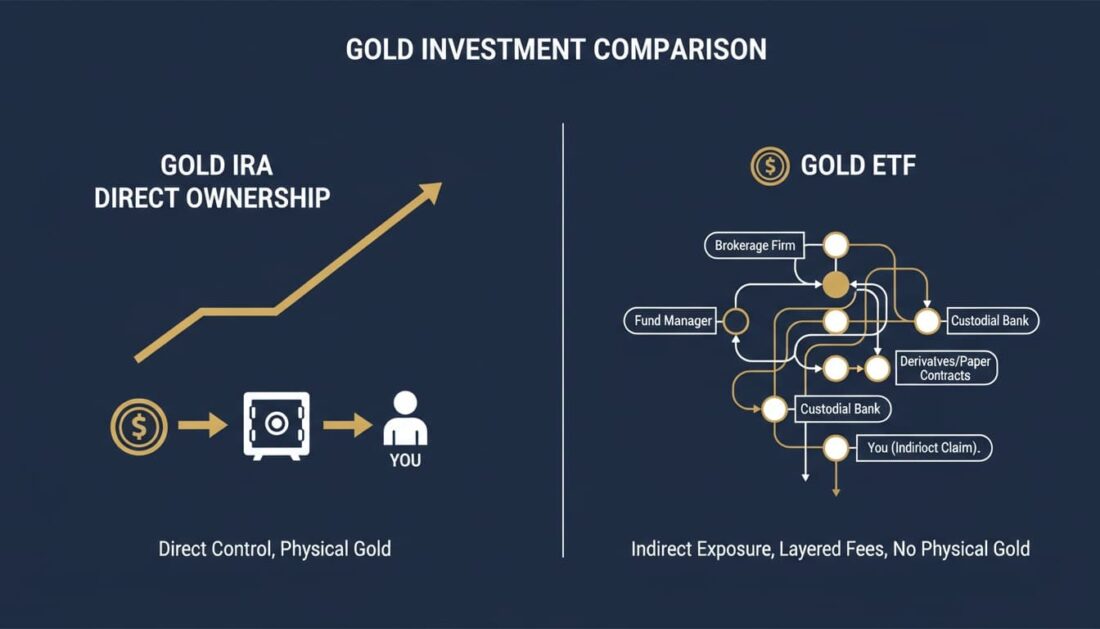

Here’s a surprise most people don’t realize: when you buy shares in a Gold ETF, you don’t actually own any gold.

You own shares in a trust. The trust owns the gold. And a chain of banks, fund managers, and custodians stands between you and the metal itself.

A Gold IRA works differently. You own physical coins or bars—stored in a vault with your name on it. No trust. No fund manager. No middlemen.

Both track the price of gold. But only one puts real, tangible metal under your control.

So which one makes more sense for retirement in 2026?

That’s what we’re going to walk through—step by step. We’ll look at ownership, taxes, fees, and what happens during a crisis when you actually need your gold to be there.

By the end, you’ll have the clarity to decide which approach fits your goals.

What’s the Real Difference Between These Two Options?

Before we get into costs or taxes, let’s start with the basics. What are you actually buying?

The answer might surprise you.

How a Gold IRA Works

A Gold IRA is a self-directed retirement account that holds physical precious metals.

You own actual gold—typically U.S.-minted coins like the Gold American Eagle—stored in an IRS-approved depository.

Here’s the structure:

- You own the account

- A custodian handles the paperwork and IRS reporting

- A depository stores your physical gold in a secure vault

- A dealer (like Brighton) helps you choose and purchase IRS-approved metals

When you buy gold through this account, it’s shipped to the depository and held in your name. You maintain ownership. You get the same tax benefits as a Traditional or Roth IRA.

And when you’re ready to take a distribution? You can receive actual coins and bars—shipped directly to you.

How a Gold ETF Works

A Gold ETF is a financial product that tracks the price of gold.

When you buy shares of GLD, IAU, or another gold ETF, you’re purchasing units in a trust. The trust holds gold bullion in vaults on behalf of all shareholders.

