What Are the Risks of Storing Gold in a Bank Safe Deposit Box?

A bank safe deposit box is not a sanctuary. It's a lease.

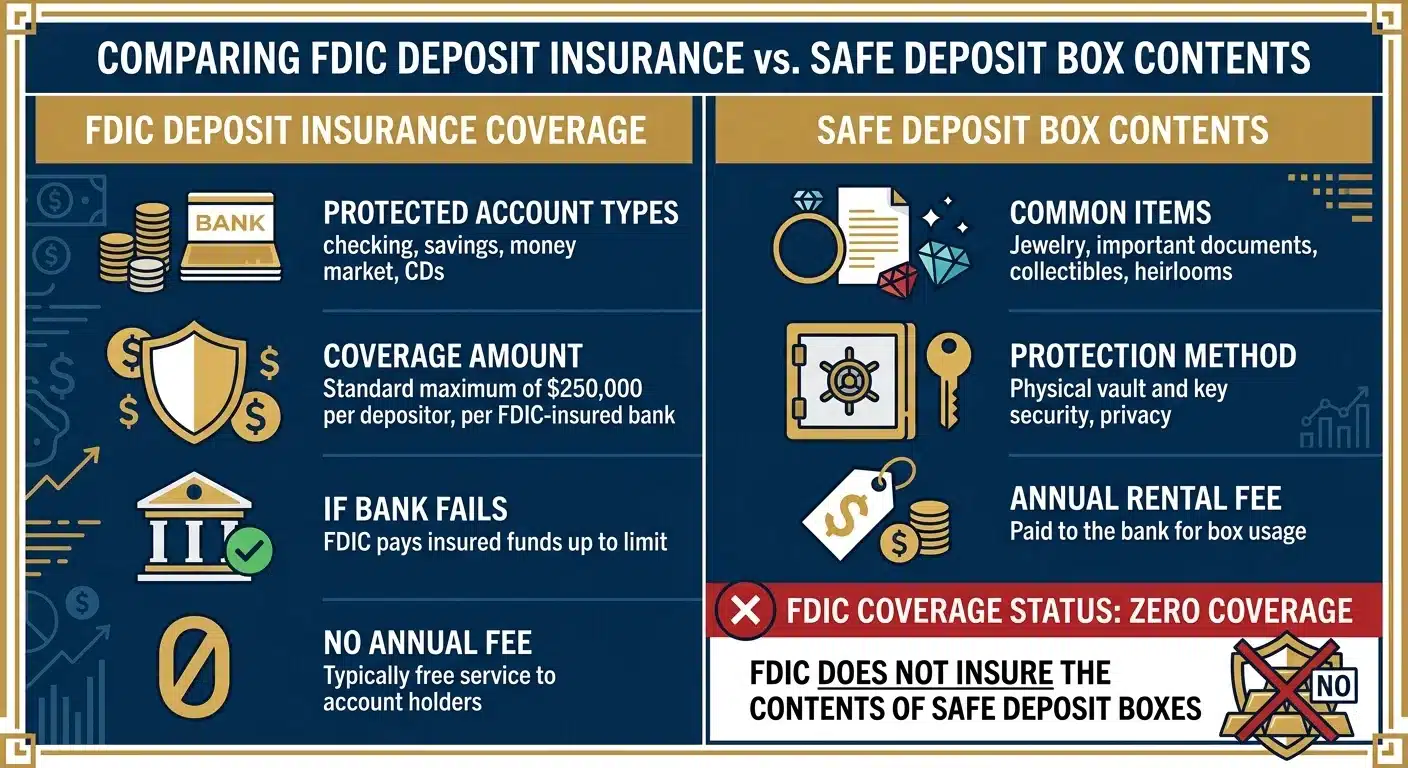

That distinction matters more than most gold owners realize. The legal framework of a safe deposit box is a landlord-tenant relationship — the bank assumes no fiduciary liability and keeps no official record of what's inside. FDIC deposit insurance covers exactly 0% of the physical contents stored in a safe deposit box. Gold, silver, coins, bars — none of it carries any federal protection if the box is damaged, robbed, or lost.

Access is the second structural problem. Safe deposit box access depends entirely on active retail branch operating hours. If the branch is closed — for any reason — the metals inside are completely unreachable. That is not a theoretical concern. The Emergency Banking Act of 1933 enforced a 4-day nationwide bank closure, during which 100% of physical access to all safe deposit boxes was suspended. Government and probate courts carry the same authority: a court can freeze access to a safe deposit box immediately upon the primary holder's death, creating legal complications that surviving family members are often unprepared to handle.

