No. You can’t store Gold IRA gold at home.

And here’s the thing—in 2026, the consequences for trying have never been clearer.

The IRS has always required that precious metals in an IRA stay in the physical possession of an approved trustee or depository. That’s not new. What’s changed is how aggressively this rule is now enforced—and how definitively the courts have ruled against “home storage” schemes.

In 2021, the U.S. Tax Court delivered a landmark decision in McNulty v. Commissioner. It eliminated any ambiguity. The ruling confirmed that storing IRA-owned gold at your home—even through an LLC structure—triggers an immediate taxable distribution.

The McNultys lost their entire tax-deferred status. They owed roughly $270,000 in taxes plus over $50,000 in penalties. All because they stored American Eagle coins in a home safe.

Here’s the short version: if you want to hold physical gold in a retirement account, it has to be stored at an IRS-approved depository—not your basement, not your closet, and not a safe deposit box you control.

The good news? Proper Gold IRA storage isn’t complicated. It’s handled by your custodian and depository, requires minimal effort on your part, and keeps your retirement savings fully protected.

Let’s walk through exactly why home storage doesn’t work, what the law actually says, and how to hold physical gold the right way.

Why the IRS Doesn’t Allow Home Storage for Gold IRAs

The rule against home storage isn’t arbitrary. It comes directly from how IRAs are designed—and from specific language in the Internal Revenue Code.

IRAs exist to help Americans save for retirement by offering tax advantages. In exchange for those benefits, the IRS sets strict rules about who controls the assets.

The Physical Possession Requirement

Section 408(m) of the Internal Revenue Code contains the key provision.

It says that gold, silver, platinum, or palladium bullion can only be held in an IRA if it’s “in the physical possession of a trustee.”

That’s not a suggestion. It’s a requirement.

The trustee has to be either a bank or a non-bank entity that’s demonstrated to the IRS that it’ll administer the account in compliance with all applicable regulations.

Your home safe doesn’t qualify. Neither does a safety deposit box you can access.

The IRS has been clear about this. According to their official guidance, gold and other bullion are considered “collectibles” under IRA statutes—and the law discourages holding collectibles in IRAs. The exception for certain precious metals only applies when they’re held by an approved trustee.

Why Personal Possession Equals Distribution

When you take personal possession of IRA assets, the IRS treats it as though you’ve withdrawn those assets from the account.

It doesn’t matter if you label the coins as IRA property.

It doesn’t matter if you keep meticulous records.

It doesn’t matter if you never sell a single piece.

The moment you exercise “unfettered control” over IRA assets—meaning you can use them however you want—the IRS considers it a distribution.

This applies to all IRA assets, not just precious metals. The difference is that stocks and bonds exist as electronic records. Gold and silver are tangible. That tangibility creates opportunities for people to think they can hold their retirement savings in their hands.

They can’t. Not without tax consequences.

The “Adequate Vault” Requirement

There’s another layer to this.

IRS regulations under Section 1.408-2(e) require that assets needing safekeeping be deposited in an “adequate vault.”

The regulation specifically addresses fiduciary requirements for non-bank trustees. If assets require safekeeping—and physical gold certainly does—they have to be stored in a vault that meets professional standards.

A home safe, no matter how robust, doesn’t meet this standard.

A safety deposit box to which you have access doesn’t either.

The vault has to be under the trustee’s control, not yours.

The McNulty Ruling: What Actually Happened

The 2021 McNulty v. Commissioner case removed any remaining doubt about home storage Gold IRAs. The Journal of Accountancy’s analysis of the ruling confirmed how definitively the court rejected home storage arrangements.

Here’s what the court found—and why it matters for anyone considering similar arrangements in 2026.

The Facts of the Case

In 2015, Andrew and Donna McNulty decided to set up self-directed IRAs.

They researched options online and discovered a company called Check Book IRA. The company advertised that customers could store American Eagle coins at home without tax consequences—as long as the coins were titled to an LLC owned by the IRA.

Donna McNulty followed the instructions.

She formed an LLC called Green Hill Holdings. Her self-directed IRA became the sole member of the LLC. She then used IRA funds to purchase American Eagle gold and silver coins, which were shipped to her personal residence and stored in a safe.

