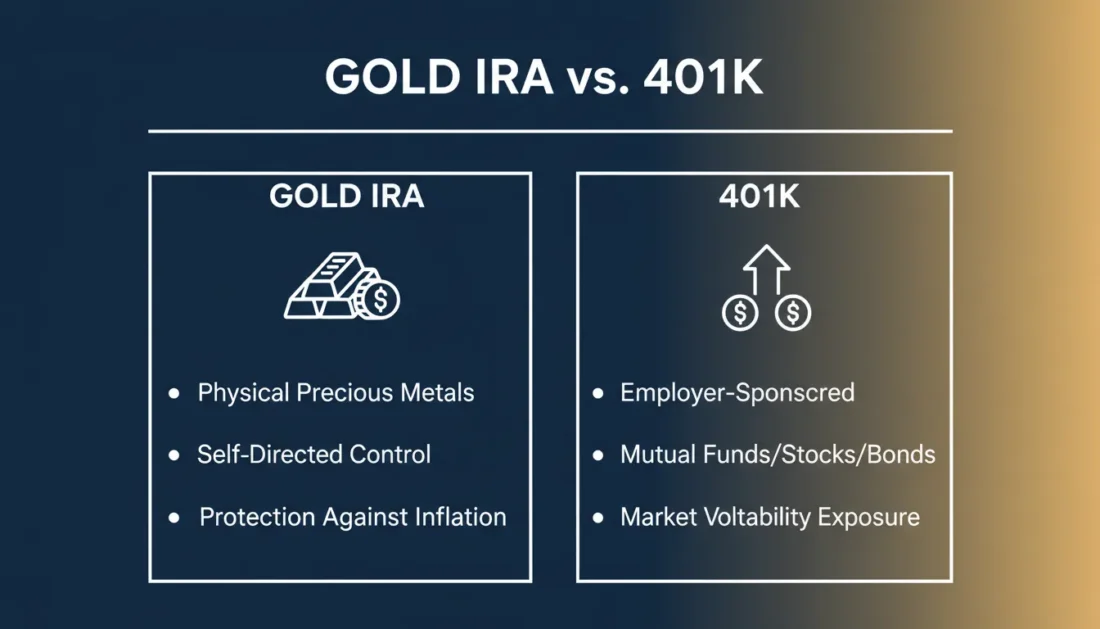

Here’s the short version: a Gold IRA lets you hold physical precious metals—actual gold and silver bars and coins—inside a retirement account. A 401(k) limits you to paper assets like stocks, bonds, and mutual funds.

Both offer tax advantages. But only one gives you direct ownership of something tangible.

If you’ve spent years building your retirement through a 401(k), you’re not alone. Millions of Americans have their entire nest egg tied up in paper promises—shares in companies, fund units, electronic entries on a statement.

There’s nothing wrong with that approach. But it does leave you exposed to risks that physical gold was designed to address.

The question isn’t whether one is “better.” It’s whether you understand the trade-offs—and whether you have the option to hold something real.

A self-directed Gold IRA doesn’t replace your 401(k). For many of our customers, it complements it. It adds a layer of protection that paper assets simply can’t provide.

If you’re considering opening a self-directed gold IRA, this comparison will help you see exactly what you’re getting with each option.

Let’s walk through it together.

What Is a 401(k) and How Does It Work?

A 401(k) is an employer-sponsored retirement savings plan. You contribute a portion of your paycheck—before taxes, in most cases—and the money goes into an account managed by a custodian your employer selected.

Most plans offer a menu of mutual funds, target-date funds, and sometimes company stock. You pick from that menu. The custodian handles everything else.

The Contribution Limits for 2026

The IRS announced that the 2026 contribution limit for 401(k) plans is $24,500—up from $23,500 in 2025. Fidelity’s breakdown of the new limits shows how catch-up contributions work for different age groups.

If you’re 50 or older, you can add a catch-up contribution of $8,000. That brings your total to $32,500.

And here’s something new: if you’re between 60 and 63, a “super catch-up” provision lets you contribute up to $11,250 instead of the standard $8,000. That means you could put away as much as $35,750 in 2026.

Employers can also contribute. The combined limit for employee and employer contributions is $72,000.

The Advantages of a 401(k)

- Employer matching — Many employers match a percentage of your contributions. That’s essentially free money toward retirement.

