What Paperwork Do I Need for a Gold IRA Rollover? (2026 Checklist)

If you’ve been thinking about moving retirement funds into physical gold, the paperwork question is probably top of mind. What forms do you actually need? Who provides them? And how do you make sure nothing gets lost between your current custodian and your new one?

Here’s the good news — it’s simpler than most people expect.

A gold IRA rollover in 2026 comes down to four core documents: a Self-Directed IRA Application, a valid government-issued ID, a Transfer or Rollover Request Form, and a Purchase Authorization. That’s it.

If you’re rolling over from an employer plan like a 401(k), there’s one additional piece — a safe harbor explanation your plan administrator is required to provide. And as of January 2026, the IRS updated those requirements through IRS Notice 2026-13.

The most important decision you’ll make isn’t which form to fill out first. It’s choosing a direct transfer over an indirect rollover. A direct transfer moves your funds from one custodian to another — you never touch the money. No mandatory tax withholding. No 60-day deadline. No risk of an accidental taxable event.

Whether you’re executing a precious metals IRA rollover from a traditional IRA, a Roth, a 401(k), or a Thrift Savings Plan — the documents below cover every scenario. And with gold trading above $5,000 per ounce and central bank demand still running strong into 2026, more Americans are understanding gold IRA funding methods than at any point in the last decade.

Don’t let the paperwork be the thing that slows you down.

The 4 Documents You’ll Need (And Who Provides Each One)

Every gold IRA rollover — regardless of where your money is coming from — follows the same four-document path. No surprises. No hidden forms.

Here’s what each one does and what to look out for.

Document 1: Self-Directed IRA (SDIRA) Application

This is the form that opens your new account. It establishes you with a custodian that’s authorized to hold physical precious metals on your behalf.

Your new SDIRA custodian provides this. Most offer an online application with e-signature — no printing, no scanning, no mailing.

You’ll enter your personal information, choose your account type (Traditional, Roth, SEP, or SIMPLE), and designate your beneficiaries.

One thing to double-check — if you’re married and live in a community property state, your spouse may need to consent to any non-spouse beneficiary designation. It’s a small detail that’s easy to overlook.

The whole thing takes about five minutes.

Document 2: Valid Government-Issued ID

You can’t open a retirement account without proving you are who you say you are. This one’s straightforward.

A current driver’s license, U.S. passport, state-issued ID, or military ID will work. Most custodians accept a clear photo or digital scan — uploaded through their secure portal.

The key? Make sure the name on your ID matches the name on your SDIRA application exactly. Even a missing middle initial can cause a delay.

Document 3: Transfer or Rollover Request Form

This is the document that actually moves your money. It authorizes your current custodian — or your employer’s plan administrator — to release your funds to the new SDIRA.

Some custodians provide a pre-filled version to make it easier. You’ll just need your current account number, the dollar amount you want to move, and the receiving custodian’s details.

Here’s where the biggest decision in the entire process shows up — direct transfer or indirect rollover.

A direct transfer sends the funds straight from one custodian to another. You never see the check. No taxes withheld. No deadline pressure.

An indirect rollover means the check comes to you. And the moment it does, a 60-day clock starts ticking.

We’ll break down exactly why that matters — and how to avoid the most common trap — in the next section.

Document 4: Purchase Authorization

Once your SDIRA is funded, this form instructs your metals dealer to acquire specific IRS-approved products on your behalf.

You’ll confirm the products you want — like Gold American Eagles or Gold Buffaloes — along with quantities and pricing. Your dealer coordinates with your custodian to make sure everything lines up.

Only metals meeting IRS fineness standards qualify for an IRA. For gold, that means .995 fine or higher. U.S.-minted coins from the United States Mint are among the most popular choices because they meet IRS requirements and carry the full backing of the U.S. government.

That’s the full checklist. Four documents — most of them digital — and when you’re working with a concierge team that handles the coordination between custodians and depositories, the process is seamless.

