If you’ve been researching gold coins for your retirement account, you’ve probably noticed one name keeps coming up: the American Gold Eagle.

There’s a reason for that.

The Gold Eagle isn’t just another bullion coin. It’s the only 22-karat gold coin that qualifies for a precious metals IRA—thanks to a specific exception Congress wrote into federal law. Every other gold coin and bar has to meet a stricter 99.5% purity standard. The Gold Eagle doesn’t.

That legal distinction matters. But it’s only part of the story.

What makes the Gold Eagle the go-to choice for so many retirement-focused customers? It comes down to a combination of factors: U.S. government backing, a durable alloy that holds up over decades, instant recognition at any coin dealer in the country, and the peace of mind that comes from owning something tangible with a 40-year track record.

If you’re weighing your options—wondering whether the Gold Eagle is right for your situation—this guide will walk you through everything you need to know.

The Legal Foundation: Why Gold Eagles Get Special Treatment

Before 1986, Americans couldn’t easily acquire newly minted U.S. gold coins.

The government had been out of the gold coin business for over 50 years. If you wanted gold, your options were limited to foreign coins, private mint products, or pre-1933 collectibles.

That changed when President Ronald Reagan signed the Gold Bullion Coin Act of 1985.

This legislation authorized the U.S. Treasury to mint gold bullion coins for the first time since the 1930s. It specified that all gold must come from “newly mined domestic sources.” And it established four denominations: the $50 one-ounce, $25 half-ounce, $10 quarter-ounce, and $5 tenth-ounce coins.

The first American Gold Eagles rolled off the presses at the West Point Mint in 1986. Within months, they became the world’s best-selling gold bullion coin.

The IRS Exception That Changes Everything

So why does any of this matter for your retirement account?

Internal Revenue Code Section 408(m) generally prohibits IRAs from holding “collectibles.” That category includes most coins, art, antiques, gems, and precious metals.

If your IRA acquires a collectible, the IRS treats it as an immediate taxable distribution. Not ideal.

But Congress carved out a narrow exception.

Section 408(m)(3)(A) specifically names American Eagle coins—gold, silver, and platinum—as exempt from the collectibles rule. They’re written directly into the statute.

What does that mean in practice? Gold Eagles don’t have to meet the standard 99.5% purity requirement that applies to other precious metals. While bars and foreign coins must hit that threshold to qualify for an IRA, American Gold Eagles get a pass at just 91.67% purity.

Why the special treatment? Congress wanted to support the American Eagle program and encourage domestic gold ownership.

Why This Matters for Your Retirement

The practical impact is straightforward.

If you’re rolling over retirement funds to gold, American Gold Eagles are automatically on the approved list. No questions asked.

Your IRA custodian doesn’t need to verify purity or authenticate the coins through a third party. The U.S. Mint’s guarantee is sufficient.

Compare that to foreign coins or private mint products. These require verification that they meet the 99.5% threshold. Some custodians charge extra fees for this authentication process. Some won’t bother with certain products at all.

Gold Eagles skip that friction entirely.

You get clarity and control from day one—knowing exactly what you own and that it meets every IRS requirement without additional hoops.

The 22-Karat Advantage: Durability Meets Purity

Many first-time precious metals purchasers assume that higher purity always means better quality.

It doesn’t. And understanding why can save you from a common misconception.

The American Gold Eagle is struck in 22-karat gold—an alloy of 91.67% pure gold, 3% silver, and 5.33% copper. This composition dates back centuries to what’s called “crown gold,” the same standard used by the British Empire for its sovereign coins.

So what does that alloy actually do for you?

Why Pure Gold Isn’t Always Ideal

24-karat gold is soft. Very soft.

Pure gold rates just 2.5 on the Mohs hardness scale—barely harder than a fingernail. It scratches easily, dents under pressure, and can deform with handling.

That’s fine for gold bars sitting untouched in a vault. But it’s a problem for coins that might change hands multiple times over decades.

