Here’s a surprise most people don’t expect: gold doesn’t track inflation the way you might think.

It doesn’t rise in lockstep with the Consumer Price Index. It doesn’t move predictably when gas prices spike or grocery bills climb.

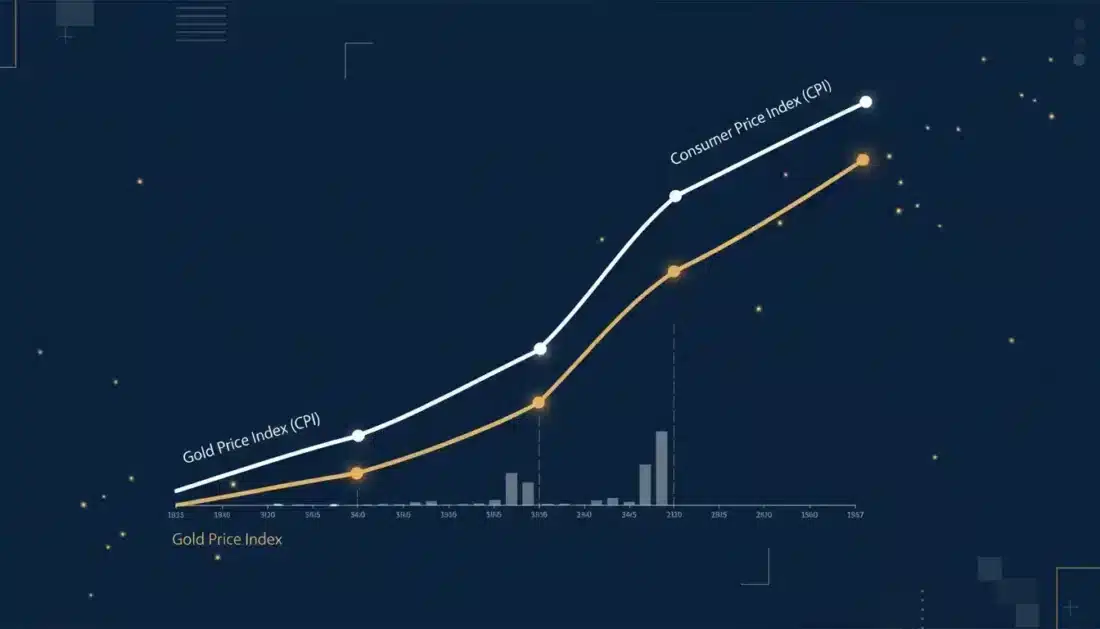

And yet—over the long term—gold has consistently preserved purchasing power while the dollar has lost roughly 96% of its value since 1913.

So what’s really going on here?

Since 2020, cumulative inflation has eaten away about 25% of the dollar’s buying power. A dollar today gets you what 80 cents bought just six years ago.

Gold? It’s risen from around $1,500 per ounce to over $4,600 during that same stretch.

That’s not a coincidence. But it’s also not as simple as “inflation goes up, gold goes up.”

Understanding how gold actually behaves—and why it works differently than most people assume—gives you clarity and control over your decisions. Whether you’re evaluating gold as a retirement strategy or simply trying to protect what you’ve built, the truth is more nuanced than the headlines suggest.

Let’s walk through it together.

What the Numbers Actually Show

Here’s what we’re seeing when we dig into the data.

According to the World Gold Council, only about 16% of gold’s price movements since 1971 can be explained by changes in CPI inflation.

That’s a weak correlation for something often called “the ultimate inflation protector.”

But here’s what matters more: gold has delivered an average inflation-adjusted return of roughly 4% annually since 1970. It hasn’t just kept pace with rising prices—it’s outpaced them over time.

How do those two facts fit together?

Short-Term Swings vs. Long-Term Stability

Gold doesn’t behave like a Treasury Inflation-Protected Security. Month-to-month—even year-to-year—gold prices can swing wildly compared to CPI.

