What Makes the American Silver Eagle Ideal for an IRA in 2026?

Here’s a surprise most people don’t know: the IRS doesn’t allow just any silver coin inside a retirement account.

In fact, most silver products are flat-out prohibited. Buy the wrong one with IRA funds, and the IRS treats it like you took a cash withdrawal — complete with taxes and a potential 10% penalty.

But the American Silver Eagle? It’s one of the few silver coins specifically named in the tax code as approved for IRAs.

That’s not a suggestion from a financial website. It’s federal law — IRC Section 408(m)(3).

Every Silver Eagle contains one troy ounce of .999 fine silver. The U.S. Mint backs every coin for weight, content, and purity. And it carries a $1 face value as legal tender.

Now here’s what makes 2026 different from any year before it.

This year’s Silver Eagle isn’t just another annual release. It’s a once-in-a-generation commemorative coin — marking both the 40th anniversary of the Silver Eagle series and America’s 250th birthday. For the first time ever, the Mint struck it with a dual date — “1776–2026” — and a Liberty Bell privy mark featuring the numeral “250.”

That combination — IRS compliance, U.S. government backing, and historic commemorative value — is why the 2026 Silver Eagle stands apart.

Whether you’re evaluating silver as a retirement strategy or comparing gold and silver acquisitions for the first time, this guide walks you through what makes this coin a cornerstone for a physical silver IRA — and why the window to acquire it won’t last.

Why the IRS Specifically Approves the Silver Eagle

Most people assume any silver coin can go into an IRA.

It can’t. And the consequences of getting it wrong are steep.

What Happens If You Choose the Wrong Silver

The IRS classifies most coins, stamps, metals, gems, and artwork as “collectibles.” That’s the default under IRC Section 408(m).

If your IRA purchases a collectible? The IRS treats it like you took a distribution — right then and there. You’d owe income tax on the full amount, plus a potential 10% early withdrawal penalty if you’re under 59½.

That’s a costly mistake. And it’s entirely avoidable.

The Exception That Makes Silver Eagles Different

Congress carved out a narrow exception to that collectibles rule. Section 408(m)(3) allows two categories of precious metals inside an IRA:

- Specific U.S. Mint coins — Gold, silver, and platinum coins described in Title 31 of the United States Code. The American Silver Eagle falls right here.

- Bullion meeting minimum purity — Silver must be .999 fine. Gold must be .995. Platinum and palladium must be .9995. And the metal has to be held by a qualified trustee.

What makes the Silver Eagle unique? It qualifies under both rules. It’s a congressionally approved coin and it meets the .999 purity standard.

No generic round can say that.

Why U.S. Government Backing Matters for Your Retirement

When the U.S. Mint stamps its mark on a Silver Eagle, it’s confirming three things: the coin weighs exactly 31.103 grams, contains exactly one troy ounce of .999 fine silver, and carries legal tender status.

Why does that matter?

Private mints produce beautiful silver rounds — and many do contain .999 silver. But there’s no federal confirmation behind those claims. The burden of verifying what you actually own falls on you.

With a Silver Eagle, that verification is built in. Every dealer, every depository, and every custodian in the country recognizes it on sight.

That kind of acceptance translates directly into liquidity — and peace of mind — especially during times of economic uncertainty.

The 2026 Semiquincentennial: A Historic “Key-Date” Release

The American Silver Eagle has been minted every year since 1986.

That’s four decades of consistent production, consistent purity, and consistent global demand.

But 2026 isn’t a typical year. It’s a dual-anniversary milestone — and it won’t happen again.

40 Years of the Silver Eagle

The Silver Eagle program launched in 1986 under the Liberty Coin Act. Congress told the U.S. Mint to convert excess silver from the Defense National Stockpile into government-backed bullion coins.

Since then? Over 700 million Silver Eagles sold worldwide.

No other silver bullion coin — domestic or foreign — can match that track record. Four decades of unbroken production, consistent purity, and universal market acceptance.

That kind of history matters when you’re deciding what to hold in a retirement account.

America’s 250th Birthday — and the Liberty Bell Privy Mark

July 4, 2026, marks the Semiquincentennial — the 250th anniversary of the signing of the Declaration of Independence.