The Federal Trade Commission advises that physical precious metals storage arrangements require independent, all-risk insurance policies — and that buyers evaluate independent third-party vaults to avoid custody conflicts. A bank safe deposit box satisfies neither condition.

The core problem is this: physical gold exists precisely because it operates outside the paper financial system. Placing it inside a bank vault re-entangles it with the exact institutional vulnerabilities it was meant to bypass. Private, segregated vaulted storage — held outside the banking system entirely — is the arrangement that actually addresses custody, insurance, access, and long-term liquidity. A safe deposit box cannot.

- What a Bank Safe Deposit Box Actually Is — And What It Isn't

- The FDIC Insurance Gap That Most Safe Deposit Box Customers Don't Know About

- Why Banks Carry No Legal Liability for Your Gold

- How Banks and Governments Can Cut Off Your Access

- How Private Vaulted Storage Eliminates These Risks

-

Frequently Asked Questions About Safe Deposit Box Gold Risks

- Are the contents of a bank safe deposit box insured by the FDIC?

- Can the government or a bank freeze access to my safe deposit box gold?

- What happens to my gold if the retail bank fails or declares bankruptcy?

- How does storing gold in a bank safe deposit box compare to private vaulted storage?

- Who is legally responsible if my physical gold is stolen from a bank safe deposit box?

- Is a safe deposit box ever a reasonable option for storing physical gold?

- The Bottom Line on Bank Safe Deposit Boxes and Physical Gold

What a Bank Safe Deposit Box Actually Is — And What It Isn't

Here's what most gold owners get wrong before they ever open a safe deposit box: they assume the bank's presence implies the bank's protection.

It doesn't.

A safe deposit box isn't a custody arrangement. It isn't a vault account. It isn't a place where the bank holds your property and bears responsibility for its safety.

It's a rental. The legal framework of safe deposit box rental is classified as a lease rather than a fiduciary bailment — the same legal sense as renting a storage unit or an office suite. The bank's obligation ends at providing the physical space. What you put inside, and what happens to it, is entirely your problem.

That distinction hits differently when your asset is physical gold. The entire point of holding physical metals is to operate outside the institutional financial system — to own something a bank can't freeze, can't digitize, and can't claim responsibility over.

Putting that asset inside a bank safe deposit box re-entangles it with the very institution it's meant to bypass. The vaulted storage model exists precisely because this re-entanglement has real consequences — legal, logistical, and financial. how physical wealth storage works

The Lease Agreement Nobody Reads Before Storing Gold

When you rent a safe deposit box, you sign a lease. Most people sign it the way they click through a terms-of-service agreement — quickly, without reading. That's where the gap between assumption and legal reality opens up.

The bank doesn't maintain any inventory or official catalog of what's inside your box. That's not an oversight. It's a feature of the legal structure.

The bank isn't your custodian. It's your landlord. It provides four walls and a lock — and has no legal responsibility for, and no formal knowledge of, what's stored inside.

And then there's the clause that tends to stop people cold when they finally read it: the bank carries zero liability for loss, theft, or damage to anything inside your box.

This isn't a loophole. It's written into the lease by design. Courts have upheld it consistently. The risks of safe deposit boxes don't trace back to any single bad actor or negligent branch manager. The structure itself — the lease, the liability exclusion, the landlord relationship — is the problem. (via This Library Of Congress)

Why the 'Secure Container' Mental Model Fails Gold Owners

Most people picture a safe deposit box as a small private vault — something that operates on its own, sealed off from whatever else the bank has going on.

For most stored items, that picture is close enough. For gold owners, it's the picture that gets them in trouble.

Physical gold is a sovereign asset because it exists outside the paper financial system. The moment it goes into a bank safe deposit box, that sovereignty ends.

