Is a Gold IRA a good idea for your retirement?

Here’s the short version: it depends on what you’re trying to accomplish.

If your goal is preserving purchasing power, reducing exposure to dollar-denominated assets, and holding something tangible inside a tax-advantaged account—then yes, a Gold IRA can make sense as part of a broader retirement strategy.

If you’re looking for income-generating assets or quick, aggressive growth? Probably not the right fit.

Here’s what most people miss: a Gold IRA isn’t designed to replace your entire retirement. It’s designed to protect a portion of it—more like an insurance policy that happens to sit inside your IRA than a growth engine.

Gold doesn’t pay dividends. It doesn’t generate interest.

What it does is hold its value when paper assets struggle. That’s exactly why J.P. Morgan Global Research projects prices could average $5,055 per ounce by the fourth quarter of 2026—potentially climbing toward $5,400 by the end of 2027.

The real question isn’t whether gold is “good” or “bad.”

It’s whether gold fits your situation—your timeline, your concerns, and what you’re trying to protect.

Let’s break down the pros, the cons, and what this actually looks like in practice.

Why This Conversation Matters Right Now

Gold isn’t making headlines because of hype. It’s making headlines because of what’s happening in the broader economy.

In 2024, gold delivered a 27% return—slightly outperforming the S&P 500’s 25% total return.

That marked the first time in recent history both assets exceeded 25% gains in the same calendar year.

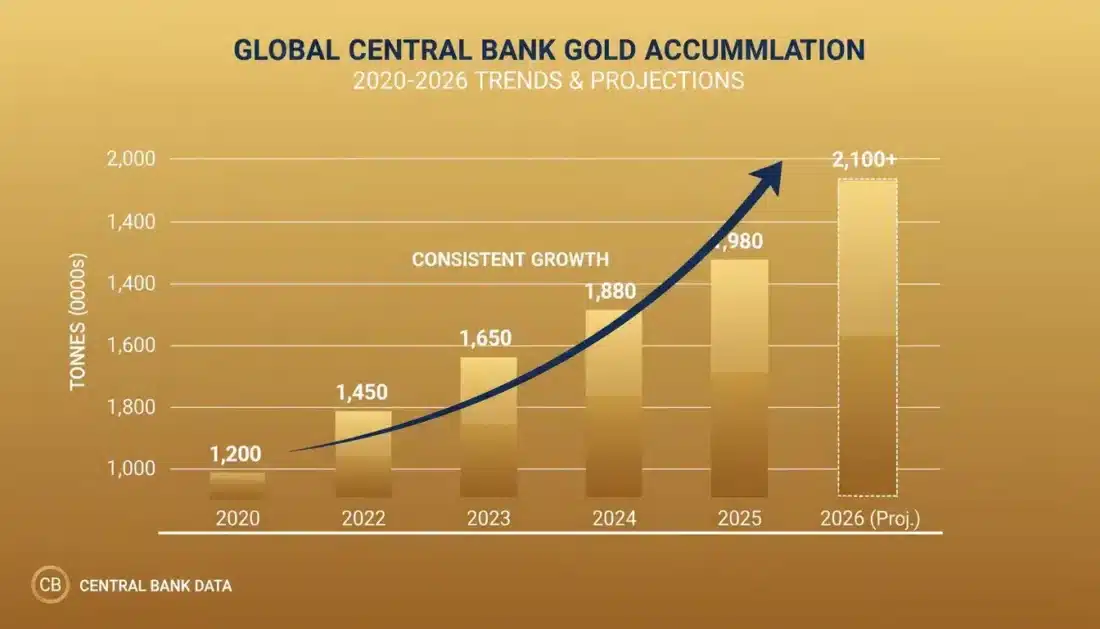

The momentum has continued. Gold broke through $4,000 per ounce for the first time. Central banks around the world have purchased over 1,000 tonnes annually for three consecutive years—a pace not seen in modern financial history.

So what’s driving this?

What’s Behind the Surge

Several factors are converging at once:

- Central bank buying — Countries like Poland, China, India, and Turkey are actively increasing their gold reserves to reduce reliance on the U.S. dollar. According to the World Gold Council, central banks now hold nearly 20% of official reserves in gold—up from around 15% at the end of 2023.