Here’s how it’s structured:

- You own shares in a trust

- A fund manager operates the ETF

- A trustee oversees the fund’s assets

- A custodian (often a major bank) stores the physical gold

- Sub-custodians may hold gold across multiple locations

You don’t own specific bars or coins. You own a proportional claim on whatever the trust holds.

As the founder of GLD himself put it: “When you buy GLD shares, you’re buying ownership in a trust… The individual does not own gold that backs the trust.”

Why This Matters

Here’s the question worth asking: Why are you considering gold in the first place?

If it’s for price exposure—just tracking gold’s ups and downs—an ETF does that efficiently.

But if it’s for peace of mind? For knowing you own something real that doesn’t depend on banks, fund managers, or electronic markets working correctly?

That’s where physical ownership starts to look different.

How Do the Costs Actually Stack Up?

One of the most common things we hear: “Aren’t Gold IRAs more expensive than ETFs?”

It’s a fair question. And the answer depends on how much you’re holding.

What Gold ETFs Charge

Gold ETFs charge an annual expense ratio—a percentage of your holdings deducted automatically each year.

Here’s what the major funds charge:

- SPDR Gold Shares (GLD): 0.40% annually

- iShares Gold Trust (IAU): 0.25% annually

- SPDR Gold MiniShares (GLDM): 0.10% annually

- abrdn Physical Gold Shares (SGOL): 0.17% annually

On a $100,000 position, a 0.40% expense ratio costs $400 per year. On $250,000, it’s $1,000. The percentage stays the same—but the dollar amount keeps climbing.

What Gold IRAs Charge

Gold IRAs involve a few different fees:

- Setup fees: $50–$150 (one-time)

- Annual custodian fees: $75–$300 per year

- Storage fees: $100–$300 per year

- Transaction fees: $25–$50 per trade (some custodians waive this)

Most customers can expect $200–$300 per year for custodian and storage combined.

Here’s the key difference: these are typically flat fees—not percentages.

Where the Math Flips

Let’s look at how this plays out at different account sizes:

| Account Size | GLD (0.40%) Annual Cost | Typical Gold IRA Annual Cost |

|---|---|---|

| $25,000 | $100 | $200–$250 |

| $50,000 | $200 | $200–$250 |

| $100,000 | $400 | $200–$250 |

| $250,000 | $1,000 | $200–$250 |

| $500,000 | $2,000 | $200–$250 |

See the pattern?

At smaller account sizes, ETFs have a cost advantage. But once you’re above $50,000–$75,000, the flat-fee Gold IRA becomes more cost-efficient.

For retirement accounts—where balances often exceed $100,000—the “ETFs are cheaper” assumption doesn’t hold up.

What About No-Fee Options?

Here’s something else worth knowing: some providers offer structures that eliminate annual custodial fees entirely.

Brighton’s No Fee Precious Metals IRA, for example, covers custodial fees for the lifetime of the account on qualified purchases.

That changes the calculation completely. If you’re comparing a no-fee Gold IRA to a 0.40% expense ratio ETF, the IRA costs less at every account size.

What About Taxes?

Here’s something most people don’t realize until tax time: gold ETFs are taxed differently than stocks.

And not in a good way.

The 28% Surprise

The IRS classifies physically-backed gold ETFs as “collectibles.”

Under IRC Section 408(m), that means long-term gains are taxed at a maximum rate of 28%—compared to 15–20% for most stocks and bonds.

Let’s say you bought $50,000 of GLD shares. Gold goes up. You sell for $75,000—a $25,000 gain.

At the 28% collectibles rate? You owe $7,000 in federal taxes.

At the standard 20% rate (if it applied)? You’d owe $5,000.

That’s a $2,000 difference on a single transaction—just because of how the IRS classifies gold ETFs.

Short-term gains are even worse—taxed as ordinary income, up to 37%.

How Gold IRAs Handle Taxes

Gold IRAs sidestep this problem entirely.

- Traditional Gold IRA: Contributions may be tax-deductible. Your gold grows tax-deferred. You pay ordinary income tax when you take withdrawals in retirement.

- Roth Gold IRA: Contributions are made with after-tax dollars. Your gold grows tax-free. Qualified withdrawals in retirement are completely tax-free.

Neither structure triggers the 28% collectibles rate during the accumulation phase.

