How Do Required Minimum Distributions Work with a Gold IRA? (2026 Rules)

Here’s a surprise most Gold IRA owners don’t think about until it’s right in front of them — the IRS doesn’t care that your retirement account holds physical coins in a vault. When you turn 73, they want their share. And the way you handle it can either cost you gold or keep every ounce in your hands.

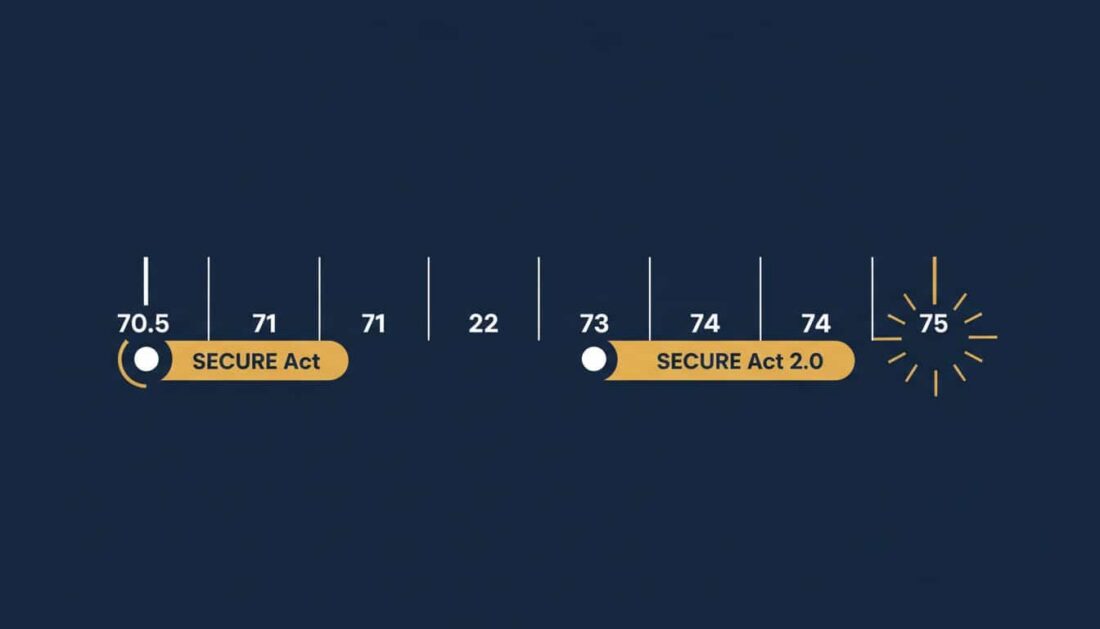

That mandatory withdrawal is called a Required Minimum Distribution. In 2026, owners of Traditional Gold IRAs must begin taking RMDs at age 73 under the SECURE Act 2.0. The amount is calculated by dividing your account’s Fair Market Value as of December 31 of the previous year by a life expectancy factor from the IRS. For age 73, that factor is 26.5.

But here’s what makes a Gold IRA different from a regular brokerage account.

You’re not just clicking “withdraw” and getting a direct deposit. Your account holds real, physical metal — coins and bars sitting in an approved depository. So when it’s time for a distribution, you’ve got a choice most people don’t realize they have: sell the metal for cash, or take what’s called an in-kind distribution — where the actual gold gets shipped directly to you.

That means you can satisfy the IRS requirement without losing a single ounce.

And if you own more than one IRA? There’s a rule — called the aggregation rule — that lets you take the entire RMD from a different, more liquid account. Your gold stays untouched.

Whether you’re just starting to explore understanding gold IRA distribution options or you’ve owned precious metals for years, this guide walks through everything — the math, the methods, the deadlines, and the strategies that give you peace of mind and keep you in control.

What Are RMDs — and Why Do They Apply to Your Gold?

Think of it this way. When you funded your Traditional IRA, the government gave you a deal — you didn’t pay taxes on that money going in. RMDs are simply how the IRS collects on that deal later.

It’s not complicated. It’s just the price of tax-deferred growth.

Why the IRS Requires Withdrawals

Every dollar in your Traditional IRA — including a self-directed Gold IRA — has been growing tax-free. The IRS can’t let that continue forever.