- Dollar weakness — The U.S. dollar has weakened significantly against a basket of other currencies. According to Morgan Stanley Research, this decline has been one of the steepest in decades. When the dollar weakens, gold typically strengthens.

- Debt concerns — Billionaire investor Ray Dalio has compared escalating U.S. debt payments to “plaque in the arteries,” warning of a potential “economic heart attack” that hasn’t been priced into markets. Speaking at the Greenwich Economic Forum, Dalio recommended up to 15% of a retirement picture in gold—three times what most traditional financial professionals suggest.

- Inflation persistence — While inflation has moderated from 2022 peaks, it remains elevated. The Bureau of Labor Statistics data shows cumulative inflation since 2020 exceeding 20%. Dollars saved five years ago simply buy less today.

Understanding why gold is valuable in the first place helps explain why these economic conditions drive demand.

Why This Matters for Your Retirement

If you’re within 10-15 years of retirement—or already retired—these trends hit differently than they do for a 30-year-old with decades to recover from market downturns.

When the dollar loses purchasing power, your retirement savings buy less.

When markets correct, you may not have time to wait for recovery.

When banking systems face stress, access to funds can become uncertain.

Gold doesn’t solve all of these problems. But it addresses a specific one: maintaining purchasing power regardless of what happens to paper currencies or financial markets.

That’s the conversation we’re having here. Not whether gold is the “best” thing to own—but whether it deserves a place in your retirement picture.

The Pros: What a Gold IRA Does Well

Let’s start with what physical gold—held inside an IRA—actually delivers.

There are solid reasons to buy gold that apply specifically to retirement planning. Here’s what matters most.

Protection Against Dollar Decline

The U.S. dollar has lost over 96% of its purchasing power since 1913.

That’s not a political statement—it’s math from the Federal Reserve’s own data.

Gold tends to move in the opposite direction. When currencies weaken, gold strengthens. When confidence in government debt erodes, gold benefits.

This isn’t speculation. It’s the reason central banks are buying gold at record levels—they’re protecting their reserves against the same risks individual customers face.

Tax-Advantaged Growth

Here’s something many people don’t realize.

Owning physical gold outside an IRA subjects you to collectibles tax rates—up to 28% on gains.

Inside a Traditional Gold IRA? Those gains grow tax-deferred until you take distributions.

Inside a Roth Gold IRA? Qualified withdrawals are tax-free.

The same tax advantages that make Traditional and Roth IRAs attractive for stocks and bonds apply to precious metals. The difference is you’re holding something physical.

No Counterparty Risk

Stocks depend on company performance. Bonds depend on the issuer’s ability to pay. ETFs depend on the fund manager and custodian.

Physical gold in an IRS-approved depository? It’s yours. Period.

It doesn’t depend on a corporation staying solvent, a government making good on promises, or a financial institution maintaining liquidity.

As Ray Dalio put it in his CNBC interview: “Gold is the only asset that somebody can hold and you don’t have to depend on somebody else to pay you money for.”

That’s clarity you can’t get from paper assets.

Portfolio Diversification

Gold has low correlation with stocks and bonds. This means it often moves independently—or in the opposite direction—from traditional assets.

Here’s what the data shows:

During the nine years when the S&P 500 posted negative returns since 1971, gold outperformed in eight of them. Gold averaged returns of 19.4% while stocks averaged losses of 15.3%, according to analysis from Monetary Metals.

That’s diversification that actually works when you need it most.

Understanding the differences between gold and silver can help you build an even more balanced precious metals position.

Tangible Ownership

There’s something psychologically different about owning physical metal versus digits on a screen.

You can’t print more gold. You can’t hack it. It’s been valued for 5,000 years across every culture and civilization.

For retirement-aged customers who’ve watched market crashes, banking crises, and currency fluctuations—owning something real provides peace of mind that numbers in an account simply don’t.

The Cons: What You Need to Consider

A Gold IRA isn’t for everyone. Here’s what to weigh before moving forward.

