Here’s what the historical record shows: in five of the last six major U.S. recessions, gold prices went up while everything else went down.

That’s the quick answer.

But if you’re someone who’s spent decades building your retirement savings—and you’re watching the news right now wondering what happens next—you probably want more than the quick answer.

You want to know why gold tends to rise when the economy struggles. You want to know if this pattern holds up when you really need it to. And you want to know what it means for your situation specifically.

That’s what we’re going to walk through here.

We’ll look at what actually happened during every major downturn since the 1970s. We’ll explore why gold behaves the way it does—including a pattern that surprises most people. And we’ll cover what leading institutions are saying about where prices might be headed from here.

If you’ve been evaluating gold as a retirement strategy, this context can help you think through your options with clarity and confidence.

Gold’s Track Record During Every Major Downturn Since 1970

Let’s start with what we know for certain.

Since the U.S. moved away from the gold standard in 1971, there have been six major recessions. Gold gained ground in five of them.

The gains weren’t small, either. According to Bureau of Labor Statistics data and industry research, gold has averaged over 20% gains during official recession periods.

Here’s how each downturn played out:

The 1973-1975 Recession

This one followed the Vietnam War and the OPEC oil crisis.

Gold was newly free to trade on the open market after Nixon ended the gold standard. Prices tripled during this period—from $35 per ounce to over $180.

Now, some of that gain reflected the transition from fixed to market pricing. But the recession environment clearly supported gold’s rise.

The Early 1980s Double-Dip

Two back-to-back recessions hit in 1980 and 1981-1982. The Federal Reserve pushed interest rates above 21% to fight inflation.

Gold reached $850 per ounce in January 1980—its all-time high at the time. It pulled back during the recession itself, but remained dramatically higher than where it started the decade.

The 1990-1991 Recession

Here’s the one exception.

Gold prices actually declined modestly during this relatively mild downturn—dropping from around $400 to the $360 range.

Why? The early 1990s were unusual. The Cold War had just ended. Inflation was low. Central banks—especially the Bank of England—were actively selling their gold reserves.

The conditions that typically support gold during recessions simply weren’t present.

This matters because it reinforces an important point: gold doesn’t respond to recessions automatically. It responds to what usually accompanies recessions—currency concerns, monetary expansion, and financial system stress.

The 2001 Dot-Com Recession

The tech bubble collapsed. The NASDAQ fell 78% from its peak.

Gold started climbing during this period—a modest 5% gain during the recession itself. But that marked the beginning of a decade-long run that would eventually take prices above $1,900.

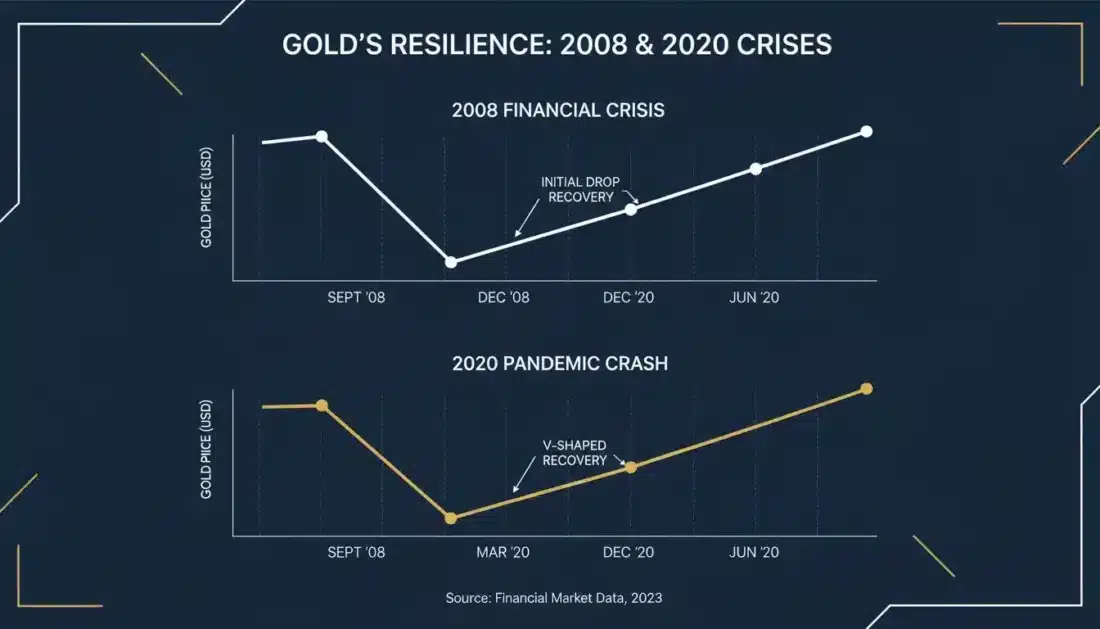

The 2008 Great Recession

This is where things get interesting.

