How Do I Sell My Physical Gold When I Need Liquidity?

Selling physical gold for liquidity involves contacting a reputable dealer, receiving a quote based on the current spot price minus the dealer’s buy spread, and shipping or delivering the gold for verification. The dealer’s buy spread often ranges from 2% to 15%. Once the dealer verifies weight and purity, payment is issued via wire transfer, check, or ACH within a few business days. The entire process can often be completed in under two weeks.

The U.S. Mint does not buy back bullion products from the public. Sellers work with dealers who specialize in purchasing precious metals. Pricing transparency and process clarity vary by dealer. Some explain their pricing openly. Others create pressure to act immediately.

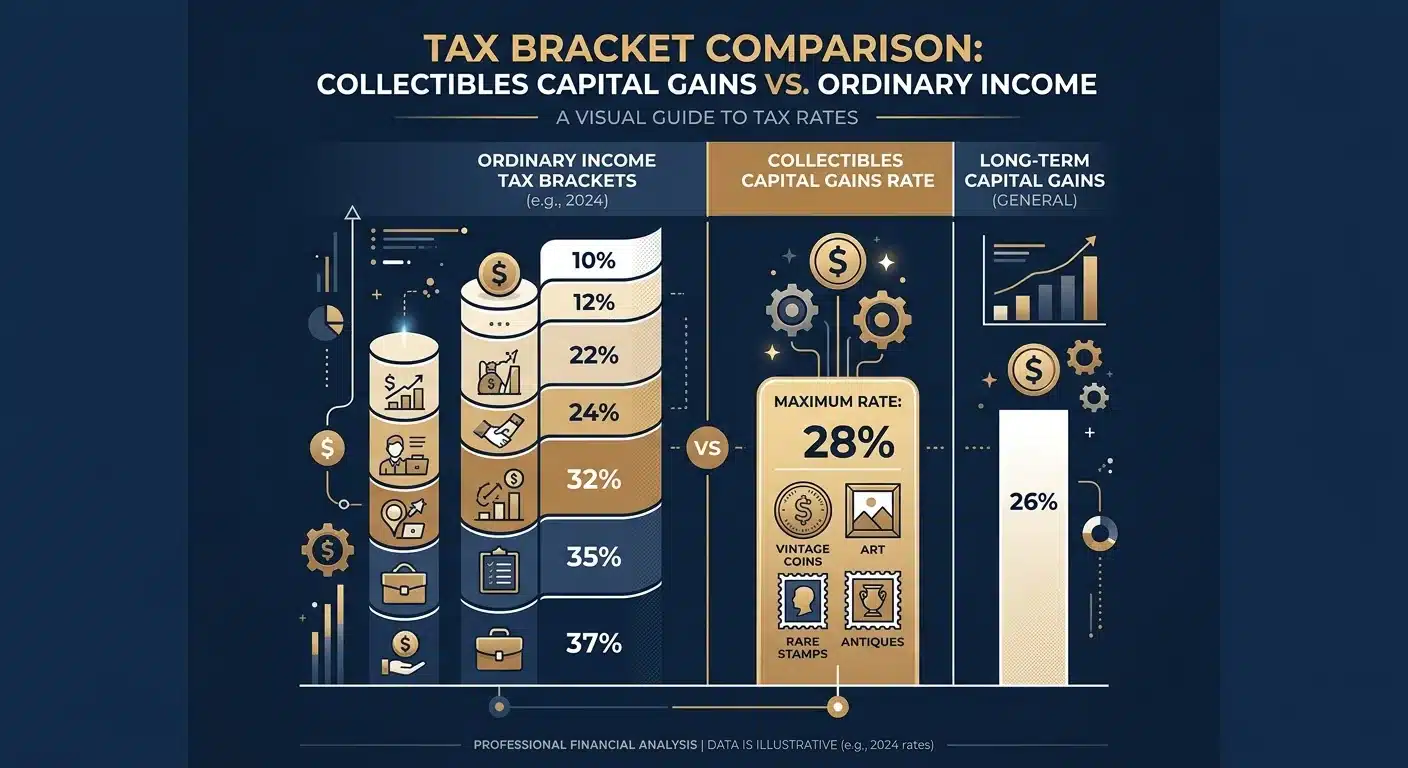

Profits from selling physical gold held for more than one year are taxed as collectibles at a maximum federal rate of 28%. Dealers are legally required to file IRS Form 8300 if a customer uses more than $10,000 in cash in a single transaction or related transactions. These are standard tax and reporting requirements.