The American Gold Buffalo, for example, is struck in .9999 fine gold (24-karat). It’s a beautiful coin. But it’s also notably more susceptible to surface marks than the Gold Eagle.

The Gold Eagle’s alloy adds strength without reducing gold content.

You still get exactly one full troy ounce of pure gold in each coin. The coin simply weighs a bit more—33.93 grams total—because of the silver and copper that make it harder.

The Practical Benefits Over Time

Think about what happens over a 20 or 30-year holding period in a retirement account.

Your coins will be handled during transfers between depositories. They’ll be inventoried, audited, and eventually distributed. Each touchpoint introduces the possibility of minor damage.

A coin that resists scratching maintains its condition better over time.

Condition affects resale value—especially if you ever decide to sell through channels that consider numismatic premiums.

The Gold Eagle’s durability also explains its popularity in the secondary market. Dealers know these coins hold up well. They’re confident paying strong buyback prices because the coins they receive are typically in excellent condition despite years of storage.

| Coin | Purity | Composition | Hardness | IRA Eligible |

|---|---|---|---|---|

| American Gold Eagle | 91.67% (22K) | Gold, silver, copper alloy | Higher (more durable) | Yes (statutory exception) |

| American Gold Buffalo | 99.99% (24K) | Pure gold | Lower (softer) | Yes (meets purity standard) |

| Canadian Gold Maple Leaf | 99.99% (24K) | Pure gold | Lower (softer) | Yes (meets purity standard) |

| South African Krugerrand | 91.67% (22K) | Gold, copper alloy | Higher (more durable) | No (not named in statute) |

Notice something in that table?

The Krugerrand shares the same 22-karat composition as the Gold Eagle—but it’s not IRA-eligible. Congress didn’t name it in the exception. Only American Eagles get that treatment.

Liquidity: The Quiet Advantage

When you acquire physical gold, you’re making a decision that could span decades.

At some point, you may need to sell—for a distribution, to rebalance, or to access funds. How easily can you do that? And what will you actually receive when the time comes?

These questions matter more than most people realize when choosing which coins to hold.

Universal Recognition

Walk into any reputable coin dealer in America with a one-ounce Gold Eagle.

They’ll know exactly what it is. No authentication required. No waiting for a grading service to verify. No suspicious phone calls to confirm you’re not holding a counterfeit.

The Gold Eagle’s design—Augustus Saint-Gaudens’ Lady Liberty on the front, the eagle on the reverse—is instantly recognizable. It’s been struck with the same specifications since 1986.

Dealers trust it because the U.S. Mint guarantees the weight, content, and purity.

Compare that to less common coins. A Chinese Gold Panda might be perfectly legitimate, but a dealer unfamiliar with the series may want to verify it before paying full value. That takes time. It might cost you money in testing fees.

Gold Eagles don’t have that friction. You walk in, you sell, you leave with your funds.

Strong Secondary Market Demand

Liquidity isn’t just about recognition—it’s about demand. Are there ready buyers when you’re ready to sell?

According to data from the World Gold Council, central banks purchased over 1,045 metric tons of gold in 2024 alone. That’s the third consecutive year above 1,000 tons—far exceeding the 473-ton annual average from 2010–2021.

Global demand for physical gold remains robust.

Within that market, American Gold Eagles command consistent interest from both individual purchasers and institutional buyers. Most major dealers offer active buyback programs specifically for Gold Eagles.

They maintain inventory because they know customers want them.

When you’re ready to sell, you’re entering a market with ready buyers—not searching for someone willing to take a less common product off your hands.

What Dealers Actually Pay

Gold Eagles typically sell at or slightly above the gold spot price plus a small premium. When you sell back to a dealer, you’ll generally receive spot price plus a portion of that premium.

The spread—the difference between what you pay and what you receive when selling—tends to be tighter on Gold Eagles than on less liquid products.