No Income Generation

Let’s be direct about this.

Gold doesn’t pay dividends. It doesn’t generate interest. The only return comes from price appreciation.

This matters if you’re counting on your retirement accounts to produce income.

A Gold IRA is better suited for the “preservation” portion of your retirement—not the “income” portion.

Think of it this way: gold is the insurance. Dividend stocks, bonds, or annuities might be the income. They serve different purposes.

Higher Fees Than Traditional IRAs

Gold IRAs cost more to maintain than a basic stock-and-bond IRA at a traditional brokerage. That’s just the reality.

Here’s what typical fees look like:

| Fee Type | Typical Range |

|---|---|

| Account Setup | $50-$150 (one-time) |

| Annual Administration | $75-$300 |

| Storage and Insurance | $100-$300 |

| Transaction/Wire Fees | $25-$50 per trade |

| Dealer Premium | 3-5% above spot price |

Most customers pay between $200 and $600 annually for administration and storage combined.

On a $100,000 Gold IRA, that’s 0.2-0.6% per year—not dramatically different from many mutual fund expense ratios, but higher than index funds.

Why the fee? Physical gold requires real security. It needs to be stored in an IRS-approved vault, insured against theft and damage, and tracked for compliance. That costs money.

Brighton’s No Fee Precious Metals IRA eliminates custodial fees for the lifetime of the account on qualified purchases—which changes this calculation significantly. But you should always understand the fee structure before committing to any provider.

Required Professional Storage

You cannot store IRA gold at home.

This is non-negotiable under IRS regulations.

Physical gold in your IRA must be held in an IRS-approved depository—facilities with institutional security, insurance, and regular audits. If you store it yourself, the IRS treats it as a distribution, triggering taxes and potential penalties.

Some customers find this frustrating. They want to hold the metal in their hands.

That’s understandable—but the trade-off is losing the tax advantages entirely.

If physical possession matters more than tax benefits, a cash purchase outside an IRA might be a better fit for that portion of your metals.

Liquidity Considerations

Selling physical gold from an IRA takes longer than selling stocks with a click.

The process typically involves coordinating with your custodian, arranging sale through a dealer, and waiting 3-5 business days for settlement.

This isn’t a problem if you’re treating gold as a long-term holding. It becomes a problem if you need quick access to cash in an emergency.

The solution? Don’t put money in a Gold IRA that you might need on short notice. Keep appropriate liquidity elsewhere.

Price Volatility

Gold can drop. Short-term price swings of 5-6% in a single day have occurred during market turbulence.

Over long periods, gold tends to preserve purchasing power. Over short periods, it can be volatile.

If you’re planning to liquidate within a year or two, that volatility matters. If you’re holding for a decade or more, short-term swings become less relevant.

This is why Gold IRAs work best as part of a long-term strategy—not a short-term trade.

Gold IRA vs. Traditional IRA: A Direct Comparison

How do the two structures actually compare? Here’s a direct breakdown:

| Factor | Traditional IRA | Gold IRA |

|---|---|---|

| Asset Type | Stocks, bonds, mutual funds, ETFs | Physical gold, silver, platinum, palladium |

| Income Generation | Dividends, interest, capital gains | Price appreciation only |

| Counterparty Risk | Dependent on markets and institutions | No counterparty risk (physical ownership) |

| Annual Fees | Often minimal or zero | $200-$600 typically |

| Storage | Electronic/custodial | IRS-approved depository required |

| Liquidity | Same-day or next-day | 3-5 business days typical |

| Tax Treatment | Tax-deferred (Traditional) or tax-free (Roth) | Same as Traditional/Roth IRAs |

| Inflation Response | Depends on holdings | Historically rises with inflation |

| Contribution Limits (2026) | $7,500 ($8,600 if 50+) | Same limits apply |

| RMD Requirements | Required at age 73 | Same requirements apply |

The fundamental difference isn’t in the IRA structure—it’s in what you’re holding inside it.

Both offer the same tax advantages. Both have the same contribution limits and distribution rules.

The difference? Whether you’re holding paper assets dependent on markets and institutions—or physical metal you actually own.

