Here’s the short version: segregated storage keeps your gold in its own labeled box—separate from everyone else’s. Non-segregated storage pools your gold with identical items from other customers.

Both are safe. Both are insured. Both are IRS-approved.

So why does the choice matter?

It comes down to one question. When you eventually take delivery of your gold—whether that’s five years from now or twenty—do you want your exact coins back? Or are you fine receiving equivalent coins of the same type?

That’s really the core of it.

Segregated storage costs a bit more—typically $50 to $150 extra per year. But it guarantees you’ll get back the precise coins or bars you originally purchased.

Non-segregated storage saves you money. You still own real, physical gold. But when you withdraw, you might receive different coins than the ones you started with—same type, same weight, same purity, just not the identical items.

For most folks? Either option works just fine.

But let’s dig into the details so you can decide what fits your situation.

How Segregated Storage Actually Works

Think of segregated storage like having your own personal safe deposit box inside a larger vault.

Your coins arrive at the depository. Staff inspect them, record the details—weight, type, serial numbers—and place them in a container with your name on it.

That container sits on a shelf, separate from everyone else’s metals.

What Makes It Different

The key word here is separation.

Your gold doesn’t just get tracked on paper. It gets physically kept apart from other customers’ holdings.

Delaware Depository—one of the largest precious metals custodians in the country—describes it this way. They say segregated bullion is “inspected, packaged, labeled, and stored in high-security vaults, physically separate and apart from the bullion of other customers.”

Pretty straightforward, right?

When you want your gold back, they pull your box. They verify the contents match your account records. They ship your items—the exact items you deposited—right to your door.

No substitutions. No questions about which coins are yours.

Who Typically Chooses This Option

Some customers just sleep better knowing their gold sits in its own space. That’s reason enough.

But there are a few situations where segregated storage makes extra sense.

Larger holdings. If you’ve got $100,000 or more in physical gold, that extra $50-$150 per year is a tiny fraction of your total value. The added peace of mind? Might be worth every penny.

Estate planning. When it’s time to pass metals to your heirs, having clearly segregated assets makes the transfer simpler. Less paperwork. Less confusion. Less potential for disputes.

Future delivery plans. Maybe you’re building a position in Gold American Eagles with the intention of eventually holding them yourself. Segregated storage means you’ll receive those exact coins years later—not substitutes.

And honestly? Some folks just like the idea of their property staying theirs in the most literal sense.

Nothing wrong with that.