The process itself is simple. The experience depends on whether the dealer treats the seller as someone who made a thoughtful decision or as a transaction to close quickly. Clarity matters. Transparency matters. The goal is to exit ownership with the same confidence used to enter it.

- The Simple Reality of Selling Physical Gold

- Who Actually Buys Your Gold Back?

- What Determines How Much You’ll Receive

- The Actual Process — Step by Step

- Tax Obligations You Need to Know

- Frequently Asked Questions

- How quickly can I get cash when I sell my physical gold?

- Will I get the full market spot price for my gold coins?

- What are the most common mistakes to avoid when selling gold for liquidity?

- Are there taxes on the profits when I sell my physical gold?

- What documents do I need to provide when selling my gold to a dealer?

- Is it better to sell gold to a local coin shop or a national online dealer?

- The Bottom Line

The Simple Reality of Selling Physical Gold

Most people who ask about selling aren’t really asking about the mechanics.

They’re asking: Will I get a fair price? Will this take months? Will someone pressure me into selling at the worst possible moment?

Those concerns are valid. And clarity matters more than speed every time.

The actual process is straightforward. You contact a dealer. They quote a price — the current spot price minus their spread. You ship your metals or bring them in. They verify weight and purity. You get paid. The entire timeline can be completed in under two weeks.

What derails people isn’t the process.

It’s opaque pricing. It’s manufactured urgency. It’s being treated like a panicked seller instead of someone who made a deliberate choice to own something real.

The question isn’t whether you can sell your gold when you need to.

It’s whether you’ll feel as confident walking out of ownership as you did acquiring physical metals.

Confidence comes from clarity — not jargon, not complexity.

A reputable dealer explains pricing upfront. They don’t invent urgency. They don’t treat your decision to sell as weakness or panic.

They walk you through shipping or drop-off, verification, payment timing — so you know exactly what happens next.

This isn’t about squeezing every last dollar from a one-time sale.

It’s about working with someone who treats you on the way out the same way you were treated on the way in — like someone who values ownership and wants control of the process.

If that’s the experience you had buying, that’s the experience you deserve selling.

Who Actually Buys Your Gold Back?

Here’s a question most people don’t ask until they need to: who’s on the other side of the transaction when you decide to sell?

It’s not the government. It’s not a bank. And it’s not the entity that minted the coins.

The answer matters — because knowing who you’re dealing with tells you whether the process will feel simple or deliberately opaque.

The U.S. Mint Does Not Buy Back Bullion

If you’re holding American Eagles or other U.S.-minted products, here’s the thing most people assume incorrectly.

The U.S. Mint doesn’t buy back its bullion products. They produce the coins. They don’t participate in the resale market.

So when you sell, you’re working with private dealers — not a government window.

That’s not a flaw. That’s how the market works.

Reputable Dealers and Buyers

Your buyers are precious metals dealers — local, national, or online.

They purchase coins, bars, and rounds based on current market pricing, authenticity, and condition. Brighton Gold is one of those buyers. So are APMEX, JM Bullion, and regional coin dealers who’ve operated for decades.

The distinction you’re looking for isn’t dealer versus non-dealer.

It’s transparent dealer versus opaque one. The Federal Trade Commission explicitly warns consumers against dealers who use high-pressure tactics to create a false sense of urgency.

That’s not a caution. That’s the disqualifier.

A reputable buyer doesn’t push you to sell today. They don’t tell you prices are crashing unless you act right now.

They explain the process, show you current pricing, and let you decide.

If it feels like a sales pitch instead of a service — leave.

What Determines How Much You’ll Receive

Most people who ask about selling gold aren’t really asking about the process.

They’re asking: Will I get a fair price?

And that’s a better question — because fair doesn’t mean full spot, and it never has.

The price you receive when you sell physical gold comes down to three things: the current market price for gold, the dealer’s spread, and what you’re selling.

None of it’s hidden. None of it’s arbitrary.

And none of it should surprise you if the dealer explains it upfront.

Spot Price and the Bid-Ask Spread

Here’s how it works.

Gold’s spot price — the current spot price of gold — is the baseline. That’s the live market price for one troy ounce of pure gold. When a dealer quotes you a buy price, they’re quoting below spot.

The difference is the spread.

The spread covers the dealer’s operating costs, verification expenses, and the risk they’re taking on holding inventory.

It’s not a penalty. It’s the cost of liquidity.

