires a carrier that specializes in high-value commodity logistics — declared value coverage, tamper-evident packaging standards, and full transit insurance from handoff to depository intake.

Each piece individually protected. The shipment sealed, labeled with declared value, and covered under a transit insurance policy that matches what you're sending.

Don't rely on standard carrier liability caps — those exist for ordinary parcels, not bullion shipments. The declared value on your transit policy should match your inventory documentation exactly. Any gap there is a gap in your coverage.

Institutional depositories work with vetted logistics partners for exactly this reason. Clean transit documentation creates an unbroken paper trail — from your front door to the depository's intake desk.

That trail is what makes every subsequent account statement and third-party review defensible. It's also where the audit process begins. Knowing how to audit vaulted gold starts here, with the records you create before anything ships.

Step 4: Confirm Receipt and Establish Ongoing Access

When your shipment arrives, the depository's team verifies the contents against your documented inventory. Every piece weighed, inspected, and logged into the facility's system.

You receive written confirmation of receipt. That's the moment custody formally transfers — from transit to institutional holding.

From that point, your access runs through the custodian's reporting and audit systems — account statements, third-party audits, IRA account management if you've set that structure up.

The gold that was sitting quietly in a home safe, invisible to any institutional record, is now fully documented, fully insured, and fully recognized.

The ounces are the same. What changes is everything around them — the insurance structure, the audit trail, the IRA eligibility, the liquidity when it actually matters.

A home safe answers one question: where is it? Professional custody answers every other question that determines what that gold can actually do for you and your family.

The metal doesn't change. Its situation does.

| Transition Step | Key Action | What to Verify | Common Pitfall |

|---|---|---|---|

| Document and Inventory Your Holdings | Create a written record of every coin, bar, and round — denomination, weight, purity, mint year, condition, and any identifying features such as serial numbers or edge markings | Inventory matches what will actually ship; photographs taken; all identifying details logged before packing begins | Relying on memory or a rough estimate — if the shipment contents don't match the paperwork at depository intake, the verification process stalls and the chain of custody is compromised |

| Choose Your Vault and Custodian | Select an IRS-approved custodian and an approved depository that offers segregated storage, full-value insurance coverage, and independent third-party auditing | Custodian holds IRS-recognized legal title; depository maintains segregated — not pooled — storage; facility operates under independent audit protocols | Conflating the depository and the custodian — these are two distinct decisions; choosing a facility without confirming the custodian's IRS-approved status leaves the IRA eligibility question unresolved |

| Pack and Ship with Insured Transit Logistics | Use a carrier that specializes in high-value commodity shipping; pack to professional standards with tamper-evident materials; declare full value and confirm transit insurance matches the inventory documentation exactly | Transit insurance covers the full declared value from handoff to depository intake; declared value on the policy matches inventory records; tamper-evident seals are intact at delivery | Relying on standard carrier liability limits — those caps apply to general parcels, not bullion shipments; a gap between declared value and insurance coverage creates unrecoverable exposure during transit |

| Confirm Receipt and Establish Ongoing Access | Receive written confirmation of receipt from the depository; verify every piece has been weighed, inspected, and logged; establish custodian account access for statements, audit requests, and IRA management | Written receipt confirms contents match the shipped inventory; every item is logged in the depository's system; account access is active and audit-capable from day one | Treating receipt confirmation as a formality — discrepancies between the shipped inventory and the depository's intake log are far easier to resolve immediately than weeks or months later |

Who This Process Is Right For — and Who It Isn't

Straightforward process. Not a universal one.

This transition serves specific owners well. Others, it doesn't serve at all. That distinction is worth naming before you decide anything.

Brighton Gold doesn't manufacture urgency. That's not how we work.

What we do is give you a clear picture — where professional custody genuinely changes the outcome, and where it doesn't.

Most owners don't make this call based on what professional custody is. They make it based on what it unlocks — and whether that matters to their situation. The answer starts with chain of custody documentation.

The Right Customer for Professional Vaulting

This transition is built for owners holding meaningful quantities of physical gold — and who want those holdings to actually do something.

IRA eligibility. Institutional-grade insurance. Clean liquidation when the timing is right. Professional custody is what makes each of those possible. Not someday. Now.

It's also the right move for owners who've been building their holdings over time — and now feel the gap between what they're protecting and what their storage arrangement actually provides.

The Commodity Futures Trading Commission has documented the legal and financial risks tied to non-compliant home storage configurations. A better safe doesn't fix that. A stronger insurance rider doesn't fix that. The risk resolves when the custody structure meets the standard the regulatory environment actually recognizes.

Serious ownership, at every scale, trends toward the most defensible structure available. That's not coincidence.

If that's the standard you want your gold to meet, this transition is the path.

Who Should Not Make This Move

Here's who this isn't for. Short-term traders — buying today, selling in six months on a price forecast — professional vaulting adds cost and process without adding value to that objective.

Brighton Gold isn't the right fit for that relationship. We'd rather say it plainly than waste your time.

And if what you want is someone to hand you a guaranteed outcome — a fiduciary telling you exactly what to do with your money — that's not Brighton Gold. We don't pretend otherwise.

We educate. We guide the transition. We support you at every stage of ownership. What you do with that information is your call.