Tighter spreads mean more of your gold’s value stays in your pocket when you exit.

| Product Type | Typical Buy Premium Over Spot | Typical Sell Premium Over Spot | Spread |

|---|---|---|---|

| American Gold Eagle (1 oz) | 3-5% | 0-2% | 2-4% |

| American Gold Buffalo (1 oz) | 4-6% | 0-2% | 3-5% |

| Generic Gold Bar (1 oz) | 2-4% | -1% to 1% | 2-4% |

| Foreign Government Coin | 4-7% | -1% to 2% | 3-7% |

These spreads vary based on market conditions, dealer policies, and current demand. But the pattern holds: Gold Eagles consistently offer competitive buy/sell spreads because of their deep market acceptance.

The Design: A Century of American Craftsmanship

You might be wondering—does the design really matter for a bullion coin?

For many customers, it does. And the Gold Eagle’s design carries a story worth knowing.

The obverse features Augustus Saint-Gaudens’ depiction of Lady Liberty—widely considered one of the most beautiful coin designs ever created. It was originally commissioned by President Theodore Roosevelt in 1905 for the $20 “Double Eagle” gold coin.

Roosevelt believed American coinage should reflect the nation’s growing prominence on the world stage. He recruited Saint-Gaudens, already America’s most famous sculptor, to create something worthy of that ambition.

Lady Liberty: From 1907 to Today

Saint-Gaudens designed a full-length figure of Liberty striding forward with confidence.

She holds a torch in her right hand—symbolizing enlightenment—and an olive branch in her left, representing peace. The U.S. Capitol building appears in the distance as the sun rises behind her.

It’s a design that captured the optimism of early 20th-century America.

And it resonated so deeply that Congress chose to revive it for the modern Gold Eagle program in 1986.

The coin you hold today features essentially the same Lady Liberty that Saint-Gaudens created over a century ago. That continuity connects you to a tradition of American craftsmanship that spans generations.

For customers focused on legacy—on holding something meaningful to pass down—that history adds a dimension beyond the metal itself. You can explore more about the coin’s features and specifications in our guide to the Gold American Eagle.

The Reverse Design

The original Gold Eagle reverse (1986–2021) depicted a family of eagles—a male carrying an olive branch flying above a nest containing a female and hatchlings. This design, created by sculptor Miley Busiek, represented family, protection, and continuity.

In 2021, the U.S. Mint introduced a refreshed reverse design by Jennie Norris.

It features a close-up portrait of an eagle’s head, capturing the bird’s intensity and strength. The update also included enhanced security features to combat counterfeiting.

Both versions are IRA-eligible. Some customers prefer the classic “family of eagles” design, while others appreciate the modern aesthetic of the newer version. From a bullion standpoint, both contain identical gold content.

How Gold Eagles Compare to Other IRA Options

When you’re comparing gold IRAs versus direct purchases, the American Gold Eagle isn’t your only option.

But understanding how it stacks up against alternatives can clarify why so many customers default to it.

American Gold Eagle vs. American Gold Buffalo

The Gold Buffalo is the U.S. Mint’s 24-karat (.9999 fine) alternative to the Gold Eagle. It was introduced in 2006 and features James Earle Fraser’s classic Buffalo Nickel design.

Which one makes more sense for your situation?

| Feature | Gold Eagle | Gold Buffalo |

|---|---|---|

| Purity | 91.67% (22K) | 99.99% (24K) |

| Gold Content | 1 troy oz pure gold | 1 troy oz pure gold |

| Total Weight | 33.93 grams | 31.10 grams |

| Durability | Higher (harder alloy) | Lower (pure gold is soft) |

| Premium | Generally lower | Generally higher |

| IRA Basis | Statutory exception | Meets purity requirement |

Both coins contain exactly one troy ounce of pure gold. The difference is structural—the Gold Eagle includes an alloy for durability, while the Gold Buffalo is pure.