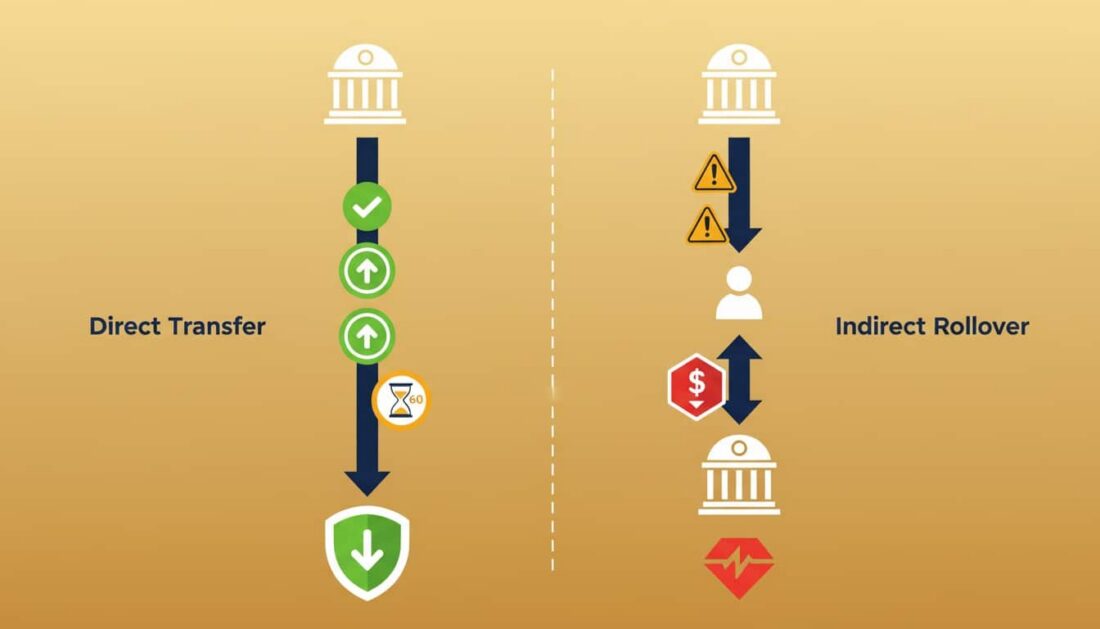

Direct Transfer vs. Indirect Rollover — Why It Changes Everything

The forms you’ll fill out depend on which method you choose to move your funds. And this single decision — direct transfer or indirect rollover — affects your taxes, your timeline, and the amount of money that actually arrives in your new account.

It’s worth understanding both before you sign anything.

How a Direct Transfer Works

A direct transfer — sometimes called a trustee-to-trustee transfer — is the simplest path. Your current custodian sends the funds straight to your new SDIRA custodian.

You never touch the money. You never see a check.

That means no mandatory tax withholding, no 60-day countdown, and no limit on how many transfers you can do in a year. The IRS doesn’t restrict trustee-to-trustee transfers the way it restricts indirect rollovers.

This is the method Brighton recommends — and the one most experienced custodians prefer — because it removes the two biggest risks in the entire process.

How an Indirect Rollover Works

With an indirect rollover, your current custodian distributes the funds directly to you. You then have exactly 60 calendar days to deposit the full amount into your new SDIRA.

If the money is coming from an employer plan — a 401(k), 403(b), or TSP — your plan administrator is required by law to withhold 20% for federal income taxes. Even if you plan to complete the rollover.

For IRA-to-IRA rollovers, there’s a default 10% withholding — though you can elect out of it.

There’s also a frequency limit. The IRS only allows one indirect IRA-to-IRA rollover per 12-month period. Direct transfers don’t count toward this limit.

Your employer’s plan administrator will also be required to provide you with a safe harbor explanation of your rollover options — updated as of January 2026 through IRS Notice 2026-13.

The 20% Withholding Trap — A Real-World Example

This is the scenario that catches more people than you’d expect.

Say you’re moving $100,000 from a 401(k) through an indirect rollover. Your plan administrator withholds 20% — that’s $20,000 — and sends you a check for $80,000.

Now, to complete the rollover without triggering a taxable event, you need to deposit the full $100,000 into your new SDIRA within 60 days.

Where does the missing $20,000 come from? Out of your own pocket.

If you only deposit the $80,000 you received, the IRS treats that $20,000 gap as a taxable distribution. And if you’re under 59½, you could face an additional 10% early withdrawal penalty on top of it.

That’s $20,000 in taxable income — plus potentially $2,000 in penalties — just because the check was made out to you instead of your custodian.

