How Does the Industrial Demand for Silver Impact Wealth Preservation?

Industrial demand is depleting the physical silver supply — permanently.

That is the core dynamic connecting silver's industrial role to long-term wealth preservation. It is not a forecast. It is a math problem already in progress, and the numbers are unambiguous.

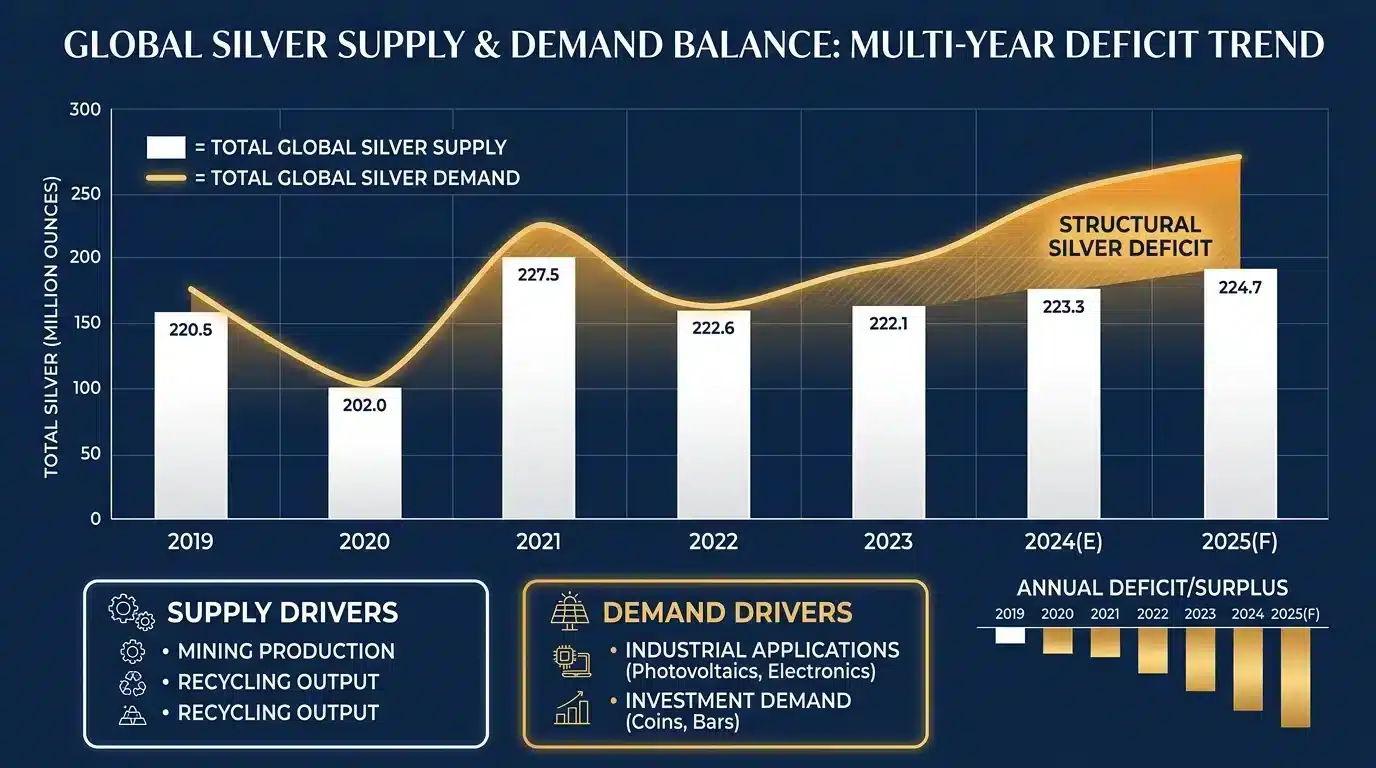

Global industrial silver demand is projected to reach a record 710.9 million ounces — a 9% increase driven by photovoltaic solar panels and electric vehicles. At the same time, global silver mine production fell to 830.5 million ounces in 2023, a 1% contraction that leaves the supply side unable to keep pace. The result: a structural physical deficit projected at roughly 215.3 million ounces — the fourth consecutive year the world has consumed more silver than it has produced.