Precious metals may appreciate, depreciate, or remain unchanged. Professional custody doesn't change that reality. It ensures that whatever happens, your gold is held in the most defensible, most accessible structure available to you.

Frequently Asked Questions About Transitioning Gold to a Vault

Most people aren't confused about whether vaulting makes sense. They're stuck on what happens next — the specifics that come up when the metal is in front of you and a decision has to be made.

Here's what comes up most often. Answered straight.

Is it legal to transition privately stored home gold into a professional depository?

Yes. Completely legal.

Gold you own outright has no legal restriction on where it lives. Moving it from a home safe to a professional depository is a transfer of physical custody — not a regulated transaction, not a filing event, not something that requires regulatory approval.

The legal layer only enters when IRA eligibility is involved. Under Internal Revenue Code Section 408(m), IRA-held precious metals must be in the custody of an IRS-approved trustee or custodian. Self-storage of IRA gold isn't permitted — full stop.

But for privately purchased gold you own outside a retirement account? The decision is yours. A well-documented, properly insured shipment. That's the whole transaction.

How does professional vaulting protect gold from home storage security liabilities?

Home storage answers one question: where is it? Professional vaulting answers the questions that decide what your gold can actually do.

A better safe doesn't fix the structural problems. Theft exposure, fire and flood vulnerability, zero independent documentation — those aren't fringe scenarios. They're baked into the nature of private domestic storage.

The Commodity Futures Trading Commission has specifically documented the legal and financial risks tied to non-compliant home storage configurations. The concern isn't just theft. It's the entire framework of documentation, custodianship, and regulatory standing that home storage doesn't provide.

Professional depositories run under independent auditing. They carry full-value insurance built for high-value bullion. They hold your metals in segregated storage — your ounces, separate from everyone else's.

That's the difference between storing gold and holding gold.

What are the specific steps required to physically pack and ship gold to a vault?

Every piece gets individually protected before it goes into outer packaging — wrapped, cushioned, separated so nothing shifts in transit.

The shipment is sealed and labeled with a declared value that matches your inventory exactly. Then it moves only through a carrier that specializes in high-value commodity logistics. General carrier liability caps aren't built for bullion. You need declared-value coverage and transit insurance that reflects the full worth of what you're sending — from pickup through depository intake.

At intake, the depository team verifies every piece against your inventory documentation. Each item weighed, inspected, logged into the facility's system.

You get written confirmation of receipt. That's the chain-of-custody transfer — the moment your gold moves from transit into institutional holding.

How does third-party transit insurance work during a home-to-vault gold transition?

Transit insurance for bullion isn't standard parcel coverage. It's a declared-value policy — it covers the full stated worth of your shipment, not a liability cap, not a replacement-cost estimate.

You declare the value when the shipment is initiated. The policy covers that amount from pickup through depository intake.

Here's where owners get tripped up: your declared value has to match your inventory documentation exactly. Any gap between the two creates a problem the moment you ever need to file a claim.

Vetted logistics partners that specialize in precious metals handle this as standard operating procedure — not a special request. Clean documentation, full declared value, unbroken coverage. That's what professional bullion transit looks like.

Can I transition my home-stored gold into an IRA-compliant vault system?

Yes — and for many owners, IRA eligibility is exactly what drives the decision.

Under Internal Revenue Code Section 408(m), IRA-held gold must be in the custody of an IRS-approved trustee or custodian. Home storage doesn't meet that standard. Doesn't matter how good the safe is. Doesn't matter what the insurance rider says.

When those same ounces move into an approved depository through a self-directed IRA structure, they become IRA-eligible — fully documented, custodian-held, compliant with the regulatory framework that the IRS actually recognizes.

Brighton Gold's concierge transition process is built for exactly this path: connecting you with vetted custodians and approved depositories so the IRA structure is established correctly from the start.

The metals don't change. The structure they sit inside does.

Your Gold Hasn't Changed — Its Situation Has

Think about what's actually sitting in that home safe.

Same ounces. Same purity. Same metal you paid for.

But invisible — to every institution, every custodian, every system that determines what that gold can actually do when you need it to do something. The insurance structure isn't there. The audit trail isn't there. The custodial documentation that makes your holdings liquid, transferable, and IRA-eligible isn't there.

The gold doesn't change. Its situation does.

Four steps close that gap entirely.

Document and inventory. Choose your vault and custodian. Ship with insured transit logistics. Confirm receipt and establish ongoing access.

When those four steps are done, the gold that used to answer one question — where is it? — now answers all of them. Who holds it. Whether it's insured. Whether it qualifies for an IRA. Whether it can be liquidated cleanly when the time comes.

Professional custody doesn't change what you own. It changes what your ownership can actually do.

That's the moment Brighton Gold's concierge transition process is built for — when what you're holding has outgrown the structure it's sitting in.

No pressure. No urgency. No deadline we manufactured to move you faster than you're ready to go.

A clear, supported path from where your gold is today to a structure that's institutionally recognized, fully insured, and capable of doing what you need it to do.

The home safe answered where. The vault answers everything that comes after that.

Your metals don't change. But what they're sitting inside — and what that costs you in risk, liquidity friction, and IRS exposure — that's worth a real conversation. Brighton Gold's complimentary consultation walks you through exactly what a transition looks like for your specific holdings, including how the No Fee Precious Metals IRA works and whether your metals qualify.