Here’s what most people don’t realize: the IRS doesn’t care how much of your 401(k) you roll over to gold. There’s no minimum. No required percentage. You can move all of it, part of it, or none of it—and as long as you follow the rules, you won’t owe a penny in taxes or penalties.

So which path makes more sense for your situation?

A partial rollover lets you keep some money in your existing 401(k) while moving a portion into a Self-Directed Gold IRA. A full rollover consolidates everything into one account—backed entirely by physical precious metals.

Both options work. Both are tax-free when done correctly.

The real question isn’t which one is “better.” It’s which one fits your goals, your timeline, and the kind of peace of mind you’re looking for.

Let’s walk through both—step by step—so you can make the decision that’s right for you.

What Is a 401(k) to Gold Rollover, Exactly?

Before we compare partial and full rollovers, let’s make sure we’re on the same page.

A Gold IRA—sometimes called a precious metals IRA—is a special type of Self-Directed IRA. Instead of holding paper assets, it holds physical gold, silver, platinum, or palladium in an IRS-approved depository.

You own the metal. It’s stored in your name. And it stays tax-deferred until you take distributions in retirement.

When you’re executing a precious metals IRA rollover, you’re simply moving funds from your current 401(k)—or another retirement account like a 403(b), TSP, or traditional IRA—into this new Gold IRA.

The process is straightforward. Most rollovers complete in 1-3 weeks.

How It Works

You open a Self-Directed Gold IRA with a custodian that handles precious metals.

Then you contact your 401(k) plan administrator and request a rollover. The funds transfer from one custodian to the other—either electronically or by check made payable to the new custodian.

Once the money arrives, you work with a precious metals dealer like Brighton to choose IRS-approved gold or silver. Those products ship to an approved depository and get stored in your name.

That’s it. You now own physical metal inside a tax-advantaged retirement account.

Direct vs. Indirect Rollovers—Why It Matters

This is where a lot of people run into trouble.

A direct rollover sends funds straight from your 401(k) custodian to your Gold IRA custodian. You never touch the money. No taxes withheld. No deadline to worry about. No risk of accidentally triggering a taxable event.

An indirect rollover puts the cash in your hands first. Your 401(k) administrator withholds 20% for taxes—and you’ve got just 60 days to deposit the full amount into your new IRA. Miss that window? The whole thing becomes taxable income. And if you’re under 59½, you’ll likely owe a 10% early withdrawal penalty on top of that. Major brokerages like Fidelity outline this process in detail.

Here’s the bottom line: request a direct rollover. It’s simpler, safer, and what most custodians recommend.

The Partial Rollover: A Balanced Approach

A partial rollover lets you move some of your retirement savings into physical gold—while keeping the rest where it is.

It’s not all-or-nothing.

You’re adding another layer to your strategy without walking away from what you’ve already built.

Why Some People Choose This Path

There are a few situations where a partial rollover just makes sense.

You want to keep getting employer contributions. If you’re still working and your plan allows in-service rollovers (usually after age 59½), you can move part of your balance into a Gold IRA and still earn matching contributions on future deferrals.

You might need early access. Here’s something a lot of folks overlook—the Rule of 55. If you leave your job at age 55 or later, you can withdraw from that employer’s 401(k) without the 10% early withdrawal penalty. But that rule doesn’t apply to IRAs. If you’re between 55 and 59½ and think you might need those funds before the standard retirement age, keeping some money in your 401(k) preserves that option.

You’d rather start small. Not everyone wants to move their entire retirement in one transaction—and that’s okay. A partial rollover lets you put 10%, 20%, or whatever percentage feels right into physical metals. Then you can adjust over time based on how you feel about the experience.

You like having options. Different accounts come with different rules. Keeping assets in more than one place gives you flexibility down the road.

What a Partial Rollover Looks Like

Let’s say you’ve got $200,000 in your 401(k) and you want to move $50,000 into gold.

You’d contact your plan administrator and request a partial direct rollover. The $50,000 transfers to your new Gold IRA custodian—tax-free. The remaining $150,000 stays right where it is.

