Gold coins and gold bars both qualify for an IRA. But they’re not the same.

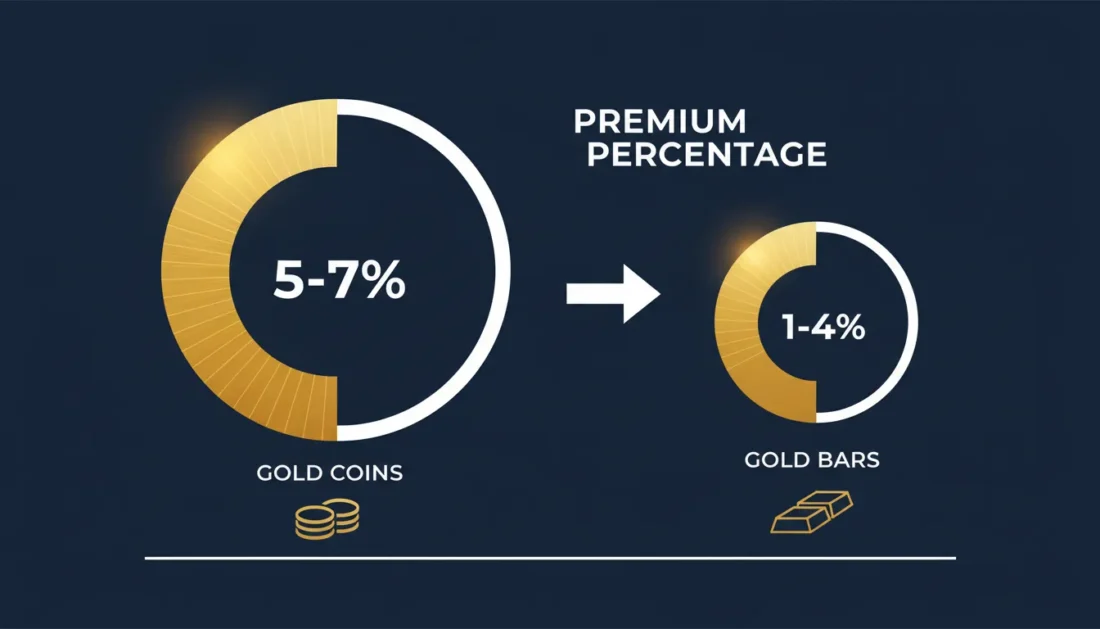

The main difference? Gold bars usually cost less—about 1-4% over the spot price. Sovereign coins like the American Gold Eagle run closer to 5-7% above spot. That gap adds up, especially on larger purchases.

But coins offer something bars don’t. They’re easier to recognize. They’re easier to sell. And when it comes time to take money out of your account, they give you more options.

For most people opening a self-directed gold IRA, it’s not really a question of picking one or the other. It’s about finding the right mix—one that fits your goals, your timeline, and how much flexibility you’ll want down the road.

Let’s walk through everything you need to know so you can make a decision that feels right.

The Basics: How Coins and Bars Are Different

Before comparing prices, it helps to understand what you’re actually looking at.

Gold coins and gold bars do the same thing at a basic level—they let you hold physical gold inside a tax-advantaged account. But they’re made differently. They’re priced differently. And they’re valued differently when you go to sell.

How Gold Coins Are Made

Sovereign gold coins come from government mints. The U.S. Mint makes the American Gold Eagle under rules set by the Gold Bullion Coin Act of 1985. Every detail—weight, purity, design—is written into law.

That matters for a couple of reasons.

Government-minted coins carry legal tender status. A 1 oz American Gold Eagle has a $50 face value stamped right on it. Of course, the real value is tied to the price of gold—which is a lot higher than $50 right now.

Making these coins takes work:

- Each design requires detailed engraving and precision tooling

- Blanks have to meet exact weight specs before they’re struck

- Quality control checks every coin against design standards

- Packaging and authentication add extra handling steps

All of that adds cost. And that cost shows up in the premium you pay.

How Gold Bars Are Made

Gold bars come in two main types—cast bars and minted bars.

Cast bars are simple. Molten gold gets poured into a mold, cooled, and stamped with basic marks—weight, purity, and the refiner’s hallmark. No fancy designs. No legal tender status. No complicated production.