For long-term retirement planning, this is a meaningful advantage.

Can You Hold an ETF Inside an IRA?

Yes—you can hold gold ETF shares inside a Traditional or Roth IRA at most brokerages.

This avoids the 28% collectibles tax problem because you’re not realizing gains in a taxable account.

But here’s the trade-off: you still don’t own physical gold. You still own shares in a trust.

If you want both tax advantages and tangible ownership? A self-directed Gold IRA gives you both.

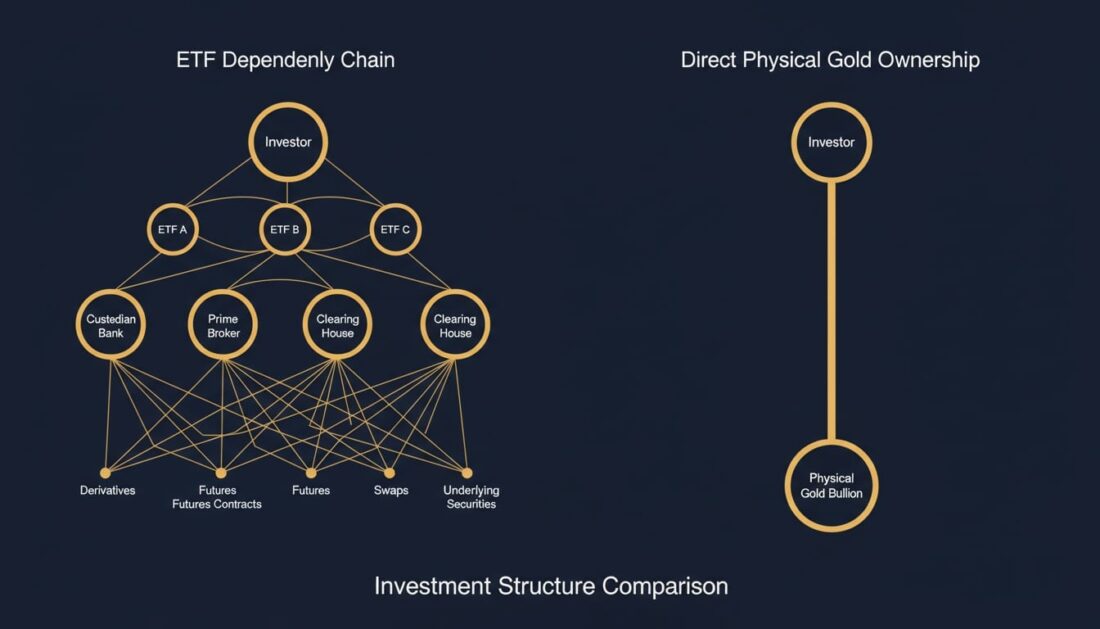

What Is Counterparty Risk—and Why Should You Care?

Here’s a term worth understanding: counterparty risk.

It means your value depends on someone else holding up their end of the deal.

With physical gold in your name, counterparty risk is minimal. With paper claims on gold, the chain of dependencies gets longer.

The ETF Dependency Chain

When you buy shares in a gold ETF like GLD, here’s what has to work correctly for you to access your value:

- The fund manager has to operate the ETF properly

- The trustee has to oversee assets accurately

- The custodian (often a major bank) has to store and track the gold

- Sub-custodians may hold gold across various locations

- The stock exchange has to function normally

- Your brokerage has to process your trades

- Electronic settlement systems have to work

That’s a lot of moving pieces.

And here’s the thing—if any link in that chain experiences stress, your access to value could be delayed or complicated.

This isn’t just theoretical. During the 2016 Brexit vote, several UK investment funds temporarily suspended redemptions due to “extraordinary market conditions.” Regular depositors couldn’t access their own money—precisely when they needed it most.

What the Fine Print Says

Gold ETF prospectuses contain clauses that limit the fund’s liability in various scenarios.

Custodian failures. Sub-custodian issues. Regulatory actions. “Force majeure” events.

The fine print acknowledges that things can go wrong—and limits your recourse if they do.

Physical Gold: No Dependencies

Physical gold in a Gold IRA sits in a vault with your name on it.