The coins were stored alongside non-IRA metals the McNultys had purchased separately.

Here’s where the numbers get painful.

Donna McNulty purchased roughly $411,000 worth of coins through this arrangement. When the IRS audited their returns, it determined that she’d received taxable distributions equal to the full cost of those coins in the years she took possession.

The Court’s Decision

The Tax Court ruled decisively against the McNultys.

Judge Robert Goeke found that Donna McNulty’s physical possession of the coins gave her “unfettered control” over the IRA assets—regardless of the LLC structure.

The formal interposition of the LLC didn’t change the fundamental reality: she could do whatever she wanted with those coins.

The court stated plainly: “Personal control over the IRA assets by the IRA owner is against the very nature of an IRA.”

The McNultys tried several arguments.

They claimed the coins were properly titled to the LLC. They argued that labeling the coins as IRA property prevented commingling. They suggested that Section 408(m)’s trustee requirement applied only to bullion, not coins.

The court rejected each argument.

On the labeling defense, the court noted skepticism about whether simply labeling assets prevents commingling.

On the coins-versus-bullion argument, the court found no evidence that Congress intended to exempt coins from trustee custody requirements.

The Financial Damage

The ruling cost the McNultys dearly.

| Category | Amount |

|---|---|

| Taxable Distribution Value | ~$730,000 |

| Federal Taxes Owed | ~$270,000 |

| Accuracy-Related Penalties | $50,000+ |

| Total Financial Impact | $320,000+ |

And here’s the part that stings most: the McNultys tried to argue “reasonable cause” to avoid the penalties. They claimed they’d relied on Check Book IRA’s advice and done their research.

The court wasn’t persuaded.

It characterized Check Book IRA’s website as “an advertisement of its products and services” rather than professional advice. The court noted that “a reasonable person would recognize it as such and would understand the difference between professional advice and marketing materials.”

The “Checkbook IRA” Myth Explained

For years, promoters marketed “Checkbook IRAs” as a legal way to store gold at home.

The McNulty ruling didn’t just reject this approach—it exposed the fundamental flaw in the reasoning.

How Checkbook IRAs Were Supposed to Work

The pitch went like this: you set up a self-directed IRA, then direct your custodian to purchase membership in a single-member LLC that you control.

The LLC opens a bank account. You, as the LLC’s manager, have “checkbook control” over the funds.

For certain alternative IRA acquisitions—like real estate or private notes—this structure can work. The LLC makes the purchase, and the asset is titled to the LLC (which is owned by your IRA).

Promoters extended this logic to precious metals.

They claimed you could have the LLC purchase gold, then store it at your home because technically the LLC—not you personally—owned the coins.

It sounded clever. It wasn’t legal.

Why the Structure Fails for Precious Metals

Section 408(m) contains special rules for precious metals that don’t apply to other IRA-eligible assets like real estate.

For gold, silver, platinum, and palladium to be held in an IRA, they have to be in the physical possession of an approved trustee.

This requirement exists specifically because precious metals are portable, liquid, and easily concealed.

The checkbook IRA structure might allow you to buy gold through an LLC. But the moment you take physical custody of that gold—even as the LLC’s manager—you’ve violated the trustee possession requirement.

The McNulty court addressed this directly.

It found that Mrs. McNulty’s control over the coins as the LLC’s manager was functionally identical to personal possession. The LLC structure provided no protection.

What Promoters Got Wrong

Companies like Check Book IRA promoted the idea that IRA-owned LLCs could hold precious metals locally, “legally.”

The McNulty ruling demonstrated that this advice was incorrect.

The court noted that Check Book IRA’s website advertised storing “Gold or Silver” at home and offered “Protection by NOT having your IRA Gold or Silver 1,000 miles away.”

This was marketing, not compliance guidance. And the McNultys paid the price for trusting it.

If you’ve been approached with similar pitches—or if you’re currently using this type of arrangement—it’s worth understanding that the IRS position is clear and the courts have upheld it.

