Yes—physical gold offers protections that paper alternatives simply can’t match.

Here’s what it comes down to: when you own physical gold, you own it outright. There’s no middleman. No custodian who might fail. No fund manager making decisions on your behalf.

With gold testing $5,000 per ounce in early 2026—up over 65% from a year ago—more Americans are asking a simple question: Does my gold actually exist?

The answer depends entirely on how you hold it.

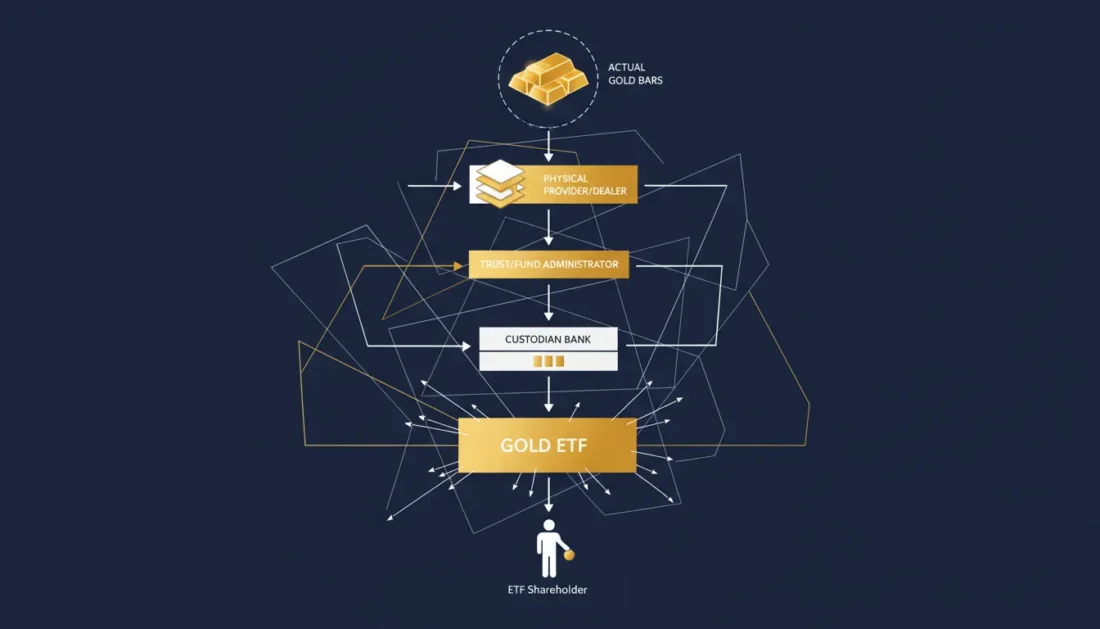

Gold ETFs like GLD and IAU offer convenience. You can buy and sell with a few clicks. But here’s the thing most people don’t realize: you’re not actually buying gold. You’re buying shares in a trust that claims to hold gold on your behalf.

You can’t request delivery. You can’t visit a vault and see your bars. And if something goes wrong with the fund, the custodian, or the broader financial system? You’re an unsecured creditor standing in line with everyone else.

Gold mining stocks? That’s a different kind of risk altogether. You’re betting on a company’s ability to pull gold out of the ground profitably—subject to management decisions, labor disputes, environmental rules, and political instability in mining regions around the world.

Physical gold removes these concerns entirely.

When you hold coins or bars in an IRS-approved depository—or in your hands through direct delivery—that metal is yours. Period.

It’s why tangible ownership vs. digital exposure has become such a critical consideration for retirement-focused customers in 2026.

This article breaks down the real differences—counterparty risk, tax treatment, accessibility, and what central banks understand that most Americans don’t.

Understanding Counterparty Risk: The Hidden Danger in Paper Gold

Counterparty risk is simple: it’s the chance that someone you’re depending on won’t hold up their end of the deal.

With physical gold, counterparty risk is essentially zero. The metal in your possession—or held in your name at an IRS-approved depository—doesn’t depend on any third party to exist or be accessible.

Paper gold? That’s a different story.

