Here’s a surprise most people don’t realize: you can hold real, physical gold inside a retirement account. Not a fund. Not a paper promise. Actual coins and bars—stored in your name.

But there’s another way. You can skip the IRA entirely and buy gold directly—taking delivery to your door or storing it on your own terms.

So which approach makes sense?

It comes down to your goals. A Gold IRA gives you tax advantages and lets you use existing retirement funds. Buying direct gives you immediate access and control—no waiting until age 59½.

The good news? You don’t have to choose one or the other. Many customers use both.

This guide walks through how each option works, what they cost, and which scenarios favor each approach. By the end, you’ll have the clarity to move forward with confidence.

What Is a Gold IRA?

A Gold IRA is a retirement account that holds physical gold instead of paper assets.

It works like a traditional or Roth IRA—same contribution limits, same tax rules—but the holdings are coins and bars rather than funds or securities.

Here’s what makes it different: the gold is real. It sits in an IRS-approved vault, insured and held in your name. You’re not buying shares of something that tracks gold prices. You’re buying actual metal.

How a Gold IRA Works

Setting up a Gold IRA involves three parties.

You make the decisions—what to buy, when to buy, how much.

A custodian handles the paperwork. They administer the account, ensure IRS compliance, and facilitate transactions. All IRAs must be held by a custodian—that’s IRS rules, not optional.

A depository stores the gold. This is an IRS-approved vault with institutional security and insurance.

The process works like this: open a self-directed IRA with an approved custodian, fund it through contributions or a rollover from an existing retirement account, select your gold through a dealer like Brighton, and the custodian arranges storage.

You maintain full ownership. The gold is held for your benefit—not mixed with anyone else’s assets.

IRS Purity Requirements

Not just any gold qualifies.

The IRS sets strict purity standards for precious metals held in IRAs:

- Gold — Minimum 99.5% pure (0.995 fineness)

- Silver — Minimum 99.9% pure (0.999 fineness)

- Platinum and Palladium — Minimum 99.95% pure

There’s one notable exception: the American Gold Eagle. Despite being 91.67% pure (22-karat), it’s explicitly approved because it’s minted by the U.S. government with guaranteed weight and content.

Other popular IRA-eligible products include the American Gold Buffalo, Canadian Gold Maple Leaf, and gold bars from COMEX-approved refiners.

What doesn’t qualify? Collectible coins, numismatic items, and anything below the purity threshold.

If you accidentally put ineligible gold in your IRA, the IRS treats it as a taxable distribution. That could mean income taxes plus a 10% penalty if you’re under 59½.

Contribution Limits and Funding

Gold IRAs follow standard IRA contribution rules.

For 2025, you can contribute up to $7,000 per year—or $8,000 if you’re 50 or older. For 2026, limits are set to increase to $7,500 and $8,600 respectively.

But here’s what most people miss: rollovers have no dollar limit.

If you have an existing 401(k), traditional IRA, TSP, or other qualified retirement account, you can transfer any amount into a Gold IRA. A direct trustee-to-trustee transfer keeps the process tax-free and penalty-free.

This is how most customers build substantial gold holdings—not through annual contributions, but through rollovers of existing retirement funds.

What Does Buying Gold Directly Mean?

Buying gold directly means purchasing physical gold that ships to you—or gets stored on your behalf—outside of any retirement account.

No custodian. No IRS purity rules. No contribution limits.

You buy gold, take delivery, and own it outright.

How Direct Purchases Work

The process is straightforward.

Select the gold products you want—coins, bars, rounds. Pay for them. Choose delivery or storage.

- Home delivery — Gold ships to your address via insured carrier, typically within 1–3 weeks

- Vaulted storage — Gold is stored at a secure facility on your behalf, with insurance and allocated storage options

With direct purchases, you control access. There’s no waiting until age 59½. No required distributions. No custodian approval needed to sell or take possession.

You can hold the gold yourself, store it in a safe deposit box, or use professional vault storage. Whatever fits your preference.

What Products Can You Buy?

Unlike a Gold IRA, direct purchases have no IRS purity restrictions.