The Real IRS Requirements for Gold IRA Storage

Understanding what the IRS actually requires takes the guesswork out of opening a self-directed gold IRA.

The rules are straightforward when you know what to look for.

Approved Trustee Types

The Internal Revenue Code defines who qualifies as a trustee for IRA purposes:

- Banks — Any institution supervised and examined by state or federal banking regulators

- Credit Unions — Insured credit unions meeting federal requirements

- Trust Companies — Corporations subject to state banking supervision and examination

- Non-Bank Trustees — Entities that have demonstrated to the IRS that they’ll administer accounts in compliance with Section 408 requirements

Most precious metals IRAs use specialized custodians—non-bank trustees approved by the IRS specifically for alternative assets.

These custodians partner with approved depositories that handle the physical storage.

Depository Requirements

Approved depositories have to meet rigorous standards for security, insurance, and fiduciary responsibility.

Common depositories used for Gold IRAs include:

- Delaware Depository Service Company — A licensed trust company and COMEX/NYMEX-approved depository with $1 billion in insurance coverage

- Brinks Global Services — A global security leader with facilities in Los Angeles, New York, Salt Lake City, and other locations

- International Depository Services (IDS) — An exchange-approved facility with locations in Delaware, Texas, and Canada

These facilities provide institutional-grade security: 24/7 monitoring, climate control, biometric access, and comprehensive insurance through Lloyd’s of London.

Your custodian handles the relationship with the depository. You choose where your metals are stored, but the custodian manages the paperwork and ensures compliance.

Metal Purity Standards

Not all gold qualifies for IRA inclusion.

The IRS sets minimum fineness requirements:

| Metal | Minimum Fineness | Purity Percentage |

|---|---|---|

| Gold | .995 | 99.5% |

| Silver | .999 | 99.9% |

| Platinum | .9995 | 99.95% |

| Palladium | .9995 | 99.95% |

The American Gold Eagle is the only coin exempted from the gold purity requirement. Despite having a fineness of .9167 (91.67% pure, alloyed with copper and silver for durability), Congress specifically allowed it for IRA inclusion.

Other IRS-approved gold coins include Canadian Maple Leafs, Austrian Philharmonics, and Australian Kangaroos—all of which meet or exceed the .995 fineness standard.

What Happens If You Store IRA Gold at Home

The consequences of home storage are severe and immediate.

Understanding what’s at stake can help you avoid costly mistakes.

Immediate Tax Treatment

The moment you take personal possession of IRA-owned gold, the IRS treats the full value as a distribution.

This isn’t a delayed consequence. It happens in the tax year you take possession.

If your Gold IRA is traditional (pre-tax contributions), the distribution is taxed as ordinary income.

If you moved $100,000 in gold home, that $100,000 gets added to your income for the year.

Depending on your tax bracket, you could owe $22,000 to $37,000 or more in federal income tax alone—plus state taxes if applicable.

The 10% Early Withdrawal Penalty

If you’re under age 59½, the pain compounds.

The IRS assesses a 10% additional tax on early distributions from IRAs. This penalty applies to the full amount of the distribution.

On that $100,000 example? That’s another $10,000.

The penalty exists specifically to discourage people from accessing retirement funds before retirement age. Home storage triggers it automatically because taking possession equals distribution.

Accuracy-Related Penalties

The McNulty case included an additional layer of penalties.

When the underpayment of tax is substantial—or when the IRS determines you were negligent or disregarded rules—it can assess accuracy-related penalties under Section 6662.

These penalties typically equal 20% of the underpayment.

On significant amounts, they add tens of thousands of dollars to an already painful bill.

The McNultys tried to avoid these penalties by claiming reasonable cause—they argued they’d relied on professional advice. The court rejected this defense because the advice came from a company selling the very product in question, not from a tax professional providing independent guidance.

Loss of Tax-Deferred Status

Perhaps the most significant long-term damage: you lose the tax advantages entirely.

A Gold IRA’s value comes from tax-deferred (or tax-free, for Roth) growth. IRS Publication 590-B outlines how distributions work.

When you trigger a distribution through improper storage, you don’t just owe taxes now—you lose the ability to continue deferring taxes on those funds forever.