Gold touched $1,011 per ounce in March 2008. Then Lehman Brothers collapsed—and gold dropped 28% to $730 by October.

Wait. Gold dropped during the worst financial crisis in generations?

Yes. Initially.

Here’s why: when institutions face margin calls and need cash immediately, they sell whatever they can. Gold is liquid. It gets sold.

But here’s what happened next.

From that October 2008 low, gold surged 78% within two years. By August 2011, it reached $1,917.90—a 163% gain from the crisis bottom.

The initial dip turned out to be the buying opportunity of a generation.

The 2020 COVID Recession

The pattern repeated almost exactly.

Gold started 2020 at $1,575. When markets crashed in mid-March, gold briefly dropped below $1,500.

Within months, it hit a new all-time high of $2,072.50.

The recovery happened much faster than 2008—months instead of years. Central banks responded with massive stimulus almost immediately, and that stimulus pushed gold higher.

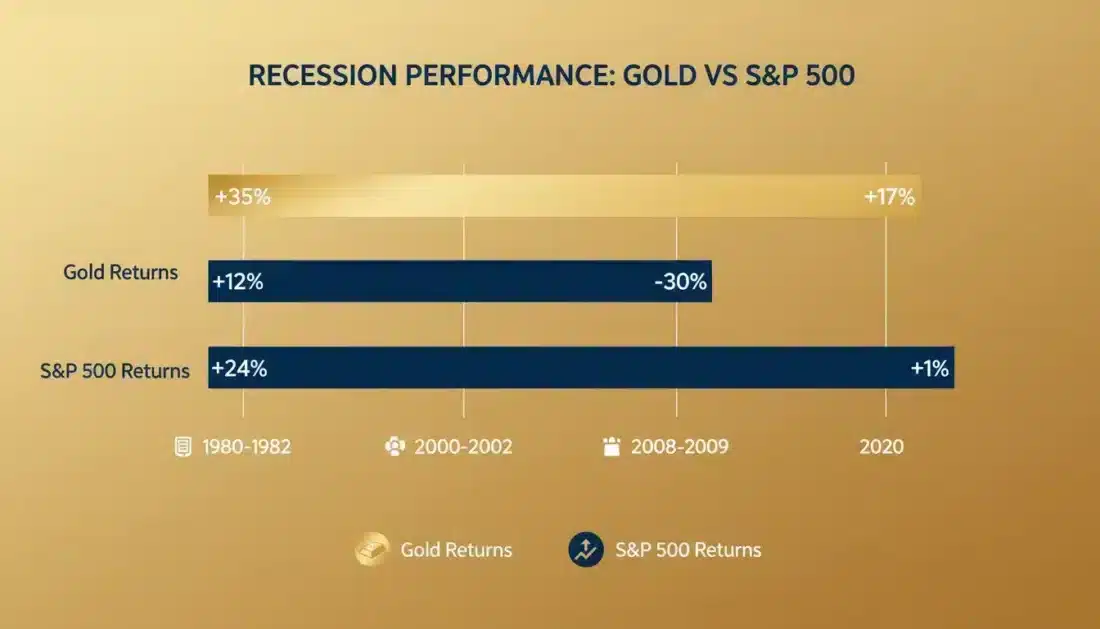

Comparing Gold and the Broader Market: What the Numbers Show

If you’ve spent years building your retirement in traditional accounts, here’s what you’re really wondering: does gold actually hold up when the broader market falls?

The short answer is yes—in most cases, it does more than hold up.

| Recession Period | Gold Performance | S&P 500 Performance | Difference |

|---|---|---|---|

| 1973-1975 | +73% | -48% | +121% |

| 1980-1982 | +23% | -27% | +50% |

| 1990-1991 | -9% | -3% | -6% |

| 2001 | +5% | -24% | +29% |

| 2007-2009 | +47% | -49% | +96% |

| 2020 | +32% | -34% (initial) | +66% |

The 1990-1991 period stands alone as the only time gold underperformed. Every other recession saw gold either hold steady while the market fell—or gain significant ground.

