What Are the Best Silver Coins to Buy for Retirement Accounts?

The best silver coins for a retirement account are sovereign-minted, IRA-eligible bullion coins that meet the IRS fineness standard of 0.999 pure silver and qualify for custodian-administered holding under Section 408(m) of the Internal Revenue Code. The decision isn’t speculative. It’s structural — the form of ownership you choose determines what survives outside the paper banking system.

The U.S. American Silver Eagle is the most widely held option and the clearest standard. It contains 1 troy ounce of 99.9% pure silver, has been in continuous production since 1986, and carries a statutory exception granted directly by Congress under the Liberty Coin Act of 1985. That exemption isn’t a technicality — it’s an individual authorization that sets the American Silver Eagle apart from every other qualifying coin.

Two foreign coins also clear the IRS threshold. The Canadian Silver Maple Leaf is minted at 99.99% purity. The British Silver Britannia has been produced to 0.999 fineness since 2013. Both are accepted in self-directed Precious Metals IRAs when held through an approved custodian at an IRS-recognized depository.

All three coins meet the minimum eligibility bar. But meeting the bar and being the right choice aren’t the same thing. Liquidity, purity, sovereign backing, and long-term verifiability all shape what a coin is actually worth when conditions change.

Precious metals may appreciate, depreciate, or remain unchanged. What doesn’t change is the form of ownership — physical metal, held in your name, outside the paper banking system.

- Why IRA Silver Rules Exist — and What They Actually Require

- Why Most Dealers Get Silver Coin Selection Wrong

- The Best IRS-Approved Silver Coins for Retirement Accounts

- How to Hold IRA-Eligible Silver: Custody, Storage, and What Happens Next

- Frequently Asked Questions

- What makes a silver coin eligible for a Precious Metals IRA?

- Why is the U.S. American Silver Eagle the preferred coin for retirement accounts?

- Can I hold IRA-eligible silver coins at home?

- How do fees for a Silver IRA affect my retirement savings over time?

- Are there tax penalties when rolling over an existing 401(k) into physical silver?

- Is the Canadian Silver Maple Leaf or British Silver Britannia a good alternative to the American Silver Eagle?

- The Bottom Line on Silver Coins for Retirement

Why IRA Silver Rules Exist — and What They Actually Require

The IRS didn’t invent silver rules to be difficult. Retirement accounts come with real tax advantages — and Congress built real conditions around what earns those advantages.

Under Internal Revenue Code Section 408, physical gold and silver are classified as collectibles by default. Collectibles are prohibited inside IRAs — full stop. The entire framework that makes a Precious Metals IRA possible rests on statutory exemptions that carve specific coins and bullion out of that classification. If a coin doesn’t qualify for one of those exemptions, it doesn’t belong in the account.

That’s the only starting point that matters. A silver coin that doesn’t clear the statutory requirements isn’t a second-tier choice — it’s a disqualified asset that can trigger taxes and penalties the moment it enters the account. Knowing what clears the bar isn’t optional. It’s the whole question. physical silver retirement protection

The IRS Purity Standard and the Collectibles Trap

The IRS sets a minimum fineness of 0.999 for silver bullion held in a retirement account. That’s the line. A coin below that standard doesn’t qualify — no matter how it’s marketed, no matter how familiar the mint.

Here’s where the collectibles trap catches people. The IRS treats most coins and precious metals as collectibles under Section 408(m). Holding a collectible inside a traditional IRA is treated as a distribution in the year it’s acquired — taxable income, plus a potential 10% early withdrawal penalty if you’re under 59½. The fineness standard isn’t bureaucratic red tape. It’s the line between a legitimate retirement holding and an accidental taxable event.

The IRS rules for investing in individual retirement arrangements are unambiguous on this. Silver bullion that meets the 0.999 fineness standard clears the Section 408(m) exemption. Anything below that line doesn’t — full stop. Purity isn’t a minor spec buried in the fine print. It’s the threshold between a legitimate retirement holding and an accidental taxable event.