You can buy U.S.-minted coins like the Gold American Eagle or American Gold Buffalo. Foreign sovereign coins like Canadian Maple Leafs or South African Krugerrands. Gold bars in various sizes. Even collectible coins if that’s your interest—though be aware that numismatic or “collectible” coins often carry significantly higher premiums that can affect your total cost basis.

Most customers favor U.S.-minted bullion for its recognizability and liquidity. The Gold American Eagle remains the most popular choice—widely recognized and easy to sell anywhere in the world.

Who Chooses Direct Purchases?

Direct gold purchases appeal to customers who want:

- Immediate access — No waiting for retirement age

- Privacy — No custodian reporting or brokerage statements

- Flexibility — Ability to sell, gift, or use gold at any time

- Simplicity — No ongoing custodian fees or administrative requirements

- Legacy planning — Easy transfer to heirs outside of probate

Many customers use direct purchases alongside an IRA—using the IRA for long-term retirement savings and direct purchases for accessible reserves.

Gold IRA vs. Direct Purchase: Side-by-Side

Understanding the differences comes down to a few core factors.

| Factor | Gold IRA | Direct Purchase |

|---|---|---|

| Tax Treatment | Tax-deferred (traditional) or tax-free (Roth) | Capital gains taxed at up to 28% |

| Access to Gold | Restricted until age 59½ | Immediate and unrestricted |

| Storage | Required IRS-approved depository | Your choice: home, safe deposit box, or vault |

| Annual Fees | $200–$600 typical (custodian + storage) | None (unless using optional vault storage) |

| Contribution Limits | $7,000–$8,600 per year (rollovers unlimited) | No limits |

| RMDs | Required starting at age 73 (traditional) | None |

| IRS Purity Requirements | Yes (99.5% for gold) | No restrictions |

| Early Withdrawal Penalty | 10% if under 59½ | Not applicable |

When Does a Gold IRA Make More Sense?

A Gold IRA fits customers who:

- Want to use existing retirement funds (401k, IRA, TSP) to acquire gold

- Are focused on long-term retirement planning rather than short-term access

- Want tax-deferred or tax-free growth on their gold holdings

- Don’t need liquidity from their gold before retirement

- Are comfortable with annual custodian and storage fees

The tax advantages are significant.

In a traditional Gold IRA, you defer taxes until withdrawal—potentially decades of growth without annual tax drag. In a Roth Gold IRA, qualified withdrawals are completely tax-free, including all appreciation.

When Do Direct Purchases Make More Sense?

Direct purchases fit customers who:

- Want immediate physical possession and control

- Are buying gold outside of retirement planning

- Want flexibility to sell, gift, or use gold at any time

- Prefer to avoid ongoing custodian fees

- Value privacy and accessibility

There’s also a practical consideration.

Gold held in an IRA appears on custodian statements and requires annual reporting. Direct purchases can be more discreet—though both are subject to IRS reporting requirements for large cash transactions.

Tax Implications: IRA vs. Direct

Taxes are one of the biggest differences between these two approaches.

The rules aren’t complicated. But they significantly affect your net returns.

How Gold IRAs Are Taxed

Traditional Gold IRA:

Contributions may be tax-deductible. The value of your holdings can appreciate tax-deferred—you pay no taxes on gains until you take distributions. Withdrawals are taxed as ordinary income at your marginal rate.

Roth Gold IRA:

Contributions are made with after-tax dollars—no upfront deduction. But potential gains accrue tax-free. Qualified withdrawals after age 59½ (and five years of account ownership) are completely tax-free. That includes all appreciation.

Key consideration: Traditional Gold IRAs require minimum distributions starting at age 73. Roth Gold IRAs have no RMDs during your lifetime.

How Direct Purchases Are Taxed

Physical gold is classified as a collectible by the IRS.

That triggers a different—and often higher—tax treatment than other assets.

According to the IRS, long-term capital gains on collectibles are taxed at your ordinary income rate, capped at 28%. Short-term gains (held one year or less) are taxed as ordinary income at your marginal rate.