From there, you’d work with Brighton to pick IRS-approved metals—maybe some American Gold Eagles or a mix that includes silver. Those products ship to an approved depository and get stored in your name.

Your 401(k) keeps operating like it always has. You’ve just added a new layer to your retirement picture.

A Few Things to Keep in Mind

With a partial rollover, you’ll have two accounts to manage. Two sets of statements. Two fee structures.

For some people, that’s no big deal. For others, the extra complexity isn’t worth it.

Also—not every plan allows partial rollovers. Some require you to take everything or nothing. It’s worth checking with your plan administrator before you assume this option is on the table.

The Full Rollover: Consolidation and Control

A full rollover moves your entire 401(k) balance into a Gold IRA.

Everything goes. Nothing left behind.

This approach tends to appeal to people who’ve already left their employer, who are close to retirement, or who simply want all their retirement savings in one place.

Why Some People Prefer This Path

Simplicity. One account. One custodian. One set of fees. One statement to review. There’s something to be said for knowing exactly where everything is—especially as you get closer to the years when you’ll actually be drawing on these funds.

You’ve moved on from your old job. Once you’ve left the company, there’s no reason to keep your 401(k) sitting there. Your former employer has no obligation to offer you favorable terms, and your options may be limited.

You want full control. In a Self-Directed Gold IRA, you choose the metals. You choose the storage type—segregated or non-segregated. You choose the depository. That level of control simply isn’t available in most employer-sponsored plans.

You believe in tangible ownership. If your goal is long-term wealth preservation—not chasing short-term gains—a full rollover positions your entire retirement balance in something you can actually see and touch.

What a Full Rollover Looks Like

Same example: you’ve got $200,000 in your 401(k), and you want to roll over the whole thing.

You request a complete direct rollover from your plan administrator. The entire $200,000 transfers to your Gold IRA custodian.

Once the funds clear, you select your metals and have them shipped to an approved depository.

From that point forward, your retirement holdings are backed entirely by physical precious metals—held in your name.

A Few Things to Consider

You’ll give up the Rule of 55. This one’s worth repeating. If you’re between 55 and 59½, rolling your entire 401(k) into an IRA means you can’t take penalty-free early withdrawals under the Rule of 55 anymore. The earliest you can access IRA funds without penalty is generally 59½.

Storage fees apply. Physical metals have to be stored in an IRS-approved depository. Annual custodian and storage fees typically run $200-350—but they’re flat fees, regardless of account size. That means larger accounts often pay a smaller percentage overall.

Metal selection matters. A $200,000 account gives you real purchasing power. You’ll want to choose wisely—whether that’s U.S.-minted gold coins, a mix of gold and silver, or a combination that fits your goals. Our team can help you think through what makes sense.

Partial vs. Full Rollovers: A Side-by-Side Look

Here’s a quick snapshot of how the two options stack up.

| Factor | Partial Rollover | Full Rollover |

|---|---|---|

| Control Over Metals | Applies to the portion you move | Applies to your entire balance |

| Account Simplicity | Two accounts to track | One consolidated account |

| Rule of 55 Access | Preserved on the 401(k) portion | Lost once rolled to IRA |

| Future Employer Match | Still available on remaining 401(k) | Not applicable |

| Fee Structure | Two sets of fees | One set of fees |

| Best For | Phased approach, early access needs | Simplicity, maximum control |

Neither option is universally “right.” It depends on where you are in life.

Scenario A: Still Working, Age 52

You’re employed, you’re 52, and you like the idea of owning some physical gold—but you’re not ready to give up employer matching contributions.

Best fit: Partial rollover (if your plan allows in-service distributions). Move a portion into a Gold IRA while continuing to build your 401(k) balance.

Scenario B: Recently Retired, Age 58

You just retired at 58. Your 401(k) is sitting with your former employer, and you don’t expect to need the funds before 59½. You want everything in one place.

Best fit: Full rollover. You’re close to penalty-free access anyway, and consolidation makes your retirement picture a lot cleaner.

Scenario C: Left Your Job at 56, Might Need Early Access

You left your employer at 56. You want exposure to physical gold—but you’re not sure whether you’ll need some of those funds before 59½.