The American Silver Eagle Exception — and Why It Matters

The American Silver Eagle doesn’t just clear the purity bar — it has its own lane in the law. Congress authorized it under the Liberty Coin Act of 1985, and that authorization comes with something no fineness threshold can match: an individual statutory exemption written directly into the IRC. Other coins qualify because they meet a numerical standard. The American Silver Eagle qualifies because Congress named it — specifically, explicitly, and permanently.

That distinction matters more than it sounds. A coin that qualifies on a general purity standard is subject to regulatory interpretation — guidance updates, rule revisions, future clarifications that shift the ground beneath it. The American Silver Eagle — first released in 1986 and in continuous production since — rests on explicit Congressional authorization. That doesn’t move with regulatory trends. It’s the difference between qualifying for the account and being written into the law that governs it. When you’re deciding what sits beneath your retirement savings for the long haul, that difference is exactly the kind of thing that holds up. buy silver.

| IRS Requirement | Rule Detail | What Fails This Standard | Key Statutory Reference |

|---|---|---|---|

| Minimum Purity Standard | Silver bullion must meet a fineness of 0.999 or higher to qualify as an IRA-eligible asset | Coins minted below the 0.999 threshold — including older issues from historically recognized mints — regardless of their collectible or resale value | IRC Section 408(m)(3) |

| Collectibles Prohibition | Physical metals are classified as collectibles by default under the IRC; holding a disqualified asset inside an IRA triggers a deemed distribution in the year acquired | Numismatic coins, commemorative issues, and any silver product that does not meet a specific statutory or purity exemption | IRC Section 408(m)(1)–(2) |

| Statutory Exemption Requirement | A silver coin or bullion must qualify under a named statutory exemption — either through individual Congressional authorization or by meeting the IRS fineness standard — to escape the collectibles classification | Foreign bullion coins that meet purity standards but lack direct U.S. statutory authorization; silver rounds minted by private refiners without recognized sovereign backing | IRC Section 408(m)(3)(A)–(B) |

| Approved Custodian and Depository | IRA-eligible silver must be held by an approved, non-bank trustee or custodian and stored at an IRS-recognized depository — the account holder cannot take personal possession | Home storage arrangements; safe deposit box storage; any setup where the account holder directly controls the physical metal while it remains inside the IRA structure | IRC Section 408(a); IRS Publication 590-A |

| U.S. and State-Minted Coin Exception | Coins minted by the U.S. Treasury or by individual states under authority of federal law are explicitly exempted from the collectibles prohibition, provided they meet the applicable fineness or are named directly in the statute | Coins minted by foreign sovereigns that have not been individually named in U.S. tax law, even if widely traded and recognized internationally | IRC Section 408(m)(3)(A) |

Why Most Dealers Get Silver Coin Selection Wrong

Most dealers aren’t building your retirement. They’re building their margin.

That’s the honest starting point.

Here’s the part most articles skip: a coin can clear every IRS requirement and still be the wrong choice for retirement. Eligibility is the floor — not the finish line. What actually matters is liquidity, resale recognition, and whether any reputable dealer will price that coin fairly the day you need to move it.

The American Silver Eagle clears every one of those bars. It’s 99.9% pure silver, sovereign-backed by the U.S. government, and universally recognized across the secondary market. Most of what gets pushed as an alternative doesn’t come close to that combination. Why American Silver Eagles are the standard

