Gold IRA Withdrawal Rules: What Happens When You Take Money Out? (2026)

If you’ve spent years building a Gold IRA, there’s a question you’ll eventually need to answer — how do you actually take money out?

It’s simpler than most people expect. But the rules do matter. And getting them wrong can cost you thousands in penalties you didn’t need to pay.

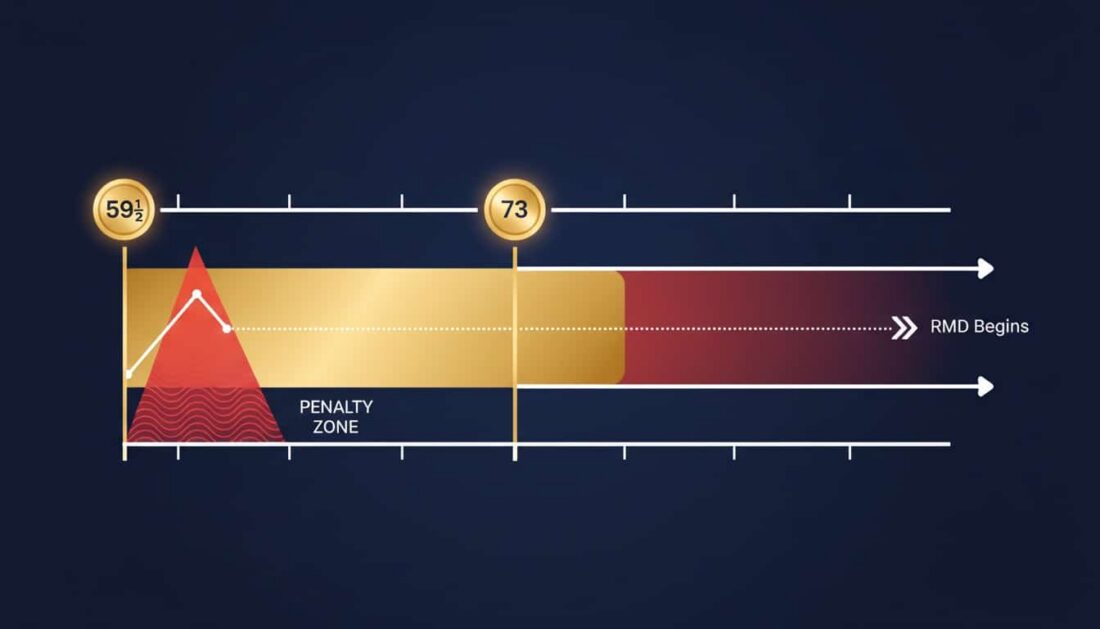

Here’s the short version: after age 59½, you can withdraw without penalty. Before that, you’ll likely owe a 10% early withdrawal penalty plus income tax. At age 73, the IRS says you must start taking money out — whether you want to or not.

What most owners don’t realize? You don’t have to sell your gold to take a distribution. You can have the actual coins or bars shipped right to your door. It’s called an “in-kind” distribution — and it’s one of the features that makes a Gold IRA different from any other retirement account.

Whether you’re understanding gold IRA distribution options for the first time or you’re getting close to your first Required Minimum Distribution, this guide walks you through every rule that matters in 2026 — clearly and without the jargon.

The Two Age Thresholds Every Gold IRA Owner Needs to Know

Two ages matter more than anything else when it comes to your Gold IRA — 59½ and 73.

Everything about your withdrawal strategy — the taxes, the penalties, the timing — traces back to where you fall between those two numbers.

Age 59½ — The Penalty-Free Line

Once you turn 59½, you can take distributions from your traditional Gold IRA without the 10% early withdrawal penalty.

You’ll still owe ordinary income tax on whatever you pull out. That doesn’t change. But the extra penalty? Gone.

This works the same way it does for any traditional IRA. The IRS doesn’t treat Gold IRAs differently here. Your metals are tax-deferred — and distributions are taxed as ordinary income when they come out.