The pressure comes from both directions at once. Industrial consumption burns through the available float from one side. Contracting mine supply fails to replenish it from the other.

Photovoltaic demand alone reached 193.5 million ounces in 2023 — a 64% increase from the prior year. Solar panels require up to 20 milligrams of silver per watt of capacity. That silver is not recovered. It is consumed and permanently removed from the global physical supply.

Silver is not simply a commodity subject to sentiment and price cycles. It is a metal with a shrinking physical float, driven by industrial mandates written into national energy policy and manufacturing supply chains worldwide.

For anyone considering physical silver ownership as part of a long-term wealth protection strategy, this industrial pressure is not background context. It is the foundation. The factory floor and the vault are competing for the same limited supply — and that competition does not resolve in favor of abundance.

- Silver's Dual Identity: Industrial Metal and Monetary Asset

- Why Most Precious Metals Buyers Miss the Industrial Story

- The Green Energy Mandate Is Rewriting Silver's Demand Floor

- What the Supply Deficit Means for Physical Silver Owners

- How to Think About Physical Silver as a Wealth Preservation Tool

-

Frequently Asked Questions

- How does rising industrial demand for silver affect its availability for physical wealth preservation?

- Why does silver's role in green energy technology make it a strategic long-term hold?

- Does industrial consumption of silver mean its price is more volatile than gold?

- Can a global recession reduce industrial silver demand and hurt my wealth preservation plan?

- How does the industrial supply deficit impact the physical premiums of silver coins and bars?

- Physical Silver in a World That Can't Stop Using It

Silver's Dual Identity: Industrial Metal and Monetary Asset

No other metal lives in two worlds at once the way silver does.

It carries thousands of years of monetary history — real, tangible, universally recognized as a store of value. And it is, right now, being permanently consumed by the technologies powering the modern economy.

Both identities are operating at full intensity. At the same time.

Most metals pick a lane. Gold is almost entirely monetary — its industrial footprint is small relative to its role as a store of value. Copper is almost entirely industrial — nobody holds copper bars as a wealth protection strategy.

Silver does both. Not partially — fully. That is what makes its position structurally different from every other metal on the market.

That duality is not an interesting footnote. It is the reason the supply math hits differently for owners.

When industrial mandates permanently consume physical silver at record rates, the same metal that has served as sound money for civilizations gets pulled off the table — ounce by ounce — by the factory floor. Understanding how that silver industrial-wealth dynamic works is the starting point for any serious conversation about physical ownership.

The Metal That Serves Two Masters

Think of it as serving two masters — and both masters are demanding more simultaneously.

On one side: manufacturers and energy producers who need silver because no substitute performs at the same level for the same cost. On the other: those seeking to preserve wealth outside the traditional financial system, for the same reason their predecessors did for centuries. Silver is real. It is portable. It is universally recognized.

Both sides want the same physical metal. Neither side is stepping back.

Here's what that looks like in practice. Photovoltaic silver demand alone reached 193.5 million ounces in 2023 — a 64% increase from the prior year. Solar panels require up to 20 milligrams of silver per watt of generating capacity.

That silver is not recovered at the end of a panel's life in any meaningful commercial volume.

It is consumed. Permanently removed from the physical float.

That is the tension at the center of silver's dual identity.

The same ounces that would otherwise change hands between owners are being soldered into solar infrastructure across the globe. Both masters draw from the same finite pool — and only one of them ever adds back to it.

Why the Industrial-Wealth Dynamic Is Unique to Silver

No other precious metal faces this structural tension at this scale.

Gold's industrial consumption is modest relative to its total above-ground supply. Platinum and palladium serve industrial roles, but their monetary track records are narrow by comparison. Silver alone carries the full weight of both functions — simultaneously, at scale, with no substitute waiting in the wings.

That is precisely what makes its supply dynamics so consequential for those who hold it.