Your ownership doesn’t depend on:

- Fund managers making correct decisions

- Trustees maintaining proper oversight

- Custodian banks remaining solvent

- Electronic markets functioning normally

- Settlement systems processing trades

As Ray Dalio told CNBC: “Gold is the only asset that somebody can hold and you don’t have to depend on somebody else to pay you money for.”

That’s a powerful statement from someone who’s spent decades studying how financial systems break down.

Can You Actually Take Delivery of Physical Gold?

Here’s a question we get often: “Can I actually get my hands on the gold if I want to?”

The answer depends entirely on which path you choose.

Gold ETF: Delivery Isn’t Really an Option

For most people, taking physical delivery from a gold ETF isn’t practical.

Here’s why:

- Redemption is limited to “authorized participants”—large financial institutions trading in blocks worth tens of millions

- Minimum thresholds often require 100,000 shares or more

- The process is expensive, slow, and designed for institutional use

- Most retail purchasers must sell shares for cash—you can’t request gold bars

One industry source puts it plainly: “Retail holders cannot request delivery of physical gold.”

If the ability to take physical possession matters to you—whether for estate planning, emergency access, or simply knowing you can hold what you own—ETFs don’t provide that path.

Gold IRA: A Clear Path to Your Gold

With a Gold IRA, the gold in your account is specific, identifiable metal.

When you take a distribution after reaching retirement age, you have two options:

- Cash distribution: Sell the metals and receive the dollar value

- In-kind distribution: Take physical delivery of your actual gold coins or bars

The in-kind option means you can literally receive your Gold American Eagles, Gold Buffalos, or bullion bars—shipped directly to your home.

You declare the fair market value as a distribution, pay applicable taxes, and the metal is yours to hold.

That’s real ownership. That’s control.

What Does Ray Dalio Say About Gold Right Now?

Ray Dalio founded Bridgewater Associates—one of the world’s largest hedge funds.

When he talks about gold, people listen. And lately, he’s been saying a lot.

The 15% Recommendation

At the October 2025 Greenwich Economic Forum, Dalio recommended allocating up to 15% of total holdings to gold.

That’s triple the traditional 5% guidance. And it aligns with what the World Gold Council has been tracking—record central bank accumulation and surging ETF inflows throughout 2025.

His reasoning?

- Rising government debt levels—the U.S. now carries over $37 trillion

- Historical parallels to the 1970s, when inflation and deficit spending drove gold higher

- Gold’s role as “the second-largest reserve currency” behind the dollar

- Central banks worldwide increasing their gold reserves

“When you’re doing your asset allocation, what is going to protect your real after-tax returns?” Dalio asked his audience. “Gold is a very excellent diversifier.”

Why Physical Ownership Fits His Logic

Here’s what stands out about Dalio’s comments: his emphasis on gold as a counterparty-free asset.

“Gold is the only asset that somebody can hold and you don’t have to depend on somebody else to pay you money for,” he told the forum.

That’s not an argument for ETF shares. That’s an argument for physical ownership.

Central banks understand this. They’re accumulating physical bars and coins—not ETF shares. For individual purchasers following similar logic, the case for tangible ownership becomes clear.

How Do These Options Compare for Long-Term Retirement?

Retirement planning operates on a different timeline than short-term trading.

The factors that matter most—security, tax efficiency, control, and legacy transfer—often point toward physical ownership in ways that aren’t obvious when you’re just comparing expense ratios.

Time Horizon Makes a Difference

- Short-term (under 5 years): ETFs offer easy entry and exit. Counterparty risk feels less pressing over shorter periods.

- Medium-term (5–15 years): The tax advantages of Gold IRAs start to compound. Flat fees look better compared to percentage-based expenses.

- Long-term (15+ years): Physical ownership eliminates decades of counterparty dependency. Estate planning options expand. The “hassle” of setting up a Gold IRA becomes negligible relative to how long you’ll hold it.

For retirement accounts—which might be held for 20, 30, or 40+ years—the arguments for physical ownership get stronger over time.

Estate Planning and Legacy

Physical gold in a Gold IRA can transfer to beneficiaries with clear ownership documentation.

The gold itself—actual coins and bars—can pass to heirs either as in-kind distributions or through inherited IRA structures.