Here’s what that looks like at each stage:

- Before 59½ — You’ll owe income tax plus a 10% early withdrawal penalty on most distributions. There are exceptions — but the default rule is clear.

- Between 59½ and 73 — This is what we’d call the optional window. You can take distributions whenever you want, in any amount, penalty-free. There’s no requirement to withdraw anything. Many owners use this window to pull metals or cash during lower-income years — reducing their overall tax hit.

- At 73 and beyond — Required Minimum Distributions kick in. The IRS requires you to start withdrawing, ready or not.

Age 73 — When Withdrawals Become Mandatory

Under the SECURE Act 2.0, the RMD age shifted to 73 for anyone born between 1951 and 1959. Born in 1960 or later? Your RMD age moves to 75, starting in 2033.

Your first RMD is due by April 1 of the year after you turn 73. Every one after that? December 31 of each year.

Now — here’s where Gold IRA owners need to pay closer attention than most.

Your account holds physical metals. Not cash. Not paper holdings that sell with a click. Selling gold or silver, processing the paperwork, and getting the funds out takes time. So don’t wait until late December to start the process. Give yourself — and your custodian — room to work.

Cash Distribution vs. In-Kind Distribution — Your Two Options

When it’s time to take money out of your Gold IRA, you’ve got a choice most people don’t know they have.

You can take cash. Or you can take the actual gold.

Each path works differently — and each creates a different outcome for your taxes, your timeline, and your control over the metals.

How Cash Liquidation Works

Cash is the more straightforward route. Here’s how it plays out:

- Step 1 — You contact your custodian and request a distribution for a specific dollar amount.

- Step 2 — The custodian sells enough metals from your account to cover that amount at the current market price.

- Step 3 — The cash is wired to your bank or mailed as a check. Most custodians complete this in 3 to 5 business days.

- Step 4 — Your custodian reports the distribution on Form 1099-R, which you’ll use at tax time.

The fair market value at the time of sale determines what’s taxable. If gold is trading around $5,000 per ounce and your custodian sells two ounces, that’s $10,000 in taxable income for the year.

How In-Kind Distribution Works

An in-kind distribution means you receive the actual physical metals — the coins or bars themselves — instead of cash.

This is what makes Gold IRAs unlike any other retirement account.

Here’s the process:

- Step 1 — You tell your custodian which metals you want delivered.

- Step 2 — The custodian determines the fair market value of those metals on the distribution date. Most use the LBMA Gold Price PM fix or COMEX closing prices as the benchmark.

- Step 3 — The metals ship from the depository to your home — or to a private storage location you choose.

- Step 4 — The custodian reports the FMV as a taxable distribution on Form 1099-R — even though you never received cash.