To honor this milestone, the U.S. Mint added two features to the 2026 Silver Eagle that have never appeared on the coin before:

- Dual dating — The inscription “1776–2026” replaces the standard single year. It’s the first time in 40 years that a Silver Eagle has carried two dates.

- Liberty Bell privy mark — A small Liberty Bell with the numeral “250” struck into the obverse. A direct reference to the nation’s founding.

These features exist only on the 2026 issue. Once the Mint moves to 2027, this edition is done. It won’t be produced again.

What Does “Key Date” Mean for You?

In the coin world, a “key date” is a year with lower production numbers, unique design features, or historical significance that sets it apart.

The 2026 Silver Eagle checks all three boxes.

Now — for IRA purposes, the coin’s value is reported at melt value. That’s the spot price of one ounce of .999 silver on any given day. Same standard for all bullion in retirement accounts.

But the commemorative significance could drive stronger secondary-market demand when it’s time to sell or take a distribution. That’s a practical advantage worth knowing about.

Precious metals may appreciate, depreciate, or remain unchanged.

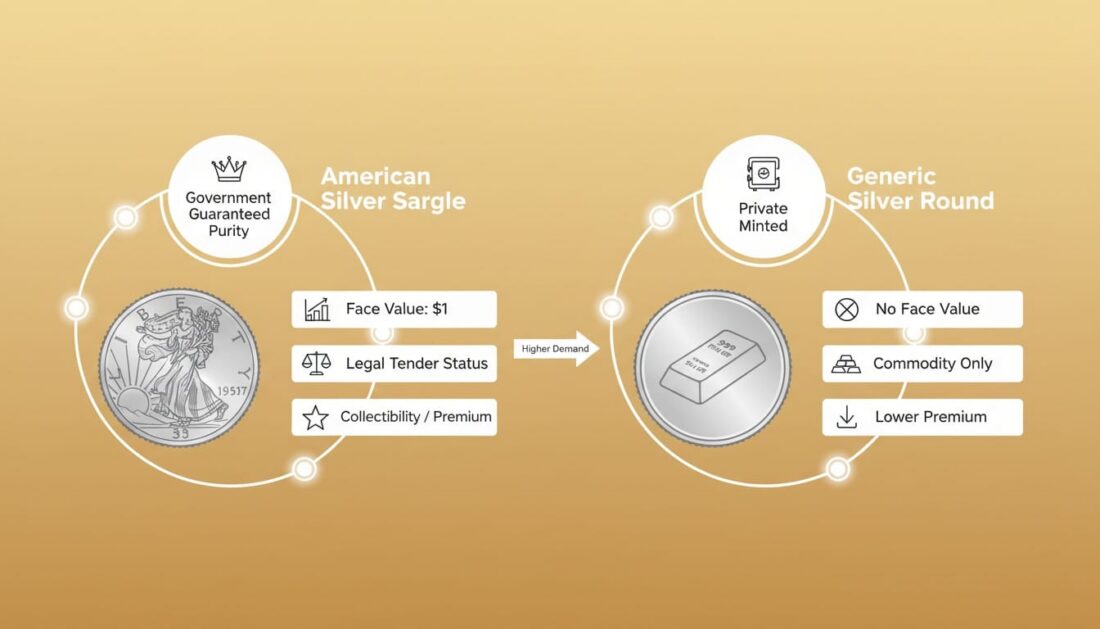

Silver Eagle vs. Generic Round: What the Premium Actually Pays For

Here’s a question we hear all the time from first-time silver owners:

“Why would I pay more for a Silver Eagle when I can get the same ounce of silver in a round for less?”

Fair question. And the answer comes down to what happens when it’s time to sell.

That Premium Comes Back to You

Silver Eagles typically carry a higher premium over spot price than generic rounds — often $4 to $8 per ounce depending on market conditions.

But here’s what most people miss: you get that premium back when you sell.

Dealers consistently pay more for Silver Eagles than for generic rounds. The demand simply doesn’t stop. During the 2008 financial crisis, Silver Eagles held significantly higher premiums while generic products became difficult to move.