The High-Margin Proof Coin Problem

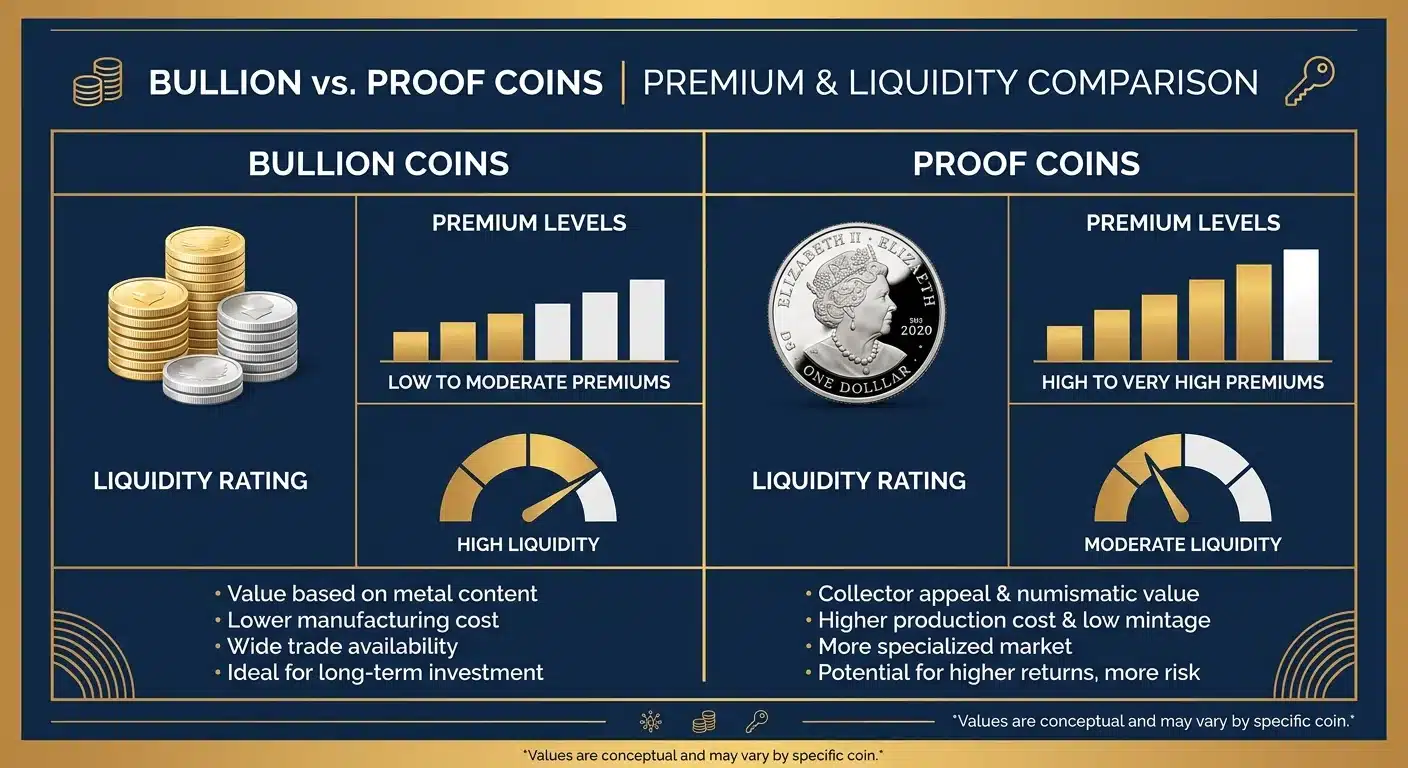

Here’s what the play looks like. A dealer recommends a proof coin or a limited-edition foreign issue. The premium over spot is significantly higher — which means a larger margin for the dealer. The coin clears the 0.999 fineness threshold, so it technically qualifies. The customer has no reason to question it.

The problem shows up later — sometimes years later. Proof coins and numismatic issues carry premiums built on collectibility, not silver content. When it’s time to sell or transfer, that collectibility premium often disappears entirely. You’re left holding a coin worth its silver weight — but you paid significantly more than that to acquire it.

That gap between acquisition cost and resale value isn’t a minor inefficiency. It’s structural erosion — and it compounds over time. The form of ownership you choose determines what survives outside the paper banking system. A high-premium proof coin is still physical metal. But it’s physical metal you overpaid for, in a form the secondary market doesn’t reward.

Bullion coins like the American Silver Eagle — 1 troy ounce of 99.9% pure silver — trade on metal content and sovereign backing. That’s what creates real liquidity. Their value is transparent, verifiable, and recognized by any dealer in the market. That’s the standard worth owning. Brighton Gold’s learning center covers exactly why that distinction matters for long-term owners.