Compare that to the maximum 20% rate for other long-term capital gains. As Kiplinger reports, this higher rate applies to physical gold, gold coins, gold bars, and even gold ETFs backed by physical metal.

It’s one reason tax-advantaged accounts like IRAs are attractive for gold holdings.

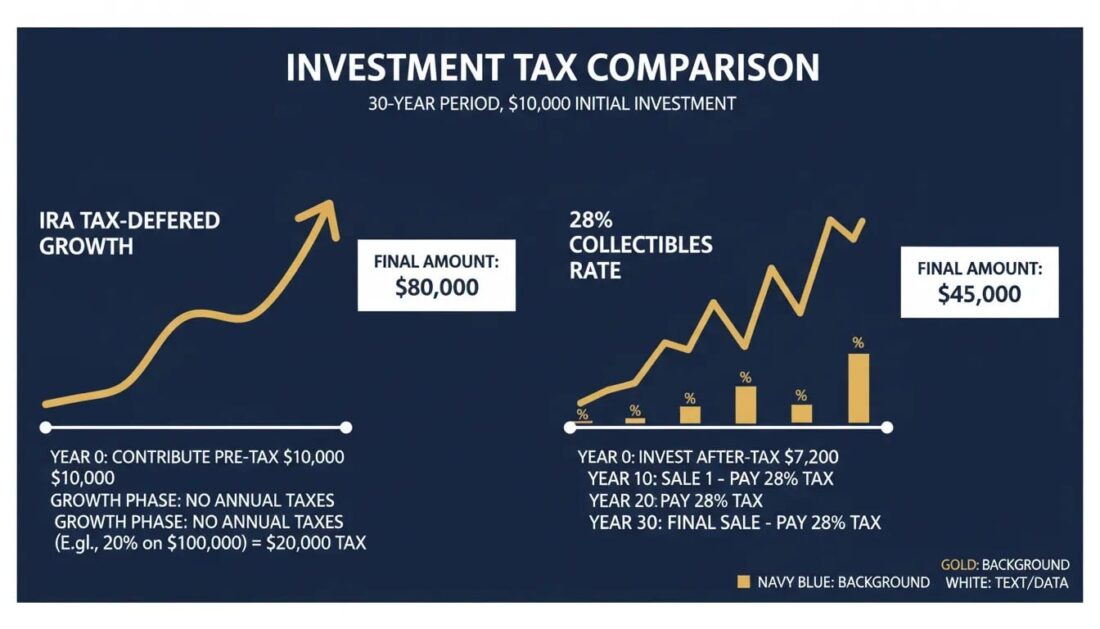

Tax Comparison Example

Imagine you purchase $50,000 in gold that appreciates to $100,000 over ten years—a $50,000 gain.

| Scenario | Tax Due on $50,000 Gain |

|---|---|

| Traditional Gold IRA | $0 now (taxed at withdrawal as ordinary income) |

| Roth Gold IRA | $0 now, $0 at qualified withdrawal |

| Direct Purchase (28% bracket) | $14,000 federal capital gains tax |

| Direct Purchase (24% bracket) | $12,000 federal capital gains tax |

The IRA defers or eliminates the tax entirely. The direct purchase triggers a substantial tax bill when you sell.

Does that mean direct purchases are wrong? Not at all—they offer benefits IRAs can’t match.

But from a pure tax perspective, IRAs provide a meaningful advantage for long-term gold holdings.

Storage and Custody: Your Options

Where your gold is stored—and who controls access—matters more than most people realize.

Gold IRA Storage Requirements

IRS rules require that Gold IRA assets be stored at an approved depository.

You cannot store IRA gold at home. Not in a safe deposit box. Not anywhere else—even if you have a secure facility.

This isn’t optional.

If you take physical possession of IRA gold without properly distributing it, the IRS treats it as a taxable distribution. You’d owe income taxes plus a 10% penalty if you’re under 59½.

Approved depositories offer two main options:

- Segregated storage — Your gold is stored separately, identified specifically as yours. Higher cost, but maximum traceability.