The compounding benefit of decades of tax-deferred growth disappears instantly.

How Proper Gold IRA Storage Actually Works

The compliant approach to setting up a precious metals IRA is simpler than the schemes promoters try to sell.

Here’s how legitimate Gold IRA storage works.

The Custodian-Depository Relationship

When you open a Gold IRA, you work with three parties:

- A precious metals dealer — Like Brighton, who helps you select IRS-approved products

- A custodian — A company approved by the IRS to hold and administer self-directed IRAs

- A depository — A secure storage facility approved to hold precious metals for retirement accounts

The custodian serves as the trustee that the IRS requires.

They don’t physically hold your metals—that’s the depository’s job—but they maintain the legal relationship and handle all required reporting.

When you purchase metals for your IRA, the dealer ships them directly to your chosen depository. The custodian records the transaction. You receive confirmation that your metals have arrived and are allocated to your account.

You never touch the metals until you take a qualified distribution in retirement.

Segregated vs. Non-Segregated Storage

Most depositories offer two storage options:

Segregated storage keeps your specific metals separate from other customers’ holdings. The exact coins or bars you purchased are stored individually and identified by your account number. When you eventually withdraw, you receive the same items you deposited.

Non-segregated storage (also called commingled or allocated storage) holds your metals alongside those of other customers. The depository tracks the type and quantity you own, but the physical items aren’t separated. When you withdraw, you receive equivalent items meeting the same specifications—but not necessarily the identical pieces.

Both options are fully compliant with IRS requirements.

The choice often comes down to personal preference and cost—segregated storage typically carries slightly higher fees.

For owners who value knowing they’ll receive their exact pieces, segregated storage provides peace of mind. For those focused primarily on the metal’s value, non-segregated storage works just as well at a lower cost.

The Rollover Process

Most Gold IRAs are funded through rollovers from existing retirement accounts.

This process is straightforward when handled correctly.

A direct rollover (trustee-to-trustee transfer) moves funds from your existing 401(k), traditional IRA, or other qualified account directly to your Gold IRA custodian. The money never touches your hands.

This is the cleanest approach. There’s no withholding, no 60-day deadline, and no risk of accidentally triggering a taxable distribution.

An indirect rollover gives you possession of the funds for up to 60 days. You receive a check, deposit it into your account, then write a check to your new custodian. This works, but it’s riskier—miss the 60-day window, and you’ve got a taxable distribution.

Executing a precious metals IRA rollover through direct transfer typically takes two to three weeks from start to finish.

The custodian handles the paperwork. You choose the metals. The depository confirms receipt.