What Gold ETF Prospectuses Actually Say

Most people never read the fine print.

But buried in the SPDR Gold Trust (GLD) prospectus are statements that should give any thoughtful person pause:

- If gold is lost, damaged, stolen, or destroyed — The responsible party “may not have the financial resources sufficient to satisfy the Trust’s claim.”

- If the Custodian becomes insolvent — Its assets “may not be adequate to satisfy a claim by the Trust or any Authorized Participant.” There may also be “delay and costs incurred in identifying the gold bars.”

- Unallocated gold accounts — Gold held in unallocated accounts “is not segregated from the Custodian’s assets.” If the custodian fails, you become an unsecured creditor.

This isn’t speculation. It’s disclosure language required by SEC exchange-traded product guidelines.

The Custody Chain Problem

Here’s what happens when you buy shares of GLD:

- The fund’s trustee (Bank of New York Mellon) oversees operations

- The custodian (HSBC and JPMorgan) stores the gold

- Subcustodians may store additional portions in various global locations

- Sub-subcustodians operate without written custody agreements

- Authorized Participants handle share creation and redemption

Each layer introduces potential failure points. Each additional party dilutes accountability.

And here’s what surprises most people: you can’t redeem your shares for physical gold.

Only Authorized Participants—large financial institutions—can redeem shares, and only in “baskets” of 100,000 shares at a time. For individual shareholders, there’s no path to physical delivery.

Why This Matters More in 2026

The 2008 financial crisis showed how quickly institutions can fail. During the banking stress of 2023, several regional banks collapsed within days.

Gold ETFs are designed for normal market conditions.

But people don’t buy gold for normal conditions—they buy it for uncertainty. For protection. For peace of mind.

Physical gold, held in segregated storage with direct ownership, removes the entire custody chain from the equation. When you understand gold IRA fee structures, you’ll often find that the peace of mind of direct ownership costs less than expected.

| Feature | Physical Gold (IRA) | Gold ETF (GLD/IAU) | Gold Mining Stocks |

|---|---|---|---|

| Counterparty Risk | None (direct ownership) | Multiple layers | Company + market |

| Redeem for Metal | Yes | No (only Authorized Participants) | No |

| Custody Chain | Single depository | Custodian → Subcustodians | N/A |

| Insolvency Protection | Metal remains yours | Unsecured creditor | Equity holder |

| You Own | Specific bars/coins | Shares in a trust | Stock certificates |

Gold Mining Stocks: Leveraged Exposure with Amplified Risk

Mining stocks seem attractive at first glance.

When gold rises, mining company profits can surge—providing “leverage” to the gold price.

But that leverage cuts both ways. And the risks extend far beyond what happens to gold itself.

Operational Risks That Don’t Affect Physical Gold

Gold miners face challenges that have nothing to do with the price of gold:

- Cost inflation — Labor, energy, and equipment costs can squeeze margins even when gold prices rise. The industry has seen significant cost pressures in 2025-2026.

- Declining ore grades — Mines produce less gold per tonne of rock processed over time. That means more spending just to maintain production levels.

- Geopolitical instability — Major gold deposits are located in regions with political risk, including parts of Africa, South America, and Central Asia. Regulatory changes, nationalization threats, and civil unrest can impact operations overnight.

- Environmental and regulatory challenges — Permitting delays, environmental cleanup requirements, and changing rules can halt or delay production for years.

- Management decisions — Poor capital allocation, failed acquisitions, or operational missteps can destroy shareholder value regardless of gold prices.

In 2025, the FTSE Global Precious Metals & Mining Index rose 86%—far outpacing broader markets. But that performance came with severe volatility and concentrated in a handful of companies that successfully managed these operational challenges.

The Correlation Breakdown

Mining stocks often move with broader equity markets, not just gold prices.

During the 2008 financial crisis, gold rose while mining stocks fell. During the COVID crash of March 2020, both gold and miners dropped initially—even though gold recovered quickly, miners took longer.

What does this mean for you?

If you’re buying gold specifically to reduce correlation with traditional markets, mining stocks may not provide the protection you expect.