So what does that mean for someone considering physical silver today?

It means the global mandates accelerating solar panel deployment — written into energy policy across the United States, Europe, and Asia — are directly competing with every owner who wants to acquire or hold the real thing. The clean energy transition is not a distant trend. It is an active, ongoing drain on the same supply that supports physical silver ownership.

This is what separates silver from every other wealth preservation metal on the market.

Its industrial-wealth duality is not a side note — it is the foundational reason the supply-demand math points in one direction. The physical float shrinks. The two-sided squeeze tightens.

And those who own the real thing hold something the factory floor cannot replace.

| Characteristic | Gold | Silver | What It Means for Owners |

|---|---|---|---|

| Primary Role | Monetary store of value — held in vaults, central bank reserves, and private ownership across centuries | Both monetary metal and irreplaceable industrial commodity — consumed permanently by manufacturing at industrial scale | Silver faces demand pressure from two directions simultaneously; gold does not |

| Industrial Consumption Rate | Minimal — the vast majority of gold ever mined still exists above ground in some form | Significant and permanent — industrial applications consume silver in ways that remove it from the available physical supply | Every ounce consumed by a solar panel or circuit board is an ounce that cannot be held, traded, or passed down |

| Supply Replenishment | Mine production adds to a large, stable above-ground stock — new supply has modest impact on total float | Mine supply is contracting while consumption accelerates — the physical float shrinks as demand from both industrial and ownership channels grows | A shrinking float with rising demand from multiple sources creates structural scarcity rather than cyclical price movement |

| Monetary Heritage | Thousands of years as the world's dominant monetary reserve — central banks hold gold as a primary reserve asset today | Thousands of years as circulating money and a store of value — silver coins served as everyday currency across civilizations | Both metals carry deep monetary credibility; silver's history as everyday money gives it broad recognition among owners worldwide |

| Substitutability in Key Applications | No industrial mandate requires gold — it can be held or released without competing against factory demand | No commercially viable substitute performs at silver's level for the same cost in solar, electronics, and automotive applications — manufacturers cannot simply switch | Industrial demand for silver is structurally locked in by technology and policy; it does not respond to price signals the way discretionary demand does |

| Wealth Preservation Profile | Widely held as a long-term store of value with deep institutional recognition and liquidity worldwide | Physical ownership offers the same long-term wealth preservation characteristics — with the additional dynamic that industrial consumption is permanently reducing the global supply available to owners | Owners of physical silver hold an asset whose available supply faces dual pressure that no other precious metal experiences at the same scale |

Why Most Precious Metals Buyers Miss the Industrial Story

Here's how most people find silver: the price is lower than gold. So they draw the obvious conclusion — silver is just the affordable version of the same thing.

That framing isn't wrong. But it is incomplete in a way that costs real money. The moment silver becomes a price-ratio play against gold, the factory floor disappears from the conversation — the permanent industrial consumption, the solar mandates drawing from the same finite supply. And that is the part of the story that actually changes the math.

The result is a fundamental misread of what silver actually is. Not a cheaper version of gold — a structurally different metal with a supply problem that industrial demand is actively widening. Global industrial silver demand is projected to reach a record 710.9 million ounces, a 9% increase that no price chart comparison with gold will ever show you.

The 'Cheaper Gold' Misread

The price relationship between gold and silver is real — and worth understanding. But treating that ratio as the primary reason to own silver means ignoring everything underneath it: the supply contraction, the industrial mandates, the permanent consumption eating into available ounces. For what that ratio actually measures — and what it doesn't — see the Gold-to-Silver Ratio.

Starting and ending with price turns silver into a spread trade. That is not how an owner thinks about a physical asset with permanent industrial consumption shrinking its available supply. Those are two entirely different decisions.

So what does the 'cheaper gold' framing cost the buyer who relies on it? Context. The context that explains why the two-sided squeeze exists at all. Mine supply is contracting. Industrial demand is at record levels. The physical deficit is projected at roughly 215.3 million ounces — the fourth consecutive year the market has consumed more silver than it has produced. None of that shows up in a price ratio.