This is why so many people exploring the benefits of physical gold ownership are thinking about what it could mean for their retirement accounts.

It isn’t just about price appreciation. It’s about having something tangible that doesn’t depend on the same forces affecting everything else.

Why Does Gold Tend to Rise During Recessions?

Gold’s track record during downturns isn’t coincidence. There are specific reasons why this pattern holds.

When Paper Loses Value, Tangible Gains Appeal

Recessions shake confidence in paper-based assets.

During the 2008 crisis, the Producer Price Index for gold rose 12.8% in 2009 alone. According to the Bureau of Labor Statistics, purchasers were searching for something that would maintain value during economic contraction.

The same pattern emerged in 2020. And we’re seeing it again today.

When confidence in financial institutions wavers, tangible assets become more attractive.

Central Banks Print Money—and Gold Responds

Recessions trigger aggressive monetary responses.

Central banks cut interest rates. They inject liquidity through programs like quantitative easing. More dollars chasing the same amount of gold means higher gold prices.

From September 2010 to September 2011—following the Fed’s easing programs—gold prices jumped over 50%.

That wasn’t coincidence.

The Dollar Relationship

Gold and the U.S. dollar typically move in opposite directions.

When the dollar weakens—as it often does during recessions when the Fed is cutting rates and expanding the money supply—gold strengthens.

For people concerned about the purchasing power of their savings, this relationship offers a form of protection. When your dollars buy less, your gold typically buys more.

No Counterparty Risk

Here’s something that matters during a financial crisis.

Gold doesn’t depend on anyone else’s promise to pay.

When Lehman Brothers collapsed, bondholders lost billions. When banks fail, deposits above FDIC limits can be frozen. When governments default—as has happened in Argentina, Greece, and elsewhere—currency holders suffer.

Physical gold sits in a vault. It doesn’t rely on a bank’s solvency, a government’s creditworthiness, or a company’s balance sheet.

This characteristic becomes particularly valuable when the financial system itself is under stress.

What’s Different About the Current Environment?

The factors supporting gold today are unlike anything we’ve seen in decades.

This isn’t a typical cycle. Several structural shifts suggest something more permanent may be happening.

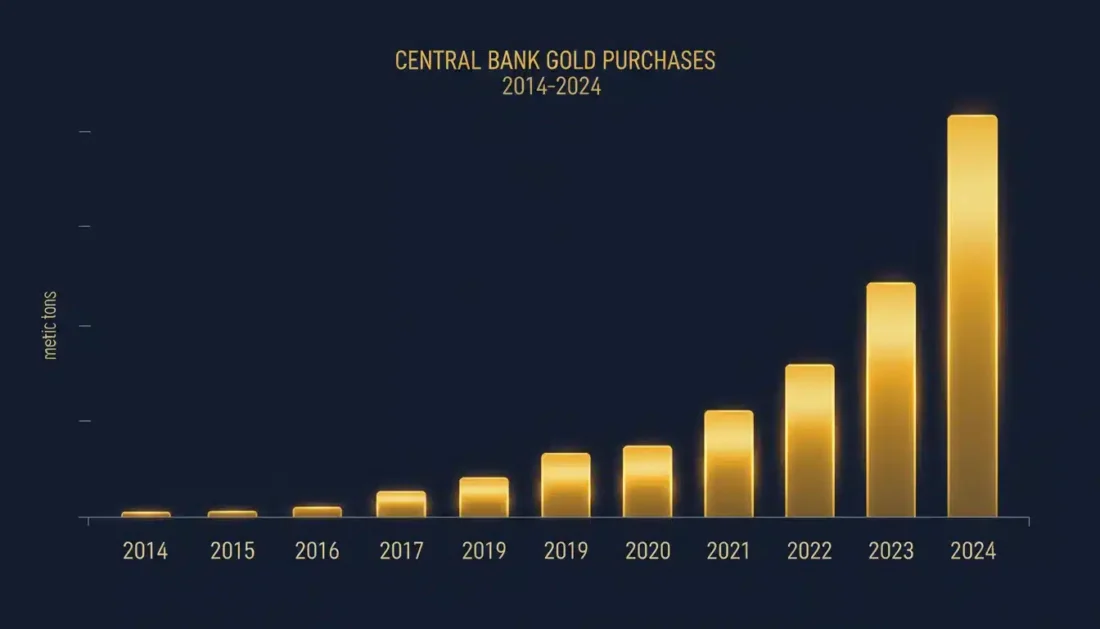

Central Banks Are Buying at Record Pace

Central banks purchased over 1,000 tonnes of gold in 2022, 2023, and 2024.