Physical gold, by contrast, has maintained its intrinsic value through every financial crisis in recorded history—precisely because it doesn’t depend on any company’s performance.

Junior Miners: Higher Risk, Unproven Reward

Junior mining companies—smaller firms searching for new deposits—carry even greater risk:

- Pre-revenue operations — Most juniors don’t produce gold yet. They burn cash while searching for economically viable deposits.

- Financing risk — They depend on capital markets for funding. When money gets tight, juniors often can’t complete exploration or development.

- Execution risk — Moving from discovery to production requires years and billions of dollars. Many projects never make it.

Successful junior miners can generate substantial returns. But the failure rate is high, and losses can be total.

| Risk Factor | Physical Gold | Gold ETF | Senior Miners | Junior Miners |

|---|---|---|---|---|

| Gold Price | Direct exposure | Direct exposure | Leveraged | Highly Leveraged |

| Operational Risk | None | None | Moderate | High |

| Management Risk | None | Fund manager | Moderate | High |

| Geopolitical Risk | None (U.S. storage) | Custody locations | Mining locations | Mining locations |

| Financing Risk | None | None | Low | Very High |

| Equity Market Correlation | Low | Low | Moderate | High |

Tax Treatment: What You Need to Know

Tax treatment varies significantly depending on how you hold gold—and where you hold it matters even more.

Here’s what we’re seeing in 2026.

Outside Retirement Accounts

The IRS classifies gold—whether physical or in ETF form—as a “collectible.” This means different rules apply.

- Physical gold and gold ETF gains — Taxed at a maximum 28% long-term capital gains rate (compared to 0%, 15%, or 20% for regular securities)

- Mining stocks — Taxed at standard long-term capital gains rates of 0%, 15%, or 20% depending on income

- Short-term gains — All gold-related gains held less than one year are taxed as ordinary income (up to 37%)

This creates an interesting dynamic: if you’re holding gold outside a retirement account and paying taxes on gains, mining stocks receive more favorable treatment than physical gold or ETFs.

But that tax advantage comes with all the operational and market risks we discussed above.

Inside Retirement Accounts: The Game Changer

When you hold physical gold inside a properly structured Precious Metals IRA, tax treatment changes dramatically.

- Traditional IRA — Gains grow tax-deferred. You pay ordinary income tax when you take distributions in retirement—often at a lower rate than your working years.

- Roth IRA — Contributions are made with after-tax dollars, but qualified distributions—including all gains—are completely tax-free.

- No collectibles rate — Within an IRA, there’s no 28% collectibles rate. The gain simply becomes part of your distribution, taxed (or not) according to your account type.

This is why establishing a precious metals IRA has become such a popular strategy for retirement-focused customers. You get the security of physical ownership plus the tax advantages of a retirement account.

IRS Requirements for IRA-Eligible Gold

Not all gold qualifies for IRA inclusion.

Section 408(m) of the Internal Revenue Code sets specific standards:

- Purity requirements — Gold must be at least 99.5% pure (0.995 fineness). Silver requires 99.9% purity.

- American Gold Eagle exception — The only exception is the American Gold Eagle, which is 91.67% pure but specifically approved by Congress.

- IRS-approved storage — Personal possession by the IRA owner is prohibited. Gold must be held by an IRS-approved trustee at an approved depository.

- No collectibles — Rare coins, graded coins, and numismatic items are not eligible regardless of gold content.

When you’re acquiring U.S.-minted gold coins for an IRA, the American Gold Eagle and American Gold Buffalo are the most popular choices—backed by the U.S. government and widely recognized.

| Tax Scenario | Physical Gold (Taxable) | Physical Gold (IRA) | Gold ETF | Mining Stocks |

|---|---|---|---|---|

| Long-Term Capital Gains | 28% max | Tax-deferred/Tax-free | 28% max | 0-20% |

| Short-Term Capital Gains | Ordinary income | N/A | Ordinary income | Ordinary income |

| Within Traditional IRA | Tax-deferred | Tax-deferred | Not typically held | Tax-deferred |

| Within Roth IRA | Tax-free | Tax-free | Not typically held | Tax-free |

| Estate Treatment | Stepped-up basis | Inherited IRA rules | Stepped-up basis | Stepped-up basis |

What Central Banks Understand That Most Americans Don’t

Here’s something that doesn’t get enough attention: the world’s central banks are buying gold at the fastest pace in 50 years.