Best fit: Partial rollover. Move part into a Gold IRA for long-term protection. Keep enough in your 401(k) to access under the Rule of 55 if you need it.

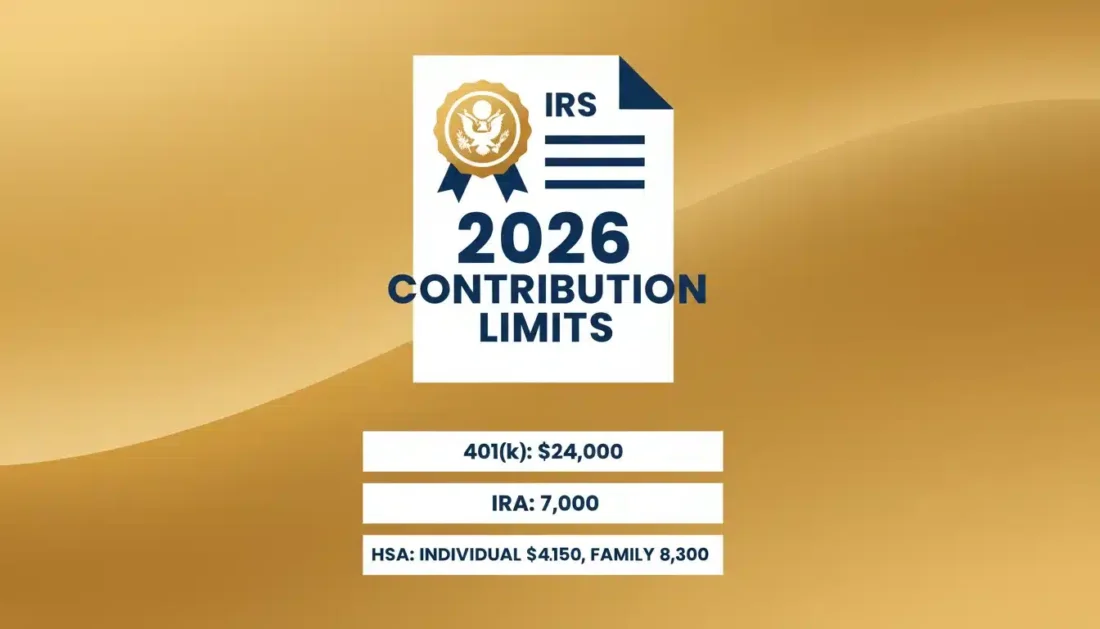

2026 IRS Rules That Apply

The IRS updated retirement account limits for 2026. Here’s what you need to know.

2026 Contribution Limits

| Account Type | Standard Limit | Age 50+ Catch-Up | Ages 60-63 Super Catch-Up |

|---|---|---|---|

| 401(k), 403(b), TSP | $24,500 | $32,500 | $35,750 |

| Traditional/Roth IRA | $7,500 | $8,600 | N/A |

| Combined 401(k) Total | $72,000 | $80,000 | $83,250 |

Here’s the key thing: rollover amounts don’t count toward these limits.

You could roll over $500,000 into a Gold IRA and still contribute another $7,500 (or $8,600 if you’re 50+) that same year. The rollover is separate.

Rollover Rules Worth Knowing

- 60-day rule: If you take an indirect rollover, you’ve got 60 days to deposit the funds. Miss the deadline and it becomes taxable income.

- One-per-year rule: The IRS allows only one indirect IRA-to-IRA rollover per 12-month period. This doesn’t apply to direct rollovers or 401(k)-to-IRA rollovers—those are unlimited.

- 20% withholding: Indirect rollovers from 401(k) plans trigger mandatory 20% federal tax withholding. If you want to roll over the full amount, you’ll need to come up with that 20% from somewhere else.

- No minimum percentage: The IRS doesn’t require you to move any specific amount. Roll over 5%, 50%, or 100%—it’s your call.

Tax Treatment

Direct rollovers from a traditional 401(k) to a traditional Gold IRA are tax-free. The funds keep their tax-deferred status.

Roth 401(k) to Roth Gold IRA? Also tax-free—and qualified withdrawals stay tax-free in retirement.