- Automatic payroll deductions — Contributions happen without you having to think about it.

- Tax-deferred growth — You don’t pay taxes on gains until you withdraw funds in retirement.

- High contribution limits — The $24,500 limit is significantly higher than traditional IRA limits.

The Limitations Worth Understanding

Here’s what a 401(k) doesn’t offer: control over the actual assets.

You’re limited to whatever options your plan administrator provides. You can’t hold physical gold. You can’t hold real estate. You can’t hold individual stocks in most cases.

You’re choosing from a pre-selected menu—and that menu is made up entirely of paper assets.

Your 401(k) balance is also tied to market performance. When markets drop, your balance drops. There’s no floor, no tangible backing, no physical asset you can point to and say, “That’s mine.”

And while the tax advantages are real, they come with strings. Early withdrawals before 59½ typically trigger a 10% penalty plus income taxes. Required Minimum Distributions start at 73, whether you need the money or not.

What Is a Gold IRA and How Does It Differ?

A Gold IRA is a self-directed Individual Retirement Account that holds physical precious metals instead of—or alongside—paper assets.

It’s called “self-directed” because you choose the specific assets, rather than picking from a limited menu.

The mechanics are similar to a traditional IRA. Contributions may be tax-deductible. Growth is tax-deferred. Withdrawals in retirement are taxed as ordinary income.

The difference? What’s inside the account: actual gold bars and coins, stored in an IRS-approved depository.

If you’re curious about the full mechanics, our guide on establishing a precious metals IRA walks through the process step by step.

How Gold IRA Contribution Limits Compare

For 2026, the IRA contribution limit is $7,500—up from $7,000 in 2025. If you’re 50 or older, you can add a catch-up of $1,100, bringing your total to $8,600.

That’s significantly lower than 401(k) limits.

But here’s what most people don’t realize: rollovers don’t count against contribution limits.

Got $200,000 sitting in an old 401(k)? You can roll the entire amount into a Gold IRA without affecting your annual contribution allowance.

That’s how many of our customers fund their precious metals accounts—not through annual contributions, but through penalty-free rollovers from existing accounts.

What You Actually Own in a Gold IRA

This is the part that surprises people.

When you buy gold inside a Gold IRA, you’re buying actual physical metal. Real coins. Real bars. Stored in a vault with your name on the account.

It’s not a gold ETF. It’s not shares in a mining company. It’s not a paper claim on gold stored somewhere else.

You own the metal itself.

The IRS requires gold held in an IRA to meet specific purity standards—generally 99.5% for gold bars and most coins. American Gold Eagles, despite containing 91.67% gold, are specifically approved. American Gold Buffalos, Canadian Gold Maple Leafs, and bars from accredited refiners like PAMP Suisse or the Royal Canadian Mint also qualify.

The metals must be stored in an IRS-approved depository. You can’t keep IRA gold at home—that would trigger a distribution and potential penalties.

Gold IRA vs. 401(k): A Side-by-Side Comparison

Let’s put the key differences in perspective.

| Feature | Traditional 401(k) | Self-Directed Gold IRA |

|---|---|---|

| Asset Type | Stocks, bonds, mutual funds (paper assets) | Physical gold, silver, platinum, palladium |

| Control | Limited to plan menu | You select specific metals |

| Contribution Limit (2026) | $24,500 ($32,500 with catch-up) | $7,500 ($8,600 with catch-up) |

| Employer Match | Often available | Not applicable |

| Rollover Eligible | Yes—to IRA or Gold IRA | Yes—from 401(k), IRA, TSP, 403(b) |

| Tangible Asset | No | Yes—you own physical metal |

| Market Correlation | High (tied to stock/bond markets) | Low (gold often moves independently) |

| Custodian | Selected by employer | You choose |

| Storage | Electronic/digital entries | IRS-approved depository |

| RMDs at Age 73 | Yes | Yes |

The table tells part of the story. But the real difference shows up during periods of stress.

When Paper Assets and Physical Assets Behave Differently

In 2008, the S&P 500 lost roughly 37%. Gold finished the year up 5%.

In 2020, when markets swung wildly during the early pandemic months, gold climbed steadily to what was then an all-time high.

And in 2025? Gold rose approximately 67%—one of its strongest years in decades—while traditional equities posted more modest gains amid inflation concerns and geopolitical uncertainty.