Who This Section Is Not Written For

This section isn’t for the buyer who wants to trade silver positions every quarter or time purchases around spot price movements. That’s a different relationship — and it isn’t what Brighton Gold is built for.

If the question is “which coin gives me the best return this quarter” — this isn’t the right framework. Brighton Gold doesn’t forecast prices, time the market, or recommend coins based on near-term performance. Those aren’t services we offer. And honestly, no one can deliver them reliably.

What this section is written for is the customer who wants to know what to hold for the long term, why certain coins are structurally superior for retirement accounts, and how to avoid the margin-driven recommendations that quietly erode what you’ve built. If that’s where you are — keep reading.

| Coin Type | Typical Premium Over Spot | Resale Liquidity | IRA Eligible | Who It Benefits Most |

|---|---|---|---|---|

| Sovereign Bullion Coin (e.g., American Silver Eagle) | Low to moderate — priced close to spot with a standard premium reflecting minting and distribution costs | High — universally recognized by dealers and secondary market buyers; easy to verify and price | Yes — meets the 0.999 fineness threshold and, in the case of the American Silver Eagle, carries an individual Congressional exemption | The long-term retirement owner who prioritizes liquidity, resale transparency, and structural security over novelty |

| Proof or Collectible Coin | High — premium reflects collectibility, limited mintage, or aesthetic finish rather than silver content alone | Variable and often low — collectibility premium frequently disappears at resale; value depends on market demand for that specific issue | Technically eligible if purity meets the 0.999 threshold, but the collectibility premium is not recoverable — and proof coins can blur the line with numismatic restrictions | The dealer — higher margin on the sale; the customer typically absorbs the cost of an inflated premium that silver content alone cannot support |

| Foreign Bullion Coin (e.g., Silver Maple Leaf, Silver Britannia) | Low to moderate — comparable to sovereign bullion; premium reflects sovereign mint origin and purity guarantee | Moderate to high — well-known foreign issues are generally recognized, but resale depth is narrower than U.S.-minted coins in the domestic market | Yes — if purity meets the 0.999 threshold; no individual statutory exemption, so eligibility rests entirely on meeting the general fineness standard | Owners who prioritize purity options or geographic diversification of physical holdings — a reasonable secondary choice, not the structural first choice |

| Generic or Private Mint Round | Low — priced near spot with minimal brand recognition premium | Low — not recognized as sovereign coinage; resale requires more scrutiny from buyers; pricing is less consistent across dealers | Only if purity meets 0.999 — no sovereign backing, no statutory exemption, and no guarantee of custodian acceptance in a Precious Metals IRA | Buyers focused purely on acquiring silver by weight at the lowest cost; structurally unsuitable for retirement accounts where liquidity and custodian acceptance matter |

| Numismatic Coin | Very high — premium reflects historical significance, condition grading, and collector demand entirely independent of silver content | Unpredictable — value depends on collector market conditions, not on silver spot price or sovereign recognition | Generally no — numismatic coins are typically treated as collectibles under IRC Section 408(m) and do not qualify for Precious Metals IRAs | Coin collectors and dealers who benefit from high margins; not appropriate for retirement accounts regardless of the silver content |

The Best IRS-Approved Silver Coins for Retirement Accounts

Three sovereign-minted coins clear the IRS threshold and belong in a serious conversation about retirement ownership — the U.S. American Silver Eagle, the Canadian Silver Maple Leaf, and the British Silver Britannia. Each meets the 0.999 fineness requirement. Each comes from a government mint. But they aren’t interchangeable — and the differences matter more than most owners realize.

This isn’t a purity comparison. It’s a question about what kind of ownership you’re building beneath your retirement savings. The form you choose determines what survives outside the paper banking system — and that question applies just as directly to silver coins vs. silver bars.

So here’s the breakdown — purity, IRS standing, liquidity, and what a long-term owner should understand before choosing one.