For a deeper dive into how Gold IRA transfers and rollovers work between account types, we’ve created a comprehensive guide.

How Much of Your Retirement Should Be in Gold?

This is where opinions diverge. And honestly? There’s no single right answer.

The Traditional View

Most financial professionals suggest keeping precious metals to 5-10% of a total retirement picture.

The logic: gold provides diversification benefits at this level without overexposing you to a single non-yielding asset.

The Current Environment View

Given today’s economic conditions, some prominent voices are recommending higher allocations.

Ray Dalio, founder of Bridgewater Associates—the world’s largest hedge fund—has publicly stated that “from a strategic asset allocation perspective, you would probably have something like 15% of your portfolio in gold because it is the one asset that does very well when the typical parts of your portfolio go down.”

His reasoning centers on debt concerns, currency debasement risk, and gold’s role as the only major asset with no counterparty dependence.

Finding Your Number

The appropriate allocation depends on several factors:

- Your timeline — Closer to retirement or already retired? Higher preservation allocation may make sense.

- Your existing holdings — Heavy in stocks and bonds? Gold provides genuine diversification. Already holding real estate and other tangibles? You may need less.

- Your concerns — Worried about dollar purchasing power? Currency controls? Banking access? Gold addresses these specifically.

- Your comfort level — Some customers sleep better knowing they own physical metal. Others prefer liquidity. Both are valid.

A common approach: start with a smaller allocation—perhaps 5-10%—and evaluate over time. If it brings peace of mind and you see value in expanding, you can always add more.

What 2026 Market Conditions Mean for Gold

What are major institutions actually projecting? And why does it matter?

Price Forecasts from Major Banks

| Institution | 2026 Gold Price Target |

|---|---|

| J.P. Morgan | $5,055/oz (Q4 average) |

| Goldman Sachs | $4,900/oz |

| Bank of America | $5,000/oz |

| Morgan Stanley | $4,400/oz |

| Deutsche Bank | $4,450/oz |

These aren’t fringe predictions. They’re projections from some of the largest financial institutions in the world—based on analysis of supply, demand, and macroeconomic factors.

J.P. Morgan’s Natasha Kaneva, head of Global Commodities Strategy, states: “The long-term trend of official reserve and investor diversification into gold has further to run. We expect gold demand to push prices toward $5,000/oz by year-end 2026.”

Why These Projections Matter

The forecasts are built on observable trends:

- Central bank buying remains elevated — J.P. Morgan projects around 755 tonnes of central bank purchases in 2026. While lower than the 1,000+ tonne years of 2022-2024, it’s still well above historical averages of 400-500 tonnes.

- ETF inflows are returning — Gold-backed ETFs have posted record quarterly inflows. Institutional money is flowing back toward gold.

- Structural diversification continues — Many central banks with less than 10% of reserves in gold are actively working to increase that share. The potential demand from this shift alone could support prices for years.

The Caution

Forecasts are projections—not guarantees.

Gold can drop. Unexpected events can shift markets. No one knows exactly where prices will be in 12 months.

Precious metals may appreciate, depreciate, or remain unchanged depending on market conditions.

The more important question: regardless of where prices go short-term, does holding physical gold serve your long-term retirement goals?

If you’re buying to preserve purchasing power over a decade or more, trying to time the exact entry point matters less than having the position at all.

The Process: How a Gold IRA Actually Works

Thinking about moving forward? Here’s what the process actually looks like.

Step 1: Open a Self-Directed IRA

A Gold IRA is technically a “self-directed IRA”—an IRA structure that allows assets beyond stocks and bonds.

You’ll need a custodian that specializes in these accounts. The custodian handles paperwork, ensures IRS compliance, and coordinates with depositories.

They don’t sell you the metals—that’s the dealer’s role.

Setup typically takes a few days to a week.

Step 2: Fund the Account

You have several options:

- Direct rollover from an existing 401(k), 403(b), TSP, or other employer plan — Funds transfer directly from one custodian to another. No taxes. No penalties. No 60-day clock to worry about.

- IRA transfer from an existing Traditional or Roth IRA — Same process. Direct custodian-to-custodian transfer.