But zoom out, and the picture changes.

- The 1970s — Gold surged from $35 per ounce to over $800 as inflation peaked above 14%. This decade cemented gold’s reputation.

- The 1980s and 1990s — Gold stayed relatively flat despite moderate inflation. Owners who expected automatic gains were disappointed.

- 2008 to 2020 — Gold climbed from around $800 to over $2,000—not because of high inflation, but due to money printing, economic uncertainty, and currency concerns.

- 2020 to 2026 — Gold has more than tripled while cumulative inflation hit 25%. Strong performance during a period when purchasing power protection mattered most.

The pattern? Gold performs best during monetary instability—conditions that often accompany inflation but aren’t limited to it.

Why Month-to-Month Tracking Misses the Point

If you’re focused on whether gold perfectly tracks next month’s CPI report, you’re asking the wrong question.

CPI measures how much more groceries or gasoline cost compared to last year. It’s a snapshot of consumer prices.

Gold responds to something deeper: the purchasing power of the dollar itself, confidence in monetary policy, and the desire for something tangible outside the traditional financial system.

When the Federal Reserve expanded the money supply by over $6 trillion during 2020-2021, gold didn’t wait for CPI to catch up. It moved in anticipation of what that expansion would mean for the dollar’s long-term value.

This is why central banks—who think in decades, not quarters—continue accumulating gold even when short-term inflation data bounces around.

| Time Period | Cumulative Inflation | Gold Price Change | What Happened |

|---|---|---|---|

| 1971-1980 | +105% | +2,329% | Significant outperformance |

| 1980-2000 | +119% | -44% | Gold lagged |

| 2000-2011 | +31% | +505% | Strong outperformance |

| 2020-2026 | +25% | +207% | Strong outperformance |

Understanding Real Yields—And Why They Matter

One of the strongest historical predictors of gold’s performance isn’t inflation itself. It’s something called “real yields.”

Real yields represent the return you actually earn on bonds or savings after subtracting inflation.

When real yields turn negative—meaning inflation exceeds the interest rate you’re earning—gold becomes significantly more attractive.

Here’s why this matters for your situation.

The Opportunity Cost Question

When you hold physical gold, you’re holding something that doesn’t pay dividends or interest.

In a world where bonds pay 5% and inflation runs at 2%? There’s a real cost to holding gold instead.

But when bonds pay 5% and inflation runs at 7%? You’re losing purchasing power holding those bonds. Suddenly gold looks a lot more appealing.

- Historical relationship — Between 2003 and 2021, gold prices and 10-year real yields showed a correlation of approximately -0.73 (strongly inverse). When real yields fell, gold rose.

- Post-2022 shift — This relationship has weakened. Gold has performed well even as real yields stayed elevated above 1.5%. Analysts point to structural factors like central bank buying and de-dollarization trends.

- 2026 outlook — With the Federal Reserve expected to continue cutting rates and inflation remaining above target, real yields could compress further—providing ongoing support for gold prices.

The key insight? Even if the traditional relationship has weakened, the fundamental logic remains. When your dollars lose purchasing power sitting in savings accounts or bonds, tangible things that hold their value become more attractive.

What “Debasement” Actually Means

You’ll hear analysts describe gold as a “debasement protector” rather than an “inflation protector.” The distinction matters.

Inflation measures consumer prices. Debasement refers to the loss of a currency’s underlying value due to excessive money creation, unsustainable debt, or loss of confidence.

Since 1913, the U.S. dollar has lost approximately 96% of its purchasing power according to Federal Reserve data.

That’s not a short-term blip. That’s a century-long trend.

Gold priced in dollars has risen from $20.67 per ounce in 1913 to over $4,600 today. Not because gold became more valuable in absolute terms—but because it took increasingly more dollars to buy the same amount of gold.

This is what protecting purchasing power with gold actually looks like. You’re not betting on inflation ticking up 0.3% next month. You’re positioning yourself against the long-term trajectory of fiat currency.