U.S. American Silver Eagle — The Sovereign Standard

The American Silver Eagle isn’t just the most recognized silver coin in the United States. It’s the only one written into the Internal Revenue Code by name. That’s not a marketing claim — it’s a statutory fact. Every other qualifying coin earns IRA eligibility by meeting the 0.999 fineness threshold. The American Silver Eagle holds an individual exemption under IRC Section 408(m)(3) that exists entirely independent of general purity rules. Congress authorized it directly. That’s a different kind of standing.

The U.S. Mint’s specifications for American Eagle bullion are unambiguous: 1 troy ounce of 99.9% pure silver, nominal face value of $1 — legal tender backed by the full faith of the U.S. government. That face value detail isn’t incidental. It’s sovereign backing in a form no foreign coin can replicate. For retirement owners who want something universally recognized, immediately liquid, and structurally uncomplicated — this is the standard.

Secondary market recognition matters as much as IRS eligibility. The American Silver Eagle is recognized by virtually every reputable dealer in the country. When it’s time to sell, exchange, or transfer, there’s no verification friction. That transparency is what long-term ownership should rest on. And it’s why American Silver Eagles the standard isn’t just a phrase — it’s a structural reality.

Canadian Silver Maple Leaf — The High-Purity Alternative

The Canadian Silver Maple Leaf is the highest-purity sovereign silver coin available for IRA ownership. The Royal Canadian Mint’s 99.99% pure Maple Leaf is struck at 0.9999 fine silver — a meaningful margin above the IRS minimum. The Royal Canadian Mint has produced this coin since 1988, building decades of international secondary market recognition. That purity record is real, and it’s earned.

That 0.9999 fineness is a legitimate differentiator. For some owners, it matters. The Maple Leaf also trades well internationally — which becomes relevant when long-term ownership includes cross-border exchange or transfer scenarios. It’s a strong coin. But whether its strengths fit your specific ownership structure is a different question.

Here’s the honest trade-off: the Maple Leaf is a foreign-minted coin. It qualifies under the IRS purity standard. But it doesn’t carry the Congressional authorization the American Silver Eagle holds. For domestic retirement accounts built around long-term U.S.-based ownership, that distinction is worth weighing. The Canadian Silver Maple Leaf is a strong choice — but it’s a secondary standard. Not the primary one.

British Silver Britannia — The European Sovereign Option

The British Silver Britannia has been minted at 0.999 fine silver since 2013 — an upgrade from its previous 0.958 standard that brought it into IRS compliance for retirement accounts. The Royal Mint’s Silver Britannia specifications confirm both the current fineness and the historical transition. It’s a sovereign-minted coin backed by the British government, with strong recognition across European and international markets. That upgrade matters — but so does what it doesn’t change.

For U.S.-based retirement accounts, the British Silver Britannia qualifies — but its domestic secondary market liquidity runs thinner than either the American Silver Eagle or the Canadian Maple Leaf. It’s the right coin for an owner with specific reasons to hold a European sovereign issue. For most retirement accounts built around long-term domestic ownership, it sits third. Behind a coin that rests on Congressional authorization. And behind one that leads on purity.

| Coin Name | Country of Origin | Silver Purity | Weight | IRA Eligible | Notable Feature |

|---|---|---|---|---|---|

| U.S. American Silver Eagle | United States | 99.9% (0.999 fine) | 1 troy ounce | Yes — statutory exemption under IRC §408(m)(3) | Only coin named individually in the Internal Revenue Code; legal tender backed by U.S. government |

| Canadian Silver Maple Leaf | Canada | 99.99% (0.9999 fine) | 1 troy ounce | Yes — exceeds 0.999 fineness threshold | Highest purity of the three leading IRA-eligible sovereign silver coins; introduced by the Royal Canadian Mint in 1988 |

| British Silver Britannia | United Kingdom | 99.9% (0.999 fine) | 1 troy ounce | Yes — meets 0.999 fineness threshold since 2013 | Upgraded from 0.958 fineness in 2013; sovereign-minted by the Royal Mint with strong international market recognition |

How to Hold IRA-Eligible Silver: Custody, Storage, and What Happens Next

Knowing which coins qualify gets you halfway there. The other half is custody — and getting that wrong unwinds the entire structure just as fast as buying a disqualified coin.