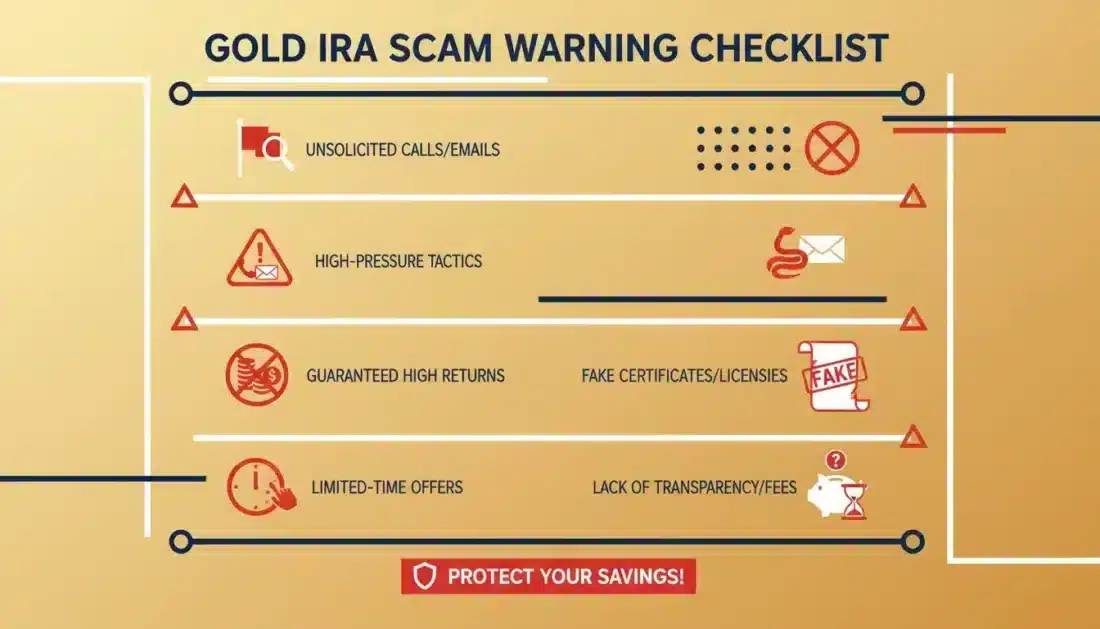

Recognizing Home Storage Schemes

Knowing what to avoid is just as important as knowing what to do.

Promoters of home storage schemes use specific tactics to make non-compliant arrangements sound legitimate.

Red Flags to Watch For

Be cautious of any company that advertises:

- “Home storage” or “private storage” Gold IRAs — These phrases signal non-compliant arrangements

- “Checkbook control” for precious metals — This structure fails for gold and silver specifically

- Storage “at home” or “in your possession” — Direct violation of trustee requirements

- “Keep your metals close” or “1,000 miles away” language — Appeals to emotion over compliance

- Promises of “legal” home storage — The McNulty ruling proves otherwise

Legitimate Gold IRA providers are straightforward about storage requirements.

They explain that metals have to be stored at approved depositories. They don’t promise workarounds or loopholes.

Questions to Ask Before Opening an Account

Protect yourself by asking direct questions:

- Where will my metals be physically stored?

- Is the depository approved by the IRS for retirement account storage?

- Will I ever have physical possession of the metals while they’re in my IRA?

- Who serves as the trustee for my account?

- Can you provide documentation of your custodian’s IRS approval?

Any hesitation or evasion in answering these questions should prompt you to look elsewhere.

The True Cost of “Convenience”

Home storage schemes appeal to a natural desire for control.

There’s something satisfying about the idea of holding your retirement savings in your hands.

But that convenience comes at an enormous cost.

The McNultys didn’t just pay hundreds of thousands in taxes and penalties. They lost the entire tax-deferred benefit of their IRAs. They paid lawyers to fight the IRS and lost. They became a cautionary tale cited in IRS publications and tax court decisions.

Proper Gold IRA storage at a professional depository costs a few hundred dollars per year in fees.

That’s a rounding error compared to the tax consequences of improper storage.

The Security Benefits of Professional Storage

Beyond compliance, professional depositories offer security that no home safe can match.

Understanding these benefits helps put storage costs in perspective.

Insurance Coverage

Professional depositories maintain comprehensive insurance policies—typically through Lloyd’s of London—covering theft, natural disasters, employee malfeasance, and in-transit losses.

Delaware Depository, for example, carries $1 billion in coverage. Your metals are protected whether they’re sitting in the vault or being transported for delivery.

Home storage? Your homeowner’s insurance likely provides minimal coverage for precious metals—often capped at a few thousand dollars. Separate riders are expensive and still don’t match institutional coverage levels.

Physical Security

Approved depositories use multiple layers of protection:

- Class 3 vault construction — Reinforced concrete, steel barriers, and penetration-resistant design

- 24/7 monitoring — Motion sensors, seismic detection, and continuous video surveillance

- Biometric access controls — Only authorized personnel can enter storage areas

- Armed security — On-site guards and rapid response capabilities

- Redundant systems — Backup power, fire suppression, and climate control

Your home safe might be rated for burglary resistance, but it can’t match the security infrastructure of a facility designed specifically for precious metals storage.

Professional Inventory Management

Depositories maintain meticulous records of every item in their custody.

Regular audits verify that holdings match account records. Serial numbers are tracked. Purity is confirmed on intake.

This documentation matters for insurance claims, estate planning, and IRS compliance.

When you eventually take distributions, you have clear records of what you own and when you acquired it.