- New contribution — You can contribute up to $7,500 in 2026 ($8,600 if you’re 50 or older) in cash, which is then used to purchase metals.

For customers wondering how to roll over a 401(k) to a Gold IRA without penalty, the key is using a direct rollover rather than taking a distribution yourself.

Step 3: Select Your Metals

Not all gold qualifies for IRA inclusion.

IRS rules require:

- Gold: Minimum 99.5% purity (exception: American Gold Eagle at 91.67%)

- Silver: Minimum 99.9% purity

- Platinum: Minimum 99.95% purity

- Palladium: Minimum 99.95% purity

Popular IRA-eligible options include:

- American Gold Eagles — The most popular choice, specifically approved by Congress

- American Gold Buffalos

- Canadian Gold Maple Leafs

- Gold bars from accredited refiners (LBMA-approved)

Collectible coins, numismatic pieces, and coins that don’t meet purity standards are not eligible.

Step 4: Purchase and Storage

Once funded, you work with a dealer to select and purchase your metals.

The dealer ships directly to an IRS-approved depository—never to your home.

You’ll choose between:

- Segregated storage — Your metals are kept separate from other customers’. Higher cost, but your specific coins and bars are always identifiable.

- Non-segregated (commingled) storage — Your metals are stored with others of the same type and purity. Lower cost, but you receive equivalent metals when you liquidate rather than the exact pieces you purchased.

Both options are fully insured and audited regularly.

Step 5: Ongoing Management

After setup, a Gold IRA requires minimal attention.

You’ll receive annual statements showing your holdings, their current value, and any activity.

When it’s time to take distributions—at age 59½ or later to avoid early withdrawal penalties—you can either:

- Sell metals and receive cash

- Take physical delivery of your metals (treated as a distribution)

Required Minimum Distributions (RMDs) begin at age 73 under current rules. You can satisfy RMDs by liquidating metals or taking in-kind distributions.

What You Can Do Next

If this overview has clarified whether a Gold IRA fits your situation, here are your options.

If You’re Ready to Explore Further

Start with education. Understand what you’d be holding, why, and how it fits your broader picture.

The worst decisions happen when people rush into something they don’t fully understand.

Brighton offers complimentary consultations where we walk through your specific situation—no pressure, no obligation. We’ll explain exactly how the process works, answer your questions, and help you determine if this makes sense for you.

That’s what concierge service looks like. Support at every stage of ownership—not just when you’re buying.

If You’re Not Sure Yet

That’s perfectly reasonable. Take time to:

- Review your current retirement holdings

- Consider your timeline and goals

- Think about what concerns you most about the next decade

- Research different providers and compare fee structures

The right time to act is when you’re confident it serves your goals—not when someone pressures you into a decision.

If Gold Isn’t Right for You

Also perfectly reasonable.

A Gold IRA isn’t for everyone. If you need income generation, want maximum liquidity, or simply don’t share the concerns that drive gold ownership, other strategies may fit better.

The goal is always finding what actually serves your retirement—not selling you something that doesn’t fit.

Frequently Asked Questions

Is a Gold IRA a good idea for most retirees?

A Gold IRA can be a good idea for retirees seeking to preserve purchasing power and reduce exposure to dollar-denominated assets.

It works best as a portion of a broader retirement strategy—typically 5-15% of total holdings—rather than a complete replacement for traditional accounts.

The decision depends on your timeline, risk tolerance, and financial goals. Customers who value tangible ownership, worry about currency stability, or want genuine diversification from paper assets often find value in the structure.

What are the main disadvantages of a Gold IRA?

The main disadvantages include higher fees than traditional IRAs (typically $200-$600 annually for storage and administration), no dividend or interest income from physical gold, required use of an IRS-approved depository for storage, and potential liquidity delays when selling metals.

Gold can also experience price volatility in the short term.

These factors make Gold IRAs better suited for long-term preservation rather than short-term trading or income generation.

How much does it cost to maintain a Gold IRA?

Most Gold IRA owners pay between $200 and $600 per year in total fees. This includes custodian administration fees ($75-$300), storage and insurance fees ($100-$300), and occasional transaction fees ($25-$50 per trade).