Here’s the rule that surprises most people: you can’t buy IRA-eligible silver coins and store them in a home safe. That isn’t an IRA — it’s a taxable distribution waiting to happen. Under Section 408(m) of the Internal Revenue Code, physical metals inside a retirement account must be held by an approved custodian, at an approved depository. That structure isn’t bureaucratic overhead. It’s what keeps the tax-advantaged status of your account intact.

Some customers arrive having never heard the word custodian in this context. Others have heard it and decided the complexity makes the whole thing impractical. Both assumptions are wrong — and both end up costing people a structure they could have had. Sort out what custody actually looks like, and what it costs over time, before you acquire a single coin.

The Custodian Requirement — What It Means and Why It Exists

The IRS doesn’t allow self-custody of IRA-eligible silver — and the reason isn’t arbitrary. Tax advantages attached to a retirement account require independent oversight. An approved custodian holds the account on your behalf, maintains the legal records, and verifies that everything inside meets the statutory requirements under IRC Section 408(m) — codified in full at Internal Revenue Code Section 408. You don’t manage the account directly. That’s the point — and it’s what keeps the structure legally sound.

That custodian works alongside an approved depository — a secured, insured facility where your physical metals are vaulted in your name. You own the metal. The depository holds it. The custodian documents it. Owner, custodian, depository — that three-part structure is what makes a Precious Metals IRA legally sound. Each layer has a defined role. None of them are optional.

Here’s what most articles skip: the custodian requirement isn’t a drag on the system. It’s what separates physical ownership inside a retirement account from every paper instrument surrounding it. Your metals aren’t a line item on a brokerage statement. They’re vaulted assets held in your name, with documented custody. That distinction is exactly what this structure is built around — and it’s the one that holds up when the paper system doesn’t.

The Brighton Gold No-Fee Precious Metals IRA Structure

Brighton Gold’s No Fee Precious Metals IRA is built around one structural commitment: the fees most firms layer onto IRA accounts — annual custodian fees, storage fees, administrative charges — don’t apply for the lifetime of the account on qualified purchases. That’s not a promotional offer with an expiration date. It’s a decision about what kind of relationship this is — and it changes the long-term math of what you’re actually holding.

The process itself isn’t complicated. You open a self-directed IRA. Fund it — through a new contribution, a transfer from an existing IRA, or a rollover from a qualified retirement plan. Select your IRA-eligible silver coins. The metals are purchased and vaulted at an approved depository in your name. Brighton Gold guides every step — before the acquisition, through the transaction, and after. That’s what a concierge experience actually means in practice.

What you’re building isn’t a position you’ll trade out of next quarter. It’s a layer of physical ownership — sovereign-backed, custodied in your name, sitting entirely outside the paper banking system. Every IRS rules for investing in individual retirement arrangements requirement, every IRC Section 408(m) restriction, every 0.999 purity threshold, every custodian structure covered here exists for the same reason. The form of ownership you choose determines what survives outside the paper banking system. That’s the payoff for getting the structure right — not price performance, not timing, not a coin’s aesthetic appeal.

Silver Coins vs. Silver Bars: Which Is Right for Your Retirement Account?

The coin-versus-bar question comes up early in almost every retirement silver conversation — and it deserves a direct answer. Both formats meet the IRS minimum fineness of 0.999 when properly certified. But the structural differences between them show up in liquidity, secondary market recognition, and what happens when it’s time to sell or transfer. Those differences matter more than most people expect when they’re first asking the question.

Sovereign-minted coins — the American Silver Eagle most of all — carry instant secondary market recognition. Any reputable dealer knows exactly what they are, how to price them, and how to verify them on sight. Bars require assay verification in many secondary market transactions. That adds friction to what should be a transparent process. For retirement owners focused on long-term liquidity, coins typically serve the structure better — and that’s the case Brighton Gold makes when the silver coins vs. silver bars question comes up.