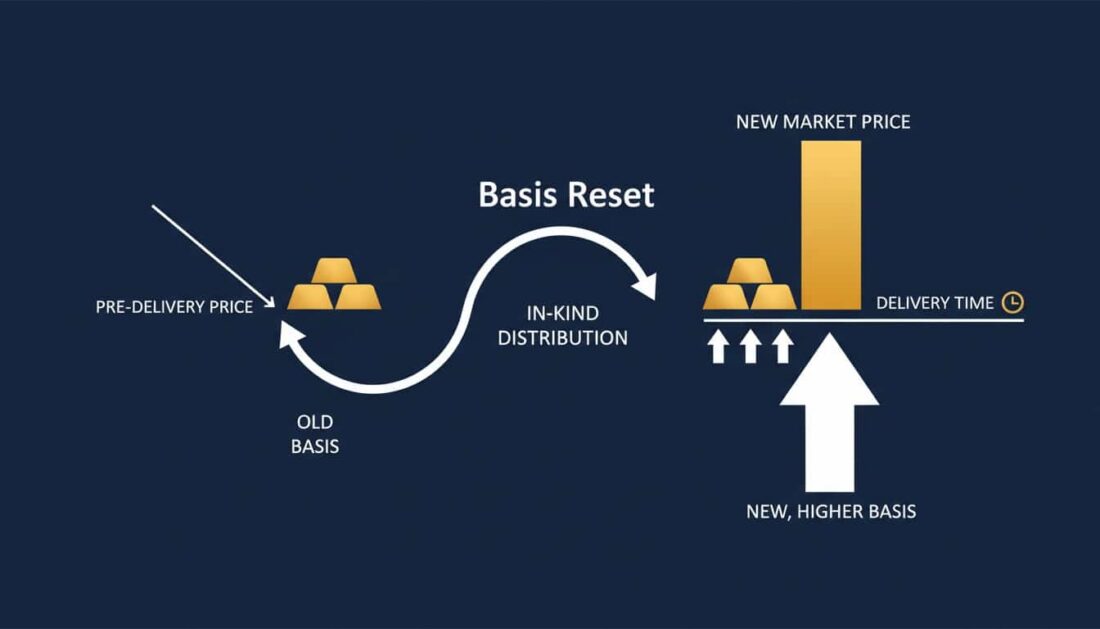

Here’s the part that catches people off guard. When you take an in-kind distribution, the FMV on the distribution date becomes your new cost basis for those metals.

That’s called a “basis reset.” We’ll cover why it matters — and why it can actually work in your favor — a little later.

Comparing Your Two Options

| Cash Liquidation | In-Kind Distribution | |

|---|---|---|

| What You Receive | Cash (check or wire) | Physical coins or bars |

| Processing Time | 3-5 business days | 5-10 business days (includes shipping) |

| Taxable Amount | Sale price of metals | FMV on distribution date |

| Cost Basis | Not applicable (you received cash) | FMV on distribution date becomes new cost basis |

| Delivery Fees | None (standard distribution) | Shipping and insurance costs may apply |

| Ongoing Position | You no longer hold the metals | You maintain physical ownership outside the IRA |

So which one’s right for you?

If you need cash for living expenses or an RMD — cash liquidation keeps it simple. If you want to keep holding physical gold or silver outside of a tax-deferred account — maintaining control while meeting your distribution requirements — in-kind delivery is worth a closer look.

Early Withdrawal Penalties and the Exceptions That Matter in 2026

What happens if you need to access your Gold IRA before 59½?

The short answer — it’s expensive. You’ll typically owe a 10% early withdrawal penalty on top of ordinary income tax.

But the IRS does recognize situations where the penalty doesn’t apply. And the SECURE Act 2.0 added a new one that took effect after December 31, 2023.

The Standard 10% Penalty

Say you’re 52 and take a $10,000 cash distribution from your traditional Gold IRA.

Here’s what that costs:

- Ordinary income tax — The full $10,000 gets added to your taxable income. In the 22% bracket, that’s $2,200 in federal tax.

- 10% early withdrawal penalty — Another $1,000.

- Total hit — Roughly $3,200 on a $10,000 withdrawal — and that’s before state taxes.

That’s a steep price. It’s why early withdrawals are generally a last resort.

Exceptions to the 10% Penalty

The IRS waives the 10% penalty in several situations. You’ll still owe income tax — but the extra penalty goes away.

- Permanent disability — If you’re totally and permanently disabled as the IRS defines it, distributions are penalty-free.

- Substantially Equal Periodic Payments (SEPP) — Under IRS Rule 72(t), you can set up equal payments based on your life expectancy. These must continue for at least five years or until you reach 59½ — whichever comes later.

- Unreimbursed medical expenses — If your out-of-pocket medical costs top 7.5% of your adjusted gross income, you can withdraw up to that excess amount without the penalty.

- First-time home purchase — Up to $10,000 (lifetime limit) for buying, building, or rebuilding a first home.

- Health insurance while unemployed — If you’ve received at least 12 straight weeks of unemployment compensation, withdrawals for health premiums avoid the penalty.

- IRS levy — If the IRS levies your IRA directly, the distribution is exempt from the penalty.

Do any of these apply to you? If so, you’ll want to file Form 5329 with your tax return to claim the exception.

The New SECURE Act 2.0 Emergency Exception

This one’s new — and it’s worth knowing about.