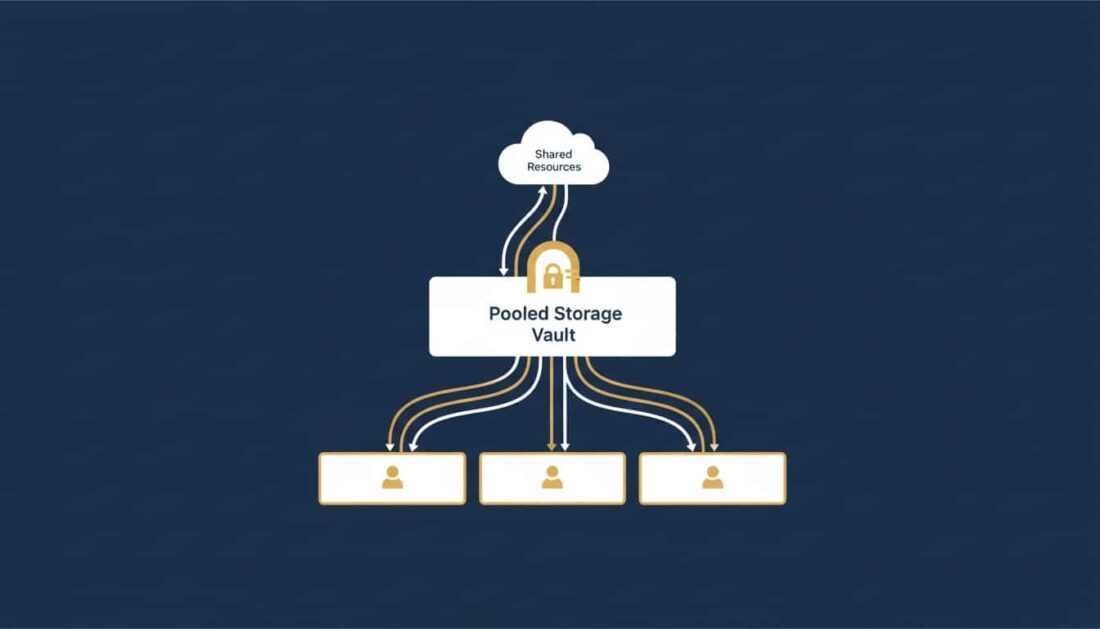

How Non-Segregated Storage Works

Non-segregated storage—sometimes called “commingled” or “pooled”—takes a different approach.

Your gold gets stored alongside identical items from other customers. The depository tracks who owns what by product type and quantity, not by individual serial numbers.

Now, here’s what trips people up. This doesn’t mean you own “shares” of gold or some kind of paper claim.

You still own actual, physical gold. It’s real. It’s sitting in a vault. It’s insured.

The depository just manages inventory differently.

How Your Ownership Stays Protected

Let’s say you purchase ten 1-ounce Gold American Eagles through your precious metals IRA.

The depository records that your account holds ten Gold Eagles. Those coins go into a vault section with Gold Eagles from other customers—but everyone’s quantities are tracked meticulously.

They know exactly how many coins belong to you. They’re insured. They’re accounted for. They’re legally yours.

The difference? Your ten coins aren’t sitting in their own labeled box. They’re stored together with other Gold Eagles because—functionally—one is identical to another.

Delaware Depository’s FAQ puts it simply. They store “fungible bullion products which, by nature, are commercially interchangeable.”

Fungible. That’s the key word.

Think about it like cash at a bank. The bank doesn’t keep “your” specific twenty-dollar bills in a separate drawer. But you still own your balance. You can withdraw it anytime.

Same idea here.

The Trade-Off: Lower Cost, Less Specificity

Non-segregated storage costs less because it’s simpler to manage.

No separate containers for every customer. No tracking individual serial numbers. Less administrative overhead.

Those savings get passed along to you.

| Storage Type | Annual Fee Range | What You Get at Withdrawal |

|---|---|---|

| Segregated | $150 – $300 | Your exact original coins/bars |

| Non-Segregated | $100 – $250 | Equivalent coins/bars of same type |

For customers focused on owning physical gold as a wealth preservation strategy—rather than collecting specific items—non-segregated storage delivers the same core benefit at a lower price.

Your gold is real. It’s vaulted. It’s insured. It’s yours.

You simply might not get the identical coins you started with if you ever take delivery.

For most people? That’s perfectly fine.

Side-by-Side: What’s Really Different?

Let’s break down the practical differences. Because once you see them clearly, the choice usually becomes obvious.

Security and Insurance

Here’s something that surprises a lot of folks: both storage types offer the same robust security and insurance.

Delaware Depository carries $1 billion in “all-risk” insurance through Lloyd’s of London. That coverage applies to segregated and non-segregated holdings.

Brinks—another major depository—provides comprehensive vault and cargo insurance across both options.

So the question isn’t whether your gold is protected. It absolutely is.

The difference is more about documentation.

With segregated storage, insurance claims can reference your specific, identified items. There’s a cleaner paper trail.

With non-segregated storage, claims reference your proportional share of pooled holdings.

Either way? You’re covered.

The Cost Difference

Storage fees vary by depository and custodian. But the pattern holds: segregated costs more.

Here’s what you’re typically looking at:

| Fee Type | Segregated | Non-Segregated |

|---|---|---|

| Annual Storage | $150 – $300 | $100 – $250 |

| As % of Holdings | ~1.0% – 1.5% | ~0.5% – 0.8% |

| Typical Minimum | $150+ | $95 – $125 |

The premium for segregated storage usually runs $50 to $150 per year.