What Central Banks Understand

Central banks have purchased over 1,000 tonnes of gold annually for three consecutive years. That’s roughly double the decade-long average before 2022.

They’re not doing this because they expect CPI to jump next quarter.

They’re building reserves for reasons that should resonate with anyone focused on long-term wealth preservation.

A Structural Shift in Reserve Management

According to the World Gold Council’s 2025 survey, 73% of central bank respondents expect the U.S. dollar’s share of global reserves to decline over the next five years.

A record 43% plan to increase their own gold holdings.

- Poland — Added 67 tonnes in the first half of 2025, bringing total reserves to 543 tonnes (28% of total reserves)

- China — Continued consistent monthly additions despite record prices, signaling strategic priority over cost considerations

- Brazil — Purchased 43 tonnes over three months in late 2025, marking a significant acceleration

- India, Turkey, Kazakhstan — All maintained steady buying programs throughout 2025

These aren’t speculative moves. Central banks think in decades, not quarters.

Their continued accumulation at prices above $4,000 per ounce signals confidence in gold’s long-term value—regardless of where prices go in any given month.

J.P. Morgan forecasts approximately 755 tonnes of central bank purchases in 2026. That’s lower than peak years but still well above the pre-2022 average of 400-500 tonnes.

Why This Matters for You

The phrase “de-dollarization” describes a global trend of reducing dependence on U.S. dollar-denominated holdings.

It’s not just central banks. Pension funds, sovereign wealth funds, and large institutions are increasingly adding gold to their strategic reserves.

This trend creates structural support for gold prices regardless of short-term inflation data.

It also raises an important question: If the world’s largest reserve managers are diversifying away from dollar holdings, what does that tell you about keeping all your wealth in dollar-denominated accounts?

Understanding the intrinsic value of precious metals helps explain why this shift is happening. Gold has no counterparty risk. It can’t be printed or created. And it’s maintained its value across civilizations for thousands of years.

When Gold Performs Best—And When It Doesn’t

Not all inflationary periods work the same way. Gold’s response depends heavily on what’s causing prices to rise—and what else is happening in the economy.

Conditions That Favor Gold

Gold tends to deliver its strongest performance under specific conditions:

- Cost-push inflation — When prices rise due to supply shocks (like oil crises), gold typically responds positively. The 1970s showed this pattern clearly.

- Monetary debasement — When excessive money creation drives inflation, gold benefits from loss of confidence in the currency. The 2020-2025 period demonstrated this.

- Currency instability — When confidence in a currency collapses, gold serves as a store of value. This explains gold’s popularity in countries experiencing severe currency problems.

- Negative real yields — When inflation exceeds interest rates, the cost of holding gold disappears. This has been a consistent driver historically.

Conditions That Challenge Gold

Gold’s purchasing power protection can weaken under certain circumstances:

- Demand-driven inflation — When prices rise due to strong economic growth rather than currency debasement, gold may lag. Strong growth often brings rising real yields and a stronger dollar—headwinds for gold.

- Falling inflation with high real yields — When inflation is dropping and real yields are rising, gold faces pressure. The 1980s and 1990s showed this pattern.

- Strong economic confidence — When markets are rallying and optimism runs high, attention may shift away from gold toward growth-oriented options.

| Inflation Type | Gold Performance | Example Period |

|---|---|---|

| Supply shock | Strong | 1973-1980 |

| Monetary debasement | Strong | 2020-2025 |

| Demand-driven growth | Moderate to weak | 1983-1999 |

| Falling inflation | Weak | 1981-1985 |

| Currency crisis | Very strong | Various periods |

The takeaway? Gold isn’t a simple inflation tracker. But it tends to perform best precisely when purchasing power protection matters most—during periods of monetary instability, currency concerns, and loss of confidence in traditional financial systems.

The 2026 Outlook: What Analysts Expect

Major financial institutions have published their 2026 gold outlook. The consensus points to continued strength—though with varying degrees of optimism.