And they’re not buying ETF shares or mining stocks.

They’re demanding physical delivery.

The Numbers Are Staggering

According to the World Gold Council, central banks have purchased over 1,000 tonnes of gold annually since 2022—more than double the 2010-2021 average of 473 tonnes per year.

In 2024 alone, central banks bought 1,045 tonnes. Poland, India, and Turkey led the buying.

The trend continues into 2025 and 2026. Year-to-date net purchases through November 2025 totaled over 250 tonnes, with Poland (83 tonnes), Kazakhstan (41 tonnes), and Brazil (43 tonnes) among the largest buyers.

Most significantly, the World Gold Council’s 2025 Central Bank Gold Reserves Survey showed:

- 95% of respondents expect global gold reserves to increase in the coming year

- 43% anticipate increases in their own reserves

- Zero respondents expected any decline in gold holdings

Why does this matter to you?

Why Physical, Not Paper?

Central banks could easily hold gold through ETFs or futures contracts. It would be more convenient and cheaper to manage.

But they don’t.

They understand that paper claims can be frozen, seized, or become worthless during geopolitical stress. The 2022 freezing of Russian central bank reserves held in Western institutions was a wake-up call for monetary authorities worldwide.

Physical gold, held in sovereign vaults or trusted locations, can’t be digitally frozen or sanctioned.

It’s why emerging market central banks—particularly China, which has reported 13 consecutive months of gold purchases—are building physical reserves.

The Signal for Individual Owners

If the institutions responsible for managing global monetary systems are choosing physical gold over paper alternatives, that’s worth paying attention to.

They’re not speculating on price movements. They’re building structural reserves for long-term security.

Individual owners seeking the same clarity and control can follow the same principle: own the metal, not a claim on it.

Liquidity and Accessibility: Separating Fact from Misconception

One common argument for ETFs is liquidity. You can sell GLD shares in seconds through your brokerage account.

But this argument deserves a closer look.

ETF Liquidity Has Limits

ETFs are liquid in normal market conditions.

But “normal” isn’t when most people need access to their gold.

During the COVID market panic of March 2020, ETF prices briefly diverged significantly from the underlying gold value. Trading volumes spiked, but bid-ask spreads widened.

In a true financial crisis, ETF liquidity could be tested further. Remember: you can’t redeem your shares for physical gold. You can only sell them on the exchange—and someone has to be willing to buy.

Physical Gold Is More Accessible Than You Think

Modern precious metals IRAs and dealers have made physical gold highly accessible:

- Buying — Place an order and lock in your price. Brighton handles logistics from there.

- Storage — IRS-approved depositories provide secure, insured storage. Your specific bars and coins are segregated and documented.

- Selling — Reputable dealers, including Brighton, can facilitate sales when you’re ready. Pricing is transparent based on spot markets.

- Delivery — You can take physical delivery of your gold at any time (outside an IRA) if you prefer home storage.

The process isn’t instant like clicking “sell” on a brokerage screen.

But when you’re talking about wealth preservation for retirement, does a few days matter?

For most people, the slight reduction in immediate liquidity is a worthwhile trade-off for direct ownership and the elimination of counterparty risk.

The IRA Liquidity Question

Within an IRA, both ETFs and physical gold are subject to the same distribution rules. You can’t access either without taking a distribution (and potentially paying taxes and penalties if you’re under 59½).

The difference is what happens when you do take a distribution:

- ETF — You receive cash from selling shares

- Physical gold IRA — You can receive cash OR take “in-kind” distribution of the actual metal

That second option—receiving your actual gold—is only available with physical holdings. It’s a flexibility that paper alternatives simply can’t match.

The Brighton Approach: Why Concierge Service Matters

Buying gold sounds simple.

The reality is more nuanced—especially when it involves retirement accounts.