Access is tied entirely to retail branch operating hours. Probate courts — state and federal — can freeze the box the day its primary holder dies. The Emergency Banking Act of 1933 shut down every bank in the country for four days, suspending physical access to every safe deposit box in America without exception. The container looks independent. The legal and physical reality is that it answers to the same institutional system as everything else in that building.

| Feature | Bank Safe Deposit Box | Private Vaulted Storage |

|---|---|---|

| Legal relationship | Landlord-tenant lease — the bank provides space only, with no custodial responsibility | Independent custody arrangement — your metals are held in your name by a dedicated custodian |

| Bank liability for contents | None — the bank bears no legal responsibility for loss, theft, or damage to box contents | Full — the facility carries independent, all-risk insurance coverage on stored assets |

| Inventory or record of contents | None maintained — the bank keeps no official catalog of what is inside your box | Fully documented — segregated holdings are recorded, verified, and assigned to the account holder |

| Access hours | Restricted to active retail branch operating hours — no access outside those windows | Accessible outside traditional banking hours through custodian protocols |

| Vulnerability to government or court action | Probate courts and federal authorities can freeze access immediately upon the primary holder's death or a legal order | Held outside the traditional banking system — not subject to standard bank-freeze mechanisms |

| Relationship to the paper financial system | Fully embedded — the box sits inside a bank, subject to all of its institutional and legal constraints | Separated — private vaulted storage operates outside the banking system your metals are intended to bypass |

| FDIC protection | Not applicable — FDIC insurance covers deposit accounts only, not physical contents stored in a box | Not applicable — independent all-risk insurance policies provide coverage instead |

The FDIC Insurance Gap That Most Safe Deposit Box Customers Don't Know About

Most people who rent a safe deposit box assume the bank's presence implies protection.

It doesn't.

FDIC deposit insurance covers checking accounts, savings accounts, money market accounts, and certificates of deposit. That's it. Physical assets stored in a safe deposit box aren't covered. Not partially. Not with exceptions. The coverage is exactly 0%.

That's not a loophole. Federal deposit insurance was built to protect dollar-denominated accounts — not sovereign physical assets.

And here's the irony: many gold owners choose physical metals specifically to operate outside the paper financial system. A safe deposit box places that gold right back inside it — and strips away the federal protection customers assume is automatic.

What FDIC Insurance Actually Covers — And the Hard Stop

The FDIC's deposit insurance FAQ is unambiguous: deposit insurance covers only traditional deposit accounts. The program was built after the banking crises of the early 20th century to keep depositors whole when institutions collapsed — to guarantee that money in bank accounts wouldn't vanish overnight. Physical valuables in a box were never part of that mandate. They weren't an oversight. They simply weren't the problem being solved.

Here's the hard stop.

If your safe deposit box contents are lost, stolen, or destroyed — flood, fire, theft, bank failure — there's no federal safety net. The FDIC won't compensate you. The bank's liability, per the lease structure, is essentially zero. The entire responsibility for insuring those contents sits with you.

The Federal Trade Commission puts it plainly: physical precious metals storage arrangements require independent, all-risk insurance policies. That's not a suggestion. It's the practical floor when the institution housing your assets carries no liability for them. Perceived security that doesn't survive scrutiny is a pattern worth examining — starting with home storage misconceptions

Why Most Gold Owners Assume Coverage That Doesn't Exist

The assumption is understandable. Banks are federally regulated. The FDIC logo sits at the teller window. The safe deposit area is inside the same building — often steps from the vault. That environment signals security, and customers extend that impression to everything inside.

But the FDIC's protection stops at the account boundary. Physical gold sitting on the other side of that line is completely unprotected — and the bank's physical design gives no indication of that fact.

This is the detail that consistently surprises customers — not because it's hidden in fine print, but because the bank's physical environment creates an impression the legal reality doesn't support. The building feels like protection. The lease says otherwise.

The FTC is direct on this: buyers must evaluate independent third-party vaults to avoid custody conflicts. The starting point for honest precious metals education on storage is always the same — understand exactly what protection exists before assuming it does. A bank safe deposit box doesn't pass that evaluation.

| Account or Asset Type | FDIC Insured? | Coverage Limit | What This Means for Gold Owners |

|---|---|---|---|

| Safe Deposit Box Contents (Physical Gold) | No | 0% — no federal coverage | Physical gold stored in a safe deposit box carries exactly zero federal insurance protection — loss, theft, or destruction is entirely the owner's responsibility |

| Private Vaulted Storage (Independent Third-Party) | No — but requires independent all-risk policy | Determined by the owner's insurance arrangement | The FTC requires independent, all-risk insurance policies for physical precious metals storage — private vaults are structured to support this; bank safe deposit boxes are not |

Why Banks Carry No Legal Liability for Your Gold

Most gold owners never ask the one question that matters most: if something goes wrong, who pays?

The answer is almost certainly not the bank.

The legal framework of safe deposit box rental is classified as a lease rather than a fiduciary bailment. That one distinction is everything.