That’s the real value of the premium. It’s not a markup. It’s a liquidity advantage.

When you’re building a retirement position, you’re not just acquiring silver. You’re acquiring the ability to convert it back to cash — quickly and at a fair price — whenever you’re ready.

Side-by-Side Comparison

| Feature | American Silver Eagle | Generic Silver Round |

|---|---|---|

| Producer | U.S. Mint (federal government) | Private mints (varies) |

| Purity | .999 fine silver (1 troy oz) | .999 fine silver (1 troy oz) |

| Legal Tender | Yes — $1 face value | No |

| Government Backing | Weight, content, and purity confirmed by U.S. government | No government backing |

| IRA Eligible | Yes — specifically named in IRC 408(m)(3) | Only if from accredited refiner meeting .999 standard |

| Anti-Counterfeiting | Type 2 reeded edge variation + hidden features | None standard |

| Global Recognition | Universally accepted by dealers worldwide | Varies by mint and design |

| Typical Buyback | Higher — strong secondary market demand | Lower — trades closer to melt value |

Both products contain the same amount of silver. But the Silver Eagle gives you federal confirmation, IRA approval by name, built-in anti-counterfeiting features, and unmatched resale demand.

That’s what the premium pays for.

The Silver Market in 2026: Why Physical Supply Matters

You don’t need to be a market analyst to see what’s happening with silver right now.

The world is using more silver than it’s producing. And it’s been that way for six years straight.

Six Years of Running Short

According to the Silver Institute, the global silver market is headed for its sixth consecutive annual deficit in 2026. Demand keeps outpacing supply — with a projected shortfall of roughly 67 million ounces this year alone.

This isn’t a blip. The cumulative deficit from 2021 through 2025 hit approximately 820 million ounces, according to Metals Focus. That gap has been filled by drawing down above-ground inventories — essentially spending silver that was already mined and stored.

Here’s what’s driving it:

- Mine production — About 820 million ounces expected in 2026, barely up from last year. Silver is mostly a byproduct of copper, zinc, and gold mining — so even when silver prices rise, new supply doesn’t automatically follow.

- Industrial demand — Around 650 million ounces projected. Solar panels, electronics, electric vehicles, and green technology all require silver — and those sectors keep growing.

- Physical ownership demand — Forecast to jump 20% in 2026 to a three-year high of 227 million ounces, as more people respond to tight supply and rising prices.

What Does That Mean If You Own Silver Eagles?

When physical silver gets tight, government-minted coins tend to feel the effects first. The U.S. Mint sources its silver blanks from approved suppliers — and when those suppliers face raw material pressure, production slows down.

We saw this play out during the 2020–2021 supply squeeze. Silver Eagle premiums climbed sharply. Owners who already held Eagles watched their coins strengthen in resale value while generic products struggled to find buyers.

In 2026, the picture is further complicated by China’s decision to tighten silver export controls — placing silver under an approval-based licensing system similar to rare earth minerals. China refines an estimated 60–70% of the world’s silver. That policy shift has added another layer of pressure to an already tight market.

So what does this mean for someone holding physical Silver Eagles in a retirement account?

It means you own the actual metal. It doesn’t depend on a fund manager, a bank’s balance sheet, or a foreign government’s export rules.

It sits in a vault. With your name on it.

How to Add Silver Eagles to Your IRA

Most people are surprised by how simple this process actually is.

You don’t need special expertise. You don’t need weeks of paperwork. And you don’t have to move everything you’ve built to make it work.

Here’s what the process looks like — step by step.

Step 1: Open a Self-Directed IRA

A regular brokerage IRA won’t work for physical metals. You’ll need a self-directed IRA custodian — a financial institution the IRS has approved to hold things like gold, silver, platinum, and palladium.

The custodian handles the administrative side: account setup, IRS reporting, records, and coordination with the depository where your metals are stored.

What should you look for?

- IRS approval and a clean regulatory record

- Transparent fees — setup, annual, and storage

- Experience with precious metals accounts

- Responsiveness when you have questions

Step 2: Fund the Account

There are three main ways to put money into a self-directed precious metals IRA:

- Direct transfer — Your current IRA custodian sends funds straight to the new custodian. The money never touches your hands. This is the simplest and most common method.