For most precious metals dealers, the spread ranges from 2% to 15% depending on market conditions, the product you’re selling, and the dealer’s business model.

What separates a reputable dealer from one you should avoid?

The reputable dealer tells you the spread before you ship anything. They explain what it covers. They don’t treat it like a negotiation or a secret.

If you’re being quoted a price and the dealer won’t explain how they arrived at it — that’s not transparency. That’s opacity dressed up as efficiency.

Condition and Product Type

Not all gold sells for the same price, even at the same weight.

A Gold American Eagle in mint condition sells for more than a scratched-up foreign coin of the same weight. Why? Liquidity. Recognizability. Demand.

Dealers pay more for products they can turn around quickly — and U.S.-minted coins are at the top of that list.

Condition matters too.

Coins in original mint packaging, bars with intact assay cards, and bullion that hasn’t been damaged or altered — all of that commands a higher buy price.

It’s not about vanity. It’s about the next buyer’s confidence. The easier your product is to verify and resell, the closer your payout gets to spot minus the standard spread.

| Factor | Impact on Offer | What It Means for You |

|---|---|---|

| Current spot price of gold | Sets the baseline for all dealer offers | The live market price is your starting point — dealers quote below spot, not above it |

| Dealer spread | Determines how far below spot you’ll be paid | Covers operating costs and inventory risk — transparency here separates reputable dealers from operators |

| Product type and recognizability | Higher demand products command higher buy prices | U.S.-minted coins sell faster and easier than foreign or generic bullion — dealers pay more for liquidity |

| Condition and packaging | Mint condition with original packaging increases offer | Intact assay cards, undamaged coins, and sealed packaging signal authenticity and resale confidence |

| Weight and purity verification | Dealers verify before finalizing payment | Your quoted price is confirmed only after the dealer tests and weighs your metals |

| Market volatility and timing | Wider spreads during unstable markets | Dealers adjust spreads when prices swing rapidly — not because they’re taking advantage, but because they’re managing risk |

The Actual Process — Step by Step

You know what you’re selling and what it’s worth. Here’s how it actually works.

The mechanics aren’t complicated. There’s no maze.

What separates a smooth transaction from a frustrating one is transparency — and a dealer who treats you like someone who made a thoughtful decision, not a target.

Contact the Dealer

Start by reaching out to a reputable dealer.

That means someone who doesn’t manufacture urgency. Who doesn’t imply you’re losing money by waiting. Who doesn’t treat your inquiry like a closing bell.

You’ll provide basic information — what you’re selling, quantity, condition.

A professional dealer quotes you a buy price based on the current spot price minus their spread. They explain how they arrived at that number. They tell you what happens next.

If they won’t explain their pricing model or they’re pushing you to commit before you’ve had time to think — that’s not clarity. That’s pressure.

And pressure is exactly what Federal Trade Commission guidance warns you to avoid.

Verify and Ship

Once you’ve accepted the offer, you’ll ship your metals or drop them off in person if the dealer has a physical location.

Most dealers provide insured shipping labels if you’re sending your gold. That’s standard. It’s not a red flag — it’s how the gold purchasing and delivery process works in reverse.

Before you ship, document everything.

Photograph your coins or bars. Record serial numbers if applicable. Note any original packaging or assay cards you’re including.

This isn’t paranoia. It’s good practice. You’re creating a record so there’s no ambiguity on the other end.

Reputable dealers confirm receipt as soon as your shipment arrives.

You’ll know it got there. You’ll know when inspection starts. You won’t be left wondering whether your package is sitting in a warehouse somewhere.

Inspection and Offer

The dealer verifies what you sent — weight, purity, condition. They’re confirming that what arrived matches what you described.

This step usually takes one to two business days. If there’s a discrepancy — say, a coin’s condition was overstated or a bar doesn’t match its assay card — the dealer contacts you before moving forward.

Once verification is complete, you receive a formal offer.

If it matches the quote you accepted, you approve it and payment processing begins. If market conditions shifted between your initial quote and the inspection — and some dealers lock prices while others quote live — you’ll have the option to accept the revised offer or request your metals back.

A trustworthy dealer doesn’t penalize you for walking away.

Payment

Payment arrives within a few business days of your approval.

Most dealers offer wire transfer, ACH, or check. Wire is fastest. ACH takes a few days. Checks take longer.

Choose what works for your timeline.

From first contact to payment in your account, the entire process can often be completed in under two weeks.