Minted bars are a step up. They’re cut from sheets of refined gold and stamped with more detailed marks. Some come in sealed packaging that certifies what’s inside. But even minted bars don’t need the same level of precision that sovereign coins require.

The result? Lower production costs mean lower premiums for you.

Why This Matters for Your IRA

When you’re acquiring U.S.-minted gold coins or bars for a retirement account, you’re not buying for looks. You’re buying for value—both now and years from now.

Knowing how these products are made helps explain why coins cost more than bars of the same weight. It’s not about quality or purity. It’s about what goes into making them.

IRS Rules: What Actually Qualifies

Not all gold qualifies for an IRA. The IRS sets specific rules under Section 408(m)(3), and missing those requirements can create tax problems.

Here’s what you need to know.

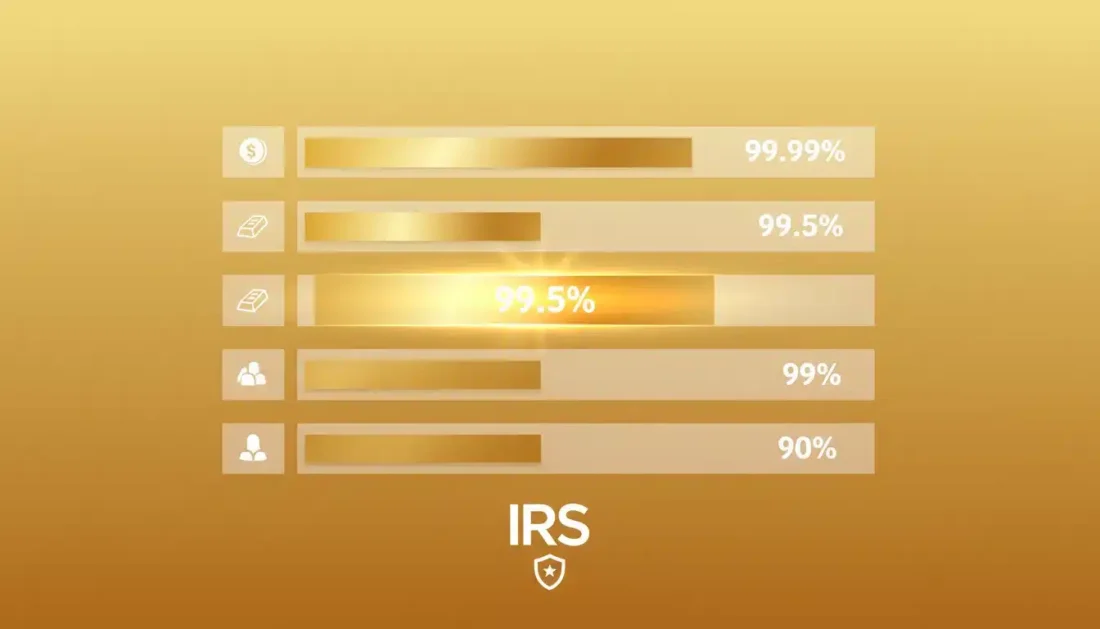

The 99.5% Purity Rule

For gold to be IRA-eligible, it has to be at least 99.5% pure (.995 fineness). This goes for bars, rounds, and most coins.

Here’s the interesting part. The American Gold Eagle doesn’t meet that standard. It’s made with 91.67% gold (22-karat). But Congress created a specific exception for Eagles, making them the only gold coin below 99.5% purity that qualifies for an IRA.

| Metal | Minimum Purity | Notes |

|---|---|---|

| Gold | 99.5% (.995) | American Gold Eagle exempt at 91.67% |

| Silver | 99.9% (.999) | American Silver Eagle meets standard |

| Platinum | 99.95% (.9995) | American Platinum Eagle eligible |

| Palladium | 99.95% (.9995) | Canadian Maple Leaf eligible |

Why the exception? The American Gold Eagle uses “crown gold”—the same 22-karat mix historically used in British sovereigns and South African Krugerrands. The copper and silver in the alloy make the coin harder and more durable. And it still contains exactly one troy ounce of pure gold.