That’s far above the 473-tonne annual average from 2010-2021.

According to the World Gold Council, this represents a fundamental change in how reserve managers view gold.

| Period | Annual Central Bank Gold Purchases |

|---|---|

| 2014-2016 (3-year total) | 1,576 tonnes |

| 2022-2024 (3-year total) | 3,220 tonnes |

| Increase | +104% |

Poland’s central bank has been among the largest buyers. The Czech National Bank has purchased gold for 30 consecutive months. Brazil added 43 tonnes in just three months during late 2025.

The World Gold Council’s 2025 survey found that 95% of central bankers expect global gold reserves to continue increasing over the next 12 months.

None of those surveyed plan to reduce their holdings.

What do they know?

The Geopolitical Shift

After Western nations froze Russia’s foreign reserves in 2022, central banks worldwide took notice.

Gold can’t be frozen by a foreign government. It can’t be sanctioned. It can’t be switched off.

Countries from China to Turkey to Brazil are reconsidering how much of their reserves they want held in dollar-denominated assets.

The result is structural demand that’s unlikely to reverse regardless of short-term price movements.

The Debt Situation

U.S. government debt has surpassed $36 trillion.

Annual interest payments now exceed $1 trillion.

There’s no realistic path to surplus on the horizon.

Historically, when governments accumulate debt they can’t repay through growth or taxation, they repay it through inflation—effectively reducing the value of the currency over time.

Gold has served as protection against currency devaluation for thousands of years. That function hasn’t changed.

Where Do Experts See Gold Headed in 2026?

With gold trading above $5,000 per ounce in January 2026, many people are wondering: can prices really go higher?

Here’s what major financial institutions are forecasting:

| Institution | 2026 Gold Price Forecast |

|---|---|

| J.P. Morgan | $5,055 (Q4 average) |

| Goldman Sachs | $4,900 |

| Bank of America | $5,000 |

| Morgan Stanley | $4,400-$4,500 |

| Yardeni Research | $6,000 |

| J.P. Morgan (upside scenario) | $6,000+ |

According to J.P. Morgan Global Research, prices are expected to push toward $5,000 per ounce by Q4 2026, with $6,000 possible longer term.

The key factors these institutions cite:

- Central bank demand expected to remain elevated at around 755 tonnes annually

- ETF inflows projected at 250 tonnes for 2026

- Retail demand for bars and coins expected to exceed 1,200 tonnes annually

- Ongoing shift away from dollar-denominated reserves

Does this mean gold will definitely rise? No. Nothing in financial markets is certain. Gold can—and does—experience corrections.

But the structural factors supporting prices look different from previous cycles.

When you’re understanding gold IRA fee structures and thinking through your options, knowing what major institutions expect can help provide context.

Is a Recession Actually Coming?

If gold tends to rise during recessions, the natural question is: are we headed for one?

Economists are divided. But concern is clearly elevated.

| Institution | 2026 Recession Probability |

|---|---|

| J.P. Morgan | 40% |

| Moody’s Analytics | 42% |

| Goldman Sachs | 20% |

| RSM US | 30% |

| Bloomberg Consensus | 30-35% |

According to Goldman Sachs Research, the probability of a recession in the next 12 months has fallen from 30% to 20%.

J.P. Morgan Research maintains a higher 40% probability, citing trade tensions and policy uncertainty.

Here’s what’s worth noting: even the optimistic forecasters aren’t ruling out a downturn. They’re simply saying they don’t expect one as their base case.

A 20-42% probability range means we’re far from “all clear.”

For someone protecting retirement savings, the question isn’t just “will there be a recession?”

It’s “can I afford to be wrong if there is?”

The Pattern That Surprises People: Gold’s Initial Dip

One thing consistently catches people off guard when they first look at gold: it often drops at the start of a crisis before it rises.

Understanding this pattern is important if you’re considering physical gold.

The Liquidity Squeeze

In March 2008, gold touched $1,011.

By October, it had dropped to $730—a 28% decline during the worst financial crisis since the Great Depression.

In March 2020, gold fell briefly below $1,500 during the COVID crash.

Why?

In a severe liquidity crisis, everything liquid gets sold. Banks, hedge funds, and institutional players need cash immediately to meet margin calls. They sell whatever they can—including gold.