- Rollover — Funds from a 401(k), TSP, or other qualified plan are distributed to you and then deposited into the new IRA within 60 days. One rollover per 12-month period is allowed.

- Cash contribution — Direct deposits up to the annual IRA limit. For 2026, that’s $7,500 if you’re under 50 or $8,600 if you’re 50 and older.

Here’s what most people don’t realize — the majority of customers fund their precious metals IRA through a transfer or rollover from an existing account. That means there’s no contribution limit on the amount moved. You’re simply relocating funds from one qualified account to another.

If you’re considering moving an existing IRA into precious metals, the process typically wraps up in under two weeks.

Consult your CPA or tax professional for guidance specific to your situation.

Step 3: Choose Your 2026 Silver Eagles

Once your account is funded, you work with a precious metals dealer like Brighton to pick your products. For the 2026 Semiquincentennial Silver Eagle, you’ll want to confirm:

- The coins are bullion-grade — not proof or burnished collectible versions, which carry higher premiums

- They meet the .999 fine silver standard

- They’re sourced from the U.S. Mint’s authorized distribution network

Your dealer coordinates directly with your custodian to make sure everything is properly documented and compliant. Brighton’s concierge service means you’re supported through every step — from product selection to depository delivery.

Step 4: Secure Depository Storage

IRS rules require that IRA-held precious metals be stored in an approved depository — not in your home, not in a safe deposit box, and not in your personal possession.

This isn’t a limitation. It’s a protection.

Approved depositories offer segregated storage — meaning your metals are held separately, identified as yours alone, and fully insured. You’ll receive regular statements from your custodian showing exactly what you own and where it’s stored.

Here’s a quick look at how the steps come together:

| Step | What Happens | Who Handles It | Typical Timeline |

|---|---|---|---|

| Open SDIRA | Select custodian, complete application | You + custodian | 1–3 business days |

| Fund account | Transfer, rollover, or contribution | Custodian coordinates | 3–10 business days |

| Select products | Choose 2026 Silver Eagles (bullion-grade) | You + Brighton | Same day as funding |

| Depository storage | Coins shipped to approved vault, segregated | Brighton + depository | 3–5 business days |

Most customers complete this entire process in under two weeks. And with Brighton’s support at every stage of ownership, you’re never guessing what comes next.

How to Verify Your 2026 Silver Eagle Is Authentic

Counterfeiting is a real concern in the precious metals world. And the more popular a coin is, the more counterfeiters target it.

The Silver Eagle is the most popular silver bullion coin on the planet. So the U.S. Mint takes authentication seriously.