Why Paper Silver Doesn't Solve the Problem

But here's the objection that comes up next: if physical silver is getting harder to source, why not just hold an ETF instead?

A silver ETF is a financial instrument. It is a claim on silver — not silver itself. It removes nothing from the industrial float. It gives the holder nothing physical to store, transfer, or pass down. And when the structural deficit tightens — when the factory floor and the vault genuinely compete for the same ounces — a claim on silver and an ounce of silver are not the same thing. Not even close.

Physical ownership is the point. Not exposure. Not a financial position. The industrial supply deficit driving silver's structural squeeze is a real-world phenomenon playing out in mining output and manufacturing order books — not in a brokerage account. Those who buy physical silver hold something the factory floor actually competes for. That distinction is the entire argument.

| Approach to Silver | What Buyers Assume | What the Supply Data Actually Shows | Risk to Wealth Preservation |

|---|---|---|---|

| Price-ratio play against gold | Silver is simply a cheaper version of gold — ownership is justified by the spread between the two metals | Silver's supply dynamics are structurally different from gold's — industrial consumption permanently depletes the physical float in ways gold's modest industrial use does not | Decisions made on price ratio alone ignore the structural supply deficit and the industrial mandates actively widening it |

| Paper silver / ETF exposure | A financial claim on silver provides the same outcome as holding the physical metal | A silver ETF is a financial instrument — it represents exposure to price movement, not ownership of an ounce that competes with industrial demand | When the physical float tightens, a claim on silver and an ounce of silver held outright are not equivalent — the ETF holder owns a position, not the metal |

| Commodity sentiment trade | Silver's value moves primarily with market sentiment, macro cycles, and investor appetite | Industrial mandates — energy policy, automotive electrification, solar deployment targets — drive structural consumption that operates independently of market sentiment | Treating silver as a sentiment-driven commodity misses the supply-side pressure that persists regardless of price cycles or macro conditions |

| Single-function monetary metal | Silver serves the same function as gold — a store of value outside the financial system — and the two metals can be evaluated on the same terms | Silver carries a full industrial role simultaneously with its monetary heritage — a dual-function profile no other precious metal holds at the same scale | Evaluating silver only through a monetary lens produces an incomplete picture of the supply dynamics that determine how much physical silver is actually available to own |

| Short-term price timing | The right moment to acquire silver is determined by where the price sits today relative to recent highs or lows | Mine supply is contracting while industrial consumption is at record levels — the structural deficit is a cumulative, multi-year phenomenon not visible in short-term price charts | Waiting for a more favorable price entry point treats silver as a trading instrument rather than a physical asset with a shrinking available float |

| Abundance assumption | Silver is a common metal — supply is elastic and will expand to meet any increase in demand | Global mine supply has contracted, not expanded, even as industrial demand has reached record levels — new mine development takes years and cannot respond quickly to demand surges | Assuming supply will normalize understates how long structural deficits can persist and how directly that persistence affects the physical availability of silver for ownership |

The Green Energy Mandate Is Rewriting Silver's Demand Floor

The green energy transition isn't a future event. It's happening right now — in manufacturing facilities, on rooftops, and on factory floors across every major economy at the same time.

Governments across the United States, Europe, and Asia have written clean energy targets into national law. Those targets don't live in a spreadsheet. They live in procurement contracts, manufacturing schedules, and installation timelines — and every one of those timelines requires silver.

That's what a structural demand floor looks like. Global industrial demand for silver — as documented by the U.S. Securities and Exchange Commission — is projected to hit a record 710.9 million ounces, a 9% increase driven by photovoltaic and automotive applications alone. That number isn't built on optimism. It's the mathematical consequence of mandates already signed into law.

Photovoltaic Solar: The Largest Single Driver of New Demand

Solar is now the single largest driver of new industrial silver demand. Photovoltaic silver consumption hit a record 193.5 million ounces in 2023 — a 64% jump from the prior year. That's not a gradual trend. That's acceleration.