ETF shares transfer as paper assets within brokerage accounts, subject to the same counterparty dependencies that existed during your lifetime.

For customers focused on legacy planning and leaving something tangible to children or grandchildren, physical gold provides what ETF shares can’t: a real, holdable inheritance.

Control and Independence

A Gold IRA operates outside the traditional brokerage system.

Your gold isn’t held by a fund. It isn’t traded on an exchange. It isn’t subject to fund manager decisions.

It sits in a vault, owned by you, waiting until you decide to distribute it.

This kind of independence aligns with the reasons many people turn to gold in the first place—a desire for assets that exist outside the conventional financial system.

The Complete Comparison: Gold IRA vs. Gold ETF

Here’s everything side by side:

| Factor | Gold IRA | Gold ETF |

|---|---|---|

| What You Own | Physical gold coins/bars in your name | Shares in a trust holding gold |

| Counterparty Risk | Minimal (depository storage only) | Multiple layers (fund, trustee, custodian, sub-custodian, exchange) |

| Physical Delivery | Yes—in-kind distribution available | No—retail purchasers cannot redeem for gold |

| Annual Costs (under $50K) | $200–$300 typical | $50–$200 (expense ratio) |

| Annual Costs (over $100K) | $200–$300 typical | $400+ and rising |

| Tax Treatment (Taxable Account) | N/A (IRA structure) | 28% max collectibles rate |

| Tax Treatment (Within IRA) | Tax-deferred or tax-free (Roth) | Tax-deferred or tax-free (Roth) |

| Setup Complexity | Moderate (custodian, depository required) | Low (standard brokerage) |

| Liquidity | Multi-day process | Instant during market hours |

| Crisis Access | Independent of financial system | Dependent on markets, brokerages, fund operations |

| Estate Planning | Physical metal transfers to heirs | Paper shares transfer through brokerage |

The right choice depends on what matters most to you.

If instant liquidity and minimal setup are your priorities, ETFs may fit better.

If counterparty elimination, physical ownership, and long-term tax efficiency matter more, a Gold IRA likely serves you better.

Who Should Consider a Gold IRA Over an ETF?

A Gold IRA isn’t the right fit for everyone.

But for certain situations, the advantages of physical ownership outweigh the extra setup.

When a Gold IRA Makes Sense

- You’re focused on retirement with a 10+ year horizon. The benefits of physical ownership compound over time. The setup effort becomes negligible over decades of holding.

- You’re concerned about financial system risks. If you want gold specifically because you don’t fully trust banks, funds, or electronic markets—owning ETF shares defeats the purpose.

- Your account balance is above $50,000. Flat-fee IRA structures become more cost-efficient than percentage-based ETF expenses at higher balances.

- You want tax efficiency. Avoiding the 28% collectibles rate (in taxable accounts) or accessing Roth IRA tax-free growth makes Gold IRAs attractive for long-term wealth building.

- You want the option of physical delivery. If knowing you can actually hold your gold matters, a Gold IRA provides that path.

- You’re thinking about legacy. Passing tangible gold to heirs is simpler—and more meaningful—than passing brokerage account shares.

When an ETF Might Make More Sense

- You’re making short-term tactical moves. If you’re trading gold for near-term price swings, ETF liquidity matters more than ownership structure.

- Your allocation is small (under $25,000). Percentage-based fees may be lower at smaller account sizes.

- You want everything in one brokerage account. If consolidation matters more than physical ownership, ETFs offer simplicity.

Frequently Asked Questions

Is a Gold IRA safer than a Gold ETF during a market crash?

During market disruptions, a Gold IRA offers advantages because you own physical metal stored in an approved depository—not shares in a trust.

Gold ETFs depend on fund managers, custodians, and electronic markets to function properly. If any of these systems experience stress during a crisis, your access could be delayed or complicated.

Physical gold in a Gold IRA exists independently of financial system functionality.

Can I take physical delivery of gold from an ETF?

For most people, no.

Physical redemption from gold ETFs like GLD is limited to “authorized participants”—large financial institutions trading in blocks worth tens of millions of dollars.

The minimum threshold often requires 100,000 shares or more. Retail purchasers can’t request gold bars—they sell shares for cash.