- Non-segregated (commingled) storage — Your gold is stored with other customers’ holdings of the same type. Lower cost while maintaining individual ownership records.

Both include comprehensive insurance and institutional-grade security. Most depositories are bonded, audited, and insured through Lloyd’s of London or similar carriers.

Storage fees typically run $100–$300 per year depending on the storage type and account size.

Direct Purchase Storage Options

When you buy gold directly, storage is entirely your choice.

- Home storage — Keep gold in a home safe or secure location. Maximum access, but you bear responsibility for security and insurance.

- Safe deposit box — Store gold at a bank or credit union. More secure than home storage, but limited access during non-business hours.

- Professional vault storage — Use a private depository for allocated storage. Similar security to IRA depositories, but without IRA restrictions.

The key difference: direct purchase storage is optional and flexible.

You can change your mind, move your gold, or take it home anytime. With an IRA, the depository requirement is fixed until you take a distribution.

Costs: What Will You Actually Pay?

Understanding true costs requires looking beyond the gold price itself.

Gold IRA Costs

Gold IRAs have ongoing fees that direct purchases don’t.

- Account setup fee — $50–$100 (one-time)

- Annual custodian/administration fee — $75–$300 per year

- Storage and insurance fee — $100–$300 per year

- Wire transfer fees — $25–$30 per transaction

All told, most customers pay $200–$600 annually to maintain a Gold IRA.

This doesn’t include the premium over spot price when purchasing gold—which applies to both IRAs and direct purchases.

The good news: many providers use flat-rate fees rather than percentage-based pricing. Whether your account holds $30,000 or $300,000, the annual fee stays the same.

Brighton offers a No Fee Precious Metals IRA that covers custodial fees for the lifetime of the account on qualified purchases—eliminating one of the main cost concerns. (Subject to minimum purchase requirements; ask your representative for details.)

Direct Purchase Costs

Direct purchases have minimal ongoing costs.

- No custodian fees

- No mandatory storage fees (unless you choose professional vault storage)

- No administrative costs

Your primary cost is the premium over spot price when you buy—typically 3–8% depending on the product.

If you choose professional vault storage, you’ll pay similar storage fees to an IRA depository. But home storage or safe deposit boxes have minimal cost beyond the initial safe or box rental.

Cost Comparison Over 10 Years

| Cost Factor | Gold IRA (10 years) | Direct Purchase (10 years) |

|---|---|---|

| Custodian/Admin Fees | $750–$3,000 | $0 |

| Storage Fees | $1,000–$3,000 | $0–$3,000 (optional vault) |

| Setup Fees | $50–$100 | $0 |

| Total Ongoing Costs | $1,800–$6,100 | $0–$3,000 |

The IRA’s ongoing costs are offset by tax advantages—but only if you hold long enough for tax deferral to compound.

For shorter time horizons, direct purchases may be more cost-effective.

Access and Liquidity: When Can You Use Your Gold?

One of the most important questions: how easily can you get to your gold when you need it?

Gold IRA Access Restrictions

Gold held in a traditional or Roth IRA is subject to retirement account rules.

- Penalty-free withdrawals begin at age 59½

- Early withdrawals (before 59½) trigger a 10% penalty plus income taxes

- RMDs must begin at age 73 for traditional IRAs (Roth IRAs have no RMDs during your lifetime)

You can take distributions two ways:

- Cash distribution — Sell gold within the IRA and withdraw cash

- In-kind distribution — Take physical delivery of the actual gold

Either way, the fair market value of the distribution is taxable as ordinary income (traditional IRA) or tax-free if qualified (Roth IRA).

Some customers satisfy RMDs from other accounts—leaving their gold holdings intact. Others prefer in-kind distributions to maintain physical ownership while meeting IRS requirements.

Direct Purchase Access

Direct purchases have no access restrictions.

Once you own the gold:

- Sell it anytime

- Gift it to family members

- Use it as collateral

- Take physical possession immediately

- Store it wherever you choose

There’s no waiting period, no penalties, and no required distributions.

This makes direct purchases particularly attractive for emergency reserves, gifts, inheritance planning, or customers who simply want gold outside the retirement system entirely.