This creates a temporary disconnect between gold’s long-term value and its short-term price.

Why the Recovery Follows

Once the immediate cash crunch passes, gold’s fundamental value reasserts itself.

Central banks respond to crises with rate cuts and money printing—both supportive for gold. Fear increases demand for tangible assets. The dollar typically weakens.

In 2008, gold went from $730 to $1,917 within three years—a 163% gain.

In 2020, gold went from below $1,500 to over $2,000 within months.

What This Means for You

If you own gold and a crisis hits, don’t be surprised if prices temporarily drop.

That initial decline is typically short-lived. And gold’s recovery often exceeds the recovery in other assets.

This is also why many people considering precious metals look at comparing gold and silver acquisitions as part of a broader approach—flexibility within the metals space can be valuable.

What This Means for Retirement Savers

If you’re approaching retirement—or already there—you’re probably thinking through some practical questions right now.

What role could gold play in protecting what you’ve built?

And how does someone actually add physical gold to their holdings?

Physical Gold vs. Paper Alternatives

You can get gold exposure through ETFs, mining shares, or futures contracts.

But physical gold offers something paper alternatives don’t: actual ownership of a tangible asset.

During the 2020 crisis, something interesting happened. Paper gold prices briefly diverged from physical prices. People trying to buy actual coins and bars faced significant premiums—sometimes 10-20% above spot—because physical supply couldn’t keep up with demand.

When you own physical gold, you own something real. It doesn’t depend on an exchange staying open, a fund manager making good decisions, or a counterparty honoring their obligation.

Gold IRAs vs. Direct Purchase

There are two main paths to physical gold ownership:

Gold IRA (Self-Directed Precious Metals IRA):

- Tax-advantaged growth—same as traditional IRA

- Metals stored in IRS-approved depository

- Can roll over existing 401(k), 403(b), or IRA without taxes or penalties

- Must hold IRS-approved products like Gold American Eagles, Gold Buffalos, or certain bars

Direct Purchase:

- Take immediate physical possession

- No storage or custodian fees

- More flexible—can sell whenever you choose

- No tax advantages; capital gains apply

The right choice depends on your situation.

If you have significant retirement funds in existing accounts, a Gold IRA lets you move a portion into physical metals without triggering taxes.

If you want metals you can hold in your hands, direct purchase makes sense.

When identifying trustworthy gold IRA practices, working with a reputable dealer matters. The precious metals industry includes excellent providers—and some that aren’t. Due diligence is essential.

How Much Makes Sense?

There’s no universal answer.

Common guidance suggests 5-15% of retirement holdings in precious metals.

Too little, and the allocation doesn’t meaningfully protect against a market downturn. Too much, and you’re concentrated in a single area.

The specific percentage that makes sense depends on:

- Your age and timeline to retirement

- Other sources of income like pension or Social Security

- Your overall comfort with risk

- How you view the current economic environment

A conversation with a precious metals specialist can help you think through what aligns with your goals.

Choosing the Right Gold Products

Not all gold is the same when it comes to recession protection.

The form you choose matters for liquidity, authenticity, and—if you’re using an IRA—IRS compliance.

U.S.-Minted Coins

- Gold American Eagle: The most popular U.S. gold coin. Backed by the U.S. Mint for weight, content, and purity. IRA-approved. Highly liquid worldwide.

- Gold Buffalo: 24-karat pure gold. Also IRA-approved and minted by the U.S. Mint.

Both are easily recognized, simple to authenticate, and straightforward to sell anywhere in the world.

For most purchasers, these represent the most practical choice when choosing IRS-approved gold coins.

Gold Bars

Bars typically carry lower premiums over spot price than coins.

For larger acquisitions, this cost efficiency can be meaningful.

However, bars from less-recognized refiners can be harder to sell. If you go this route, stick with bars from LBMA-approved refiners.

What to Avoid

- Collectible or numismatic coins: These carry premiums for rarity that may not hold during a crisis. You’re paying for collectibility, not just gold content.

- Foreign coins with high premiums: Some foreign coins are excellent. Others carry premiums that aren’t justified by their gold content or liquidity.

- Fractional coins for large acquisitions: Smaller coins (1/10 oz, 1/4 oz) carry higher premiums per ounce. They’re fine for smaller amounts but less efficient for larger allocations.

Frequently Asked Questions

Does gold always go up when the market goes down?

Not always in the short term.

During severe market crashes like 2008 and 2020, gold initially dropped alongside the broader market as institutions sold everything liquid to raise cash.