So at a certain age, they require you to start pulling money out. That way, they eventually collect income tax on those funds during your lifetime.

Here’s how it breaks down by account type:

- Traditional Gold IRAs — Subject to RMDs starting at age 73 for those born between 1951 and 1959. The age bumps to 75 in 2033 for anyone born in 1960 or later.

- Roth Gold IRAs — Not subject to RMDs during your lifetime. You already paid taxes on those contributions, so the IRS doesn’t need to force withdrawals.

- SEP and SIMPLE IRAs — Also subject to RMDs at age 73, even if you’re still working and receiving contributions.

The rules themselves aren’t different for a Gold IRA. The mechanics — that’s where things get interesting.

What Makes Gold IRA Distributions Different?

With a standard brokerage IRA, your custodian sells a few shares, deposits cash into your checking account, and you’re done. Maybe five minutes.

Gold IRAs don’t work that way.

Your account holds physical coins and bars inside an approved depository. You can’t just click “sell.” Someone has to either arrange a sale of real metal — or coordinate a secure shipment of coins to your front door.

Does that make it harder? Not really. It just means you need to plan ahead. Most custodians recommend starting the process 30 to 60 days before your deadline.

The important thing to know is this — the IRS treats your Gold IRA exactly like any other Traditional IRA. Same age requirement. Same formula. Same penalties if you miss it.

The only difference is logistics. And logistics, with the right guidance, are manageable.

How to Calculate Your 2026 Gold IRA RMD

The math here is simple. One division problem. But with a Gold IRA, the tricky part isn’t the formula — it’s making sure you’re starting with the right number.

The Formula

Every RMD works the same way:

Prior Year-End Fair Market Value ÷ IRS Life Expectancy Factor = Your RMD

For 2026, here’s how that plays out:

- Step 1 — Get the total Fair Market Value of your Gold IRA as of December 31, 2025. Your custodian reports this on IRS Form 5498.

- Step 2 — Look up your life expectancy factor in Table III of IRS Publication 590-B. At age 73, the factor is 26.5.

- Step 3 — Divide the FMV by your factor.

- Step 4 — That number is the minimum you must withdraw — in cash, physical metal, or a combination.

So if your Gold IRA held $200,000 worth of precious metals at year-end 2025:

$200,000 ÷ 26.5 = $7,547

That’s your 2026 RMD.

You can always take out more. You can never take out less — not without a penalty.

How Fair Market Value Works for Physical Gold

This is the part that trips people up. Your account doesn’t have a simple dollar balance like a savings account. It holds metal — and the value of that metal changes every day.

So how does the IRS know what your gold is worth?

Your custodian handles it. They use established pricing sources — typically the London PM gold fix or COMEX closing prices — to determine your account’s value as of December 31.

That year-end number is what drives your RMD calculation.

But here’s a detail worth noting. The value used to calculate your RMD is the December 31 figure. If you take an in-kind distribution later in the year, the taxable amount is based on spot price on the actual distribution date — not the number from December.

That distinction can work in your favor. More on that in the strategies section.

Key Ages and Factors from the Uniform Lifetime Table

The IRS updated these tables in 2022 to reflect longer life expectancies. That’s good news — it generally means smaller required withdrawals than under the old tables.

| Age in 2026 | Life Expectancy Factor | RMD on $200,000 Account | RMD on $500,000 Account |

|---|---|---|---|

| 73 | 26.5 | $7,547 | $18,868 |

| 75 | 24.6 | $8,130 | $20,325 |

| 78 | 22.0 | $9,091 | $22,727 |

| 80 | 20.2 | $9,901 | $24,752 |

| 85 | 16.0 | $12,500 | $31,250 |

Notice how the factor shrinks as you age — which means the withdrawal amount grows. For Gold IRA owners, that matters. Larger RMDs may mean selling more ounces or shipping higher-value coins.

One more thing — if your spouse is both the sole beneficiary of your IRA and more than 10 years younger, you’d use a different table (Table II) that usually produces a smaller distribution. You can find both in IRS Publication 590-B.

Cash, Physical Gold, or Both? Choosing Your Distribution Method

This is the decision that sets Gold IRAs apart from every other retirement account. When the IRS says “withdraw” — you get to decide what that actually looks like.