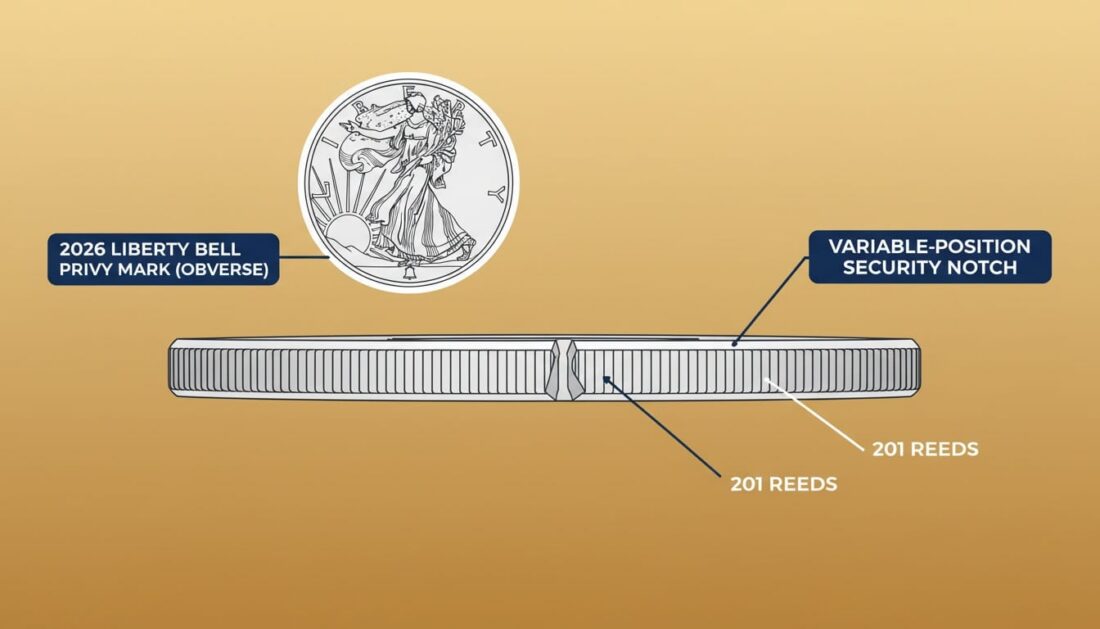

Type 2 Anti-Counterfeiting Features

In 2021, the Mint introduced the Type 2 design — the first major update to the Silver Eagle’s reverse in 35 years. Along with a new eagle design by Emily Damstra, the Mint added multiple layers of anti-counterfeiting technology:

- Reeded edge variation — The coin’s edge has 201 reeds (tiny grooves). At one specific position, a small notch interrupts the pattern. The Mint moves that notch to a different position each year — which makes old counterfeiting dies useless for new releases.

- Hidden features — The Mint has confirmed that additional covert security elements are embedded in the design but has intentionally not disclosed what they are. This makes replication significantly harder.

- 2026-specific markers — The Liberty Bell privy mark with “250” and the dual date “1776–2026” are unique to this single production year. Any coin claiming to be a 2026 Silver Eagle without these features is immediately suspect.

What to Check When You Receive Your Coins

Whether your Silver Eagles are going straight to a depository or you’re taking physical delivery down the road, here’s what to look for:

- Weight: exactly 31.103 grams (1 troy ounce)

- Diameter: 40.6 mm

- Thickness: 2.98 mm

- Edge: 201 reeds with year-specific notch position

- Obverse: Walking Liberty design with “1776–2026” dual date and Liberty Bell privy mark

- Reverse: Emily Damstra’s Type 2 eagle with oak branch

If you’re purchasing through an authorized dealer like Brighton — who sources directly from the U.S. Mint’s distribution network — the risk of encountering a counterfeit is extremely low. But knowing these details gives you an added layer of confidence.

Taking Physical Delivery: In-Kind Distributions Explained

One of the most common questions from new precious metals owners is this: “If my silver is sitting in a vault, can I ever actually hold it?”

The answer is yes. And the process has a name — it’s called an in-kind distribution.

How In-Kind Distributions Work

Once you hit 59½ — or meet another qualifying condition like disability or a first-time home purchase — you can request that your custodian distribute the actual coins to you instead of selling them for cash.

Here’s what that looks like:

- You contact your custodian and request an in-kind distribution of specific metals

- The custodian coordinates with the depository to package and ship your Silver Eagles directly to your home

- The fair market value of the coins on the distribution date is reported on Form 1099-R

- That value is treated as taxable income for the year — just like a cash distribution would be

The key difference? You end up holding the actual coins. You didn’t have to sell at a time that might not have matched your goals.

Why This Matters for Legacy Planning

Many of Brighton’s customers aren’t just thinking about their own retirement. They’re thinking about what they’ll leave behind.

Physical silver and gold can be passed to children and grandchildren — directly, tangibly, without depending on a brokerage account or a financial institution to process the transfer.

An in-kind distribution lets you move your metals out of the IRA structure and into your personal possession. From there, you decide what happens next — whether that’s holding for the long term, gifting to family, or using the metal as you see fit.

That level of control is one of the biggest reasons people choose physical metals in the first place.