That’s not nothing. But it’s not a dealbreaker either—especially for larger accounts where it represents a fraction of a percent.

One industry source described the incremental cost as “less than $50 per year” at some depositories. They called it a “small price to pay for added security” if item-specific control matters to you.

What Happens When You Withdraw

This is where the rubber meets the road.

Eventually, you’ll want to take a distribution from your precious metals IRA. Maybe it’s a Required Minimum Distribution after age 73. Maybe it’s an in-kind distribution where you receive physical gold instead of cash.

Your storage type determines what shows up at your door.

Segregated storage: You get back the exact coins or bars you originally purchased. Same serial numbers. Same items.

Non-segregated storage: You get equivalent coins or bars—same type, weight, and purity—but not necessarily the precise ones you started with.

For standard bullion like Gold Eagles? One coin is functionally identical to another. The distinction is mostly academic.

But if you specifically chose certain coins—maybe a particular mint year—segregated storage preserves that choice.

Why This Matters for In-Kind Distributions

One of the best things about a precious metals IRA? You can eventually hold what you own.

Unlike a traditional IRA where distributions come as cash transfers, a precious metals IRA gives you a choice. Take cash—or take the actual physical gold.

That second option is called an “in-kind distribution.”

And your storage type affects how it works.

What’s an In-Kind Distribution?

After age 59½, you can take penalty-free distributions from your IRA.

Starting at age 73, you’re required to take minimum distributions—RMDs.

With a precious metals IRA, you’ve got options. You can sell the metals and receive cash. Or you can have the depository ship the actual gold to you.

That’s the beauty of physical ownership. You’re not stuck with paper.

According to IRS guidelines, precious metals in an IRA must be stored by a qualified trustee. But when you’re eligible for distributions, you can take delivery of the metals themselves.

Many customers choose physical gold specifically for this reason.

How Storage Type Plays In

If you chose segregated storage, the process is clean.

The depository pulls your labeled container. Verifies the contents. Ships your specific coins or bars—insured—directly to you.

With non-segregated storage, it’s a bit different.

The depository fulfills your request with equivalent products from their pooled inventory. You’ll receive the same type and quantity. Just not necessarily the identical items you originally purchased.

For most folks, this doesn’t change the outcome. You’re receiving physical gold of the same value and specifications.

But here’s a scenario to consider.

Say you bought ten Gold Eagles in 2020 when gold was around $1,800/oz. You chose non-segregated storage to save on fees. Five years later, you take an in-kind distribution.

The depository ships you ten Gold Eagles. But they’re from a 2025 mint batch—not your original 2020 coins.

Functionally identical? Yes.

But if you had a reason for wanting those original coins—record-keeping, sentimental value, whatever—you’d need segregated storage to guarantee it.

How to Decide: A Simple Framework

There’s no universally “right” answer here. It depends on your priorities.

But let’s make this easier.

Non-Segregated Storage Probably Makes Sense If…

You’re focused on cost efficiency. Saving $50-$150 per year adds up over time.

You view gold primarily as a wealth preservation tool. Item-specific ownership matters less than simply having the gold.

You’re purchasing standard bullion products. Gold Eagles, Maple Leafs, and similar coins are fungible by design.

You don’t plan to take physical delivery anytime soon. If your metals will sit in the IRA for decades, the distinction between “your” coins and “equivalent” coins may not matter.

You’re comfortable with depository-level security. Reputable facilities like Delaware Depository and Brinks protect your holdings regardless of storage type.

For most precious metals IRA holders? Non-segregated storage delivers the core benefits at a lower cost.

Segregated Storage Probably Makes Sense If…

You want to receive your specific items. If getting back the exact coins you purchased matters, this is the only way to ensure it.

You have larger holdings. At $100,000+, the extra fee is a fraction of a percent.

You’re planning estate transfers. Clear documentation of specific assets simplifies inheritance.