That’s not a promise. It’s typical timing when both sides operate with clarity and follow-through.

The question isn’t whether you can sell your gold when you need to. It’s whether you’ll feel as confident walking out of ownership as you did walking in.

That confidence comes from clarity, not complexity.

| Step | Typical Timeline | What Happens |

|---|---|---|

| Initial contact and quote request | Same day | You contact the dealer with details about what you’re selling — product type, weight, quantity. The dealer provides a preliminary offer based on current spot price and your metal’s specifications. |

| Quote review and acceptance | 1–2 days | You review the offer. Reputable dealers hold quotes for a defined window so you’re not pressured. Once you accept, the transaction is locked in and shipping or drop-off logistics are confirmed. |

| Shipping or in-person delivery | 2–5 days | If shipping, the dealer provides insured packaging instructions. Your metal ships fully insured. In-person delivery happens at the dealer’s location — faster, no transit risk. |

| Verification and authentication | 1–2 days after receipt | The dealer weighs, tests, and authenticates your metal. U.S.-minted coins typically clear faster than bars or foreign bullion. Any discrepancies are flagged before payment is finalized. |

| Payment processing | 1–3 business days after verification | Payment is issued by wire transfer, ACH, or check. Wire is fastest — often same day. ACH typically clears in 2–3 days. Checks take longer depending on postal transit and bank hold policies. |

| Total process (end to end) | Under 2 weeks in most cases | From first contact to funds in your account — assuming both parties operate with clarity and follow-through. Delays typically come from shipping transit or authentication issues, not dealer processing. |

Tax Obligations You Need to Know

Here’s what most people don’t expect: selling gold isn’t like selling stock.

You can’t just report the gain and move on.

It’s taxed as collectibles — a completely different category with different rules and different rates.

And different surprises if you walk in unprepared.

Gold Is Taxed as a Collectible

Hold your gold more than one year and your profit gets taxed at a maximum federal rate of 28%.

That’s higher than the long-term capital gains rate on stocks or mutual funds — and most people don’t find out until they’re sitting across from their accountant.

Shorter holding periods? You’re taxed at your ordinary income rate — whatever bracket you’re in.

The IRS treats gold the same way it treats art, antiques, or rare coins.

No special exemption. No escape hatch.

This isn’t a loophole you can plan around — it’s the structure.

Brighton Gold doesn’t provide tax advice. That’s your CPA‘s job. But we make sure you know what questions to ask before you sell, not after you’ve already signed.

IRS Reporting Requirements

There’s another layer most first-time sellers don’t see coming.

IRS reporting requirements — and dealers filing IRS Form 8300 directly with the government.

Dealers aren’t just middlemen. They’re mandatory reporters.

Sell using more than $10,000 in cash in a single transaction or related transactions, and the dealer files IRS Form 8300.

It’s not optional. It’s federal law.

Different products and transaction types trigger different reporting thresholds.

The specifics depend on what you’re selling, how much, and how you’re paid.

A reputable dealer tells you upfront what gets reported and why — before you commit to anything.

| Tax Scenario | Rate or Requirement | What You Need to Do |

|---|---|---|

| Selling physical gold held for more than one year | Maximum federal rate of 28% (collectibles rate) | Report the gain on your tax return as a collectible under long-term capital gains — consult your CPA for state and income-specific implications |

| Selling physical gold held for one year or less | Taxed at your ordinary income rate — same as wages | Report the gain as short-term capital gain — no preferential rate applies; your income bracket determines what you owe |

| Selling at a loss | Loss may offset other capital gains | Document your original purchase price and sale price — a capital loss can reduce your taxable gain elsewhere; consult your CPA for specifics |

| Cash transactions over $10,000 in a single or related transactions | Dealer files IRS Form 8300 | Provide accurate identification to the dealer — the form goes to the IRS automatically, and you must still report any gain or loss |

| Dealer-reportable sales (certain products and quantities) | Dealer files IRS Form 1099-B | Specific bullion products sold in defined quantities trigger mandatory dealer reporting — a reputable dealer discloses this before you commit to the transaction |

Frequently Asked Questions

You’ve seen the process. You’ve seen the timeline. You’ve seen the tax obligations.

Here’s what customers actually ask when they’re deciding whether to sell.

These aren’t abstract questions.

They’re the concerns that surface after the mechanics are clear — when you’re deciding whether selling feels as straightforward as you were told it’d be.

How quickly can I get cash when I sell my physical gold?