Starting in 2024, the SECURE Act 2.0 created a penalty-free emergency expense distribution of up to $1,000 per calendar year.

Here’s how it works:

- You self-certify the emergency — No paperwork or proof required for your custodian. The expense just needs to be unforeseeable or immediate.

- One per year — Only one emergency distribution is allowed each calendar year.

- Three years to repay — If you put the money back, you can claim a refund on any taxes paid.

- Limits on repeats — You can’t take another emergency distribution within three years unless you’ve repaid the first one — or made contributions equal to the amount you withdrew.

It’s not a large amount. But it’s a pressure valve. If an unexpected expense comes up, you’ve got a way to access funds without destroying your retirement position.

2026 Early Withdrawal Penalty Summary

| Scenario | Income Tax | 10% Penalty | Notes |

|---|---|---|---|

| Under 59½, no exception | Yes | Yes | Standard early distribution rules |

| Under 59½, permanent disability | Yes | No | Must meet IRS disability definition |

| Under 59½, SEPP (Rule 72t) | Yes | No | Payments must continue 5+ years or until 59½ |

| Under 59½, medical expenses >7.5% AGI | Yes | No | Only the amount exceeding 7.5% qualifies |

| Under 59½, SECURE 2.0 emergency | Yes | No | Up to $1,000/year, self-certified |

| Age 59½ or older | Yes | No | Penalty-free, income tax always applies |

| Roth IRA contributions | No | No | Contributions can be withdrawn anytime tax-free |

How Required Minimum Distributions Work with Physical Gold

If you’re turning 73 this year — or you will soon — this section is for you.

RMDs are straightforward in concept. The IRS requires you to withdraw a minimum amount each year from your traditional retirement accounts, including your Gold IRA. But navigating mandatory gold IRA withdrawals gets a little more involved when your account holds physical metals instead of cash.

The RMD Calculation

The formula itself is simple:

Account Balance (December 31 of prior year) ÷ Life Expectancy Factor = Your RMD

The life expectancy factor comes from the IRS Uniform Lifetime Table in Publication 590-B.

Here’s a quick example. Say your Gold IRA was valued at $200,000 on December 31, 2025, and you turn 73 in 2026. The IRS table assigns a distribution period of 26.5 for age 73.

$200,000 ÷ 26.5 = $7,547

That’s your minimum withdrawal for the year. You can always take more — but never less.

RMD Amounts by Age

How does the required amount change as you get older? Here’s a look:

| Age | Distribution Period | RMD on $200,000 Balance |

|---|---|---|

| 73 | 26.5 | $7,547 |

| 75 | 24.6 | $8,130 |

| 77 | 22.9 | $8,734 |

| 80 | 20.2 | $9,901 |

| 85 | 16.0 | $12,500 |

| 90 | 12.2 | $16,393 |

Notice the pattern? The older you get, the larger your required withdrawal becomes. That’s by design — the IRS wants to make sure tax-deferred savings eventually generate taxable income.

The Valuation Challenge with Physical Metals

Here’s where Gold IRAs require a bit more planning than a regular retirement account.

Your custodian has to determine the fair market value of your entire Gold IRA as of December 31 each year. With paper holdings, there’s a clear closing price. With physical gold and silver, it depends on the pricing source your custodian uses.

Most custodians reference the LBMA Gold Price PM fix or COMEX closing prices. This valuation gets reported on Form 5498, which your custodian files with the IRS by May 31 of the following year.

If you hold a mix of products — American Eagles, Maple Leafs, bars of different weights — each item gets valued separately. Make sure your custodian’s valuation method is transparent. Ask about it. You’re entitled to know exactly how they’re pricing your metals.

Satisfying Your RMD — Cash or Physical Metals

You’ve got two ways to meet your RMD requirement:

- Cash method — Your custodian sells enough metals to cover the RMD amount and sends you the cash. This is the most common approach.

- In-kind method — Your custodian distributes physical metals equal in value to your RMD. The coins or bars ship to you, and the fair market value on the distribution date counts toward your RMD.