One more question worth sitting with before you lock in your format: how silver’s price behavior fits the structure you’re building. Form and custody aren’t separate decisions from volatility — they’re part of the same one. If that context belongs in your picture before you commit, start with silver’s price behavior.

| Ownership Step | What Happens | Who Is Responsible | Typical Timeframe |

|---|---|---|---|

| Open a Self-Directed IRA | A custodian-held self-directed IRA is established in your name — separate from any existing brokerage or employer-sponsored account | You and your chosen custodian | Completed before any metals acquisition begins |

| Fund the Account | The account is funded through a new contribution, a direct transfer from an existing IRA, or a rollover from a qualified retirement plan | You, your current plan administrator, and the custodian | Varies by funding method — transfers and rollovers require coordination between institutions |

| Select IRA-Eligible Silver Coins | IRA-approved coins are chosen based on IRS fineness requirements — only sovereign-minted coins meeting the statutory standard qualify | You, guided by Brighton Gold | Completed once funding is confirmed and account is active |

| Purchase and Vault the Metals | Brighton Gold executes the acquisition; metals are shipped directly to an IRS-approved depository and vaulted in your name | Brighton Gold and the approved depository | Typically completed within a short window after purchase confirmation |

| Ongoing Custodial Oversight | The custodian maintains legal account records, documents your holdings, and ensures ongoing IRS compliance for the account | Your custodian, on your behalf | Continuous — for the lifetime of the account |

| Sell, Transfer, or Distribute | When you are ready to liquidate or take a distribution, the custodian and depository coordinate the release or transfer of your physical metals | You, your custodian, and the depository | Initiated at your direction — timing depends on your instructions and market conditions |

Frequently Asked Questions

These are the questions that surface after the research — after the IRS rules land, after the coin comparisons sink in, and before anything is signed.

Direct answers. No hedging. No language designed to protect the writer instead of inform the reader.

What makes a silver coin eligible for a Precious Metals IRA?

The IRS sets a minimum fineness of 0.999 for silver bullion in a retirement account. That’s the threshold. The coin must also come from a government mint or an approved refiner — not a private one.

There’s one exception worth understanding. The U.S. American Silver Eagle qualifies under IRC Section 408(m)(3) regardless of its fineness. Congress authorized it by name. Other coins — Maple Leafs, Britannias — earn eligibility by clearing the 0.999 bar. The Eagle clears it and holds a legal backstop no other coin carries.

That distinction matters. One coin’s eligibility rests on a purity standard. The other’s rests on an act of Congress.

Why is the U.S. American Silver Eagle the preferred coin for retirement accounts?

Three things — and they don’t overlap with any other qualifying coin.

First: an explicit Congressional authorization under IRC Section 408(m)(3). Its IRA eligibility isn’t contingent on hitting a purity threshold. It’s written into the law by name.

Second: 1 troy ounce of 99.9% pure silver, minted by the U.S. Mint. Sovereign-backed. No ambiguity about what’s inside it.

Third: secondary market recognition that nothing else matches domestically. Any reputable dealer knows exactly what it is. Pricing it requires no friction, no verification delay, no explanation.

Legal standing, sovereign provenance, and liquidity — that combination is why it’s the primary standard.

Can I hold IRA-eligible silver coins at home?

No. Not legally — not without consequences.

Under Section 408(m) of the Internal Revenue Code, IRA-eligible metals must be held by an approved custodian at an approved depository. Storing retirement silver at home — even in a serious safe — disqualifies it from IRA status the moment it’s removed from approved custody.

The IRS treats that as a taxable distribution. The full value of the metals becomes taxable income in the year of the removal. If you’re under 59½, a 10% early withdrawal penalty applies on top of that.

The custodian-and-depository structure isn’t optional overhead. It’s the legal architecture that keeps the account’s tax-advantaged status intact.