Home storage relies on your personal record-keeping. In a dispute—whether with the IRS or an insurance company—professional documentation carries more weight than personal notes.

What to Do If You’re Currently Using Home Storage

If you’ve been storing IRA gold at home based on promoter advice, you’re not alone.

The question is what to do now.

Assess Your Situation

The first step is understanding where you stand.

Consider:

- When did you take possession of the metals?

- What’s the current value compared to what you paid?

- Have you reported the distribution on previous tax returns?

- What documentation do you have about the arrangement?

The answers affect your options and potential exposure.

Consult a Tax Professional

This situation requires professional guidance—not from the company that sold you the arrangement, but from an independent CPA or tax attorney.

A tax professional can help you understand:

- Whether you need to amend prior tax returns

- What penalties you might face

- Whether voluntary disclosure makes sense

- How to minimize damage going forward

The IRS often treats voluntary compliance more favorably than discovered violations.

A professional can help you navigate this decision.

Consider Corrective Action

Depending on your situation, options might include:

- Moving metals to an approved depository — This won’t undo past violations, but it stops future ones

- Amending tax returns — If you haven’t reported distributions, correcting this proactively is usually better than waiting for an audit

- Liquidating and restarting — In some cases, closing the problematic arrangement and opening a compliant account makes sense

There’s no one-size-fits-all answer.

Your specific circumstances—including the amounts involved, your tax bracket, and how long you’ve been out of compliance—all factor into the best path forward.

Building a Compliant Gold IRA Strategy

Holding physical gold in a retirement account can be a sound approach to determining gold allocation for retirement.

The key is doing it correctly from the start.

Choosing the Right Custodian

Not all IRA custodians handle precious metals.

You need a self-directed IRA custodian that specifically allows alternative assets.

Look for:

- IRS approval documentation — The custodian should be able to verify their status

- Established depository relationships — Good custodians work with multiple approved facilities

- Clear fee schedules — Understand annual fees, transaction costs, and storage charges upfront

- Responsive service — You’ll interact with them for years; customer service matters

Brighton works with established custodians who specialize in precious metals IRAs.

This ensures compliance from day one.

Selecting Appropriate Metals

Focus on IRS-approved products that serve your goals:

- American Gold Eagles — The most popular IRA gold coin, available in 1 oz, ½ oz, ¼ oz, and 1/10 oz sizes

- American Silver Eagles — Meet purity requirements with .999 fineness

- Gold and silver bars — Must be from accredited refiners and meet fineness standards

- Other sovereign coins — Canadian Maple Leafs, Austrian Philharmonics, and Australian products

Avoid collectibles, numismatic coins, and anything marketed for its rarity rather than its metal content.

If a coin’s value comes primarily from its collectible nature, it probably doesn’t qualify.

Understanding the benefits of physical gold ownership helps you build an allocation that matches your goals.

Setting Realistic Expectations

Gold in an IRA offers potential benefits, but it’s important to understand the realities:

- You won’t have immediate access — Your metals stay at the depository until you take qualified distributions

- There are ongoing costs — Storage and custodian fees are part of the arrangement

- Liquidity requires coordination — Selling requires working through your custodian

- Values fluctuate — Precious metals may appreciate, depreciate, or remain unchanged

These aren’t drawbacks so much as realities.

Understanding them upfront helps you set appropriate expectations and avoid disappointment.

Frequently Asked Questions

Is a “Home Storage Gold IRA” legal in 2026?

No. The IRS requires that all precious metals held in an IRA be stored with an approved trustee or depository. Home storage—even through an LLC structure—results in a taxable distribution. The 2021 McNulty v. Commissioner ruling confirmed this position, and IRS enforcement continues in 2026.

What was the McNulty v. Commissioner gold IRA ruling?

In November 2021, the U.S. Tax Court ruled in McNulty v. Commissioner (157 T.C. No. 10) that storing IRA-owned gold coins at home—even through an LLC structure—constitutes a taxable distribution. The McNultys owed approximately $270,000 in taxes plus over $50,000 in penalties for storing American Eagle coins in a home safe. The court found that personal possession of IRA assets gives the owner “unfettered control,” which violates the fundamental nature of an IRA.