Required Minimum Distributions and Gold IRAs

RMDs are a critical consideration for anyone with a traditional Gold IRA.

How RMDs Work with Gold

Starting at age 73, you must take annual distributions from traditional IRAs—including Gold IRAs.

The amount is calculated by dividing your December 31 account balance by an IRS life expectancy factor.

With a Gold IRA, you have two options:

- Cash distribution — The custodian sells enough gold to meet your RMD and distributes cash

- In-kind distribution — You receive physical gold equal to your RMD amount, shipped from the depository

Both are taxable as ordinary income. The in-kind option lets you maintain physical ownership while satisfying IRS requirements.

Penalty for missing RMDs: 25% of the amount you failed to withdraw. This can be reduced to 10% if you correct the error within two years.

Strategies for Managing Gold IRA RMDs

- Satisfy RMDs from other accounts — If you have multiple IRAs, you can aggregate RMDs and take them from any combination. Some customers take RMDs from traditional IRAs holding cash, leaving their Gold IRA intact.

- Roth conversion — Converting to a Roth IRA before age 73 eliminates future RMDs (though you’ll owe taxes on the conversion).

- Take in-kind distributions — If you want to maintain gold ownership, request physical delivery rather than liquidating.

- Qualified Charitable Distribution (QCD) — If you’re 70½ or older, you can donate up to $105,000 per year directly from your IRA to charity. This counts toward your RMD and isn’t included in taxable income.

Roth Gold IRAs and RMDs

Roth Gold IRAs have no RMDs during your lifetime.

This is a major advantage for customers who don’t need the income in retirement and want to maximize tax-free growth.

The trade-off: Roth contributions are made with after-tax dollars, and income limits may restrict eligibility. But for those who qualify, the combination of tax-free growth and no RMDs makes Roth Gold IRAs compelling.

Legacy Planning: Passing Gold to Heirs

How you hold gold affects how it transfers to the next generation.

Inheriting a Gold IRA

When a Gold IRA owner passes away, the account transfers to named beneficiaries.

The rules depend on the relationship.

Spousal beneficiaries can treat the inherited IRA as their own, roll it into their existing IRA, or take distributions. They’re not required to take RMDs until they reach age 73.

Non-spouse beneficiaries (children, grandchildren, trusts) must generally withdraw the entire account within 10 years under the SECURE Act’s rules. The “stretch IRA” option that allowed lifetime distributions is largely gone.

The gold itself transfers seamlessly—beneficiaries can maintain the holdings, sell, or take in-kind distributions.

Inheriting Direct Purchase Gold

Gold purchased directly passes to heirs through your estate—by will, trust, or beneficiary designation.

Key advantages:

- Step-up in cost basis — Heirs receive a stepped-up basis equal to fair market value at death. If you bought gold at $1,500/oz and it’s worth $3,000/oz when you pass, your heirs’ basis is $3,000. They owe no capital gains on appreciation during your lifetime.

- No 10-year distribution requirement — Unlike inherited IRAs, there’s no IRS mandate to liquidate within a certain timeframe.

- Immediate access — Heirs can take physical possession, sell, or continue holding without restrictions.

For customers focused on leaving gold to the next generation, direct purchases with a step-up in basis can be more advantageous than inherited IRAs subject to 10-year distribution rules.

Which Approach Is Right for You?

There’s no universal answer. The right choice depends on your goals, timeline, and how you want to hold your gold.

Choose a Gold IRA If:

- You want to use existing retirement funds (401k, IRA, TSP) to acquire gold

- You’re focused on long-term retirement planning and don’t need short-term access

- Tax-deferred or tax-free growth is a priority

- You’re comfortable with custodian and storage requirements

- You want gold as part of your retirement picture

Choose Direct Purchases If:

- You want immediate physical possession and control

- You’re buying gold outside of retirement planning

- You want flexibility to sell, gift, or use gold at any time

- You prefer to avoid ongoing custodian fees

- Privacy and accessibility are priorities

Use Both If:

Many customers use a combination.