If you want gold you can actually hold, a Gold IRA or direct cash purchase provides a clearer path.

What are the tax differences between a Gold ETF and a Gold IRA?

Gold ETFs in taxable brokerage accounts are taxed as collectibles—up to 28% on long-term gains, compared to 15–20% for most stocks.

A Traditional Gold IRA defers taxes until withdrawal. A Roth Gold IRA offers tax-free growth and withdrawals in retirement.

For retirement-focused planning, the IRA structure often provides more favorable treatment.

Does Ray Dalio recommend physical gold or ETFs for 2026?

Dalio has recommended allocating up to 15% of holdings to gold, emphasizing its role as a hedge against monetary debasement.

Notably, he’s highlighted that gold is “the only asset that somebody can hold and you don’t have to depend on somebody else to pay you money for.”

That’s a direct reference to the counterparty-free nature of physical ownership—not an endorsement of paper claims.

Why are Gold IRA fees higher than Gold ETF expense ratios?

Gold IRAs require specialized custodians, IRS-approved storage, insurance, and compliance reporting. These services don’t apply to ETF shares in a standard brokerage account.

Annual Gold IRA fees typically run $200–$300 for custodian and storage combined. ETF expense ratios run 0.10%–0.40% annually.

But the comparison shifts at larger account sizes. And some providers—like Brighton—offer no-fee IRA structures on qualified purchases that eliminate ongoing costs entirely.

Can I hold a Gold ETF inside a standard IRA?

Yes—you can hold gold ETF shares inside a Traditional or Roth IRA at most brokerages.

This avoids the 28% collectibles tax rate that applies in taxable accounts.

But you still won’t own physical gold. You’ll own shares in a trust. For customers who want both tax advantages and tangible ownership, a self-directed Gold IRA provides both.

What happens to my Gold ETF if the fund manager or custodian fails?

Gold ETFs involve multiple counterparties: fund managers, trustees, custodians, and sub-custodians.

If any link in this chain experiences financial distress, your access could be affected. ETF prospectuses contain clauses that limit fund liability in various scenarios.

While complete loss is unlikely, delays or complications during periods of stress are possible. Physical gold in a Gold IRA eliminates these dependencies.

How do I convert a Gold ETF position to a physical Gold IRA?

You’d sell your ETF shares in your brokerage account, then use those funds to open and fund a self-directed Gold IRA.

If the ETF is held in an existing IRA, you can transfer the cash proceeds directly to a Gold IRA custodian without triggering taxes.

From there, you work with a dealer to purchase IRS-approved coins or bars, which are shipped to an approved depository and held in your name.

For a detailed walkthrough, see our guide on IRA transfers and rollovers.

The Bottom Line

The Gold IRA vs. Gold ETF decision comes down to one question: What are you really trying to accomplish?

If you want price exposure to gold with maximum liquidity and minimal setup, an ETF does that efficiently.

But if you want to own physical gold inside a tax-advantaged retirement account—with no counterparty dependencies, clear estate planning benefits, and the option to take delivery?

A Gold IRA provides what an ETF simply cannot.

For retirement-focused customers in 2026, the case for physical ownership has rarely been stronger. Gold has surged past $4,500. Central banks are accumulating at record pace. And J.P. Morgan forecasts gold could push toward $5,000 by late 2026.

The question isn’t whether gold deserves a place in your retirement picture.

It’s whether you want to own the real thing—or a paper claim on it.

What You Can Do:

If you’re thinking “this all makes sense, but I don’t have time to figure it out on my own,” you’re not alone. Most customers we work with felt the same way before they realized how straightforward the process can be with the right guidance.

That’s why we offer a complimentary consultation to walk you through your options—including our No Fee Precious Metals IRA, which covers custodial fees for the lifetime of the account on qualified purchases.

We’ll show you exactly:

- How the No Fee IRA works and whether you qualify

- The difference between U.S.-minted coins and foreign alternatives

- What to expect from the purchasing and delivery process

- How to roll over or transfer existing retirement funds

- What ongoing support looks like after your purchase

Learn About the No Fee IRA — no obligation, just clarity and control over your next steps.

We’re here to help—before, during, and after your decision.