This is exactly why the direct transfer exists. And it’s exactly why most precious metals customers choose it.

| Feature | Direct Transfer | Indirect Rollover |

|---|---|---|

| Funds touch your hands? | No — custodian to custodian | Yes — check comes to you |

| Tax withholding | None | 20% (employer plans) or 10% (IRAs) |

| IRS deadline | None | 60 calendar days |

| Frequency limit | Unlimited | One per 12 months (IRA-to-IRA) |

| Risk of taxable event | Minimal | Significant if deadline missed |

What Changes If You’re Rolling Over From a 401(k)

If your funds are sitting in a 401(k), 403(b), 457(b), or Thrift Savings Plan, the paperwork expands a bit beyond the four core documents.

Employer-sponsored plans have their own rules. The good news is — they’re predictable, and your custodian can help you navigate every one of them.

The Safe Harbor Explanation

Before your employer plan can release any funds, the plan administrator has to hand you a written explanation of your options and what happens with taxes under each choice.

As of January 15, 2026, the IRS updated those explanations through Notice 2026-13. The new version reflects SECURE 2.0 Act changes — including clearer language about the 20% withholding rule and new exceptions to the 10% early withdrawal penalty.

Your plan administrator delivers this notice between 30 and 180 days before the distribution date. Read it carefully — it’s your roadmap for the entire rollover.

The Distribution Request Form

This is the employer plan’s version of the transfer authorization. It tells your plan administrator exactly how you want your funds handled — direct rollover, indirect rollover, or cash distribution.

Your HR department or plan record-keeper provides this form. To fill it out, you’ll need your new SDIRA custodian’s legal name, mailing address, EIN, and your new account number.

One thing to check first — does your plan allow partial rollovers while you’re still employed? Not all plans offer what’s called an “in-service distribution.” If yours doesn’t, you may need to wait until you leave the employer or reach age 59½.

Spousal Consent — When It Applies and When It Doesn’t

This one catches people off guard.

Employer plans governed by ERISA — the Employee Retirement Income Security Act — may require your spouse’s written consent before releasing funds. It depends on whether your plan offers an annuity payment option.

If the plan offers what’s called a Qualified Joint and Survivor Annuity and you’re choosing a lump-sum distribution or direct rollover instead, spousal consent is usually required.

But here’s the key distinction — IRAs don’t follow those same rules. Once your funds are in a self-directed IRA, you generally don’t need spousal consent for distributions or beneficiary changes. The exception is if you live in a community property state.

Not sure whether your plan requires spousal consent? Ask your plan administrator. It’s a quick question that can prevent a real delay.

| Scenario | Spousal Consent Needed? |

|---|---|

| 401(k) with annuity option — taking lump sum | Yes |

| 401(k) without annuity option — direct rollover | Generally no |

| IRA-to-IRA direct transfer | No (unless community property state for beneficiary changes) |

| TSP rollover | No (federal plans exempt) |

| Pension plan with annuity | Yes |

The 15-Minute Paperwork Path

Reading through every form and every rule can feel like a lot. But here’s what the actual experience looks like when you’re working with a team that handles the heavy lifting for you.

Most customers finish the entire paperwork process in a single sitting — often in under 15 minutes.

Step 1: Complete Your SDIRA Application (About 5 Minutes)

Your concierge team connects you with an approved custodian. You fill out the application online — name, Social Security number, beneficiary designations, account type.

E-sign it. Done.

Most applications are approved within one to two business days. Some custodians offer same-day approval.

Step 2: Upload Your ID (About 2 Minutes)

Snap a clear photo of your driver’s license or passport. Upload it through the custodian’s secure portal.

That’s the identity step — handled.

Step 3: Sign the Transfer Authorization (About 5 Minutes)

Your custodian prepares the transfer request — pre-filled with your existing account details and the receiving account information. You review it, e-sign it, and the custodian submits it on your behalf.

For employer plan rollovers, your custodian can also provide a Letter of Acceptance — confirming your new SDIRA is open and ready to receive the funds. Some plan administrators require this before they’ll release anything.

Step 4: Metal Selection and Purchase Authorization (About 3 Minutes)

Once your account is funded — typically one to three weeks after the transfer request is submitted — you’ll speak with your dealer to select IRS-approved gold and silver products.

Confirm your selections. Sign the purchase authorization. Your metals are acquired and shipped to an IRS-approved depository for secure storage — segregated in your name.