Distribution Types at a Glance

| Distribution Type | What You Receive | Tax Treatment | When It’s Available |

|---|---|---|---|

| Cash distribution | Dollar amount from metal sale | Taxable as ordinary income | Age 59½ or qualifying event |

| In-kind distribution | Physical coins shipped to you | FMV taxable as ordinary income | Age 59½ or qualifying event |

| Required Minimum Distribution (RMD) | Cash or in-kind (your choice) | Taxable as ordinary income | Age 73 (current rules) |

| Inherited IRA distribution | Cash or in-kind (beneficiary decides) | Varies by beneficiary type | Upon account holder’s passing |

Consult your CPA or tax professional for guidance specific to your situation. Distribution rules can vary based on account type, age, and individual circumstances.

Building a Retirement Strategy Around Physical Silver

So you understand the Silver Eagle’s legal standing, its 2026 commemorative significance, and the mechanics of getting it into an IRA.

Now the question becomes: how does physical silver fit into a broader retirement picture?

Why Tangible Ownership Matters

Most retirement accounts are built entirely around dollar-denominated products — money market accounts, brokerage funds, mutual funds, cash equivalents.

There’s nothing wrong with those vehicles. But they all share one thing in common: they depend on the purchasing power of the U.S. dollar.

When the dollar loses value — through inflation, monetary expansion, or policy shifts — everything priced in dollars loses purchasing power with it.

Physical silver doesn’t carry that same exposure. It’s a tangible product with global demand that exists outside the banking system. You own it. You hold it. And its value isn’t tied to a single currency.

That’s not a prediction about what the dollar will do. It’s a structural reality about how physical metals function differently from paper-based products.

How Silver and Gold Work Together

Most customers at Brighton don’t choose between gold and silver. They use both — and for different reasons.

Gold tends to carry a higher per-ounce value and a lower premium relative to spot. It’s often the foundation of a precious metals IRA.

Silver offers a lower entry point per ounce — which means you can acquire more physical metal with the same dollar amount. It also carries stronger industrial demand, which can drive price movement in ways that differ from gold.

The 2026 Silver Eagle, with its IRA eligibility and commemorative features, fits naturally alongside gold products in a well-rounded retirement approach.

What Does Getting Started Look Like?

If this is new territory for you, here’s the reality: most of Brighton’s customers felt the same way before their first conversation.

The process isn’t complicated. The terminology can seem dense at first, but once someone walks you through it, the pieces fall into place quickly.

That’s the whole point of Brighton’s concierge approach. You’re not left sorting through fine print on your own. You get clear answers, a straightforward process, and support at every stage of ownership.

Precious metals may appreciate, depreciate, or remain unchanged.

Frequently Asked Questions

Is the 2026 American Silver Eagle IRA eligible?

Yes. The American Silver Eagle is specifically named in the tax code — IRC Section 408(m)(3) — as an approved silver coin for IRAs.

Every Silver Eagle, including the 2026 Semiquincentennial release, meets the mandatory .999 fine silver purity standard. As long as your self-directed IRA custodian stores the coins in an IRS-approved depository, you’re fully compliant.

There’s no special paperwork or exception needed. The Silver Eagle’s IRA eligibility is written into federal law.

What’s the difference between a Silver Eagle and a silver round for an IRA?

Silver Eagles are produced by the U.S. Mint, carry a $1 face value, and are specifically named in the tax code as IRA-approved.

Silver rounds come from private mints, carry no legal tender status, and have to meet .999 purity from an accredited refiner to qualify for IRA inclusion.

The biggest practical difference? Liquidity. Silver Eagles typically command higher buyback prices because they’re universally recognized and trusted. When it’s time to sell or take a distribution, that recognition matters.

How does the Liberty Bell privy mark affect the value of my 2026 Silver Eagle?

The Liberty Bell privy mark with the numeral “250” is a one-year-only design element honoring America’s 250th birthday. It’s the first time a Silver Eagle has ever carried a dual date or a privy mark.

For IRA purposes, the coin is still valued at melt — the spot price of one troy ounce of .999 silver. That’s the standard for all bullion held in retirement accounts.

But outside an IRA — or when it comes time for a distribution — the commemorative nature of this release could drive stronger secondary-market demand. Collectors and precious metals owners both recognize the significance of a key-date coin.

Precious metals may appreciate, depreciate, or remain unchanged.

Why does the IRS allow Silver Eagles but not all silver coins?