Price Forecasts From Leading Institutions

- J.P. Morgan — Forecasts gold averaging $5,055 per ounce by Q4 2026, with potential to reach $5,400 by end of 2027. They cite continued central bank buying and structural demand as primary drivers.

- Goldman Sachs — Raised their December 2026 forecast to $5,400 per ounce, arguing that macro and policy concerns have become “sticky.”

- Morgan Stanley — Revised 2026 forecast upward to $4,400 per ounce, citing strong ETF inflows and retail demand alongside institutional buying.

- UBS — Expects gold to reach $5,000 per ounce in 2026 amid macroeconomic and geopolitical concerns.

- World Gold Council — Projects gold could rise 5-15% from current levels in a base case, with potential for 15-30% gains if economic conditions deteriorate significantly.

| Institution | 2026 Price Target | Key Driver Cited |

|---|---|---|

| J.P. Morgan | $5,055 (Q4 avg) | Central bank demand |

| Goldman Sachs | $5,400 (Dec) | Sticky concerns |

| Morgan Stanley | $4,400 | ETF and retail flows |

| UBS | $5,000 | Macro uncertainty |

| Financial Times (11-bank avg) | $4,610 | Consensus view |

What Could Push Prices Higher or Lower

Analysts identify several scenarios that could move gold above or below their forecasts:

What could push gold higher:

- Escalation of geopolitical conflicts driving demand for tangible holdings

- Sharper-than-expected economic slowdown prompting aggressive Fed cuts

- Acceleration of de-dollarization trends

- Continued strong central bank and ETF buying

What could push gold lower:

- Stronger-than-expected economic growth reducing demand for protection

- Fed holding rates higher for longer, pushing up real yields

- Significant dollar strength

- Central banks becoming net sellers (considered unlikely by most analysts)

For customers focused on long-term wealth preservation rather than short-term price speculation, these forecasts suggest continued relevance for physical gold. The question isn’t whether gold will hit exactly $5,055—it’s whether holding something tangible makes sense given the structural forces at play.

Silver: The Overlooked Companion

While gold gets most of the attention in inflation discussions, silver offers characteristics that complement a wealth protection strategy.

Silver’s Dual Nature

Silver functions as both a monetary metal and an industrial commodity. This dual identity creates unique dynamics:

- Monetary demand — Like gold, silver has served as money throughout history and attracts buying during uncertainty.

- Industrial demand — Over 58% of global silver demand comes from industrial applications, including solar panels, electronics, and electric vehicles. This creates demand that’s relatively price-insensitive.

- Supply constraints — Silver mine production has stagnated while demand continues growing. The Silver Institute forecasts ongoing supply deficits through 2026.

Silver has historically shown greater price volatility than gold. But it has also delivered stronger percentage gains during precious metals rallies.

In 2025, silver more than doubled—from under $30 to over $60 per ounce.

How Silver Complements Gold

Research suggests silver and gold perform differently across various conditions:

- Gold shows sharper, more sustained responses during high-inflation periods

- Silver offers protection during both high and low inflation environments due to industrial demand

- The gold-to-silver ratio (currently elevated) suggests silver may offer relative value

For customers building a comprehensive protection strategy, holding both metals provides diversification within the precious metals space. Silver’s lower per-ounce price also makes it more accessible for ongoing accumulation.

Understanding tangible ownership vs. digital exposure matters here too. Physical silver, like physical gold, provides direct ownership without counterparty risk—something paper instruments can’t match.

What This Means for You

So where does this leave you if you’re concerned about protecting your retirement savings or wealth from inflation and currency debasement?

The evidence suggests a nuanced approach.

Gold as Long-Term Purchasing Power Protection

Gold shouldn’t be viewed as a precise inflation tracker. It’s better understood as long-term insurance against currency debasement, monetary instability, and the erosion of purchasing power that happens over decades.