Do you sell the gold and take cash? Or do you have the coins shipped to your house?

Option 1: Cash Liquidation

Straightforward. Your custodian sells enough metal to cover your RMD amount. The cash gets deposited into your bank account.

- Processing time — Usually 5 to 10 business days. The custodian handles the sale and the transfer.

- Tax impact — The amount you receive is reported as ordinary income for the year.

- The trade-off — You permanently reduce your physical gold holdings. If prices rise after the sale, that appreciation is gone.

Cash is the simpler path. But for many owners, selling gold defeats the entire purpose of holding it. Why convert tangible metal back into the very dollars you were trying to move away from?

That’s a question worth sitting with.

Option 2: In-Kind Distribution

This is the option most people don’t know exists — and it’s one of the biggest advantages of owning a Gold IRA.

An in-kind distribution means you receive the actual physical coins or bars from the depository. They get securely packaged, insured, and shipped directly to your home or a private vault.

- How valuation works — The fair market value of the metal on the distribution date counts as your taxable amount and satisfies the RMD.

- Tax impact — Same as cash. You owe income tax on the value. The difference? Your gold is now in your hands — not converted to dollars.

- The advantage — You meet the IRS requirement without giving up your metal. The gold just moves from the depository to your personal possession.

Think about what that means. You satisfy the government’s rule and keep your wealth preservation position intact. The gold doesn’t disappear. It comes home.

If you’re considering this route, understanding the full logistics of executing a precious metals IRA distribution helps you plan ahead.

Option 3: A Combination

Nothing says you have to pick just one method.

If your RMD is $8,000 and you own Gold American Eagles worth roughly $2,600 each, the math doesn’t divide evenly. You could take three coins — about $7,800 — and cover the remaining $200 in cash.

It’s flexible. The IRS just cares that you hit the number.

Side-by-Side: Which Method Fits Your Goals?

| Factor | Cash Liquidation | In-Kind Distribution |

|---|---|---|

| What you receive | Dollars deposited to your bank | Physical coins or bars shipped to you |

| Processing time | 5–10 business days | 15–30+ business days |

| Additional costs | Possible liquidation spread | Shipping, insurance, handling fees |

| Tax treatment | FMV on sale date = taxable income | FMV on distribution date = taxable income |

| Your gold position after | Reduced — metal is sold | Preserved — metal is in your hands |

| Best for | Owners who need cash flow | Owners who want to keep their metal |

Here’s the question that matters most: did you buy gold to hold it — or to sell it at the first mandatory checkpoint?

For most of our customers, the answer is pretty clear.