Either way, the amount is reported as taxable income.

And either way — don’t wait until mid-December to start. Physical metal sales, shipping logistics, and custodian processing all take time. Your Gold IRA needs a longer runway than a typical account withdrawal. Start the conversation with your custodian early in the fourth quarter.

What Happens If You Miss the Deadline

Missing your RMD triggers a 25% excise tax on the shortfall — the difference between what you should’ve withdrawn and what you actually took.

On a $7,547 RMD? That’s roughly $1,887 in penalties — on top of the income tax you’d still owe.

The one piece of good news: if you correct the mistake within two years, the penalty drops to 10%. File Form 5329 with your return and include a brief explanation of the error.

But the better approach? Don’t let it happen in the first place. Plan ahead. Mark your calendar. Talk to your custodian before the end-of-year rush.

The Basis Reset — A Tax Planning Opportunity Most Owners Miss

Here’s something most Gold IRA owners don’t think about until it’s too late — and it could save you real money.

When you take an in-kind distribution, the IRS resets your cost basis to the fair market value on the day those metals leave your IRA.

Why does that matter? Because it changes how future taxes are calculated — potentially in your favor.

What the Basis Reset Means in Practice

Say you purchased 10 ounces of gold inside your IRA years ago at $1,800 per ounce. Gold’s now trading around $5,000.

You take an in-kind distribution of those 10 ounces at age 65.

Here’s what happens:

- Taxable event — The FMV of $50,000 (10 oz × $5,000) gets reported as ordinary income for the year.

- New cost basis — Your basis in those 10 ounces resets to $5,000 per ounce — not the $1,800 you originally paid inside the IRA.

- Future gains — If you later sell at $5,500 per ounce, you’d owe capital gains on just the $500 per ounce difference. Not on the full $3,200 gain from the original purchase price.

See how that works? The metals come out. You pay income tax at your current rate. And any future appreciation is taxed at the capital gains rate — which is typically lower than the ordinary income rate.

When the Basis Reset Works Best

Timing matters here. A few scenarios where this opportunity really shines:

- During a market pullback — If gold dips temporarily, taking an in-kind distribution during that dip means a lower FMV, less taxable income, and a lower basis that could appreciate once prices recover.

- In lower-income years — Retired at 62 but not collecting Social Security until 67? Those interim years may put you in a lower tax bracket. That’s a window worth using.

- For a long-term hold — Planning to keep the physical gold for years — or pass it to your children or grandchildren? The basis reset gives you a clean starting point for future tax calculations.

This is one of those areas where a conversation with your CPA or tax professional can make a real difference. The math depends on your income, your bracket, and your timeline.

Roth Gold IRA Distributions — A Different Set of Rules

If your precious metals are held in a Roth Gold IRA, the rules shift — and they shift in your favor.

The trade-off? You funded the account with after-tax dollars. But the IRS rewards that patience on the back end.

No RMDs During Your Lifetime

This is the headline.

Unlike traditional Gold IRAs, Roth Gold IRAs don’t require you to take distributions while you’re alive. Your metals can stay in the account — growing tax-free — for as long as you choose.

Thinking about legacy? This makes the Roth structure especially appealing if you want to pass your metals to your children or grandchildren without being forced to draw down the account first.

Qualified Distributions Are Tax-Free

After age 59½ — and as long as the account’s been open for at least five years — distributions from a Roth Gold IRA are completely tax-free and penalty-free. That includes your original contributions and any growth in the value of your metals.

Here’s the breakdown:

- Contributions — Can be withdrawn at any time, tax-free and penalty-free. You already paid taxes on this money.

- Earnings and growth — Tax-free only if the distribution is “qualified” — meaning you’re 59½ or older and the five-year rule is met.

- Non-qualified withdrawals of earnings — Subject to income tax and the 10% early withdrawal penalty, unless an exception applies.

The Five-Year Rule

The five-year clock starts on January 1 of the tax year you make your first Roth IRA contribution. So if your first Roth contribution was in 2022, the five-year period ends on January 1, 2027.