Rolling traditional 401(k) funds into a Roth Gold IRA triggers a taxable conversion. You’d owe income tax on the amount you convert in the year of the rollover.

Most people stick with matching account types to keep things simple.

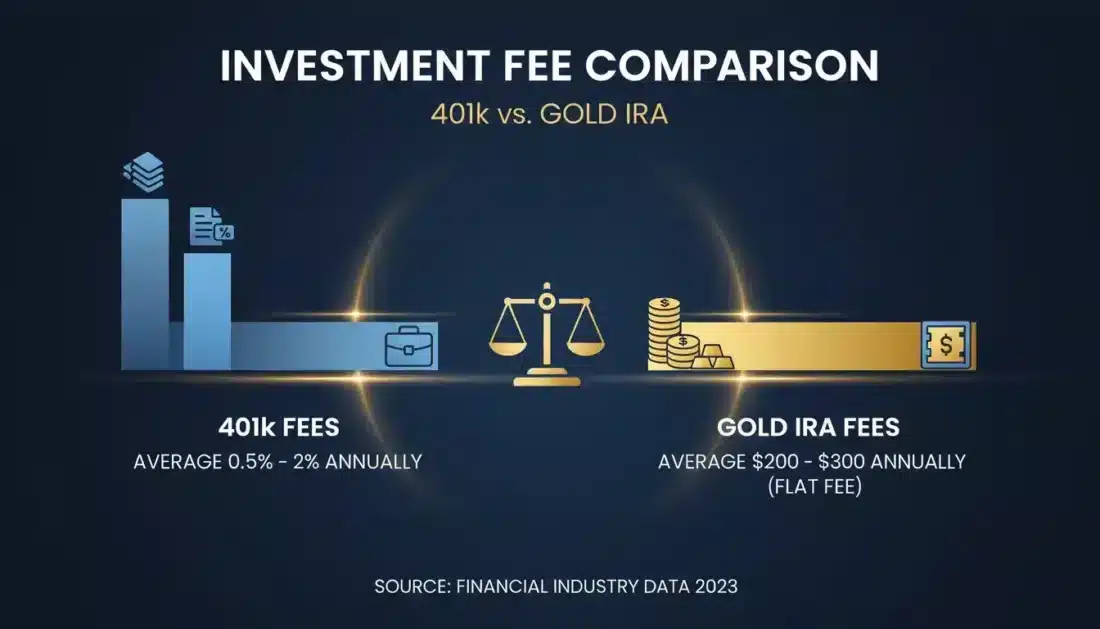

How Gold IRA Fees Compare to 401(k) Fees

Will a Gold IRA cost more than your current 401(k)?

Maybe. Maybe not. It depends on what you’re paying now—and most people have never really looked.

Typical Gold IRA Fees

Here’s what you can expect:

- Account setup: Usually $50-100 (one-time)

- Annual custodian fee: $75-150 per year

- Storage fee: $100-150 for non-segregated; $150-300 for segregated

- Wire transfer fee: $25-30 per transaction

All in, most Gold IRA owners pay $200-350 annually for custodian and storage combined.

401(k) Fees You Might Not See

Traditional 401(k) plans have fees too—they’re just buried in the fine print.

- Administrative fees: Can range from 0.5% to 2% of your balance per year

- Fund expense ratios: The mutual funds inside your 401(k) typically charge 0.5% to 1%+ annually

- Revenue sharing fees: Some plans include additional costs that quietly reduce your returns

On a $200,000 balance, a 1% annual fee equals $2,000 per year.

Compare that to the flat $250-350 annual fee on a Gold IRA—no matter how large your account grows.

A Quick Comparison

| Account Balance | Typical 401(k) Fees (1%) | Typical Gold IRA Fees |

|---|---|---|

| $50,000 | $500/year | $250/year |

| $100,000 | $1,000/year | $250/year |

| $200,000 | $2,000/year | $250/year |

| $500,000 | $5,000/year | $250/year |

The larger your balance, the more a flat-fee structure can work in your favor.

Why Physical Gold? Why Now?

What’s driving so many people to consider physical gold for their retirement in the first place?