So why does solar require this much silver? Because silver is the most electrically conductive metal on earth — and photovoltaic cells depend on that conductivity to operate at full efficiency. Clean energy transition technologies have pushed metal intensity to up to 20 milligrams of silver per watt of generating capacity. Multiply that across hundreds of gigawatts of planned global solar installation, and the consumption becomes structural — not cyclical.

Here's the detail that changes the supply math permanently: that silver isn't coming back. Solar panels aren't disassembled at end-of-life in any commercially meaningful volume that returns silver to the physical supply. The ounces consumed by photovoltaic manufacturing are, for all practical purposes, gone. Anyone pursuing a physical silver strategy needs to understand what that means — they're not competing with recycled supply. They're competing with a consumption pipeline that grows every year.

Automotive and Electronics: The Demand Layers Beneath Solar

Solar is the headline. But it's not the entire story. Automotive and electronics manufacturing add significant demand layers beneath it — and both are growing.

Electric vehicles require silver in electrical contacts, battery management systems, and onboard electronics. Conventional combustion vehicles already use it — but electrification multiplies the amount per unit significantly. The broader electronics sector — semiconductors, medical devices, industrial controls — draws on silver for the same reason solar does: its conductivity is irreplaceable at scale. The overall industrial demand projection of 710.9 million ounces reflects this compounding effect running across every sector at once.

What makes this multi-layer demand story consequential is its permanence. Solar mandates, vehicle electrification targets, and semiconductor expansion aren't policy experiments. They're infrastructure commitments measured in decades. Each layer adds to the industrial consumption baseline. Each year that baseline rises, the two-sided squeeze tightens further — mine supply contracting, the factory floor consuming more, and the physical float available to owners shrinking a little further.

| Industrial End-Use Sector | Primary Silver Application | Demand Trajectory | Substitutability |

|---|---|---|---|

| Photovoltaic (Solar) | Conductive paste in solar cells — silver enables electron flow from panel to grid | Record 193.5 million ounces consumed in 2023; 64% increase year-over-year | None at commercial scale — silver's electrical conductivity is irreplaceable in PV cells |

| Solar PV (Metal Intensity) | Silver paste applied at up to 20 milligrams per watt of generating capacity | Scales directly with every gigawatt of new solar installation mandated by policy | No commercially viable substitute — alternatives sacrifice efficiency at scale |

| Automotive & Electric Vehicles | Electrical contacts, battery management systems, onboard electronics | Contributing to record projected industrial demand of 710.9 million ounces | Silver's conductivity and thermal resistance make substitution technically prohibitive in safety-critical systems |

| Electronics & Semiconductors | Conductive pathways in semiconductors, medical devices, and industrial controls | Embedded within the 9% forecasted increase in overall industrial demand | No substitute delivers equivalent conductivity at the miniaturization scales modern chips require |

What the Supply Deficit Means for Physical Silver Owners

The two-sided squeeze isn't a theory. It has a number — and it's been getting larger every year.

The global silver market is now in its fourth consecutive year of structural physical deficit — with the projected shortfall reaching roughly 215.3 million ounces. The world consumed significantly more silver than it produced. Again. Not a one-time disruption. A pattern that has compounded year over year.

Here's what that number means if you're holding physical silver. A structural deficit doesn't fix itself through price movement. It fixes when supply catches up — or when demand pulls back. Right now, neither is happening. So the deficit compounds. And the way it was built tells you why it won't resolve quickly.

Four Consecutive Years of Structural Deficit

Four consecutive years of deficit — documented consistently by widening silver supply deficits tracked in U.S. Geological Survey reporting on global silver flows — is not a statistical anomaly. It is a structural condition. To bridge the gap between what mines produce and what industry consumes, the market has drawn down existing stockpiles and above-ground inventory. That inventory does not replenish itself.

The 215.3 million ounce projected deficit has a compounding quality that matters. Each year the market runs a deficit, the available physical float shrinks further. That float — the above-ground silver not already locked into industrial applications or institutional holdings — is exactly what physical owners and manufacturers are competing for at the same time. When it contracts, every ounce held outside the paper system becomes harder to replace.