Here’s the important detail — this applies to your entire Roth structure, not just the Gold IRA. If you’ve had any Roth IRA open for five years, that clock is already satisfied for all your Roth accounts.

The Step-by-Step Process for Taking a Gold IRA Distribution

Whether you’re taking cash or physical metals, the distribution process follows a clear sequence. Knowing what to expect — and what to have ready — takes the uncertainty out of it.

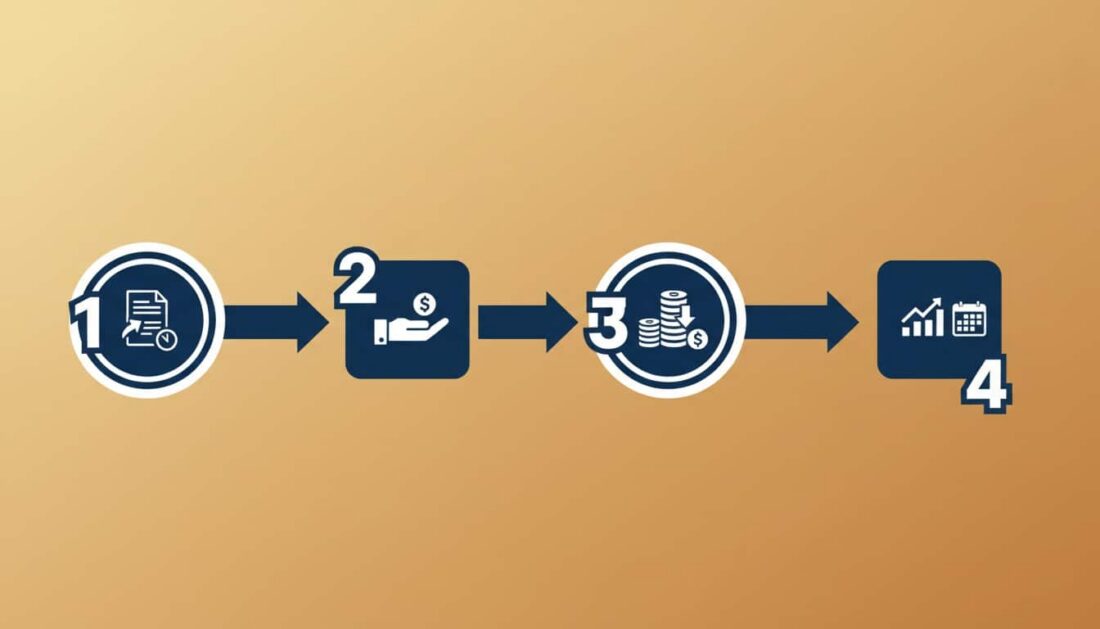

Step 1 — Submit Your Distribution Request

Contact your custodian and fill out the distribution form. You’ll need to specify:

- Distribution type — Cash or in-kind

- Amount or specific metals — A dollar amount for cash, or specific coins and bars for in-kind

- Delivery method — Wire transfer, check, or a physical shipping address

- Tax withholding — Your federal (and possibly state) withholding election

Most custodians offer online forms. Some still require a signed paper form — check ahead of time so you’re not scrambling.

Step 2 — Your Custodian Processes the Request

The custodian reviews your request, verifies your identity, and gets to work.

For cash, they’ll sell the metals at current market prices. For in-kind, they’ll coordinate with the depository to release and ship your coins or bars.

Expect 3 to 5 business days for cash and 5 to 10 business days for in-kind — including shipping time.

Some custodians charge shipping and insurance fees for physical deliveries. Ask about these costs before you pull the trigger. No surprises is always the goal.

Step 3 — Fair Market Value Gets Determined

The custodian establishes the FMV using recognized pricing benchmarks. This is the number that determines your taxable amount.

For in-kind distributions, it also sets your new cost basis.

If you’re executing a precious metals IRA distribution for the first time, ask your custodian which pricing source they use — LBMA, COMEX, or something else. Request written documentation. It’s your money, and you deserve clarity on how it’s being valued.