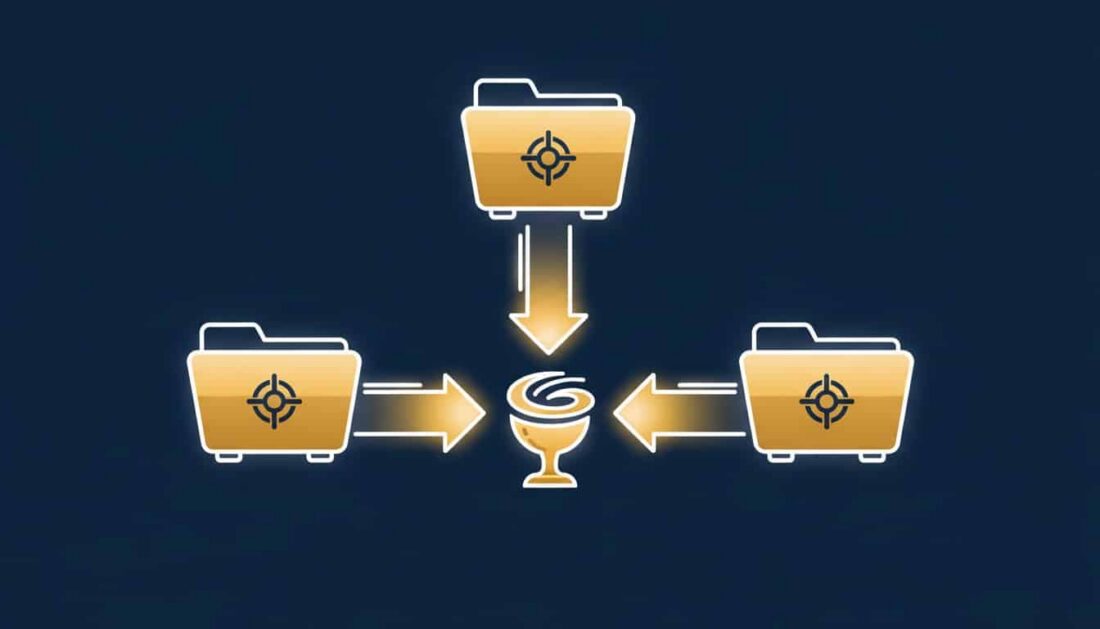

The Aggregation Rule: Keep Every Ounce and Still Satisfy the IRS

Here’s what we’re seeing more and more — owners who hold both a Gold IRA and a traditional brokerage IRA, and they don’t realize they can use one to protect the other.

It’s called the aggregation rule. And for Gold IRA owners, it might be the most valuable tool the IRS ever created.

How It Works

The IRS treats all of your Traditional IRAs — including SEP and SIMPLE IRAs — as one big pool for RMD purposes. That means:

- Step 1 — Calculate the RMD for each Traditional IRA separately, using each account’s December 31 balance and your life expectancy factor.

- Step 2 — Add all those RMD amounts together for one total number.

- Step 3 — Withdraw that total from any one account — or any combination you choose.

The IRS confirms this on their RMD FAQ page. You must calculate separately, but you can distribute from wherever makes the most sense.

Why This Changes Everything for Gold Owners

Let’s say you own a Gold IRA worth $300,000 and a regular brokerage IRA worth $100,000. Your combined RMD totals around $15,000.

Under the aggregation rule, you could pull that entire $15,000 from your brokerage account — and leave every single ounce of gold in the depository.

No selling. No shipping. No fees. No disruption to your precious metals position.

That’s not a loophole. It’s exactly how the IRS designed it.

- Your gold stays working — Physical metals keep doing what you bought them to do — sit in secure storage and hold value.

- Your liquid account covers the tax bill — Cash and money market funds are easier and cheaper to distribute.

- Peace of mind — You satisfy the requirement without second-guessing whether you should’ve held onto those coins.

For owners who specifically acquired physical gold as a long-term wealth preservation strategy, this rule is essential. It lets you stay positioned exactly where you want to be.

What the Aggregation Rule Doesn’t Cover

A few important limits to keep in mind:

- 401(k) and employer plans — You can’t pull your 401(k) RMD from an IRA. Each employer plan requires its own separate distribution.

- Inherited IRAs — These must be calculated and distributed on their own. You can’t combine an inherited IRA’s RMD with your personal accounts.

- Spousal accounts — Your IRAs and your spouse’s IRAs are calculated independently. No cross-aggregation.

Deadlines, Penalties, and Why Gold IRAs Need Extra Lead Time

Missing an RMD used to carry one of the steepest penalties in the entire tax code — 50%. The SECURE Act 2.0 brought that down significantly, but it’s still steep enough to take seriously.

The Two Deadlines That Matter

- Your first-year RMD (one-time rule) — If you turn 73 in 2026, your first distribution is due by April 1, 2027. This is a one-time grace period.

- Every year after that — All future RMDs are due by December 31 of each calendar year. No extensions.

Here’s the catch. If you delay your first distribution to April 2027, you’ll owe your 2027 RMD by December 31 of that same year. That’s two taxable distributions in one year — which could push you into a higher bracket.

For most owners, it makes more sense to take the first RMD in the year you actually turn 73. Consult your CPA or tax professional to decide what timing works best for your situation.

What Happens If You Miss the Deadline

| Penalty Detail | Old Rules (Before 2023) | Current Rules (2023+) |

|---|---|---|

| Excise tax on missed RMD | 50% of the shortfall | 25% of the shortfall |

| Reduced penalty if corrected | No formal reduction | 10% if corrected within 2 years |

| IRS waiver available | Yes, with Form 5329 | Yes, with Form 5329 |

Let’s put that in real numbers.