For customers focused purely on acquiring gold at the lowest cost per ounce, the Gold Eagle often wins. Its premiums tend to run slightly lower than the Buffalo, and its secondary market liquidity is typically stronger.

American Gold Eagle vs. Canadian Gold Maple Leaf

The Canadian Maple Leaf is arguably the Gold Eagle’s closest international competitor. It’s also .9999 fine gold and enjoys global recognition.

So what’s the difference?

- Issuing authority: The Maple Leaf is minted by the Royal Canadian Mint. The Gold Eagle is minted by the U.S. Mint. For American customers, U.S. government backing may carry more weight.

- Durability: The Maple Leaf’s pure gold composition makes it more susceptible to scratching. The Royal Canadian Mint has added security features and micro-laser engraving to recent issues, but the softness remains.

- Liquidity in the U.S.: While the Maple Leaf is widely recognized, the Gold Eagle enjoys hometown advantage. American dealers typically offer tighter spreads on American-minted products.

- Legal status: The Gold Eagle’s statutory IRA exception provides a cleaner path to eligibility. The Maple Leaf qualifies by meeting the purity standard, but it doesn’t have the same explicit Congressional blessing.

For customers who want exposure to 24-karat gold and don’t mind a slightly higher premium, the Maple Leaf is a solid choice.

But for those prioritizing domestic sourcing, durability, and liquidity, the Gold Eagle remains the standard.

Understanding IRA Storage Requirements

Here’s something that surprises many first-time precious metals IRA customers: you can’t store your Gold Eagles at home.

The IRS requires that IRA-held precious metals be stored by an approved custodian at an IRS-approved depository. This isn’t optional. It’s a strict requirement that applies to all precious metals IRAs, regardless of which coins or bars you choose.

Why Home Storage Doesn’t Work

The IRS classifies personal possession of IRA-held metals as a taxable distribution.

If you take your Gold Eagles home—even “for safekeeping”—you’ve triggered a distribution event. You’ll owe income tax on the fair market value, plus a 10% early withdrawal penalty if you’re under 59½.

The McNulty v. Commissioner case (2021) reaffirmed this principle. The court found that an IRA owner who stored American Eagle coins at home had received a constructive distribution, even though she never sold the coins or spent the proceeds.

The lesson? Don’t try to shortcut the storage requirement.

What Approved Storage Looks Like

When you purchase Gold Eagles through an IRA—after evaluating the advantages and disadvantages—your custodian arranges for storage at an IRS-approved depository.

These facilities typically offer:

- Segregated storage: Your coins are held separately from other customers’ metals, not commingled in a common vault.

- Full insurance coverage: Your holdings are insured against theft, damage, and natural disasters.

- Regular audits: Depositories undergo independent audits to verify inventory.

- Access for distributions: When you’re ready to take a distribution—either in cash or in-kind—the depository coordinates with your custodian to execute the transaction.

Storage fees vary by depository and account size. Expect to pay somewhere between $100 and $300 annually for typical holdings.

Some dealers and custodians waive storage fees for qualified purchases—Brighton, for example, offers a No Fee Precious Metals IRA that covers custodial fees for the lifetime of the account on qualified transactions.

The Physical Delivery Option

What happens when you reach retirement age and want your actual coins?

You have two choices:

- Sell and distribute cash: Your custodian liquidates your Gold Eagles at market value and distributes the proceeds. You’ll owe income tax on the distribution.

- In-kind distribution: Your custodian arranges for the physical coins to be shipped to you. You still owe income tax on the fair market value at the time of distribution, but you take possession of the actual metals.

Many customers prefer in-kind distributions.

After years of accumulating Gold Eagles in a tax-advantaged account, they want to hold what they’ve built—not just receive a check. There’s peace of mind in knowing those coins are now yours to keep, store, or pass down as you see fit.