Here’s what the data shows:

- Gold has outpaced inflation over multi-decade periods

- It performs best during conditions of monetary stress—precisely when protection matters most

- Central banks and institutions continue accumulating it for strategic rather than speculative reasons

- It carries no counterparty risk and exists outside the digital financial system

If your goal is protecting what you’ve built over a lifetime from the long-term decline in the dollar’s value, physical gold has historically served that purpose.

What You Can Do

For retirement-focused customers, several practical considerations matter:

- Self-directed IRAs — You can hold physical gold and silver in a retirement account through a self-directed structure. Products like American Gold Eagles are IRA-approved, and the metals are stored in your name at an approved depository. Understanding how a precious metals IRA works helps you evaluate whether this structure fits your situation.

- Physical ownership — Holding metal outside an IRA provides direct access and maximum privacy. Many customers maintain both IRA holdings and physical metal for delivery.

- U.S.-minted products — Products like American Gold Eagles and American Silver Eagles carry the full faith and credit of the U.S. government and are widely recognized. Acquiring U.S.-minted gold coins offers liquidity and authenticity advantages.

- Positioning approach — Most guidance suggests limiting precious metals to a portion of overall holdings rather than concentrating entirely in one area.

The key is matching your approach to your actual goals.

If you’re looking for short-term inflation tracking, gold may not be the right tool.

If you’re focused on preserving purchasing power over decades and holding something tangible outside the traditional financial system, the historical record is more supportive.

Frequently Asked Questions

Does gold always go up when the dollar goes down?

Gold and the U.S. dollar often move in opposite directions—but it’s not a guarantee.

A weaker dollar typically makes gold more affordable for international purchasers and often supports higher prices. But other factors—like central bank buying and global uncertainty—have become bigger drivers in recent years.

The relationship is strongest during periods of aggressive money printing or currency instability.

Don’t assume gold will automatically rise just because the dollar weakens. Real yields, risk appetite, and global demand also play significant roles.

What’s the difference between inflation protection and purchasing power preservation?

Inflation protection typically refers to something that rises in value alongside inflation, tracking CPI increases month-to-month.

Purchasing power preservation takes a longer view—maintaining the real value of your wealth over decades regardless of short-term price swings.

Gold works better as a purchasing power preserver than a precise inflation tracker. It’s maintained its real value over multi-decade periods while showing inconsistent short-term correlation with CPI changes.

If you need month-to-month inflation tracking, Treasury Inflation-Protected Securities may be more appropriate. If you’re focused on decades-long preservation, gold’s track record is stronger.

Is it too late to buy gold at current prices?

That depends entirely on your goals.

If you’re looking for short-term speculation, current elevated prices carry risk. Gold could consolidate, pull back, or continue higher—no one knows with certainty.

But if you’re focused on long-term purchasing power preservation, historical patterns suggest the absolute price matters less than consistent accumulation over time.

Central banks continue acquiring gold at record prices—signaling confidence in its long-term value regardless of entry point.

The key is viewing physical gold as a strategic position rather than a market-timing decision. You’re not trying to buy the bottom. You’re building a position in something that has preserved wealth across centuries.

How does the 25% inflation since 2020 compare to gold’s performance?

Since 2020, cumulative inflation has reduced the dollar’s purchasing power by roughly 25%. According to Bureau of Labor Statistics data, a dollar today buys about 80 cents worth of goods compared to 2020.

During this same period, gold has risen from around $1,500 per ounce to over $4,600—gains of more than 200%.

This significant outperformance shows gold’s potential during periods of elevated inflation and currency concerns.

That said, past performance doesn’t guarantee future results. Gold’s relationship with inflation varies across different economic conditions.

Which is better for inflation protection: physical gold or mining stocks?

Physical gold and mining stocks serve different purposes and carry different risk profiles.

Physical gold gives you direct ownership of something tangible with no counterparty risk. Its value doesn’t depend on management decisions, operational costs, or stock market sentiment. This makes it ideal for wealth preservation and crisis protection.