If you were supposed to withdraw $10,000 and didn’t, the current penalty is $2,500 (25%). Correct the mistake within two years — withdraw the full amount and file a corrected return — and the penalty drops to just $1,000 (10%).

You can also request a complete waiver by filing Form 5329 with a reasonable explanation. The IRS has historically been generous with these waivers for honest mistakes.

Why Gold IRAs Need More Time Than Paper Accounts

With a brokerage account, a distribution can process in a day or two. Maybe three.

With a Gold IRA? Weeks.

If you’re taking an in-kind distribution, the custodian has to coordinate with the depository, select specific coins, arrange secure packaging, and ship insured metal across the country. That doesn’t happen overnight.

Wait until mid-December to start the process, and you’re playing a dangerous game. One shipping delay, one holiday closure, one custodian backlog — and suddenly you’ve missed December 31.

That’s why experienced Gold IRA owners start the process no later than early November. If you’re concerned about how timing and understanding gold IRA fee structures might affect your distribution, planning early gives you room to make smart decisions instead of rushed ones.

Your 2026 Gold IRA RMD Checklist

Whether this is your first RMD or you’ve been doing this for years, a clear process keeps you on track. Here’s a practical quarter-by-quarter guide built for physical precious metals accounts.

January – March: Do the Math

- Confirm your year-end account value — Contact your custodian or wait for Form 5498 (due to you by May 31) to confirm the December 31 Fair Market Value of your Gold IRA. Some custodians provide preliminary numbers earlier.

- Look up your factor — Use Table III in IRS Publication 590-B or run the numbers through the FINRA RMD Calculator to verify.

- Calculate across all IRAs — If you own multiple Traditional IRAs, run the RMD math for each one. Add them up. Decide which account you’ll draw from.

April – June: Choose Your Path

- Pick your distribution method — Cash, in-kind, or combination? Or are you using the aggregation rule to pull from a different account entirely?

- Watch the market — If you’re planning a cash distribution, higher gold prices mean fewer ounces sold to meet the same dollar target. Timing matters.

- Call your custodian — Ask how much lead time they need. For in-kind distributions, expect 30 to 60 days — sometimes longer during Q4.

July – September: Start the Process

- Submit formal instructions — Put your distribution request in writing. Specify the method, the amount, and delivery details.

- For in-kind distributions — Confirm which coins or bars get shipped. Verify insurance coverage during transit. Make sure you’ve got a secure storage plan at home or with a private vault. If you need a refresher on how depositories handle this, understanding gold IRA storage rules covers the logistics.

- For cash distributions — Confirm bank account details and expected sale pricing.

October – December: Close It Out

- Verify completion — Whether cash or metal, confirm the distribution has been fully processed and recorded by your custodian.

- Keep your paperwork — Your custodian will issue Form 1099-R showing the distribution amount. Hold onto this for tax time.

- December 31 is non-negotiable — Make sure the transaction is settled before year-end. A request submitted on December 20 may not clear in time.

Smart Strategies to Protect Your Gold and Stay Compliant

Taking an RMD doesn’t mean your precious metals strategy falls apart. With a little planning, you can satisfy the IRS and keep your position right where you want it.

Here are the five approaches worth knowing:

- Aggregation rule — Pull your entire RMD from a more liquid account and leave the gold untouched.

- In-kind timing — Take physical delivery when spot prices dip to lower the taxable amount.

- Roth conversion — Move metal into a Roth before age 73 to eliminate future RMD obligations entirely.

- Qualified charitable distributions — Send IRA funds directly to charity — it counts toward your RMD and stays out of your taxable income.

- Coordinate with personal holdings — Use each year’s distribution as a natural way to build your outside-the-IRA position.

Use the Aggregation Rule to Leave Your Gold Alone

If you own both a Gold IRA and a traditional brokerage IRA, this is the simplest play. Calculate your combined RMD, then take the full amount from your liquid account.

Your gold stays in the depository — doing exactly what you bought it to do.

Time In-Kind Distributions to Lower Your Tax Bill

Here’s something worth thinking about.

When you take an in-kind distribution, the taxable amount is based on the gold’s spot price on the day of distribution — not your year-end valuation.

If gold dips temporarily during the year, that’s actually an opportunity. You receive the same number of coins, but the IRS considers a lower taxable value. Same gold — smaller tax bill.