This is where Brighton’s concierge approach makes a meaningful difference.

What “Concierge Service” Actually Means

We’re here to guide you through every step:

- Strategic guidance — Understanding which coins and bars fit your situation. U.S.-minted products like American Gold Eagles and Buffalos are IRA-eligible and widely recognized. Foreign products may or may not qualify depending on purity and minting.

- Compliance navigation — Ensuring your IRA is properly structured under IRS Section 408(m). Mistakes can result in immediate tax consequences and penalties.

- Custodian coordination — Working with trusted custodians to set up self-directed IRAs, coordinate transfers, and manage ongoing administration.

- Competitive pricing — Transparent pricing tied to spot markets. No hidden markups or confusing fee structures.

- Ongoing support — The relationship doesn’t end at purchase. Brighton provides support at every stage of ownership—before, during, and after the transaction.

Identifying Safe Gold IRA Practices

The precious metals IRA industry has its share of bad actors.

High-pressure sales tactics, inflated premiums, and misleading claims about “collectible” coins are unfortunately common.

When identifying safe gold IRA practices, look for:

- No pressure — Legitimate dealers don’t create artificial urgency

- Clear pricing — You should know exactly what you’re paying relative to spot prices

- Compliance focus — IRS rules are taken seriously, not treated as suggestions

- Educational approach — Good dealers want informed customers, not confused ones

Brighton takes a different approach: education first, decision when you’re ready.

The No Fee IRA Advantage

One common concern about physical gold IRAs is the cost of custodial and storage fees.

Brighton addresses this directly with the No Fee Precious Metals IRA—covering custodial fees for the lifetime of the account on qualified purchases.

This means your gold grows without the drag of annual administrative costs eating into your holdings.

Combined with competitive product pricing, physical gold ownership becomes more cost-effective than many people assume.

Frequently Asked Questions

Can I trade my Gold ETF shares for physical gold?

Not directly as an individual shareholder.

ETF shares can only be redeemed for physical gold by Authorized Participants—large financial institutions—and only in massive blocks of 100,000 shares (called “baskets”). At current prices, that’s roughly $50 million worth of shares.

For individual owners, the only option is selling your ETF shares on the market and using the proceeds to purchase physical gold separately.

You never have a claim to any specific bar of gold while holding ETF shares.

What is counterparty risk in a Gold ETF?

Counterparty risk means your holdings depend on other parties fulfilling their obligations.

With gold ETFs, you’re trusting the fund manager, the trustee, the custodian, subcustodians, and in some cases sub-subcustodians to properly store, track, and provide access to gold on your behalf.

If any of these parties fail through insolvency, fraud, or operational breakdown, your holdings could be at risk.

The ETF prospectus explicitly states that in the event of custodian insolvency, you become an unsecured creditor—and recovery could be delayed and costly.

Are gold mining stocks a good alternative to physical gold?

Mining stocks provide leveraged exposure to gold prices—meaning they can rise faster than gold when prices increase.

But that leverage works both ways.

Mining companies face operational challenges including cost inflation, declining ore grades, management decisions, labor disputes, environmental regulations, and geopolitical instability in mining regions.

In 2025, top-performing miners generated exceptional returns. But the sector also saw significant failures and disappointments.

Mining stocks are an entirely different proposition than owning the metal itself.

How is the tax on physical gold different from gold stocks?

The IRS classifies gold as a “collectible.”

Long-term gains on physical gold and gold ETFs held outside retirement accounts are taxed at a maximum 28% rate—higher than the 0-20% rate for regular securities.

Mining stocks receive more favorable treatment, taxed at standard capital gains rates.

However, within a Precious Metals IRA, physical gold grows tax-deferred (Traditional IRA) or completely tax-free (Roth IRA). This eliminates the collectibles rate disadvantage entirely.

Is physical gold in an IRA more expensive than an ETF?

Physical gold IRAs involve custodial and storage fees—typically $150-$300 annually for most accounts.

ETFs charge expense ratios (GLD charges 0.40% annually, which increases with your account value).