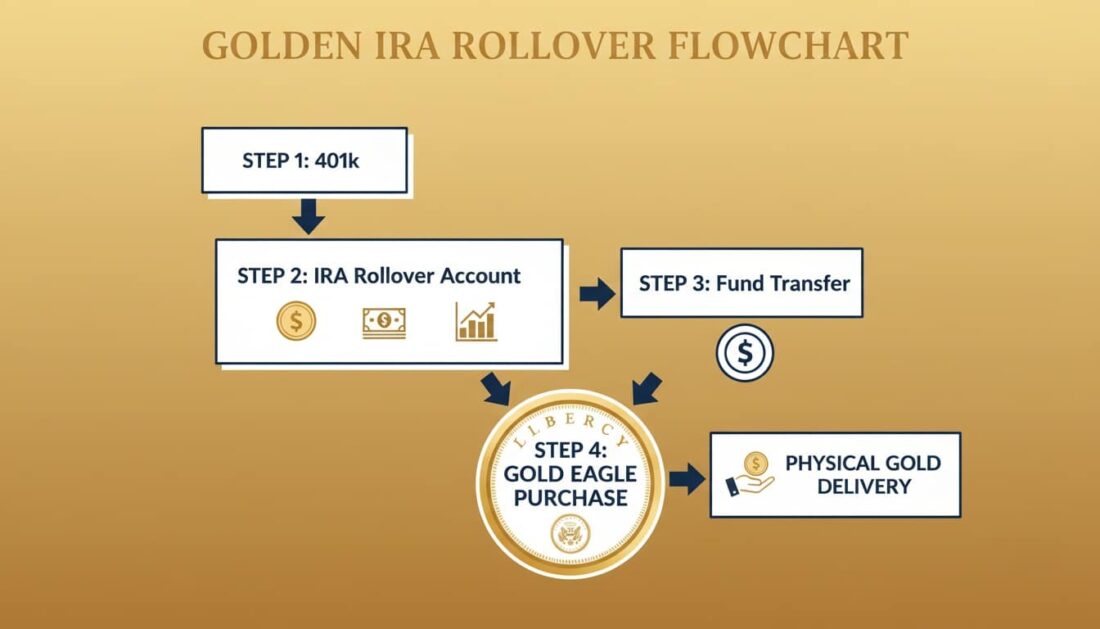

The Process: Adding Gold Eagles to Your IRA

If you’re thinking “this all makes sense, but what does the actual process look like?”—you’re asking the right question.

Adding American Gold Eagles to your retirement typically involves three steps: opening a self-directed IRA, funding it, and purchasing your metals.

Most customers complete the entire process within one to three weeks.

Step 1: Open a Self-Directed IRA

Traditional IRAs at major brokerages typically don’t allow precious metals holdings.

You’ll need a self-directed IRA with a custodian that specializes in alternative assets.

Brighton works with established custodians who handle precious metals IRAs daily. The account opening process involves standard paperwork—identification, beneficiary designations, and funding instructions.

If you already have a self-directed IRA with precious metals capability, you can skip this step.

Step 2: Fund Your Account

You have several options for getting money into your new IRA:

- Direct rollover from a 401(k) or similar plan: Your former employer’s plan administrator sends funds directly to your new custodian. No taxes withheld. This is the most common approach for customers consolidating retirement accounts.

- Trustee-to-trustee transfer from an existing IRA: Your current IRA custodian sends funds directly to your new custodian. Also tax-free and straightforward.

- 60-day rollover: You receive a distribution from your existing account and have 60 days to deposit it into your new IRA. This approach carries risk—if you miss the deadline, the distribution becomes taxable.

- Annual contribution: You can contribute up to $7,000 annually ($8,000 if you’re over 50) to a traditional or Roth IRA, subject to income limits.

For detailed guidance on the rollover process, see our article on rolling over a 401(k) to a Gold IRA without penalty.

Step 3: Purchase Your Gold Eagles

Once funds arrive at your custodian, you’re ready to buy.

You’ll work with a precious metals dealer—like Brighton—to select your coins. We’ll confirm pricing, execute the transaction, and coordinate shipping to your designated depository.