Dealer premiums of 3-5% above spot price apply when purchasing metals.

Some providers offer fee-free options—Brighton’s No Fee Precious Metals IRA covers custodial fees for the lifetime of the account on qualified purchases.

Can I store Gold IRA metals at home?

No. IRS regulations require that Gold IRA metals be stored in an IRS-approved depository.

Storing metals at home can result in the IRS treating it as a distribution, triggering taxes and potential early withdrawal penalties.

If physical possession is important to you, consider a cash purchase outside of an IRA structure for that portion of your metals. You can own gold both inside an IRA (tax-advantaged but depository-stored) and outside (full possession but subject to collectibles tax rates).

What percentage of my retirement should be in gold?

Financial experts typically recommend 5-10% of a retirement picture in precious metals.

However, some prominent voices like Ray Dalio have recently suggested up to 15% given current economic conditions and debt concerns.

The right allocation depends on your age, risk tolerance, existing holdings, and retirement timeline. Many customers start with a smaller allocation and evaluate over time.

How has gold performed compared to stocks in recent years?

Gold has outperformed the S&P 500 in several recent periods.

In 2024, gold returned 27% compared to 25% for the S&P 500.

Since 2000, gold has delivered cumulative returns that exceed the S&P 500. However, stocks have historically outperformed over longer multi-decade periods when measured from different starting points.

The key insight: gold tends to outperform during periods of uncertainty, making it valuable for diversification during market stress.

What types of gold can I hold in an IRA?

IRS rules require gold to be at least 99.5% pure (.995 fineness), with one exception: the American Gold Eagle, which is 91.67% gold but specifically approved by Congress for IRA inclusion.

Popular IRA-eligible options include American Gold Eagles, American Gold Buffalos, Canadian Gold Maple Leafs, and gold bars from accredited refiners meeting the purity standard.

Collectible coins and numismatic pieces are not eligible.

Is 2026 a good time to open a Gold IRA?

Market conditions in 2026 present several factors that support gold ownership: major financial institutions project gold prices reaching $5,000+ per ounce, central banks continue buying at elevated levels, and concerns about government debt and currency stability persist.

However, timing any market is difficult.

Most experts recommend a long-term approach rather than trying to time entry points. If gold fits your retirement strategy, the specific entry point matters less than having an appropriate position for the long term.

Conclusion

A Gold IRA isn’t a magic solution. It won’t guarantee returns, eliminate all risk, or replace thoughtful retirement planning.

What it can do is provide a specific type of protection: holding something tangible, inside a tax-advantaged structure, that doesn’t depend on the performance of paper markets or the promises of institutions.

For customers worried about dollar purchasing power, banking stability, or leaving something real to the next generation—that protection has value.

For customers focused purely on growth, income generation, or maximum liquidity—other approaches may fit better.

The honest answer to “Is a Gold IRA a good idea?” is: it depends on what you’re trying to accomplish.

If what you’ve read here resonates—if these concerns match yours, if this approach makes sense for your situation—then exploring further is worth your time.

Precious metals may appreciate, depreciate, or remain unchanged depending on market conditions. Consult your CPA or tax professional for guidance specific to your situation. Brighton does not provide financial, legal, or tax advice.

Ready to see if a Gold IRA fits your retirement picture?

If you’re thinking “this makes sense, but I want to understand how it would work for my specific situation,” you’re not alone.

Most customers we work with felt the same way before their first conversation with us.

That’s why we offer a complimentary consultation to walk through your options—including our No Fee Precious Metals IRA, which covers custodial fees for the lifetime of the account on qualified purchases.

We’ll show you exactly:

- How the No Fee IRA works and whether you qualify

- The difference between U.S.-minted coins and foreign alternatives

- What to expect from the purchasing and delivery process

- How to roll over or transfer existing retirement funds

- What ongoing support looks like after your purchase

Learn About the No Fee IRA — no obligation, just actionable insights you can use whether you work with us or not.

For current market trends and insights, check out our Gold Market Recap.

The right time to act is when you’re confident it serves your goals. We’re here whenever that is.