Approved Coin Types

The IRS recognizes several types of coins for IRA use:

- American Gold Eagle — The only 22-karat coin with an IRA exception. Comes in 1 oz, 1/2 oz, 1/4 oz, and 1/10 oz sizes.

- American Gold Buffalo — 99.99% pure (24-karat). First made in 2006 as a higher-purity U.S. option.

- Canadian Gold Maple Leaf — 99.99% pure. Recognized and traded worldwide.

- Austrian Gold Philharmonic — 99.99% pure. Europe’s most-traded gold bullion coin.

- Australian Gold Kangaroo — 99.99% pure. Design changes each year.

When choosing IRS-approved gold coins, sovereign coins from recognized governments give you the best combination of liquidity and easy verification.

Approved Bar Standards

Gold bars face the same 99.5% purity minimum. But there’s another layer—the bar has to come from a refiner that’s been approved by recognized exchanges.

The London Bullion Market Association (LBMA) keeps the “Good Delivery” list. It’s the global standard for bar quality. As of early 2026, 66 gold refiners hold LBMA approval, including PAMP Suisse, Valcambi, Credit Suisse, and the Royal Canadian Mint.

COMEX and NYMEX also keep approved refiner lists. Bars meeting these standards are accepted around the world without question.

What makes a bar IRA-eligible:

- At least 99.5% pure (.995 fineness)

- Made by an LBMA, COMEX, or nationally approved refiner

- Clear hallmarks showing weight, purity, and refiner name

- Sealed assay packaging for smaller bars (not required, but preferred)

Generic rounds from private mints usually don’t qualify. If the refiner isn’t on an approved list, the product won’t work for an IRA—no matter how much gold is actually in it.

Premiums: What You’ll Pay Above Spot

This is where the numbers really start to matter. The difference in premiums between coins and bars can mean thousands of dollars on bigger purchases.

What Is a Premium?

The “spot price” you see online is the wholesale market price for large trades between institutions. It’s a starting point—not what you’ll actually pay.

When you buy physical gold, you pay a premium that covers:

- Refining and minting costs

- Dealer margin

- Shipping and insurance

- Supply and demand

That premium changes depending on what you’re buying, who you’re buying from, and when you’re buying.

What Premiums Look Like Right Now (2026)

Based on current market conditions:

| Product Type | Typical Premium Over Spot | Best For |

|---|---|---|

| 1 oz Gold Bar (LBMA) | 1-4% | Larger purchases, cost efficiency |

| 1 oz American Gold Eagle | 5-7% | Liquidity, recognition, flexibility |

| 1 oz Canadian Maple Leaf | 4-6% | High purity, global recognition |

| 1 oz American Gold Buffalo | 4-6% | U.S. minting, 24-karat purity |

| Fractional Gold Coins | 7-12% | Smaller purchases, divisibility |

On a $100,000 purchase, that 3-4% premium difference works out to $3,000-$4,000 in savings if you choose bars over coins.

But that savings comes with trade-offs.

Why Coins Cost More

Sovereign coins carry advantages that bars can’t match:

- Government guarantee — Weight and purity backed by national mints

- Legal tender status — Recognized as official currency

- Easy verification — Familiar designs reduce counterfeiting concerns

- Established resale market — Dealers worldwide buy them without hesitation

- Fractional sizes — 1/10 oz, 1/4 oz, and 1/2 oz options for flexibility

The benefits of physical gold ownership go beyond the metal itself. When liquidity matters—and in retirement, it often does—recognizable sovereign coins offer advantages that can justify the higher cost.

When Bars Make More Sense

Gold bars become more attractive as purchase size goes up:

- $25,000+ purchases — The 3-4% premium savings starts to add up

- Long-term holding — If you’re not planning to sell pieces along the way, liquidity matters less

- Efficient storage — Bars stack neatly and take less space per ounce

- Building larger positions — Lower cost means more gold for the same dollars

For people focused on getting as much gold as possible for their money, bars deliver better value. The trade-off is less flexibility when it’s time to sell.

Liquidity: Which Sells Easier When You Need It

Premiums matter when you buy. Liquidity matters when you sell.

Recognition Makes a Difference

Walk into any reputable precious metals dealer in the world with an American Gold Eagle, and you’ll have a buyer. The coin is recognized everywhere. It’s easy to verify. No extra steps needed.