Step 4 — Tax Reporting

Your custodian issues Form 1099-R by January 31 of the following year. This is the form you’ll use when filing your return.

A few fields to pay attention to:

- Box 1 — Gross distribution amount (the FMV for in-kind distributions)

- Box 2a — Taxable amount

- Box 4 — Federal income tax withheld

- Box 7 — Distribution code (tells the IRS what type of distribution it was)

Keep everything — the distribution request form, valuation records, shipping confirmations, and your 1099-R. Hold onto it for at least seven years.

Distribution Costs — What to Expect Beyond Taxes

Taxes are the big cost. But they aren’t the only one. Depending on how you take your distribution, there are fee structures worth understanding upfront.

Common Distribution-Related Fees

- Custodian processing fee — Some custodians charge a flat fee per distribution — usually $25 to $50.

- Metal sale spread — For cash distributions, the custodian or dealer may apply a spread on the sale. This is the gap between the buy and sell price — and it can range from 1% to 5% depending on the product.

- Shipping and insurance — For in-kind distributions, shipping depends on weight, value, and destination. Insured shipping for gold typically runs $50 to $200 or more.

- Wire transfer fee — If you want your cash wired, expect $25 to $50.

None of these fees are deal-breakers. But they do add up over multiple distributions. Ask your custodian for a complete fee schedule before your first withdrawal — not after.

Fee Comparison at a Glance

| Fee Type | Cash Distribution | In-Kind Distribution |

|---|---|---|

| Custodian processing | $25-$50 | $25-$50 |

| Sale spread | 1%-5% | None |

| Shipping and insurance | None | $50-$200+ |

| Wire transfer | $25-$50 | Not applicable |

Transferring vs. Withdrawing — Know the Difference

This trips people up more often than you’d think.

A transfer between IRA custodians is not a distribution. If you’re moving your Gold IRA from one custodian to another — or executing a precious metals IRA rollover from a 401(k) — that’s a non-taxable event, as long as it’s done the right way.

Direct vs. Indirect Rollovers

A direct rollover — trustee-to-trustee — creates no tax, no penalty, and no 1099-R. The money goes straight from one custodian to the other. You never touch it.

An indirect rollover means the funds pass through your hands. That starts a 60-day clock. Miss the deadline? It becomes a taxable distribution.

If you’re moving metals, make sure your custodian handles it as a direct transfer. The last thing you need is an unintended tax bill on money you were just trying to reposition.

The 60-Day Rule and How It Catches People

The 60-day window sounds generous — until you realize how quickly it closes.

If your old custodian mails you a check, the clock starts the day you receive it. Not the day you deposit it. Not the day the new custodian processes it. The day the check hits your mailbox.

And if you miss that window — even by a single day — the IRS treats the entire amount as a taxable distribution. If you’re under 59½, the 10% early withdrawal penalty applies on top of that.

The simplest way to avoid this? Skip the indirect route entirely. A direct trustee-to-trustee transfer keeps the IRS out of the picture.

Frequently Asked Questions

Can I take my Gold IRA distribution in physical coins?

Yes — it’s called an “in-kind” distribution. Your custodian ships the actual coins or bars directly to you instead of selling them and sending cash.

The IRS treats the fair market value on the distribution date as taxable income. Once those metals leave your IRA, you own them outright. And that FMV becomes your new cost basis if you ever sell.

The process typically takes 5 to 10 business days. You can receive IRS-approved coins like American Gold Eagles, Canadian Maple Leafs, or qualifying bars.

What is the penalty for taking money out of a Gold IRA before 59½?

You’ll typically owe a 10% early withdrawal penalty on top of ordinary income tax. In the 22% bracket, that’s roughly 32% of the distribution gone — before state taxes.

Exceptions exist for disability, SEPP payments, medical expenses over 7.5% of AGI, first-time home purchases (up to $10,000), and the SECURE Act 2.0 emergency provision of up to $1,000 per year.

How long does it take to get cash from selling my Gold IRA metals?