You prefer maximum control. Some customers simply sleep better knowing their gold sits in its own space. That’s valid.

You purchased specific coin types or years. If you deliberately selected certain products, segregated storage preserves those choices.

You plan to take physical delivery soon. If you’re approaching distribution age and want your original purchases, segregated makes it seamless.

Three Questions to Ask Yourself

Before you decide, think through these:

How long will I hold these metals? If it’s decades, the specificity of segregated storage may not matter much.

Does receiving my exact original coins matter? Or am I fine with equivalent items?

How significant is the fee difference relative to my total holdings? For a $25,000 account, $100/year is 0.4%. For a $250,000 account, it’s 0.04%.

Your answers will point you toward the right choice.

How Brighton Helps You Navigate This

Choosing between storage types doesn’t have to be complicated.

At Brighton, we walk you through it—just like we walk you through product selection, custodian choice, and everything else.

That’s what concierge service means.

What That Looks Like in Practice

When you work with us, you’re not just purchasing gold. You’re getting support at every stage of ownership.

For storage decisions, that means:

- Understanding your goals. Are you focused on cost? Peace of mind? Estate planning? Your priorities shape the recommendation.

- Explaining the trade-offs clearly. We don’t push one option over another. We help you see what each choice means for your situation.

- Coordinating the logistics. Brighton works with established custodians and IRS-approved depositories. We help make sure everything runs smoothly.

- Supporting you after the purchase. Questions about distributions, delivery, storage changes? We’re here.

If you’ve already rolled over a 401(k) into a Gold IRA or you’re thinking about it, storage becomes part of the conversation.

We address it alongside everything else.

The No Fee IRA

Brighton offers a No Fee Precious Metals IRA that covers custodial fees for the lifetime of the account on qualified purchases.

Why does that matter for storage decisions?

Because it changes the cost picture. If your custodial fees are already covered, the main variable left is depository storage—where the segregated vs. non-segregated choice has the biggest impact.

We’re happy to walk through the numbers with you.

Most customers find that even with segregated storage, the total annual cost stays manageable—especially compared to traditional retirement accounts loaded with mutual fund expense ratios.

Common Depositories for Precious Metals IRAs

Your custodian typically partners with one or more IRS-approved depositories.

Here’s a quick look at the major players.

Delaware Depository

Delaware Depository is one of the most widely used in the country.

Founded in 1999, headquartered in Wilmington, Delaware. Licensed by CME Group for gold, silver, platinum, and palladium.

- Offers both segregated and non-segregated storage

- $1 billion “all-risk” insurance through Lloyd’s of London

- Multiple U.S. locations—Delaware and Nevada

- Customer assets held off-balance sheet

- Online account access through their IRA Gateway portal

- Better Business Bureau A+ rating

They specifically note that “regardless of the storage arrangement selected, customers may transfer or take delivery of their bullion at any time.”

Good to know.

Brinks Global Services

Brinks is a name most folks recognize from armored transport.

But they also operate secure vaulting facilities for precious metals.

- Over 160 years in security (founded 1859)

- Facilities across the U.S. and internationally

- IRS-approved for precious metals IRA storage

- Comprehensive cargo and vault insurance

- Real-time inventory reporting

- Armored transport services

Some customers prefer Brinks for the brand recognition and global infrastructure.

International Depository Services (IDS)

International Depository Services operates facilities in Delaware, Texas, and Canada.

- COMEX-approved depositories

- Class III UL-rated vaults

- Independent of the banking system

- Bureau Veritas annual audits

- Online customer portal

IDS positions itself as an option for customers who prefer depositories not tied to traditional financial institutions.

How to Choose a Depository

Usually, your custodian has established relationships with specific depositories. You may have a choice between options—or your custodian may use one primary facility.

Questions worth asking:

- Which depositories does this custodian work with?

- What are the storage fee structures for each option?

- What’s the process for taking physical delivery?

- How is insurance coverage structured?

Brighton can help you sort through these details as part of our concierge service.