The bank isn't holding your gold in trust. It's renting you a compartment. What happens inside that compartment — theft, damage, total loss — sits entirely outside the bank's legal accountability. Not because they're hiding something. Because the contract says so.

That lease structure determines who bears the loss. And the answer isn't the bank.

The FDIC is unambiguous: the federal deposit insurance customers associate with banking institutions covers deposit accounts — not physical assets in a box. Zero percent of what's in that box is federally insured. The liability question flows directly from the legal definition — and the legal definition says the bank owes you nothing beyond four walls and a lock. FDIC regulations governing deposit accounts make this explicit: safe deposit box contents fall entirely outside the federal insurance framework that protects bank deposits.

The Landlord-Tenant Legal Framework and What It Costs You

When you sign a safe deposit box agreement, you're entering a landlord-tenant relationship. The bank is the landlord. You are the tenant.

Its obligation ends at the door. Provide the space, provide the lock. That's what the contract says — in language most people skip past on the way to signing.

Here's what that means in practice: the bank doesn't maintain any inventory or official catalog of the items kept inside your box. It has no record of what you've stored. No way to verify a loss claim.

And because it never assumed custody of the contents in the first place, it bears no legal responsibility for them. The Federal Trade Commission is direct on this point — physical precious metals storage arrangements require independent, all-risk insurance policies, because the institution providing the space isn't providing the protection.

So here's where you land: if the contents of your box are lost, stolen, damaged, or destroyed, you're filing a claim against an institution that carries no legal liability and holds no record of what you owned. That's not a worst-case scenario. That's the default structure.

Private vaulted arrangements exist to close that gap — custody assigned, records maintained, insurance carried independently. That's the structural difference you're weighing when you look at segregated vs. non-segregated storage.

Who Is Not Watching Your Gold — And Why That Matters

The bank doesn't know what's in your box. And that's not a rhetorical point.

No catalog. No institutional record. No documentation of what you stored, when you stored it, or what condition it was in when you put it there. The bank never looked. The contract never required it to.

No record means no baseline. If your gold disappears, there's nothing in the bank's files to prove it was ever there. No custodial ledger. No independent witness. You're not filing a claim — you're making an assertion to an institution that never acknowledged your property existed.

The FTC puts the consequence plainly: buyers must evaluate independent third-party vaults to avoid exactly this kind of custody conflict. A landlord who never catalogued your belongings is not a custodian. And a bank that never recorded your gold is not protecting it — regardless of how solid the vault door looks.

This is also why home storage for Gold IRAs creates its own distinct exposure — moving the metals out of the bank doesn't solve the custody problem. It just changes its shape.

| Legal Relationship Type | Does the Institution Maintain an Inventory? | Liability If Contents Are Lost or Stolen | Applicable Framework |

|---|---|---|---|

| Bank Safe Deposit Box | No — the bank maintains no inventory or catalog of box contents | None — the lease structure assigns zero liability to the institution | Landlord-tenant lease; no fiduciary or custodial obligation |

| Private Vaulted Storage | Yes — verified records of holdings are maintained by the custodian | Defined by contract; the custodian assumes legal accountability for stored assets | Custodial bailment; institution holds assets on the owner's behalf |

| Home Storage | Owner-managed — no third-party record exists | Owner bears all risk; no institutional party has legal accountability | Personal property ownership; no custodial or lease relationship |

| Bank Deposit Account (Checking / Savings) | Yes — the institution maintains a full transaction and balance record | Federal deposit insurance (FDIC) covers losses up to established limits | Debtor-creditor relationship; regulatory protections apply to dollar-denominated accounts only |

How Banks and Governments Can Cut Off Your Access

Physical gold that you can't reach isn't protection. It's storage. And there's a meaningful difference between those two things.

Physical gold is supposed to exist outside the institutional financial system — sovereign, accessible, yours. But a safe deposit box hands that control back to the bank's schedule, the state's legal apparatus, and the federal government's emergency powers. That's not a theoretical concern. It's the documented structure of the arrangement. You're not holding the asset. You're holding a lease on a box inside a building that someone else controls.

And these aren't hypotheticals. The mechanisms that can cut you off are still active. They've already been used.