The coins are then held in your IRA account, registered in your custodian’s name for IRS purposes but segregated as your property.

That’s it. Your Gold Eagles are now part of your retirement holdings.

Why Central Banks Are Buying Gold—And What It Signals

You’re not the only one looking at gold for long-term stability.

Central banks around the world have been accumulating gold at a pace not seen in decades. And if you’re wondering whether physical gold still makes sense for long-term stability, their actions offer a useful signal.

According to World Gold Council data, central banks purchased over 1,045 metric tons of gold in 2024 alone.

That’s the third consecutive year above 1,000 tons—more than double the 400–500 ton annual average from the previous decade.

What’s Driving the Trend

Central banks don’t make decisions casually. Their gold purchases reflect institutional concerns about:

- Currency stability: With major economies carrying unprecedented debt levels, central banks are diversifying away from dollar-denominated reserves.

- Geopolitical uncertainty: Sanctions, trade conflicts, and political instability have made physical gold—which exists outside any government’s control—more attractive.

- Inflation protection: After years of aggressive monetary expansion, central banks recognize gold’s historical role as a store of value during inflationary periods.

The National Bank of Poland was 2024’s largest buyer, adding 90 tons to its reserves. Poland now holds gold as 17% of its total international reserves—approaching its stated target of 20%.

Other notable buyers included the Czech Republic, India, Turkey, and China. The buying trend spans emerging and developed economies alike.

Why This Matters Now

What does central bank activity mean for individual purchasers like you?

It suggests that sophisticated reserve managers—people whose job is to protect national wealth—see gold as a strategic asset worth holding. Not just a speculative trade, but a long-term position.

Their sustained buying creates demand that supports prices. It signals confidence in gold’s role during uncertain times.

None of this guarantees future appreciation. Gold can decline in value, and past performance doesn’t predict future results.

But the institutional backdrop for gold demand has rarely been stronger. And for customers considering whether to position part of their retirement in physical metals, that context matters.

What You Can Do

You’ve now seen why the American Gold Eagle dominates precious metals IRAs:

- Legal certainty: A statutory exception makes it automatically IRA-eligible without meeting the standard purity requirements.

- Durability: The 22-karat alloy resists scratching better than pure gold alternatives.

- Liquidity: Universal recognition means you can sell quickly at competitive prices.

- Heritage: The Saint-Gaudens design connects you to over a century of American numismatic tradition.

- Government backing: The U.S. Mint guarantees weight, content, and purity on every coin.

The question isn’t whether Gold Eagles are a solid choice. It’s whether acquiring physical gold makes sense for your specific situation.

That’s a personal decision.

It depends on your timeline, your existing holdings, your concerns about the financial system, and what you want to leave behind for your children or grandchildren.

| Consideration | Questions to Ask Yourself |

|---|---|

| Timeline | How many years until you plan to access these funds? |

| Diversification | What percentage of your retirement is currently in physical assets? |

| Legacy goals | Do you want to leave tangible assets to children or grandchildren? |

| Control | How important is holding something outside the traditional financial system? |

| Comfort level | Are you comfortable with gold’s price fluctuations in the short term? |

There’s no single right answer. But if you’ve read this far, you’re clearly thinking seriously about these questions.

Frequently Asked Questions

Is a Gold American Eagle pure gold?

Each American Gold Eagle contains exactly one full troy ounce of pure gold.

The coin weighs slightly more than an ounce because it includes a small amount of silver and copper alloy for durability.

So while the coin itself is 91.67% gold (22-karat), you’re still getting a full ounce of pure gold content—guaranteed by the U.S. Mint.

Why does the IRS allow 22-karat Gold Eagles when other coins must be 24-karat?

Congress carved out a specific exception in Internal Revenue Code Section 408(m)(3) for American Eagle gold coins.

Because they’re minted by the U.S. government and explicitly named in federal law, they bypass the standard 99.5% purity requirement that applies to other gold coins and bars.