A Gold IRA provides tax-advantaged retirement savings with long-term growth potential. Direct purchases provide accessible liquidity and flexibility for near-term needs or legacy planning.

The approaches complement each other rather than compete.

Frequently Asked Questions

Can I hold physical gold in a regular IRA?

No. Regular IRAs held at most brokerages don’t allow physical gold.

You need a self-directed IRA with a custodian that specializes in precious metals. The gold must meet IRS purity requirements—99.5% for gold—and be stored at an approved depository.

What are the annual fees for a Gold IRA?

Most customers pay between $200 and $600 per year.

This includes custodian administration fees ($75–$300), storage fees ($100–$300 depending on segregated vs. non-segregated), and any transaction fees.

Brighton offers a No Fee Precious Metals IRA that covers custodial fees for the lifetime of the account on qualified purchases.

How is physical gold taxed when I sell it?

Physical gold is classified as a collectible by the IRS.

Long-term capital gains are taxed at your ordinary income rate, capped at a maximum of 28%. Short-term gains (held less than one year) are taxed as ordinary income at your marginal rate.

This is higher than the 20% maximum rate for other long-term capital gains—one reason IRAs are attractive for gold holdings.

Can I take physical delivery of gold from my IRA?

Yes, but it triggers a taxable distribution.

When you take physical delivery, the fair market value of the gold is treated as a withdrawal. You’ll owe income taxes, and if you’re under 59½, a 10% early withdrawal penalty may apply.

Some customers take in-kind distributions to satisfy RMDs, receiving physical gold while meeting IRS requirements.

What happens to my Gold IRA when I reach RMD age?

At age 73, you must begin taking Required Minimum Distributions from a traditional Gold IRA.

You can satisfy RMDs by selling gold and taking cash, or by taking an in-kind distribution of physical gold. Either way, the distribution is taxable as ordinary income.

Roth Gold IRAs have no RMDs during your lifetime.

Is a Roth Gold IRA better than a traditional Gold IRA?

It depends on your tax situation.

A Roth Gold IRA uses after-tax dollars, but qualified withdrawals are tax-free—including any appreciation. Roth IRAs also have no RMDs during your lifetime. However, income limits apply to Roth contributions.

If you expect higher taxes in retirement or want to avoid RMDs, Roth may be preferable. If you want an upfront tax deduction and expect lower taxes later, traditional may be better.

How quickly can I access my gold if I buy direct?

With a direct purchase, you typically receive delivery within 1–3 weeks depending on the product and shipping method.

Once delivered, the gold is yours with no restrictions on access, sale, or use.

Can I use both a Gold IRA and buy gold directly?

Absolutely.

Many customers use both approaches. A Gold IRA provides tax-advantaged retirement savings, while direct purchases offer immediate access and flexibility.

The combination gives you both long-term protection and short-term liquidity.

Making Your Decision

The Gold IRA vs. direct purchase question isn’t about finding the “better” option.

It’s about matching your approach to your goals.

Gold IRAs excel at protecting retirement savings with tax advantages—especially for customers rolling over existing 401(k) or IRA funds into physical gold.

Direct purchases excel at providing accessible, flexible gold ownership without the restrictions of retirement accounts.

Both put real, tangible gold in your hands. Just with different timelines and tax treatment.

Ready to explore your options?

If you’re thinking “this all makes sense, but I don’t have time to figure it out on my own,” you’re not alone. Most customers we work with felt the same way before they realized how straightforward the process can be with the right guidance.

That’s why we offer a complimentary consultation to walk you through your options—including our No Fee Precious Metals IRA, which covers custodial fees for the lifetime of the account on qualified purchases.

We’ll show you exactly:

- How the No Fee IRA works and whether you qualify

- The difference between U.S.-minted coins and foreign alternatives

- What to expect from the purchasing and delivery process

- How to roll over or transfer existing retirement funds

- What ongoing support looks like after your purchase

Learn About the No Fee IRA — no obligation, just actionable insights you can use whether you work with us or not.

Whether you’re leaning toward an IRA, direct purchases, or both—Brighton can help you get clear answers and move forward with confidence.