It’s not complicated. It comes down to something you can feel but can’t always put into words—peace of mind.

What Gold Offers

Physical gold is tangible. You can hold it. You can see it. And when the time comes, you can pass it down to your children or grandchildren.

It’s not a promise printed on paper. It’s not tied to a company’s earnings report or a government’s spending decisions.

It’s metal that’s held value across centuries—through wars, economic crises, and currency collapses.

When you understand how a Gold IRA works, you realize it’s not about abandoning traditional retirement planning. It’s about adding something that doesn’t move in lockstep with everything else.

Central banks around the world have been buying gold at record levels over the past several years. They’re not doing it for fun—they’re doing it because even institutions that manage entire economies recognize the value of holding something real.

A Quick Note on Performance

Gold recently reached all-time highs above $5,000 per ounce. That’s not a prediction—it’s what’s happening in the market right now.

Does that mean gold will keep rising? Not necessarily.

Precious metals may appreciate, depreciate, or remain unchanged based on market conditions.

But it does mean serious institutions are taking physical gold seriously. And that’s worth thinking about as you consider your own strategy.

A Simple Framework for Making Your Decision

Let’s pull this together into something practical.

Step 1: Check Your Plan Rules

Call your 401(k) administrator and ask:

- Does the plan allow partial rollovers?

- Are in-service distributions permitted while you’re still employed?

- What’s the timeline for processing a rollover request?

- Are there any restrictions or fees?

This tells you what’s actually possible—not just what you’d prefer.

Step 2: Think About Your Age and Timeline

Your age affects your options more than most people realize.

Under 55: You’ll face a 10% penalty on early withdrawals from either a 401(k) or IRA until 59½ (with limited exceptions). The Rule of 55 isn’t available yet.

Ages 55-59½: If you’ve left your employer, the Rule of 55 lets you access your 401(k) penalty-free. But once you roll those funds into an IRA, that option goes away.

Age 59½+: You can access either account penalty-free. The Rule of 55 no longer matters.

Step 3: Consider How Much Gold Makes Sense

There’s no magic number here.

Some customers start with 10-15% of their retirement in physical metals. Others go with 25% or more. The question of how much gold to own for retirement depends on your goals and your comfort level.

A partial rollover lets you start smaller. A full rollover commits everything at once.

Step 4: Think About Storage

Gold IRAs require IRS-approved depository storage. You’ll choose between:

- Segregated storage: Your specific coins and bars are kept separate from other customers’ holdings. You’ll receive the exact same items back when you take distributions.

- Non-segregated (commingled) storage: Your metals are stored alongside similar items from other customers. You’ll receive the same type and quantity—but not necessarily the exact same pieces.

Both options are secure and IRS-compliant. Segregated storage typically costs $50-150 more per year.

Step 5: Choose Your Path

Based on everything you’ve considered:

- Partial rollover: Start with a portion now; adjust over time

- Full rollover: Consolidate everything into one Gold IRA

- Wait: Gather more information before deciding

There’s no deadline. This is your retirement. Take the time to get it right.

What Happens After You Roll Over?

Once your rollover completes and you’ve picked your metals, here’s what to expect.

Selecting Your Metals

You’ll work with Brighton to choose IRS-approved products. Popular options include:

- Gold American Eagles — The most recognized U.S.-minted gold coin

- Gold American Buffalos — 24-karat gold, 99.99% pure

- Silver American Eagles — The U.S. Mint’s flagship silver coin

- Gold and silver bars — Available in various weights from approved refiners

Not all gold qualifies. Collectible coins, foreign currency, and metals below purity requirements don’t meet IRS standards. Brighton makes sure every product we recommend is eligible.

And if you’re interested in adding silver to your Gold IRA, we can help you think through how that fits your overall strategy.

Secure Storage

Your metals ship directly to an approved depository—never to your home. That’s an IRS requirement, not a suggestion.

These facilities provide 24/7 security, full insurance coverage, regular audits, and detailed inventory records.

You’ll receive documentation confirming your holdings. And you can request distributions at any time.

Support at Every Stage of Ownership

A Gold IRA isn’t something you set up and forget about.