Frequently Asked Questions

Is my gold insured in segregated storage?

Yes.

Reputable depositories like Delaware Depository and Brinks carry comprehensive “all-risk” insurance—often through Lloyd’s of London.

Delaware Depository, for example, maintains $1 billion in coverage. That applies to both segregated and non-segregated holdings.

The difference? Segregated storage ties claims to your specific, identified items. Non-segregated coverage applies to your proportional share of pooled metals.

Either way, you’re protected.

Does segregated storage cost more than commingled?

Yes—typically $50 to $150 more per year.

Annual fees for segregated storage generally run $150 to $300. Non-segregated storage runs $100 to $250.

The premium covers the extra labor, space, and administrative procedures required to keep your metals physically separate.

For larger accounts, this difference represents a small fraction of total value.

What does “commingled” gold storage actually mean?

Commingled—also called non-segregated or pooled—means your gold is stored alongside identical products from other customers.

The depository tracks ownership by product type and quantity. Not by specific serial numbers.

You still have full legal ownership. Your gold is still real and insured. Individual items just aren’t labeled with your name.

Think of it like cash at a bank. They don’t keep “your” specific bills in a separate drawer—but you still own your balance.

Can I switch from non-segregated to segregated storage later?

Most depositories allow this.

The process typically involves a written request to your custodian, payment of any fee differential, and a brief processing period.

During that time, the depository physically separates and relabels your metals.

Check with your custodian for their specific procedures and any transfer fees.

Will I get the exact same coins back with non-segregated storage?

Not necessarily.

You’ll receive coins or bars of the same type, weight, and purity. But not necessarily the exact items with the original serial numbers.

For standard bullion like Gold Eagles? This distinction is largely academic. One coin is functionally identical to another.

But if receiving your specific original items matters—for sentimental reasons or record-keeping—segregated storage guarantees that outcome.

Which storage type is better for a Gold American Eagle?

For most customers purchasing Gold Eagles as a wealth preservation strategy? Non-segregated storage offers excellent value.

These coins are fungible—meaning one is interchangeable with another of the same type.

But if you want the exact coins you purchased when you eventually take delivery, segregated storage provides that assurance.

It depends on whether item-specific ownership matters more to you than cost savings.

Does the IRS require segregated storage for IRAs?

No.

The IRS requires precious metals in an IRA be stored by a qualified custodian at an IRS-approved depository. But it doesn’t mandate segregated storage specifically.

Both options satisfy custody requirements under IRC Section 408(m)—as long as the depository meets federal standards for security, insurance, and reporting.

Storage type is a personal preference. Not a regulatory requirement.

The Bottom Line

This choice isn’t about right or wrong. It’s about matching storage to your priorities.

Non-segregated storage offers cost efficiency, full legal ownership, and complete insurance protection. For customers focused on the wealth preservation benefits of physical gold and silver—not collecting specific items—it’s often the practical choice.

Segregated storage provides peace of mind through physical separation, exact-item traceability, and assurance you’ll receive your specific purchases. For customers who value maximum control or are planning estates, the modest premium is easily justified.

Both options work.

Both are IRS-approved.

Both protect your property.

The question is simply: which one fits you?

Ready to explore your options?

If you’re thinking “this all makes sense, but I don’t have time to figure it out on my own”—you’re not alone.

Most customers we work with felt the same way before they realized how straightforward the process can be with the right guidance.

That’s why we offer a complimentary consultation to walk you through your options—including our No Fee Precious Metals IRA, which covers custodial fees for the lifetime of the account on qualified purchases.

We’ll show you exactly:

- How the No Fee IRA works and whether you qualify

- The difference between U.S.-minted coins and foreign alternatives

- What to expect from the purchasing and delivery process

- How to roll over or transfer existing retirement funds

- What ongoing support looks like after your purchase

Learn About the No Fee IRA — no obligation, just actionable insights you can use whether you work with us or not.

Storage decisions are just one part of the picture. Let’s make sure you understand all your options before you commit to any particular path.