What are the penalties for storing IRA gold at home?

Storing IRA gold at home triggers immediate taxation on the full value of the metals as a distribution. If you’re under age 59½, you’ll also face a 10% early withdrawal penalty. The IRS may assess additional accuracy-related penalties of 20% if the violation is deemed negligent. Combined, these consequences can consume 40% or more of your metals’ value in a single tax year.

Can I store gold in a safe deposit box at my bank for an IRA?

No. A personal safe deposit box doesn’t meet IRS trustee requirements, even at a bank. IRS regulations under Section 1.408-2(e) require that assets needing safekeeping be held in an “adequate vault” under trustee control. A safe deposit box to which you have personal access doesn’t satisfy this requirement—the trustee has to maintain exclusive control over the metals.

Who is allowed to have physical possession of my Gold IRA metal?

Only an IRS-approved trustee or custodian can have physical possession of your Gold IRA metals. This typically means storage at approved depositories like Delaware Depository, Brinks Global Services, or International Depository Services (IDS). You maintain ownership, but the physical custody remains with the trustee until you take a qualified distribution.

How does the IRS find out if I store my IRA gold at home?

The IRS has multiple detection methods. Custodians are required to report IRA transactions. Precious metals dealers maintain shipping records. Bank transactions can reveal purchases. Standard IRS audits may uncover discrepancies. The McNulty case was discovered through routine IRS review. The penalties for non-compliance—potentially 40% or more of the metals’ value—far outweigh any perceived benefit of home storage.

What is the difference between segregated and non-segregated gold IRA storage?

Segregated storage keeps your specific metals separate from other customers’ holdings—you receive the exact coins or bars you purchased when you withdraw. Non-segregated (commingled) storage holds your metals alongside others in a common vault area; you receive equivalent metals meeting the same specifications, but not necessarily the same physical items. Both options are IRS-compliant when held at approved depositories. Segregated storage typically costs slightly more but provides the assurance of receiving your original pieces.

Can I use a “Checkbook IRA” or LLC structure to store gold at home?

No. The McNulty ruling specifically addressed and rejected this arrangement. The court found that even when gold is titled to an IRA-owned LLC, the account owner taking physical possession as the LLC’s manager triggers a taxable distribution. The LLC structure doesn’t change the fundamental IRS requirement under Section 408(m) that precious metals must remain with an approved trustee. This approach was marketed heavily but has been definitively ruled non-compliant.

Conclusion

The question “Can I store my Gold IRA at home?” has a clear answer in 2026: no.

The IRS requires trustee custody of precious metals in IRAs. The courts have upheld this requirement. And the penalties for non-compliance are severe.

The McNulty ruling removed any ambiguity about “checkbook IRAs” and LLC structures for precious metals. Home storage triggers immediate taxation, potential penalties of 10% or more, and the permanent loss of tax-deferred status.

But here’s what’s worth remembering: compliant Gold IRA storage isn’t difficult.

Professional depositories offer institutional-grade security and insurance at reasonable costs. Custodians handle the paperwork. And you maintain full ownership of your metals until you’re ready to take distributions in retirement.

The path to holding physical gold in a retirement account runs through approved depositories—not through your basement or a promoter’s workaround scheme.

That’s the clarity and peace of mind that comes from doing it right.

Ready to Explore a Compliant Gold IRA?

If you’ve been wondering how to hold physical gold the right way—without the risks of home storage schemes—we can help you understand your options.

Brighton offers a complimentary consultation to walk through the process, including our No Fee Precious Metals IRA, which covers custodial fees for the lifetime of the account on qualified purchases.

We’ll show you exactly:

- How the No Fee IRA works and whether you qualify

- The difference between U.S.-minted coins and foreign alternatives

- What to expect from the purchasing and delivery process

- How to roll over or transfer existing retirement funds

- What ongoing support looks like after your purchase

Learn About the No Fee IRA — no obligation, just actionable insights you can use whether you work with us or not.

If you’ve been researching Gold IRAs or considering acquiring U.S.-minted gold coins for your retirement, getting clarity on storage requirements is the essential first step.