However, gold typically recovers faster and gains more ground than equities during the broader recession period. In five of the last six major U.S. recessions, gold prices increased while the market declined.

How did gold perform during the 2008 financial crisis?

Gold showed a two-phase pattern in 2008.

It initially dropped 28% from March to October as institutions liquidated positions for cash during the Lehman Brothers collapse.

Then it surged 78% within two years—ultimately gaining 163% from the crisis low by August 2011 when it reached $1,917.90 per ounce.

Why do central banks buy gold before a recession?

Central banks purchase gold as a strategic reserve asset that holds value independent of any single currency or government.

Gold has no counterparty risk. It can’t default or be frozen by foreign governments.

Since 2022, central banks have purchased over 1,000 tonnes annually. According to the World Gold Council, 95% of surveyed central bankers expect global gold reserves to continue increasing.

What is the best gold coin to own for recession protection?

U.S.-minted coins like the Gold American Eagle and Gold Buffalo are popular choices for recession-minded purchasers.

These coins are IRA-approved, easily recognized worldwide, and backed by the U.S. Mint for weight and purity.

Their liquidity and authenticity make them straightforward to sell when needed—regardless of economic conditions.

Can I take physical delivery of my gold if the banks close during a recession?

Yes.

If you own physical gold outright—not in an IRA—you can take delivery at any time. It doesn’t depend on bank operations.

For Gold IRAs, the metals are held in an IRS-approved depository. You can request a distribution, though early withdrawals before age 59½ may incur taxes and penalties.

The key advantage of physical gold is that it exists outside the banking system.

Is gold at an all-time high too expensive to buy in 2026?

Gold reaching new highs doesn’t necessarily mean it’s overpriced.

Major institutions like J.P. Morgan forecast gold could reach $5,055 by Q4 2026, with some analysts seeing potential for $6,000.

The structural factors driving gold—central bank buying, dollar concerns, and geopolitical uncertainty—suggest current prices may represent a new floor rather than a temporary peak.

How much of my retirement should be in gold?

There’s no one-size-fits-all answer.

Many financial professionals suggest allocating between 5% and 15% of retirement holdings to precious metals.

The right amount depends on your age, risk tolerance, other holdings, and retirement timeline. A consultation with a precious metals specialist can help determine what makes sense for your specific situation.

What happens to gold IRAs during a recession?

Gold IRAs typically hold their value or appreciate during recessions—the opposite of what happens to most traditional retirement accounts.

The physical gold in your IRA is stored in a secure depository regardless of market conditions. Your ownership doesn’t change. Only the dollar value of your holdings fluctuates with the gold market.

The Bottom Line

Here’s what we know from five decades of data.

Gold has risen during five of the last six major U.S. recessions. The one exception—1990-1991—happened during an unusual period of low inflation, post-Cold War stability, and active central bank selling.

Today’s environment looks nothing like 1990.

Central banks are buying gold at record pace. Government debt has reached unprecedented levels. Geopolitical tensions have prompted a global rethinking of dollar-based reserves.

None of this tells us exactly what will happen next. Gold prices can and do fluctuate. The initial phase of a crisis often sees gold drop before recovering.

But for people concerned about protecting retirement savings from the next downturn—whenever it arrives—the historical record suggests physical gold deserves serious consideration.

The question isn’t whether gold will rise during the next recession. Based on five decades of data, it probably will.

The question is whether you’ll be positioned to benefit before that happens—or after it’s too late to act.

Precious metals may appreciate, depreciate, or remain unchanged depending on market conditions. Consult with a financial professional or tax professional for guidance specific to your situation.

Ready to explore how gold could fit into your retirement strategy?

If you’re thinking “this all makes sense, but I don’t have time to figure it out on my own,” you’re not alone.

Most customers we work with felt the same way before they realized how straightforward the process can be with the right guidance.

That’s why we offer a complimentary consultation to walk you through your options—including our No Fee Precious Metals IRA, which covers custodial fees for the lifetime of the account on qualified purchases.

We’ll show you exactly:

- How the No Fee IRA works and whether you qualify

- The difference between U.S.-minted coins and foreign alternatives

- What to expect from the purchasing and delivery process

- How to roll over or transfer existing retirement funds

- What ongoing support looks like after your purchase

Learn About the No Fee IRA—no obligation, just actionable insights you can use whether you work with us or not.

Peace of mind starts with clarity. And clarity starts with a conversation.