The IRS considers most coins “collectibles” — and collectibles are prohibited in retirement accounts. It’s a blanket rule under IRC Section 408(m).

But Congress created a specific exception in Section 408(m)(3) for U.S. Mint coins and for bullion meeting minimum purity standards. The Silver Eagle qualifies on both counts — it’s congressionally approved and it hits the .999 fine silver mark.

Many foreign or privately minted silver coins don’t meet one or both of those requirements. That’s why the Silver Eagle occupies a unique position in the IRA world.

Can I take physical delivery of my Silver Eagles when I retire?

Absolutely. Once you reach 59½ — or meet another qualifying condition — you can request an in-kind distribution.

Instead of selling the metals and getting a cash deposit, your custodian arranges for the actual coins to be shipped to you. The fair market value on the distribution date gets reported as taxable income on Form 1099-R.

Many owners prefer this route because it lets them hold the physical metal without selling at a time that might not match their goals. From there, you decide what to do with it — hold it, gift it to family, or continue building for the future.

What are the security features on the 2026 American Silver Eagle?

The 2026 Silver Eagle uses the Type 2 design introduced in 2021. It includes both visible and hidden anti-counterfeiting measures.

The most obvious feature is the reeded edge variation — a small notch that interrupts the coin’s 201 reeds at a specific position. The Mint rotates that notch each year, making old counterfeiting dies useless.

The 2026 release also carries the Liberty Bell privy mark with “250” and the dual date “1776–2026.” These markers are unique to this single production year — which makes verifying a coin’s authenticity straightforward.

How much can I contribute to a Silver IRA in 2026?

For 2026, the IRS set contribution limits at $7,500 for those under 50 and $8,600 for those 50 and older. These limits apply across all your Traditional and Roth IRAs combined.

But here’s what most people don’t realize — the majority of precious metals IRA owners fund their accounts through rollovers or transfers from existing 401(k)s, Traditional IRAs, or TSPs. Those moves aren’t subject to annual contribution limits.

You’re simply relocating funds from one qualified account to another. Consult your CPA or tax professional for guidance specific to your situation.

Is now a good time to add Silver Eagles to my IRA?

Timing any acquisition is a personal decision. And precious metals may appreciate, depreciate, or remain unchanged.

That said — the silver market has posted structural deficits for six consecutive years. Physical supply remains tight. Global demand keeps outpacing mine production. And the 2026 Silver Eagle is a one-time commemorative release that won’t be produced after this year.

Whether those factors align with your goals is something worth exploring. Brighton’s team can walk you through your options — no pressure, no obligation.

Brighton does not provide financial, legal, or tax advice.

Conclusion

The 2026 American Silver Eagle isn’t just another coin on a dealer’s shelf. It’s a federally approved, U.S. Mint-backed product with a 40-year track record — and this year’s release carries commemorative features that will never be repeated.

For retirement-focused owners, it brings together everything that matters: IRS compliance by name, .999 purity, built-in anti-counterfeiting technology, unmatched global liquidity, and a historic Semiquincentennial design.

Whether you’re exploring a precious metals IRA for the first time or adding to what you’ve already built, the 2026 Silver Eagle deserves a closer look.

Ready to see how physical silver fits into your retirement picture?

If you’re thinking “this all makes sense, but I don’t have time to figure it out on my own,” you’re not alone. Most customers we work with felt the same way before they realized how straightforward the process can be with the right guidance.

That’s why we offer a complimentary consultation to walk you through your options — including our No Fee Precious Metals IRA, which covers custodial fees for the lifetime of the account on qualified purchases.

We’ll show you exactly:

- How the No Fee IRA works and whether you qualify

- The difference between U.S.-minted coins and foreign alternatives

- What to expect from the purchasing and delivery process

- How to roll over or transfer existing retirement funds

- What ongoing support looks like after your purchase

Learn About the No Fee IRA — no obligation, just actionable insights you can use whether you work with us or not.

The 2026 Semiquincentennial Silver Eagle is a one-year release. Once it’s gone, it’s gone. If owning a piece of American history inside your retirement account sounds like it fits your goals, now’s the time to explore your options.