Gold bars—especially bigger ones—often need more checking. Dealers may want to see original packaging, assay certificates, or even run their own tests before making an offer.

This doesn’t mean bars are hard to sell. LBMA bars from well-known refiners trade actively. But there’s usually a bit more back-and-forth, and the spread between buy and sell prices can be wider—especially for bars without original packaging.

Selling Part of Your Holdings

Here’s something a lot of people don’t think about ahead of time: what happens when you need to sell just part of what you own?

If your IRA holds ten 1-oz American Gold Eagles, you can sell one, three, or seven—whatever you need. Each coin is a separate unit.

If your IRA holds one 10-oz gold bar, you’re selling the whole thing or nothing. There’s no in-between.

For retirement accounts where you might take money out over time, having that flexibility really matters. Fractional options—whether 1/2 oz bars or 1/10 oz coins—give you choices that larger units can’t.

What Dealers Pay When You Sell

When you sell gold, dealers usually pay below the spot price. The spread depends on what you’re selling:

- Sovereign coins — Usually 1-3% below spot for common dates

- LBMA bars (with assay) — Usually 1-2% below spot

- LBMA bars (no assay) — May see wider spreads or need testing

- Generic rounds — Often face bigger discounts

The same recognition that makes coins cost more when you buy usually helps you get better prices when you sell. You pay the premium twice—but the second time, it works in your favor.

Storage: How Your Gold Gets Held

IRS rules don’t allow you to keep IRA gold at home. Your metals have to be held by an approved custodian in an IRS-approved depository.

How It Works

When you set up a precious metals IRA, you’ll work with two different companies:

- Custodian — Handles account paperwork, reporting, and IRS compliance

- Depository — Provides physical storage, security, and insurance

Popular depositories include Delaware Depository, Brink’s Global Services, and International Depository Services. Each offers insured, audited storage with around-the-clock security.

Segregated vs. Non-Segregated Storage

You’ll usually choose between two storage options:

- Segregated storage — Your specific metals are kept separate from other customers’ holdings. When you sell or take a distribution, you get the exact items you purchased.

- Non-segregated (commingled) storage — Your metals are pooled with others’ holdings of the same type. You own a certain amount, but not specific bars or coins.

Segregated storage costs more—typically $150-$300 per year versus $100-$250 for commingled. For people who want their exact coins or bars back when they sell, the extra cost is worth it.

For more details, see our guide on segregated vs. non-segregated gold storage.

Storage Differences: Coins vs. Bars

From a pure storage standpoint, bars have some advantages:

| Storage Factor | Gold Coins | Gold Bars |

|---|---|---|

| Stackability | Need tubes or cases | Uniform shape, stack easily |

| Space per ounce | More packaging | Compact |

| Handling | Track each coin | Fewer items |

| Documentation | More pieces to list | Simpler records |

In practice, this affects the depository more than it affects your costs. Storage fees are usually based on value, not how much space your gold takes up. But for very large positions, bars can make inventory simpler.

What Fees to Expect

Gold IRA fees vary by custodian, but here’s a general idea:

- Setup fee — $50-$150 (one-time)

- Annual administration — $75-$300 per year

- Storage/insurance — $100-$300 per year (depends on value and storage type)

- Transaction fees — $0-$50 per buy/sell

All together, most people pay $200-$600 per year to maintain a gold IRA. These fixed costs take up a smaller share of larger accounts—another reason to think about consolidating purchases rather than making lots of small ones.

Building Your Position: Putting It Together

Now that you understand the differences, how do you actually build a position? That depends on your account size, your timeline, and how you plan to take money out.

Account Size Matters

Here’s a framework many people find helpful:

- Under $25,000 — Focus on coins. The premium difference is smaller in actual dollars, and flexibility matters more at this level.

- $25,000-$50,000 — Consider a 50/50 split. Coins for flexibility, bars for cost savings.

- $50,000-$100,000 — Weight toward bars (60-70%) while keeping some coins for partial sales down the road.

- $100,000+ — Bars make sense for most of your holdings. Keep 20-30% in smaller denominations for distribution flexibility.