Have questions about adding to your account? Changing your storage preferences? Taking a distribution?

We’re here to help—before, during, and after. That’s what we mean by concierge service. It’s not just about the transaction. It’s about the relationship.

Frequently Asked Questions

Can I do a partial rollover to gold if I’m still employed?

It depends on your plan. Some 401(k) plans allow in-service rollovers once you reach age 59½. Others won’t let you touch the funds until you leave the company. Your plan administrator can tell you what’s allowed—and what conditions apply.

Are there penalties for moving only a portion of my 401(k) to gold?

No. The IRS doesn’t penalize partial rollovers as long as you execute them properly. There’s no minimum amount required. You can move whatever portion makes sense for your situation—and the funds stay tax-deferred. Just make sure you request a direct rollover so the money goes straight from one custodian to the other.

What are the advantages of a full 401(k) to Gold IRA rollover?

A full rollover puts everything in one place. One account. One set of statements. Complete control over which metals you own and how they’re stored. For people who’ve left their employer or want to simplify their retirement picture, it’s often the cleaner path forward.

How does the 2026 contribution limit change my rollover strategy?

Rollover amounts don’t count toward annual contribution limits—they’re separate transactions. So whether you move $50,000 or $500,000, you can still contribute up to $7,500 (or $8,600 if you’re 50+) to your Gold IRA the same year. The 2026 401(k) limit is $24,500 for employee deferrals.

What happens to my employer match if I do a partial rollover?

The rolled-over funds won’t receive any new matching contributions—those only apply to future deferrals into an active plan. If you’re still working and do a partial rollover, your ongoing 401(k) contributions can still earn matching. But the portion you moved is done receiving employer contributions.

How do I decide what percentage of my retirement to hold in physical gold?

There’s no magic number. It depends on your goals, your timeline, and how you feel about holding something tangible. Many of our customers start with 10-25% and adjust from there. A conversation with a precious metals specialist can help you think through what makes sense for your situation.

Will I lose access to my funds earlier if I do a full rollover?

If you’re between 55 and 59½, possibly yes. The Rule of 55 allows penalty-free 401(k) withdrawals if you leave your job at 55 or later—but it doesn’t apply to IRAs. Rolling everything into a Gold IRA means you’d generally wait until 59½ for penalty-free access. That’s worth considering if early retirement is on your radar.

How long does a 401(k) to Gold IRA rollover take?

Most direct rollovers wrap up in 1-3 weeks. It depends on how fast your current plan processes the paperwork and how quickly the receiving custodian clears the funds. Working with an experienced team can help keep things moving smoothly.

Conclusion

Choosing between a partial and full 401(k) rollover to gold isn’t as complicated as it might seem.

If you want flexibility, need to preserve Rule of 55 access, or prefer to ease into things—a partial rollover gives you room to start small and adjust.

If you want simplicity, maximum control, and everything in one place—a full rollover makes life easier.

Both approaches are tax-free when done right. Both give you ownership of real metal held in your name. And both can be completed in as little as 1-3 weeks.

The question isn’t whether a Gold IRA is right for everyone. It’s whether it’s right for you—and whether a partial or full rollover aligns with where you’re headed.

Remember: Precious metals may appreciate, depreciate, or remain unchanged based on market conditions. Brighton doesn’t provide financial, legal, or tax advice. Consult your CPA or tax professional for guidance specific to your situation.

Ready to Explore Your Options?

If you’re thinking “this all makes sense, but I don’t have time to figure it out on my own,” you’re not alone. Most customers we work with felt the same way before they realized how straightforward the process can be with the right guidance.

That’s why we offer a complimentary consultation to walk you through your options—including our No Fee Precious Metals IRA, which covers custodial fees for the lifetime of the account on qualified purchases.

We’ll show you exactly:

- How the No Fee IRA works and whether you qualify

- The difference between U.S.-minted coins and foreign alternatives

- What to expect from the purchasing and delivery process

- How to roll over or transfer existing retirement funds

- What ongoing support looks like after your purchase

Learn About the No Fee IRA—no obligation, just actionable insights you can use whether you work with us or not.

Your retirement. Your metals. Your decision.