However, Brighton offers a No Fee IRA for life on qualified purchases, eliminating ongoing custodial fees.

This makes physical gold ownership more cost-effective than many expect—while providing direct ownership, segregated storage, and zero counterparty risk.

What happens to my gold ETF if the custodian becomes insolvent?

According to prospectus disclosures, if the custodian becomes insolvent, “its assets may not be adequate to satisfy a claim by the Trust or any Authorized Participant.”

There may also be “delay and costs incurred in identifying the gold bars.”

Gold held in the ETF’s unallocated account isn’t segregated from the custodian’s assets. In insolvency, you become an unsecured creditor standing in line with other claimants.

Physical gold in an IRS-approved depository, by contrast, remains your property regardless of what happens to any financial institution.

It’s segregated, documented, and titled in your name.

Why are central banks buying physical gold instead of ETFs?

Central banks purchased over 1,000 tonnes annually from 2022-2024—and they’re demanding physical delivery, not paper claims.

They understand that paper promises can be frozen, seized, or become worthless during geopolitical stress.

The 2022 freezing of Russian central bank reserves—as documented by the Federal Reserve Bank of New York—demonstrated this clearly.

Physical gold, held in sovereign vaults, can’t be digitally sanctioned.

It’s why the World Gold Council’s 2025 survey showed 95% of central banks expect continued global gold accumulation—with zero respondents expecting declines.

Can I hold physical gold in my existing IRA or 401(k)?

Yes, through a self-directed IRA that permits precious metals.

You can roll over funds from an existing Traditional IRA, Roth IRA, 401(k), TSP, SEP IRA, or other qualified retirement account into a Precious Metals IRA—without taxes or penalties when done correctly as a direct rollover.

The gold must meet IRS purity requirements (99.5% for gold, with an exception for American Gold Eagles) and must be stored in an IRS-approved depository.

Personal possession of IRA-held gold is prohibited under Section 408(m).

Making the Right Choice for Your Situation

There’s no universal “best” way to hold gold.

The right choice depends on your goals, timeline, and what you’re trying to accomplish.

Here’s a simple framework:

ETFs make sense if you’re:

- Looking for short-term price exposure

- Planning to hold for weeks or months, not decades

- Comfortable with counterparty risk

- Not focused on crisis protection

Physical gold makes sense if you’re:

- Focused on long-term wealth preservation

- Planning for retirement or legacy

- Seeking protection from systemic financial risk

- Wanting direct ownership with no intermediaries

- Looking to step outside the traditional financial system

Mining stocks make sense if you’re:

- Seeking leveraged exposure to gold prices

- Comfortable with significant volatility and operational risk

- Willing to research individual companies or sectors

- Already holding a core position in physical gold and looking for additional exposure

Most retirement-focused customers find that physical gold—particularly within a Precious Metals IRA—provides the combination of security, tax advantages, and peace of mind they’re looking for.

For more details on precious metals industry terminology, Brighton’s glossary provides plain-language definitions of terms you’ll encounter.

Ready to Take the Next Step?

If you’re thinking “this all makes sense, but I don’t have time to figure it out on my own,” you’re not alone.

Most customers we work with felt the same way before they realized how straightforward the process can be with the right guidance.

That’s why we offer a complimentary consultation to walk you through your options—including our No Fee Precious Metals IRA, which covers custodial fees for the lifetime of the account on qualified purchases.

We’ll show you exactly:

- How the No Fee IRA works and whether you qualify

- The difference between U.S.-minted coins and foreign alternatives

- What to expect from the purchasing and delivery process

- How to roll over or transfer existing retirement funds

- What ongoing support looks like after your purchase

Learn About the No Fee IRA — no obligation, just actionable insights you can use whether you work with us or not.

In a world where paper claims depend on institutional promises, there’s something to be said for holding the real thing.

Physical gold doesn’t rely on anyone else’s balance sheet. It doesn’t require a functioning financial system to maintain its value. And it can’t be frozen, deleted, or defaulted on.

That’s the kind of clarity and control our customers are looking for in 2026—and it’s what Brighton has helped thousands of Americans achieve.