Once the supply picture is clear, the choice of form — coins versus bars, liquidity versus storage efficiency — stops being a default. It becomes a real decision with real stakes. That context is what makes coins versus bars worth examining next.

Mine Supply Is Not Coming to the Rescue

Industrial demand is only one side of the squeeze. The other side — mine supply — is not compensating. Global silver mine production fell by 1% to 830.5 million ounces in 2023, according to the World Silver Survey. That contraction is happening at precisely the moment industrial consumption is setting records. Both sides of the equation are moving in the wrong direction — simultaneously.

The domestic picture doesn't offer an escape route. USGS silver supply data puts U.S. refined silver production at an estimated 1,000 metric tons in 2023. That's a narrow production base against global industrial consumption that's setting records. The U.S. isn't self-sufficient in silver. This is a global structural condition — not a regional imbalance that American mines can quietly close.

Here is what that means for physical owners directly. When mine supply contracts and industrial demand simultaneously hits record levels, the physical float available to non-industrial buyers is squeezed from both ends at once. That is the two-sided squeeze in its most concrete form. The factory floor does not pause while individuals decide whether to acquire. It simply consumes. And the supply that remains grows smaller.

| Supply-Demand Factor | Current Condition | Direction of Trend | Implication for Physical Owners |

|---|---|---|---|

| Structural Market Deficit | Fourth consecutive year of physical deficit, projected at roughly 215.3 million ounces | Widening — deficit has persisted and grown across multiple consecutive years | Above-ground physical float continues to shrink; each deficit year leaves fewer ounces available to non-industrial buyers |

| Global Mine Supply | Total mine production fell 1% to 830.5 million ounces in 2023 | Contracting — output declining at the moment industrial consumption hits record levels | Supply replenishment is failing to keep pace; the production base cannot close the deficit gap |

| Domestic U.S. Refined Production | Estimated at 1,000 metric tons in 2023 | Narrow — domestic output is a small fraction of global industrial consumption volumes | The U.S. is structurally dependent on global supply; domestic owners cannot rely on a domestic production buffer |

How to Think About Physical Silver as a Wealth Preservation Tool

So the question shifts.

Not what is happening to silver's supply — that's been established. The question now is what it means for someone who wants to hold the real thing. That requires a different frame.

Physical silver ownership is not a speculation on price direction.

It is an acquisition of a real, finite commodity that the factory floor actively competes to consume. The global silver market has run a structural deficit for four consecutive years — a shortfall projected at roughly 215.3 million ounces. That is not a backdrop for a trade. It is the context for ownership.

Those who hold real silver outside the paper system hold something a brokerage position cannot replicate.

The practical questions — how much to hold, in what form, through what vehicle — come after the framing. Not before.

That is exactly why Brighton Gold's silver educational guides are structured around the structural picture first. Understand the supply reality. Then make an ownership decision. Context before commitment.

Who Physical Silver Ownership Is Not For

Here's something worth saying directly: physical silver is not the right fit for every situation.

Brighton Gold does not soften that. It is part of how we work.

If the goal is short-term price exposure — buy today, sell in six months when the market moves — physical silver is the wrong vehicle.

Premiums, storage, and transaction logistics are not built for short holding periods. That is not what physical ownership is designed for, and it is not what Brighton Gold supports.

Similarly, if someone wants certainty — a guarantee that silver's value will rise, a promise that the deficit resolves in their favor — that certainty does not exist. Brighton Gold will not manufacture it.

Precious metals may appreciate, depreciate, or remain unchanged. What physical ownership provides is tangible, unencumbered access to a real commodity that the world's largest industrial sectors cannot stop consuming.

Photovoltaic silver demand alone reached a record 193.5 million ounces in 2023. The structural case for ownership is made by that number — not by anyone's forecast.

Coins, Rounds, and Bars: What Serious Owners Actually Hold

For owners who are in the right position to hold physical silver, the next question is form.

Coins, rounds, and bars each serve different priorities. That distinction is worth understanding before any purchase decision gets made.