How do fees for a Silver IRA affect my retirement savings over time?

They compound quietly — and that’s the part most people miss.

Annual custodian fees, storage charges, administrative costs. None of them feel significant in year one. Over a long holding period, they erode what you actually own. The structure around the account matters as much as the coins inside it.

Brighton Gold’s No Fee Precious Metals IRA eliminates those recurring charges for the lifetime of the account on qualified purchases. That’s not a promotional offer. It’s a structural commitment — one that changes the long-term math of what you’re holding.

The right coin gets you in. The fee structure determines what stays.

Are there tax penalties when rolling over an existing 401(k) into physical silver?

A properly executed rollover doesn’t trigger taxes or penalties. That phrase — properly executed — is doing a lot of work.

The IRS requires funds to move directly from the qualified retirement plan to the self-directed IRA custodian. That’s called a direct rollover or trustee-to-trustee transfer. The money never touches your hands.

If it does — if funds are distributed to you personally first — a 60-day window applies. Miss it, and the full amount is treated as a taxable distribution. Income taxes apply. If you’re under 59½, the 10% penalty applies too.

Brighton Gold walks customers through the rollover process before anything is signed. The mechanics are clear before any funds move.

Is the Canadian Silver Maple Leaf or British Silver Britannia a good alternative to the American Silver Eagle?

Both qualify. Neither is the primary standard.

The Canadian Silver Maple Leaf clears the 0.999 fineness requirement and exceeds it — the Royal Canadian Mint produces it at 0.9999 fine. That purity record is real. It’s a strong secondary choice, with solid international secondary market recognition.

The British Silver Britannia meets the 0.999 standard and is sovereign-minted. For owners with specific reasons to hold a European sovereign issue, it belongs in the conversation.

For U.S.-based retirement accounts built around long-term domestic ownership — the U.S. American Silver Eagle holds legal standing neither coin can replicate. Congressional authorization under IRC Section 408(m)(3) isn’t something a purity standard alone provides.

They’re not wrong choices. But the hierarchy isn’t arbitrary — and for most retirement owners, the Eagle is where the structure starts.

The Bottom Line on Silver Coins for Retirement

Everything here traces back to one question — not which coin has the best premium this quarter, but what kind of ownership you’re actually building.

The 0.999 fineness threshold isn’t bureaucratic noise. The Congressional authorization behind the American Silver Eagle isn’t a footnote. The custodian structure, the approved depository, the fineness requirements — they exist for one reason.

The form of ownership you choose determines what survives outside the paper banking system. That’s the thesis. You’ve now seen exactly how it holds.

The American Silver Eagle is the standard. 1 troy ounce, 99.9% pure, sovereign-minted, Congressionally authorized, recognized by every reputable dealer in the country. That combination isn’t an accident — it’s four decades of legal standing made liquid.

The Canadian Silver Maple Leaf earns its place as a strong secondary choice on purity alone. The British Silver Britannia qualifies — and for specific ownership situations, it’s the right call.

But the hierarchy isn’t arbitrary. It reflects liquidity, legal standing, and what the secondary market actually does when it’s time to act. The coins you choose at the start determine how much friction you face at every stage that follows.

Physical silver held in a properly structured retirement account — sovereign-backed, custodied in your name, sitting entirely outside the paper banking system — isn’t a speculative position. It’s a structural decision.

Brighton Gold’s No Fee Precious Metals IRA is built around that conviction. The right coins. The right custody. And a relationship that doesn’t end when the transaction does.

Precious metals may appreciate, depreciate, or remain unchanged. What doesn’t change is the form of ownership. If this structure still makes sense for where you are, the next step is a conversation — not a commitment.

You’ve done the research. Now the question is whether the structure holds up for your specific situation — your existing accounts, your timeline, your goals. Brighton Gold offers a complimentary consultation to walk through exactly that. Including how the No Fee Precious Metals IRA works, what qualifies, and whether it fits where you are right now. Learn About the No Fee Precious Metals IRA Most customers leave that conversation with more clarity than they expected. That’s the point.