Mining stocks offer potential leverage to gold prices—when gold rises, profitable miners may rise even more. They may also provide dividends.

But they carry company-specific risks including management quality, production costs, regulatory issues, and general stock market correlation.

For retirement protection and purchasing power preservation, physical gold typically provides more stability and direct exposure to the metal’s value. Mining stocks may offer growth potential but introduce risks that physical metal doesn’t carry.

Why do central banks keep buying gold if it doesn’t perfectly track inflation?

Central banks aren’t looking for short-term inflation tracking.

They want long-term reserve diversification, protection against currency instability, and something with no counterparty risk.

Since 2022, they’ve purchased over 1,000 tonnes annually—signaling a structural shift away from dollar-denominated reserves.

The World Gold Council’s 2025 survey found that a record 43% of central bank respondents plan to increase their gold holdings.

This buying continues even at record prices because central banks are focused on strategic positioning, not entry price optimization. They think in decades, not quarters.

Their behavior signals something important about how the world’s most sophisticated reserve managers view currency risk.

How does gold perform when real interest rates are negative?

Historically, gold has performed well when real interest rates turn negative—meaning inflation exceeds the yield on bonds or savings.

Negative real yields reduce the opportunity cost of holding gold while increasing demand for inflation protection.

Between 2003 and 2021, the correlation between gold and real yields was strongly inverse (-0.73).

However, this relationship has weakened since 2022. Gold has performed well even as real yields stayed elevated above 1.5%.

Analysts point to structural factors like central bank buying, de-dollarization trends, and geopolitical uncertainty that support gold independently of the real-yield relationship.

Can I hold physical gold in my retirement account?

Yes.

A self-directed IRA lets you hold IRA-approved physical gold and silver while keeping the same tax advantages as a traditional IRA.

Here’s how it works: you open a self-directed account with an approved custodian, fund it through a rollover or contribution, and purchase IRA-approved metals through a dealer. The metals ship to an approved depository and are held in your name.

Products like American Gold Eagles and American Silver Eagles are specifically approved for IRA holdings.

Establishing a precious metals IRA lets you combine the wealth preservation benefits of physical gold with the tax-advantaged growth of a retirement account.

The Bottom Line

Gold isn’t a perfect inflation tracker in the month-to-month sense that some expect.

The data shows only weak correlation between gold prices and CPI changes over short periods.

But that’s not really the point.

Gold has preserved purchasing power over long time horizons—outperforming inflation significantly since the dollar left the gold standard. It performs best during exactly the conditions when protection matters most: monetary instability, currency concerns, and loss of confidence in traditional financial systems.

Central banks understand this. That’s why they’ve accumulated over 1,000 tonnes annually for three consecutive years, even at record prices.

The question isn’t whether gold perfectly tracks next month’s CPI print.

It’s whether holding something tangible—outside the traditional financial system—makes sense given the long-term trajectory of fiat currency and the structural forces driving demand for alternatives.

For customers focused on protecting what they’ve built—for themselves, their families, and future generations—that’s the question worth answering.

Ready to explore your options?

If you’re thinking “this all makes sense, but I don’t have time to figure it out on my own,” you’re not alone. Most customers we work with felt the same way before they realized how straightforward the process can be with the right guidance.

That’s why we offer a complimentary consultation to walk you through your options—including our No Fee Precious Metals IRA, which covers custodial fees for the lifetime of the account on qualified purchases.

We’ll show you exactly:

- How the No Fee IRA works and whether you qualify

- The difference between U.S.-minted coins and foreign alternatives

- What to expect from the purchasing and delivery process

- How to roll over or transfer existing retirement funds

- What ongoing support looks like after your purchase

Learn About the No Fee IRA—no obligation, just actionable insights you can use whether you work with us or not.

Protecting your purchasing power starts with understanding your options. We’re here to help you get clarity.