Coins minted by the U.S. government — the Silver American Eagle, for example — carry immediate recognizability and broad liquidity. Buyers everywhere know what they are holding. That familiarity matters when it comes time to transact.

Rounds are privately minted and typically carry lower premiums over spot. They are efficient for owners who prioritize volume over brand recognition. Bars offer the best storage efficiency at scale.

And in a market running a structural deficit, every ounce held is real competition with the factory floor.

The right form depends on what the owner is trying to accomplish — storage logistics, near-term liquidity needs, and total quantity given their overall financial picture.

Brighton Gold works with customers who want to think through those specifics clearly, without pressure. That is exactly what a complimentary consultation is built for.

For anyone ready to move from the supply-demand picture to a concrete physical silver strategy, that conversation is the logical next step.

| Physical Silver Format | Liquidity Profile | IRA Eligibility | Typical Premium Range | Best Fit Owner Profile |

|---|---|---|---|---|

| U.S. Government-Minted Coins (e.g., Silver American Eagle) | Highest — universally recognized, trades easily across dealers and private buyers | Yes — IRS-approved for Precious Metals IRA on qualified purchases | Higher than rounds or bars — premium reflects government mint, legal tender status, and broad liquidity | Owners who prioritize ease of resale, broad recognizability, and IRA eligibility |

| Privately Minted Rounds | Moderate — recognized within the precious metals market but lacks government mint status | Generally not IRA-eligible — private mint rounds do not meet IRS purity and mint requirements | Lower than government coins — efficient for owners who prioritize volume acquisition over premium liquidity | Owners who want to maximize the amount of silver held per dollar spent and plan to store long-term |

| Silver Bars (various sizes) | Moderate to high depending on bar size and refiner reputation — larger bars may require assay verification on resale | Yes for qualifying bars — must meet IRS minimum purity standards and come from an approved refiner | Lowest per ounce — storage efficiency makes bars cost-effective at scale | Owners focused on storage efficiency and volume, comfortable with slightly more friction at point of resale |

| Paper Silver (ETFs, futures contracts) | High short-term trading liquidity — but ownership is a claim on silver, not physical possession | Varies by account structure — does not constitute physical metal ownership inside a Precious Metals IRA | No storage premium — but no physical silver is held; counterparty and institutional risk remain | Not aligned with Brighton Gold's ownership model — physical possession is the foundation of the wealth preservation case |

Frequently Asked Questions

The framework is useful. But the questions that keep people up at night are more specific than that.

Recession risk. Price volatility. Physical premiums. The green energy timeline. Those deserve straight answers.

These are the questions we hear most often — from people who've already worked through the supply-demand math and are now asking what it means for them personally.

How does rising industrial demand for silver affect its availability for physical wealth preservation?

Industrial demand doesn't just move the price. It moves the supply.

When factories, solar manufacturers, and automotive producers are consuming silver at record levels, they are drawing from the same above-ground float that physical owners rely on. Global industrial demand is projected to hit a record 710.9 million ounces — in a market where mine production is already contracting.

That float — the real, deliverable silver not yet locked into industrial use — shrinks with every year the structural deficit compounds. Acquiring physical silver outside the paper system means acquiring something the factory floor is simultaneously competing for.

Availability tightens as demand accelerates. That is not a theory. It is the supply math, in motion.

Why does silver's role in green energy technology make it a strategic long-term hold?

Green energy doesn't just use silver. It consumes it — permanently.

Solar panels, electric vehicles, and semiconductor components all require silver's conductivity. Once silver is embedded in those applications, it is not meaningfully recovered. Photovoltaic demand alone reached a record 193.5 million ounces in 2023 — a 64% increase from the prior year.

Government clean energy mandates are not reversing course. They are written into national law across the United States, Europe, and Asia — and every installation timeline they drive requires physical silver.

That means the structural pull on silver supply from green technology is not a short-term trend. It is a permanent, policy-driven feature of the market. Owners who hold physical silver hold a commodity that the world's fastest-growing energy infrastructure cannot function without.

Does industrial consumption of silver mean its price is more volatile than gold?