This isn’t about trying to time the market. It’s about having the flexibility to pick your window.

Consider a Roth Conversion Before RMDs Start

If you’re a few years away from age 73, converting part of your Traditional Gold IRA to a Roth eliminates future RMD obligations on those funds.

You’ll pay income tax on the converted amount that year. But once the metal is inside a Roth, it grows tax-free — and the IRS can’t force withdrawals during your lifetime.

For owners focused on control and legacy planning, that’s a powerful trade-off.

One important detail — if you’ve already reached RMD age, you have to take your current-year distribution before converting. The RMD itself can’t be rolled into a Roth.

Qualified Charitable Distributions (QCDs)

If you’re 70½ or older, you can direct up to $105,000 per year from your Traditional IRA straight to a qualified charity. It counts toward your RMD but stays out of your taxable income.

The distribution must go directly from the IRA to the charity — you can’t take it first and then donate. This works best from a liquid account, since most charities aren’t set up to receive physical gold. But paired with the aggregation rule, it’s another way to reduce your tax burden while meeting your obligations.

Coordinate with What You Already Own

If you already hold physical gold outside of a retirement account, an in-kind distribution simply adds to that position.

Many of our customers use this approach over time — gradually moving metals out of the IRA structure and into personal possession. Each year’s RMD becomes a natural transfer point.

You’re staying compliant. You’re building your personal holdings. And you’re not giving up anything along the way.

Brighton’s concierge service is built for exactly these conversations — helping you think through the options at every stage of ownership so you feel confident in the plan you choose.

Roth Gold IRAs and Inherited Accounts: What’s Different

Not every Gold IRA follows the same playbook. If you hold a Roth, or if you’ve inherited a Gold IRA from a loved one, the distribution rules look quite different.

Roth Gold IRAs: No RMDs — Ever

This is one of the biggest advantages of a Roth account.

Because you already paid taxes on your contributions, the IRS doesn’t require any withdrawals during your lifetime. No mandatory distributions. No annual calculations. No forced liquidation of metal.

Your gold can sit in the depository for decades — growing tax-free — with no one telling you when to take it out.

For owners focused on preserving wealth for children and grandchildren, this kind of flexibility is hard to beat.

Inherited Gold IRAs: Rules for Beneficiaries

When the original owner of a Traditional Gold IRA passes away, the beneficiaries inherit the account — along with distribution requirements.

Under the SECURE Act’s 10-year rule, most non-spouse beneficiaries must fully distribute the inherited IRA within 10 years of the original owner’s death. Some exceptions apply:

- Surviving spouses — Can treat the inherited IRA as their own, which resets the RMD schedule based on their own age.

- Minor children — May stretch distributions until they reach the age of majority, then the 10-year clock starts.

- Disabled or chronically ill beneficiaries — Can use their own life expectancy, similar to the old “stretch IRA” rules.

- Beneficiaries within 10 years of the owner’s age — Also qualify for life expectancy distributions.

This area has seen a lot of changes in recent years. The rules around annual distributions within that 10-year window are still evolving. If you’ve inherited a Gold IRA — or you’re thinking ahead about what happens to yours — consult a tax professional for guidance specific to your situation.

For a broader look at protecting your accounts from common risks, identifying safe gold IRA practices is a good place to start.

Frequently Asked Questions

At what age do I have to start taking RMDs from my Gold IRA in 2026?

Under the SECURE Act 2.0, owners of Traditional Gold IRAs must begin taking RMDs at age 73. This applies to anyone born between 1951 and 1959.

If you turn 73 in 2026, your first distribution is due by April 1, 2027 — but waiting means you’ll owe two distributions in the same calendar year. That’s two taxable events in one year, which could bump your bracket.

The RMD starting age rises to 75 in 2033 for those born in 1960 or later.

What is the penalty for missing a Gold IRA RMD?

The SECURE Act 2.0 dropped the penalty from 50% to 25% of the amount that should have been distributed.

Correct the mistake within two years — by withdrawing the required amount and filing a corrected return — and the penalty drops further to just 10%.

You can also request a full waiver from the IRS by filing Form 5329 and explaining what happened. The IRS has a track record of granting these waivers for honest mistakes.