This makes the Gold Eagle the only 22-karat coin eligible for precious metals IRAs.

Are American Gold Eagles more liquid than foreign gold coins?

In the United States, yes.

American Gold Eagles are recognized by virtually every coin dealer, pawn shop, and precious metals buyer in the country. Their U.S. Mint backing and standardized specifications mean you can sell them quickly without authentication delays.

Foreign coins like the Canadian Maple Leaf or South African Krugerrand may require additional verification steps when selling domestically.

Can I take physical delivery of my Gold Eagles when I reach retirement age?

Yes.

Once you reach age 59½, you can take an in-kind distribution of your actual Gold Eagle coins rather than selling them and receiving cash. You’ll owe ordinary income tax on the fair market value at the time of distribution, but you’ll physically hold the coins you’ve accumulated.

Many customers prefer this option because it gives them direct control over their metals.

What’s the difference between a Bullion Eagle and a Proof Eagle for an IRA?

Both are IRA-eligible, but they serve different purposes.

Bullion Eagles are struck for volume and priced close to the gold spot price plus a modest premium.

Proof Eagles are specially struck with polished dies, have mirror-like finishes, and carry higher premiums due to limited mintages.

Most retirement-focused customers choose bullion versions for their lower cost per ounce of gold content.

How long does it take to add American Gold Eagles to a new precious metals IRA?

Most customers complete the entire process—opening the account, funding it, and purchasing their first Gold Eagles—within one to three weeks.

The timeline depends on how quickly your existing retirement account processes the rollover or transfer. Once funds arrive at your self-directed IRA custodian, purchasing the coins typically happens within a few business days.

Do American Gold Eagles carry any face value?

Yes.

The one-ounce Gold Eagle carries a $50 face value, making it legal tender in the United States. However, this face value is purely symbolic—the actual market value is based on the gold content plus a small premium.

No one would spend a Gold Eagle at face value when it contains well over $4,000 worth of gold at current prices.

Are fractional Gold Eagles (1/2 oz, 1/4 oz, 1/10 oz) also IRA-approved?

Yes, all four sizes of American Gold Eagles qualify for precious metals IRAs.

However, most customers focused on retirement choose the one-ounce version because it carries the lowest premium per ounce of gold content.

Fractional sizes can be useful for customers who want flexibility in future distributions or prefer smaller incremental purchases.

The Takeaway

The American Gold Eagle has earned its position as the most popular IRA-approved gold coin for practical reasons—not marketing hype.

It offers legal clarity that no other 22-karat coin can match. It provides durability that 24-karat alternatives lack. It delivers liquidity that makes exit strategies straightforward. And it carries government backing that inspires confidence.

For customers focused on protecting their retirement, building a legacy, and holding something tangible outside the traditional financial system, the Gold Eagle remains the standard against which other options are measured.

Precious metals may appreciate, depreciate, or remain unchanged based on market conditions. Past performance doesn’t guarantee future results. Consult your CPA or tax professional for guidance specific to your situation.

But if physical gold makes sense for your retirement strategy, the American Gold Eagle deserves serious consideration.

If you’re thinking “this all makes sense, but I don’t have time to figure it out on my own,” you’re not alone. Most customers we work with felt the same way before they realized how straightforward the process can be with the right guidance.

That’s why we offer a complimentary consultation to walk you through your options—including our No Fee Precious Metals IRA, which covers custodial fees for the lifetime of the account on qualified purchases.

We’ll show you exactly:

- How the No Fee IRA works and whether you qualify

- The difference between U.S.-minted coins and foreign alternatives

- What to expect from the purchasing and delivery process

- How to roll over or transfer existing retirement funds

- What ongoing support looks like after your purchase

Learn About the No Fee IRA — no obligation, just actionable insights you can use whether you work with us or not.

If the American Gold Eagle is the right choice for your retirement, we’re here to help you acquire it with clarity and confidence.