Yes — silver responds to both economic cycles and monetary conditions at the same time. Gold is overwhelmingly monetary. Silver carries industrial demand on top of that, which adds a layer of price complexity gold doesn't have.

But that dual structure also means industrial consumption creates a demand floor that doesn't vanish when financial markets get nervous. Factories still need silver. Solar installations still proceed. Automotive production slows in recessions — it doesn't stop.

The structural deficit — four consecutive years of shortfall projected at roughly 215.3 million ounces — is not a volatility story. It's a supply reality.

Price movement and float shrinkage are two separate conversations. Conflating them is exactly how the supply picture gets lost.

Can a global recession reduce industrial silver demand and hurt my wealth preservation plan?

A recession can slow some industrial silver applications. Automotive production softens. Some discretionary electronics pull back.

But it does not eliminate the structural deficit — and it does not reverse the green energy mandates driving photovoltaic demand. Solar installations continue to expand globally even in slower economic periods, because infrastructure commitments written into national policy do not pause for recessions.

Mine supply was already contracting before any recessionary pressure entered the picture. Global production fell by 1% to 830.5 million ounces in 2023. That contraction does not correct itself in a downturn.

A recession that temporarily softens one category of industrial demand does not offset four consecutive years of structural shortfall or rebuild the physical float projected at roughly 215.3 million ounces.

The two-sided squeeze eases at the margin in a downturn. It does not reverse.

How does the industrial supply deficit impact the physical premiums of silver coins and bars?

Premiums are not arbitrary. They are the market pricing the physical float in real time.

When structural deficits persist, refiners and mints are sourcing silver in a market where above-ground supply is being drawn down year after year. That increased competition for real, deliverable metal works its way into what physical owners actually pay when they acquire coins or bars.

Industrial silver demand projected at 710.9 million ounces — against a contracting mine supply base — doesn't stay abstract. It shows up at the point of acquisition.

The tighter the float, the more the physical premium reflects genuine scarcity. That is not a market inefficiency. That is the supply-demand math expressing itself in the most direct way possible: in the price of the real thing.

Physical Silver in a World That Can't Stop Using It

The two-sided squeeze doesn't resolve on its own.

Mine supply is contracting. Industrial consumption is at record levels. The physical float available to non-industrial owners shrinks with every year the deficit compounds.

That is not a forecast. That is the four-consecutive-year pattern of a structural market condition — documented, measurable, and no amount of paper silver can undo it.

Here's what makes silver different from everything else.

It's a monetary metal — thousands of years of wealth preservation history, held by civilizations that didn't trust the currency of their day. And it's an irreplaceable industrial commodity. Solar installations, electric vehicles, semiconductor fabrication — none of them have a substitute. Nothing else conducts electricity at that level, at that scale, for that cost.

Both things are true at the same time. The factory floor keeps consuming. The mines aren't keeping pace. And the physical float — the real, above-ground silver available to private owners — keeps shrinking.

That's the environment in which Brighton Gold works with customers who want to buy silver and hold something tangible that no brokerage account can replicate.

Precious metals may appreciate, depreciate, or remain unchanged.

What physical silver provides — in this supply environment, against this structural backdrop — is unencumbered ownership of a finite commodity the world cannot stop consuming. That's not a sales pitch. It's the supply-demand math, stated plainly.

Brighton Gold offers a complimentary consultation for anyone who wants to understand what that math means for their own situation. No pressure. No obligation. Just a clear picture of whether holding physical silver makes sense given where they are.

The two-sided squeeze is already in motion. The question is whether an owner is holding the thing the factory floor is competing for — or watching from the outside.

That math is already moving. The float is already shrinking. And the questions it raises — how much physical silver to hold, whether a No Fee Precious Metals IRA makes sense, what ownership actually looks like in practice — don't get clearer with time.

Brighton Gold offers a complimentary consultation to walk through exactly that. What the deficit picture means for your situation. Whether the No Fee Precious Metals IRA fits where you are. What the first step looks like. No pressure. No obligation. Just a straight conversation.