These aren’t hard rules. Your specific situation—timeline, distribution plans, what you want to pass on—should guide your final mix.

The Fractional Approach

Smaller denominations deserve special attention for retirement accounts.

Yes, premiums are higher on 1/4 oz and 1/10 oz coins. But when you’re taking Required Minimum Distributions or partial withdrawals, smaller pieces let you sell exactly what you need—nothing extra.

Think about it this way: You need a $5,000 distribution. At current prices, that’s roughly 1.2 oz of gold. If you only have 1 oz coins, you’re selling two full ounces and dealing with the difference—or taking more out than you planned.

With fractional sizes, you can get much closer to what you actually need.

Adding Silver to the Mix

A lot of people also ask about adding silver to a gold IRA. The same coins-vs-bars thinking applies:

- Silver Eagles cost more but are easy to recognize and sell

- Silver bars give you more ounces for the same money

- A mix of both balances cost and flexibility

The gold-to-silver ratio changes over time. Some people use that ratio as a signal—shifting between metals as relative values move.

What Central Banks Are Doing

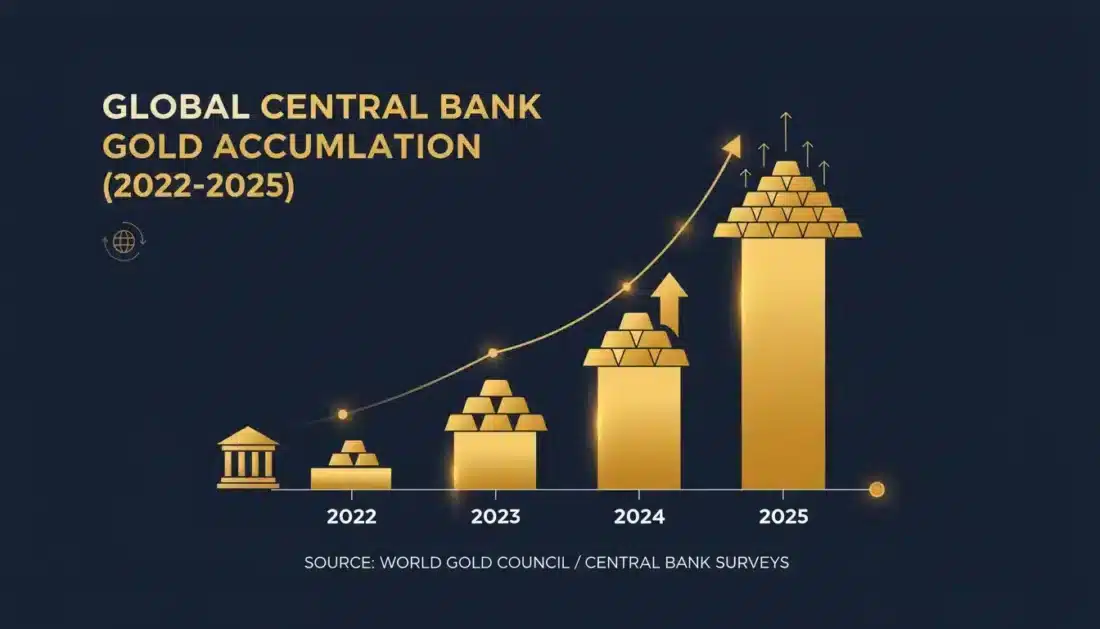

If you’re wondering what large institutions prefer—coins or bars—the answer is clear. Bars dominate central bank purchases.

According to the World Gold Council, central banks have added over 1,000 tonnes of gold in each of the last three years. That’s more than double the 400-500 tonne yearly average from the decade before. Through November 2025, purchases totaled 297 tonnes.

Why This Matters for You

Central banks aren’t buying American Gold Eagles. They’re buying Good Delivery bars—400 oz LBMA bars that move easily between institutional vaults.

But their reasons for buying gold line up closely with what many retirement-focused people are looking for:

- Moving away from dollar-based holdings

- Protection against currency swings

- Assets that hold value regardless of any single economy

The World Gold Council’s 2025 survey found that 95% of central bank respondents expected gold reserves to keep growing in the year ahead. Poland, Brazil, Kazakhstan, and Uzbekistan have been among the most active buyers.