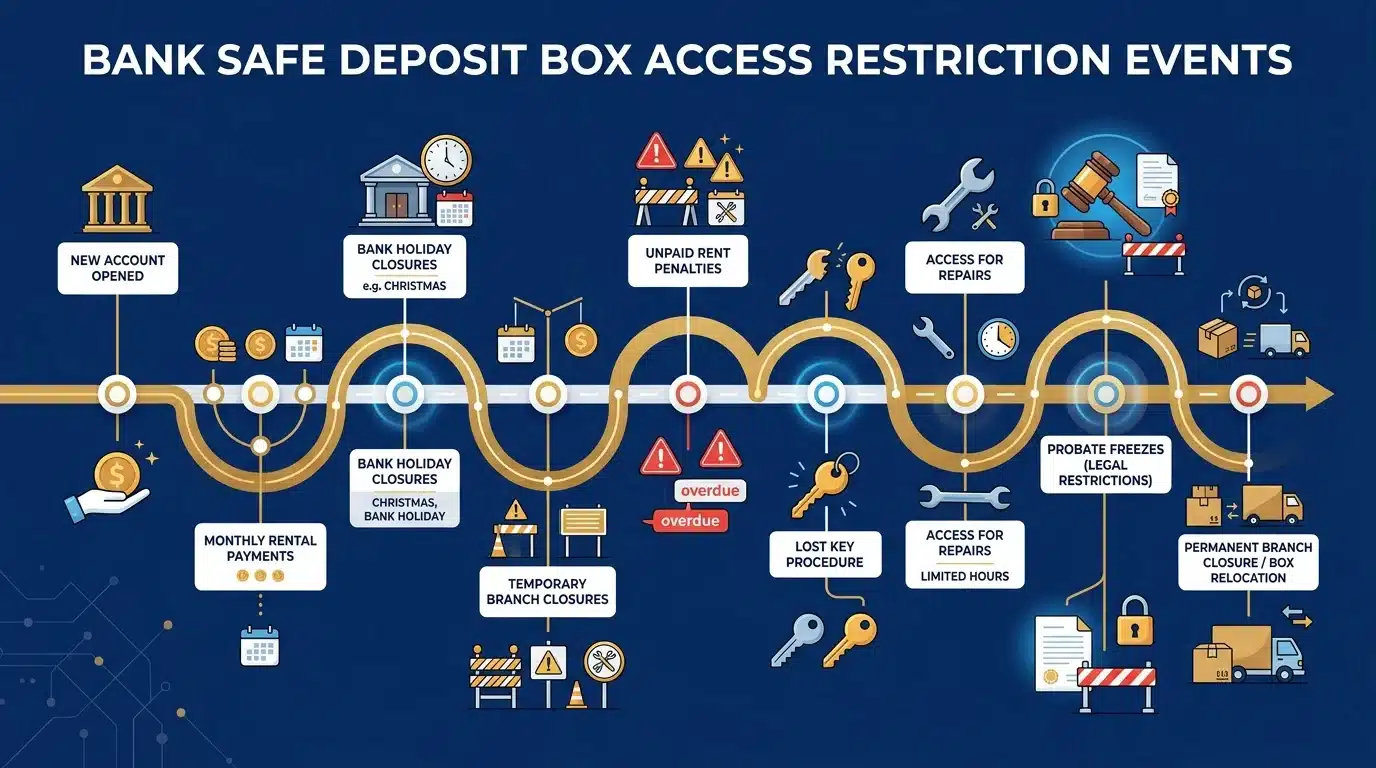

Bank Hours, Branch Closures, and Operational Lockouts

The most immediate access limitation isn't dramatic. It's mundane. Safe deposit box access is 100% dependent on active retail branch operating hours. If the branch is closed — for a holiday, a storm, a system outage, a banking disruption — there's no access to what's inside. No override. No exception.

That dependency is easy to miss when everything is running normally. Branches are open on weekdays. Access feels routine. But the moment conditions shift — the moment you actually need your physical asset right now — operating hours become a hard wall. Your gold is still there. You just can't reach it. That's not protection. That's a storage unit with a business-hours sign on the door.

Branch closures make it worse. When a retail location shuts down — temporarily or permanently — customers face transfer processes, appointment scheduling, and layers of institutional logistics just to retrieve what's theirs. For owners who chose physical metals specifically to maintain direct, self-directed access, that process contradicts the entire point. Private custody models are built to eliminate this kind of dependency. It's the core distinction we examine in segregated vs. non-segregated storage. offshore vs. domestic vault structures

Government Actions, Bank Holidays, and Probate Freezes

Routine operating hours are a limitation. Government action is a severance. The Emergency Banking Act of 1933 enforced a 4-day nationwide bank closure — and during that holiday, 100% of physical access to all retail and commercial safe deposit boxes was suspended. Every box. Every customer. No exceptions.