That’s the full process. Four steps. Four documents. Support at every stage of ownership.

| Step | What You’re Signing | Time | Who Handles the Details |

|---|---|---|---|

| 1 | SDIRA Application | ~5 min | You + Custodian |

| 2 | Government ID Upload | ~2 min | You |

| 3 | Transfer Authorization | ~5 min | You + Custodian |

| 4 | Purchase Authorization | ~3 min | You + Dealer |

What the IRS Changed in 2026 — And Why It Matters

The rules around retirement rollovers don’t stay the same year to year. The IRS made several updates in early 2026 that directly affect how gold IRA paperwork is handled — and what your plan administrator is required to tell you.

Here’s what changed and why it matters.

IRS Notice 2026-13: Updated Safe Harbor Explanations

On January 15, 2026, the IRS issued Notice 2026-13 — replacing the previous guidance from Notice 2020-62.

What’s different?

The updated safe harbor explanations now include clearer language about the 20% withholding requirement. They reflect SECURE 2.0 Act changes — including new exceptions to the 10% early withdrawal penalty for terminally ill individuals, victims of domestic abuse, and certain emergency situations.

There’s also updated guidance on Required Minimum Distributions for surviving spouses. And the IRS added a table of contents to help recipients find the sections that apply to their situation — a small change, but a helpful one.

If you’re rolling over from an employer plan, you’ll receive this notice before any funds are distributed. It’s worth reading carefully — it’s designed to help you understand every option before you make a decision.

2026 IRA Contribution Limits

Rollovers aren’t subject to annual contribution caps — you can roll over $50,000 or $500,000 without hitting a limit. But if you’re also making new contributions to your SDIRA, you’ll want to know the current numbers.

For 2026, the IRS raised the annual IRA contribution limit to $7,500 — up from $7,000 in 2025. If you’re age 50 or older, the catch-up contribution brings your total to $8,600, per IRS Publication 590-A.

Why This Matters Now

Gold is trading above $5,000 per ounce as of February 2026. Central banks purchased 863 tonnes of gold in 2025 — the third consecutive year above 800 tonnes, according to the World Gold Council.

What does that mean for your rollover paperwork? Nothing changes about the forms themselves. But it does mean more people are moving through this process right now — and the customers who have their documents ready tend to move faster and with more confidence.

Being positioned ahead of the curve starts with having the right paperwork in hand.

5 Paperwork Mistakes That Can Delay Your Rollover

Most rollover delays don’t come from complicated regulations. They come from small, avoidable mistakes on the forms themselves.

Here’s what we see most often — and what identifying safe gold IRA practices looks like in practice.

Mistake 1: Name Mismatches Between Documents

If your driver’s license says “Robert J. Smith” but your current IRA is under “Bob Smith,” your custodian may flag the transfer.

Make sure the name on every document matches exactly — including middle initials, suffixes, and hyphenations. It sounds minor. It’s not.

Mistake 2: Blank or Outdated Beneficiary Designations

Your SDIRA application includes a beneficiary section. Leaving it blank — or accidentally listing a former spouse — can create legal complications that are much harder to fix later.

Take the extra 30 seconds to fill this out correctly from the start.

Mistake 3: Choosing an Indirect Rollover Without Understanding the Consequences

We’ve covered this in detail, but it’s worth repeating. If you receive a check from an employer plan made out to you, the 20% withholding happens automatically. There’s no reversing it after the fact.

The only way to avoid it? Elect a direct rollover before the distribution is processed.

Mistake 4: Not Checking for In-Service Distribution Rules

Still employed and want to roll over funds from your current 401(k)? Not all plans allow that.

Check whether your plan offers in-service distributions before you start the paperwork. If it doesn’t, you may need to wait until you leave the employer or reach age 59½.

Mistake 5: Forgetting the Letter of Acceptance

Some plan administrators won’t release funds without a Letter of Acceptance from your new custodian. This confirms your SDIRA is open and ready to receive the transfer.

Most custodians provide this automatically. But if yours doesn’t — just ask. It takes one phone call.

Frequently Asked Questions

Do I need a Medallion Signature Guarantee for a gold IRA rollover?

Sometimes — but not always.

A Medallion Signature Guarantee is an extra layer of identity verification that goes beyond a standard notarization. It’s most commonly required when you’re moving large sums from a brokerage-style account.

Direct transfers between custodians typically don’t require one. But if your current custodian asks for it, your bank or credit union can usually provide the stamp at no charge.

The easiest way to avoid a surprise? Ask your current custodian what they require before you start.

Can I use a digital copy of my driver’s license for SDIRA paperwork?

In most cases, yes.