The entire process can often be completed in under two weeks. First contact to payment in your account.

It’s not a guarantee. It’s typical timing when both sides operate with clarity.

Wire transfers arrive fastest. ACH takes a few days. Checks take longer.

The dealer explains payment options before you approve the final offer. You choose what works for your timeline.

Will I get the full market spot price for my gold coins?

No. You won’t.

And you shouldn’t expect to.

Dealers quote you spot minus their spread. The spread often ranges from 2% to 15%. That’s how they stay in business.

It’s not hidden. A reputable dealer explains their pricing model before you ship anything.

If they won’t tell you how they arrived at their number, you’re not working with transparency. You’re working with someone who benefits from confusion.

What are the most common mistakes to avoid when selling gold for liquidity?

The biggest mistake is accepting the first offer without comparing.

You’ve held this gold for years. You waited for the right time to liquidate. Then you sell to the first dealer who answers the phone — without checking their spread, their reputation, or whether their pricing model makes sense.

The second mistake is shipping your metals before you understand the offer.

A reputable dealer explains how they price before you send anything. If they won’t tell you their spread until after your gold arrives, walk away.

The third mistake is prioritizing speed over clarity.

Selling in 48 hours sounds appealing. But if the process feels rushed, if the dealer won’t answer basic questions, if urgency is the only selling point — you’re not working with someone who respects what you own.

Are there taxes on the profits when I sell my physical gold?

Yes.

Profits from selling physical gold held for more than one year are taxed at a maximum federal rate of 28%.

That’s higher than the long-term capital gains rate on most stocks. Short-term gains are taxed as ordinary income.

The IRS treats gold as a collectible — not as a security. You report the gain or loss on your tax return.

A reputable dealer explains what gets reported before you finalize the sale.

What documents do I need to provide when selling my gold to a dealer?

Most dealers don’t ask for much when you’re selling standard bullion.

You’ll provide basic information about what you’re selling. Quantity. Condition. Product type.

If you’re selling rare or numismatic coins, you might need original assay cards or certificates of authenticity. For standard bullion, the dealer verifies weight and purity on their end.

They don’t need your purchase receipt. They don’t need proof of where you bought it.

A professional dealer tells you what they need upfront.

Is it better to sell gold to a local coin shop or a national online dealer?

It depends on what you value.

Local coin shops offer immediacy. You walk in. They evaluate your metals. You walk out with cash or a check.

National online dealers often offer better pricing. Their overhead is lower. They provide insured shipping. They explain the process in writing.

There’s no single right answer. The question is whether you prioritize speed or pricing transparency.

Both can be reputable. Both can be frustrating.

The difference is how they treat you during the process.

The Bottom Line

You don’t need to guess whether selling your physical gold is complicated.

It isn’t.

You contact a dealer. You get a quote — spot price minus their spread. You ship or drop off. They verify. You approve the final offer. Payment arrives.

Start to finish? Days. Not months.

The mechanics were never the hard part.

What separates a confident seller from a frustrated one isn’t knowing the spot price or memorizing tax brackets.

It’s clarity.

Did the dealer explain their pricing before you shipped? Did they walk you through each step? Did they treat the sale as a transaction they’re completing with you — or a closing they’re running on you?

The difference isn’t subtle.

And it’s the same difference that mattered when you decided to buy gold in the first place. You wanted something real. Something you could hold. Something that didn’t depend on a bank’s promises or a government’s solvency.

Selling shouldn’t feel like you’re undoing that decision.

It should feel like you’re using the liquidity that ownership always provided.

The question isn’t whether you can sell your gold when you need to.

You can.

The question is whether you’ll feel as confident walking out of ownership as you did walking in.

That confidence doesn’t come from complexity. It doesn’t come from jargon or opaque pricing or dealers who manufacture urgency.

It comes from working with someone who treats the process the way Brighton Gold treats it — as a concierge experience built on transparency, calm guidance, and respect for the decision you made.

You chose to own something tangible.

When you liquidate it, that choice should be validated — not regretted.

If you’re still holding physical gold — or if you’ve been thinking about adding it to your retirement picture — the real question isn’t whether you can sell when you need to. It’s whether you’ll feel as confident walking out of ownership as you did walking in. Brighton Gold offers a complimentary consultation to walk you through your options — including how the No Fee Precious Metals IRA works and whether you qualify. No pressure. No urgency. Just the clearest picture we can give you of what ownership looks like from start to finish.