That's not ancient history deployed as a scare tactic. It's a documented example of what federal emergency authority looks like when applied to the banking system. And it exposes the central flaw in the safe-deposit-box logic: putting physical gold inside a bank vault doesn't place it outside institutional reach. It places it squarely within it. The Emergency Banking Act of 1933 didn't discriminate between account holders and box renters. The doors closed for everyone.

Probate law adds a separate layer — one that doesn't require a national emergency to trigger. When the primary box holder dies, state and federal probate courts can freeze access immediately. The gold is physically untouched. But a surviving spouse, a named heir, or a designated beneficiary can find themselves locked out for months while the estate grinds through the legal process. For customers who hold physical metals specifically for legacy and family protection, that's not a minor procedural inconvenience. It's a direct failure of the premise.

This Is Not the Right Fit for Every Gold Owner

So let's be direct about fit. Brighton Gold works with customers who want to hold physical metals for the long haul — for stability, privacy, and legacy. If that's where you are, every risk we've outlined here is exactly the kind of consideration that shapes the conversation we'll have.

But if your priority is short-term liquidity, active trading, or treating physical gold as a position you expect to move in and out of — the storage conversation is less relevant, and Brighton Gold isn't your best option. We don't time the market. We don't forecast prices. We don't optimize for in-and-out transactions. That's not what we're built for, and we'd rather say that now than waste your time later.

The customer this content is written for already understands something most people don't: true asset protection means separating physical gold from institutional vulnerabilities — not finding a more convenient institutional container for it. A bank safe deposit box, as both the legal structure and the access history confirm, is that container. It's not a vault outside the system. It's the system with a smaller door.

| Access Risk Scenario | Trigger | Duration of Lockout | Your Recourse |

|---|---|---|---|

| Branch closed during emergency or disruption | Weather event, system outage, banking disruption, or temporary branch closure | Hours to days — until the branch reopens under normal operations | None. You wait. There is no emergency access mechanism for safe deposit box holders. |

| Federal bank holiday declared by government | National financial emergency or executive action suspending banking operations | Determined entirely by federal authority — not by the box holder | None during the closure period. Access resumes only when the government lifts the order. |

| Primary box holder dies | Death triggers automatic probate or estate administration proceedings | Weeks to months — dependent on court timelines, estate complexity, and state law | Heirs and beneficiaries must navigate the legal estate process before physical access is restored. |

| Branch permanently closes or relocates | Bank consolidation, regulatory action, or institutional insolvency | Indefinite — until the customer completes the institution's transfer and retrieval process | Customer must schedule retrieval through institutional channels on the bank's timeline, not their own. |

How Private Vaulted Storage Eliminates These Risks

Every failure mode we've covered has a direct answer. But the answer isn't a better bank. It's a completely different custody model.

Private vaulted storage was built to solve problems a bank safe deposit box was never designed to address. Where the bank offers a lease, a professional vault offers custody. Where the bank maintains no record of your holdings, a private vault maintains verified documentation. Where the bank's insurance stops at the account boundary, a professional vault carries independent, all-risk coverage.

The Federal Trade Commission doesn't hedge on this: physical precious metals require independent, all-risk insurance and third-party vault evaluation. Professional vaulted storage is built to clear that bar. A bank safe deposit box can't — not by accident, but by design.

Physical gold exists to operate outside the institutional financial system. Private vaulted storage keeps it there. A bank safe deposit box pulls it back in — and the system it re-entangles you with is the exact one physical metals are supposed to bypass.

Segregated Custody, All-Risk Insurance, and Independent Verification

The first distinction is custody. A professional vault doesn't rent you a compartment and move on. It assumes documented, verified responsibility for what's stored. Your holdings are catalogued, identified, and recorded — which means a loss is resolvable. A bank box claim isn't, because the bank never catalogued anything in the first place.

The second distinction is insurance. The Federal Trade Commission is explicit: physical precious metals storage arrangements require independent, all-risk insurance policies, and buyers must evaluate independent third-party vaults to avoid custody conflicts. Professional vaults carry that coverage. And it's not incidental to the service — it's the structural commitment that closes the gap the bank lease creates and leaves open indefinitely.

The third distinction is access. A private vault's operating model isn't tied to retail branch hours, state probate timelines, or federal emergency banking authority. Your access doesn't answer to an institution's schedule or the government's discretion. That independence is the whole point of holding physical metals. And it's precisely what a bank safe deposit box — by legal and physical design — can never deliver.