Most self-directed IRA custodians accept a clear digital scan or photo of your government-issued ID. It needs to be legible, unobstructed, and show all four corners.

Some custodians still require a notarized copy for larger accounts. Your custodian can tell you exactly what they need — and many now offer secure upload portals that make this step quick.

What is a Letter of Acceptance (LOA) in a gold IRA transfer?

It’s a document from your new SDIRA custodian confirming they’re ready to receive the incoming funds.

Think of it as a “green light” — formal proof that your new account is open, active, and eligible to hold the transfer. Your current custodian or plan administrator may require this letter before releasing your money.

Most SDIRA custodians issue the LOA automatically once your application is approved.

Does my spouse need to sign the gold IRA rollover forms?

It depends on where the funds are coming from.

IRAs aren’t subject to ERISA spousal consent rules. So moving funds between IRAs — or changing beneficiaries on an IRA — typically doesn’t require your spouse’s signature.

Employer-sponsored plans are different. If your 401(k) or pension offers an annuity option and you’re choosing a different form of distribution, spousal consent may be required.

And if you live in a community property state — Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, or Wisconsin — your spouse may need to consent to beneficiary changes on your new SDIRA regardless.

Consult your CPA or tax professional for guidance specific to your situation.

What is the deadline for submitting my gold IRA rollover paperwork?

For a direct transfer — there’s no strict IRS deadline. The funds move on the custodians’ timeline, usually within one to three weeks.

For an indirect rollover — you have exactly 60 calendar days from the date you receive the distribution to deposit the full amount into your new SDIRA. Miss that window, and the IRS treats the entire unredeposited amount as taxable income. If you’re under 59½, you could face an additional 10% early withdrawal penalty on top of it.

Bottom line — direct transfers don’t have a ticking clock. Indirect rollovers do. That alone is reason enough to choose the transfer route.

How do I get my 401(k) plan administrator to release the funds to gold?

Start by contacting your plan administrator or HR department and requesting a direct rollover. They’ll provide the required forms — typically a distribution request and a direct rollover election form.

You’ll need your new SDIRA custodian’s legal name, mailing address, EIN, and your new account number. If the plan requires a Letter of Acceptance from your new custodian, have that ready before you call.

Most employer plans process direct rollovers within five to fifteen business days.

What happens if I miss the 60-day rollover deadline?

The IRS treats the full unredeposited amount as a taxable distribution for that year.

If you’re under 59½, you may also face an additional 10% early withdrawal penalty. In limited circumstances, the IRS may grant a waiver — but requesting one requires self-certification or a private letter ruling.

This is the single biggest reason most precious metals customers choose a direct transfer. It removes the deadline entirely.

Can I do a partial rollover into a gold IRA?

Absolutely. You don’t have to move your entire retirement balance.

Many customers roll over a portion of their 401(k) or traditional IRA into physical metals while keeping the rest where it is. The same paperwork applies whether you move everything or just a portion — the only difference is the dollar amount on your transfer form.

It’s a common approach for customers who want to hold something tangible without completely restructuring their retirement.

Conclusion

The paperwork for a gold IRA rollover isn’t complicated — but it does need to be done right. Four core documents. One smart decision — choosing a direct transfer. And a team that handles the coordination between custodians, depositories, and dealers so you don’t have to chase down every detail yourself.

That’s what peace of mind looks like in practice.

Whether you’re rolling over $25,000 or $250,000, the path is the same. The forms are the same. And the goal is the same — holding something real, in your name, outside the traditional financial system.

Precious metals may appreciate, depreciate, or remain unchanged in value. Consult your CPA or tax professional for guidance specific to your situation.

If you’ve been thinking “this all makes sense, but I don’t have time to figure it out on my own,” you’re not alone. Most customers we work with felt the same way before they realized how straightforward the process can be with the right guidance.

That’s why we offer a complimentary consultation to walk you through your options — including our No Fee Precious Metals IRA, which covers custodial fees for the lifetime of the account on qualified purchases.

We’ll show you exactly:

- How the No Fee IRA works and whether you qualify

- The difference between U.S.-minted coins and foreign alternatives

- What to expect from the purchasing and delivery process

- How to roll over or transfer existing retirement funds

- What ongoing support looks like after your purchase

Learn About the No Fee IRA — no obligation, just actionable insights you can use whether you work with us or not.

Your retirement paperwork shouldn’t be the barrier between you and something real. Let’s make it easy.