Most custodians can complete a cash liquidation in 3 to 5 business days. You give the instruction, they sell at market price, and the cash gets wired or mailed to you.

Gold is one of the most liquid commodities in the world. The timeline isn’t about finding a buyer — it’s about custodial paperwork and banking. If you’re on a deadline, start early.

Do I have to take an RMD if my Gold IRA is a Roth?

No. Roth IRAs don’t require distributions during the owner’s lifetime. That’s one of the biggest advantages of the Roth structure — your metals can stay put and grow tax-free as long as you’re alive.

One exception to note: beneficiaries who inherit a Roth Gold IRA are subject to the SECURE Act’s 10-year distribution rule. Most non-spouse beneficiaries must empty the inherited account within 10 years.

What are the new 2026 emergency withdrawal exceptions under SECURE Act 2.0?

The SECURE Act 2.0 allows a penalty-free emergency distribution of up to $1,000 per year for unforeseeable or immediate personal or family needs. You self-certify — no documentation required. You’ve got three years to repay it.

The catch: you can’t take another one within three years unless the first is repaid or you’ve made contributions equal to the amount withdrawn.

How does the IRS calculate the value of my gold for a withdrawal?

Your custodian determines the fair market value using benchmarks like the LBMA Gold Price PM fix or COMEX closing prices.

For RMD math, the December 31 account balance from the prior year gets divided by your life expectancy factor from the IRS Uniform Lifetime Table.

For in-kind distributions, the FMV on the day the custodian releases the metals determines both your taxable amount and your new cost basis.

What happens if I miss my Gold IRA RMD deadline?

The IRS hits you with a 25% excise tax on whatever you should’ve withdrawn but didn’t. Correct the mistake within two years, and the penalty drops to 10%.

With a Gold IRA, the risk of missing deadlines is real — physical metals take longer to process than a simple cash withdrawal. Start the process early in the fourth quarter to give yourself a cushion.

Can I time my Gold IRA distribution to reduce my tax bill?

To a degree, yes. For cash distributions, selling during a market pullback means a lower sale price — and less taxable income. For in-kind distributions, the FMV on the day the custodian releases the metals is what counts. You can’t pick a date after the fact.

The bigger opportunity? Coordinating distributions with your overall income for the year. Lower-income years mean lower brackets. A conversation with your CPA or tax professional can help you map out a multi-year strategy that keeps more in your pocket.

Conclusion

Taking money out of a Gold IRA isn’t complicated — but it does require knowing the rules before you need to use them.

The difference between cash and in-kind. The timing of your first RMD. The basis reset. The penalty exceptions under SECURE Act 2.0. These are details that save you money when you understand them upfront — and cost you money when you don’t.

The most important thing you can do right now? Talk to your custodian about their specific process, timeline, and fees. If you’re approaching 73, start planning your first RMD well before the deadline. Physical metals need a longer runway than a typical account withdrawal.

Precious metals may appreciate, depreciate, or remain unchanged. Resale values depend on market conditions. Consult your CPA or tax professional for guidance specific to your situation. Brighton does not provide financial, legal, or tax advice.

If you’re approaching retirement and want clarity on how distributions work — before you’re up against a deadline — we’re here to help.

If you’re thinking “this all makes sense, but I don’t have time to figure it out on my own,” you’re not alone. Most customers we work with felt the same way before they realized how seamless the process can be with the right guidance.

That’s why we offer a complimentary consultation to walk you through your options — including our No Fee Precious Metals IRA, which covers custodial fees for the lifetime of the account on qualified purchases.

We’ll show you exactly:

- How the No Fee IRA works and whether you qualify

- The difference between U.S.-minted coins and foreign alternatives

- What to expect from the purchasing and delivery process

- How to roll over or transfer existing retirement funds

- What ongoing support looks like after your purchase

Learn About the No Fee IRA — no obligation, just actionable insights you can use whether you work with us or not.

Whether you’re five years from your first RMD or you’re ready to take your first in-kind distribution this year — the right guidance makes all the difference. That’s what concierge service looks like — support at every stage of ownership.