Industry Standards That Banks Cannot Match

Better service is the wrong frame. Professional vaults operate against global benchmarks that preserve the liquidity, verifiability, and integrity of physical gold at a scale banks never compete at.

The London Bullion Market Association sets those benchmarks for the international precious metals market. LBMA-compliant gold bars must hold a minimum purity of 995.0 parts per thousand. Each good delivery bar must fall within a strict weight range of 350 to 430 fine troy ounces. Those specifications exist so any qualified buyer, anywhere in the world, can verify and transact on a bar without independent testing. That's what institutional-grade liquidity actually looks like — and it has nothing to do with a bank lease.

A bank safe deposit box offers none of that. No documentation. No purity certification. No chain of custody that supports a future transaction or an insurance claim. The LBMA standard exists precisely because the market demands verifiable, transferable proof — and a rental compartment at a retail branch produces none of it. Customers who see that distinction — between storage as a container and storage as a verified custody arrangement — make a very different decision about where their gold belongs. Brighton Gold's approach to vaulted storage is built around exactly that distinction: segregated, documented, insured, and independent of the banking system's structural vulnerabilities.

| Risk Category | Bank Safe Deposit Box | Private Vaulted Storage | Why It Matters |

|---|---|---|---|

| Insurance Coverage | No federal deposit insurance; bank lease provides no coverage for box contents; losses are not recoverable through the banking system | Independent, all-risk insurance policy carried by the vault; every holding is covered against loss, theft, and damage | Without documented coverage, a loss event leaves the owner with no legal recourse and no financial remedy |

| Custody & Legal Responsibility | Landlord-tenant lease relationship; bank maintains no record of contents and assumes no fiduciary liability for what is stored inside | Documented, verified custodial responsibility; holdings are catalogued, identified, and formally recorded by the vault operator | Custody determines whether a loss is resolvable — a lease relationship offers no foundation for a valid claim |

| Physical Access | Access restricted to retail branch operating hours; subject to suspension during bank holidays, government-declared emergencies, or institutional closures | Access governed by the vault's independent operating model — not tied to retail branch schedules, probate timelines, or federal banking authority | Owners who hold physical gold for stability and self-direction need access that isn't contingent on an institution's schedule or a government's discretion |

| Verification & Chain of Custody | No documentation, no purity certification, and no chain of custody maintained for box contents; the bank holds no record of what is inside | Holdings maintained against international industry standards; purity, weight, and provenance documented to support future transactions and insurance claims | Verified chain of custody is what makes physical gold liquid and transactable — without it, the asset's value is difficult to realize at the point of sale |

| Independence from the Banking System | Physically located inside a bank branch; legally re-entangled with the institutional system that physical gold ownership is meant to bypass | Structurally separate from the retail banking system; sovereign asset held outside the institutional vulnerabilities it was acquired to avoid | The purpose of holding physical gold is ownership outside the paper financial system — storage that re-introduces institutional dependency defeats that purpose entirely |

Frequently Asked Questions About Safe Deposit Box Gold Risks

Good. The comparison should raise questions.

The legal and practical gaps between a bank safe deposit box and private vaulted storage are real — and they deserve straight answers.

Here are the questions we hear most — and the ones that actually matter when you're deciding where your physical gold belongs.

Are the contents of a bank safe deposit box insured by the FDIC?

No. The FDIC insures deposit accounts — checking, savings, money market, CDs. That protection stops at the account boundary.

Physical assets stored inside a safe deposit box are federally uninsured at 0%. Gold, silver, coins, bars — none of it has any federal backstop. If the contents are lost, stolen, or damaged, there's no FDIC claim to file.

Whatever recovery is possible runs through the bank's lease agreement — which is not a custody arrangement and routinely contains strict liability caps that favor the institution, not you.

Can the government or a bank freeze access to my safe deposit box gold?

Yes — and through more than one mechanism.

The most immediate is operating hours. Safe deposit box access is 100% dependent on active retail branch hours. Branch closed? You can't reach what's inside. No override, no exception.

The harder category is government authority. The Emergency Banking Act of 1933 enforced a 4-day nationwide bank closure, during which 100% of physical access to all retail and commercial safe deposit boxes was suspended. Every box. Every customer.

And at the individual level, state and federal probate courts can freeze access immediately upon the primary holder's death — sometimes locking out a surviving spouse or named heir for months while the estate works through the legal process.

What happens to my gold if the retail bank fails or declares bankruptcy?