Can I have my physical gold shipped to my house as an RMD?

Yes. It’s called an in-kind distribution.

Your custodian works with the depository to select specific coins or bars, securely package them, and ship them directly to you with full insurance coverage. The fair market value on the distribution date counts as your RMD.

Once the gold arrives, it’s yours — to store at home, place in a private vault, or hold for future sale. You can learn more about the process involved in executing a precious metals IRA rollover and related distribution logistics.

How do I calculate the Fair Market Value of my gold for the IRS?

Your custodian handles this.

They use recognized pricing sources — usually the London PM gold fix or COMEX closing prices — to determine your account’s value as of December 31 each year. That number goes on Form 5498, which gets filed with the IRS.

You can double-check the math using free tools from the SEC’s official RMD calculator or the FINRA RMD Calculator.

Do Roth Gold IRAs have Required Minimum Distributions?

No. Roth Gold IRAs are not subject to RMDs during the original owner’s lifetime.

Because Roth contributions use after-tax dollars, the IRS doesn’t require mandatory withdrawals. Your metals can stay in the depository indefinitely — growing tax-free — with no forced distributions.

That said, beneficiaries who inherit a Roth Gold IRA may face distribution requirements depending on their relationship to the original owner.

Can I take my RMD from a different IRA instead of selling my gold?

Absolutely.

The IRA aggregation rule lets you calculate the RMD for each Traditional IRA separately, then take the total from whichever account you choose. That means you can satisfy your Gold IRA’s RMD entirely from a more liquid brokerage or savings account.

Your gold stays in the depository. The IRS gets its distribution. Everybody’s happy.

What happens if gold prices drop right before my RMD deadline?

It depends on how you’re taking the distribution.

For cash distributions, a price dip means you’d need to sell more ounces to meet the same dollar amount. For in-kind distributions, a drop in price actually works in your favor — the taxable value of the coins you receive is lower, which means less reported income.

The aggregation rule also gives you flexibility here. If gold is down and you don’t want to sell at a low point, take the RMD from a different account instead.

How far in advance should I notify my custodian before taking a Gold IRA RMD?

At least 30 to 60 days — and earlier is better.

Physical precious metals transactions take longer than paper withdrawals. If you’re requesting an in-kind distribution, the custodian needs time to coordinate with the depository for metal selection, valuation, secure packaging, and insured shipping.

Start by mid-October at the latest for a year-end distribution. That gives everyone a buffer for unexpected delays.

The Takeaway

Taking RMDs from a Gold IRA doesn’t have to mean dismantling what you’ve built. The formula is straightforward. The deadlines are clear. And you’ve got more options than most people realize — from in-kind distributions that keep your metal in hand, to the aggregation rule that lets you satisfy the IRS without selling a single coin.

The key is starting early. Gold IRA distributions take more coordination than paper account withdrawals — and the difference between planning in September versus scrambling in December can be the difference between a seamless process and a missed deadline.

Whether you’re approaching 73 for the first time or navigating distributions you’ve been taking for years, the right team makes all the difference. Brighton’s concierge service is built to support at every stage of ownership — including the stage where the IRS comes knocking.

Keep in mind — precious metals may appreciate, depreciate, or remain unchanged in value. Consult your CPA or tax professional for guidance specific to your situation.

Ready to Navigate Your Gold IRA RMD with Confidence?

If you’re thinking “this all makes sense, but I don’t have time to figure it out on my own,” you’re not alone. Most customers we work with felt the same way before they realized how straightforward the process can be with the right guidance.

That’s why we offer a complimentary consultation to walk you through your options — including our No Fee Precious Metals IRA, which covers custodial fees for the lifetime of the account on qualified purchases.

We’ll show you exactly:

- How the No Fee IRA works and whether you qualify

- The difference between U.S.-minted coins and foreign alternatives

- What to expect from the purchasing and delivery process

- How to roll over or transfer existing retirement funds

- What ongoing support looks like after your purchase

Learn About the No Fee IRA — no obligation, just actionable insights you can use whether you work with us or not.

Whether you’re preparing for your first RMD or looking for a smarter way to handle distributions from your precious metals IRA, clarity starts with a conversation.