This steady institutional demand supports gold prices—whether you hold coins or bars.

Frequently Asked Questions

Are gold bars cheaper than gold coins for an IRA?

Yes. Gold bars usually carry premiums of 1-4% over spot price, while sovereign coins like the American Gold Eagle run 5-7% above spot. On larger purchases, that difference can add up to thousands of dollars in savings. But bars give up some liquidity and flexibility compared to coins.

Which gold coins are IRS-approved for my self-directed IRA?

The IRS approves several sovereign-minted coins that meet purity rules: American Gold Eagle (allowed despite its 22-karat makeup), American Gold Buffalo (99.99% pure), Canadian Gold Maple Leaf (99.99% pure), Austrian Gold Philharmonic (99.99% pure), and Australian Gold Kangaroo (99.99% pure). Generic rounds from private mints usually don’t qualify.

Do gold bars have better resale value than coins?

Not necessarily. Sovereign coins often get better buyback prices relative to spot because they’re instantly recognizable and easy to verify. Gold bars—especially those without original packaging—may face wider spreads or need extra testing. The higher premium you pay for coins when buying often means better prices when selling.

Can I have both gold bars and gold coins in the same IRA account?

Absolutely. Many people hold a mix—using bars for cost-efficient larger purchases and coins for flexibility and partial sales. There’s no IRS rule saying you can only hold one type, and having both can balance the trade-offs.

What is the minimum purity requirement for IRA gold?

Gold has to be at least 99.5% pure (.995 fineness), with one exception: the American Gold Eagle is allowed at 91.67% purity (22-karat) because of a specific Congressional exemption. Silver requires 99.9% purity. Platinum and palladium require 99.95%.

How do premiums differ between American Gold Eagles and gold bars?

American Gold Eagles usually trade at 5-7% over spot price. One-ounce gold bars from LBMA-approved refiners run 1-4% over spot. The difference reflects production complexity, government backing, and how easy they are to resell. On a $50,000 purchase, choosing bars could save $1,500-$3,000 in premiums.

What happens if I store IRA gold at home?

The IRS doesn’t allow home storage for IRA metals. If you take physical possession, it counts as a distribution—meaning income tax and possibly a 10% early withdrawal penalty if you’re under 59½. All IRA gold has to be held by an approved custodian at an IRS-approved depository.

How do storage fees compare between coins and bars?

Storage fees are usually based on account value, not the form of your holdings. Whether you hold coins or bars, expect to pay $100-$300 per year for segregated storage or $100-$250 for non-segregated storage. What type of gold you have doesn’t change these costs much.

Making Your Decision

There’s no single “right” answer when choosing between gold coins and gold bars. The best choice depends on your situation.

Coins make sense if:

- Liquidity and flexibility matter most to you

- You plan to take money out in pieces over time

- Easy recognition and verification are priorities

- Your account is under $50,000

Bars make sense if:

- Getting as much gold as possible for your dollars is the main goal

- You’re holding long-term without frequent sales

- Your account is over $50,000

- Storage efficiency matters for a larger position

A mix makes sense if:

- You want both cost efficiency and flexibility

- You’ll be taking distributions over an extended period

- You prefer spreading out across different formats

Most importantly—don’t let the perfect be the enemy of the good. Both coins and bars accomplish the core goal: holding physical gold inside a tax-advantaged structure that helps protect your purchasing power over time.

Ready to Talk Through Your Options?

If you’re thinking “this makes sense, but I’d like to talk through my own situation,” you’re not alone. Most people we work with felt the same way before they realized how simple the process can be with the right support.

That’s why we offer a complimentary consultation to walk you through your options—including our No Fee Precious Metals IRA, which covers custodial fees for the lifetime of the account on qualified purchases.

We’ll show you exactly:

- How the No Fee IRA works and whether you qualify

- The difference between U.S.-minted coins and foreign options

- What to expect from the purchasing and delivery process

- How to roll over or transfer existing retirement funds

- What ongoing support looks like after your purchase

Learn About the No Fee IRA — no obligation, just clear information you can use whether you work with us or not.

The right gold for your IRA depends on your goals, your timeline, and how much flexibility you need. We’re here to help you figure that out—whenever you’re ready.