Not much changes for the better — and potentially a great deal changes for the worse.

The legal relationship is a lease, not a bailment. The bank maintains no inventory or official catalog of what's inside your box. There's no institutional record of your holdings to anchor a claim — which means if the bank fails, there's nothing on file that proves what you stored.

In principle, safe deposit box contents aren't treated as bank liabilities during a failure — they remain your property. But reaching them during regulatory receivership or bankruptcy proceedings introduces delays, administrative layers, and no guarantee of timing.

Brighton Gold doesn't provide legal advice — consult a licensed attorney for your specific situation. But the structural picture is clear: the bank's failure becomes your logistical problem, not its obligation.

How does storing gold in a bank safe deposit box compare to private vaulted storage?

The legal relationship is the whole story.

A bank rents you a compartment and disclaims liability for everything inside. A private vault assumes custody — documented, verified, and backed by independent all-risk insurance. Those aren't comparable arrangements. One is a lease. The other is accountability.

Access is the second break point. A private vault's operating model isn't tied to retail branch hours, probate timelines, or federal emergency authority. Your access doesn't depend on whether a branch is open or whether a government order has suspended banking operations nationwide.

For anyone holding physical metals for stability and long-term legacy, those distinctions aren't fine print. They're the entire point. Brighton Gold's view on the risks of safe deposit boxes is built on exactly this contrast — which is why we direct customers toward segregated, private custody rather than banking infrastructure.

Who is legally responsible if my physical gold is stolen from a bank safe deposit box?

In most cases, no one with meaningful legal accountability.

The safe deposit box lease is a landlord-tenant arrangement — not a fiduciary bailment. The bank maintains no inventory of your holdings and assumes no custodial responsibility. It never catalogued what you stored. It can't verify a loss claim it never had a basis to make.

If theft occurs, recovery depends on the specific language in your rental agreement — which routinely includes strict liability caps — and any independent insurance policy you've arranged on your own. The FDIC won't cover it. The bank isn't legally required to make you whole.

What you're left with is a civil claim against an institution that specifically disclaimed custody of your property in the contract you signed.

Is a safe deposit box ever a reasonable option for storing physical gold?

For small quantities of low-value items — where the owner fully understands there's no FDIC coverage, no bank custody, and access tied entirely to branch hours — a safe deposit box is a practical short-term tool. Go in with eyes open and it works for what it is.

But for physical gold held as a long-term store of value, especially for legacy or retirement purposes, the structure breaks down. The bank assumes no liability. Access can be cut by routine operations, probate proceedings, or federal emergency authority — the Emergency Banking Act of 1933 proved that. And there's no documentation infrastructure to support a future insurance claim or a clean transaction.

A safe deposit box isn't always the wrong answer. But for physical gold with real wealth behind it, understanding segregated vs. non-segregated storage matters before any storage decision is made — because for serious holdings, it rarely ends up being the right one.

The Bottom Line on Bank Safe Deposit Boxes and Physical Gold

Here's what every fact in this article points to: a safe deposit box looks like security — it's actually a reentry point into the system.

The FDIC covers exactly none of what's inside. The bank maintains no catalog, holds no custody, and bears no legal liability for what's lost. Access answers to branch hours, probate courts, and federal emergency authority.

That's not asset protection. That's institutional dependency with a different lock on the door.

The alternative isn't complicated. Private, segregated vaulted storage keeps physical gold where it was meant to be — outside the banking system's structural vulnerabilities, with custody documented and independent all-risk insurance in place.

Precious metals may appreciate, depreciate, or remain unchanged. What doesn't change is where they're held and who actually bears responsibility for them.

That distinction isn't a product feature. It's the entire decision.

Brighton Gold's approach to storage starts from one conviction: physical gold held inside a bank safe deposit box isn't outside the system. It's inside it, subject to every institutional constraint covered here.

If you've been treating a safe deposit box as your custody solution, ask the harder question. Does that arrangement actually deliver what you intended when you bought the metals?

Not whether your gold is physically nearby. Whether anyone with legal accountability knows it exists.

A safe deposit box looks like security — it's actually a reentry point into the system. Private, segregated custody is how you step outside it for good.

That realization — that a safe deposit box puts your gold back inside the system it's meant to bypass — is where most customers start asking the right questions.

Brighton Gold offers a complimentary consultation to walk you through what segregated, private custody actually looks like. And if a Precious Metals IRA is part of your picture, we'll show you exactly how the No Fee IRA works and whether you qualify.