Gold doesn’t always outperform. But it often moves in the opposite direction from paper assets.

That’s precisely why many of our customers view it as a counterbalance—not a replacement—for traditional retirement accounts.

As of late January 2026, gold has continued climbing. Trading Economics reported gold rose above $5,000 per ounce, driven by safe-haven demand amid trade tensions and ongoing central bank purchases.

That’s a significant shift from just two years ago, when gold was trading around $2,000.

Why People Move from 401(k) to Gold IRA

Not everyone needs or wants a Gold IRA. But for those who do, the motivations tend to fall into a few categories.

Concern About Dollar Purchasing Power

When the currency loses value, the prices of everyday goods go up. That’s inflation.

A 401(k) full of dollar-denominated assets doesn’t protect against that. If your balance stays flat while prices rise, your purchasing power shrinks.

Gold, by contrast, has maintained purchasing power across centuries.

An ounce of gold in 1920 bought roughly the same amount of goods as an ounce today—measured in real terms. You can’t say that about the dollar.

Desire for Tangible Assets

Paper assets exist as entries in a database. They depend on counterparties—companies, fund managers, custodians, exchanges—to honor their obligations.

Physical gold doesn’t carry counterparty risk in the same way.

If you own a Gold American Eagle stored in a depository, that coin exists regardless of what happens to any particular company or financial institution.

For customers who’ve watched banking instability, account freezes, or fund blowups in recent years, that distinction matters.

Central Bank Behavior as a Signal

Here’s something worth paying attention to: central banks worldwide have been accumulating gold at historic rates.

According to J.P. Morgan Global Research, central bank gold purchases exceeded 1,000 tonnes annually from 2022 through 2024—more than double the pre-2022 average. Even in 2025, with gold at record prices, purchasing continued.

The World Gold Council reported net central bank purchases of 45 tonnes in November 2025 alone, bringing year-to-date totals to 297 tonnes. Poland, Brazil, China, and other nations continued adding to their reserves.

When the institutions that print money are buying gold, it raises a fair question: what do they know about the future of paper currency?

The Rollover Process: How to Move 401(k) Funds to a Gold IRA

This is where people often hesitate. The process sounds complicated.

It isn’t.

The IRS allows penalty-free rollovers from 401(k) plans into IRAs—including self-directed Gold IRAs. The key is doing it correctly: using a direct rollover (also called a trustee-to-trustee transfer) so the funds never pass through your hands.

Here’s how it works.

Step 1: Open a Self-Directed IRA

You’ll need an IRA custodian that specializes in precious metals. Not all custodians support physical gold—most traditional brokerages don’t.

A reputable precious metals company can help you identify an approved custodian and handle the paperwork. The account setup typically takes a few days.

Step 2: Request a Direct Rollover from Your 401(k)

Contact your current 401(k) plan administrator. Tell them you want to initiate a direct rollover to a self-directed IRA.

The administrator will send the funds directly to your new IRA custodian. Because the money moves between custodians without you touching it, there’s no tax withholding and no risk of missing the 60-day deadline that applies to indirect rollovers.

According to IRS guidance, direct rollovers are the safest method. No taxes are withheld, and the transfer maintains the tax-advantaged status of your retirement funds.

Step 3: Select Your Precious Metals

Once the funds arrive in your Gold IRA, you’ll work with an authorized precious metals dealer to select IRS-approved products.

Popular choices include American Gold Eagles, American Gold Buffalos, and gold bars from accredited refiners.

If you’re interested in acquiring U.S.-minted gold coins, these are among the most recognized and liquid options available.

You can also add silver to your Gold IRA for additional diversification within the precious metals space.

Step 4: Storage at an Approved Depository

Your metals ship to an IRS-approved depository—facilities like Brink’s Global Services, Delaware Depository, or similar institutions that meet federal security and insurance requirements.

You’ll choose between segregated or non-segregated storage. Segregated storage keeps your metals separate from other customers’ holdings. Non-segregated is typically less expensive but means your metals are commingled with others of the same type and quality.

Timeline and What to Expect

Most of our customers complete the entire rollover process in two weeks or less.

Our guide on executing a precious metals IRA rollover walks through the timeline in detail.

The critical point: this isn’t a taxable event when done correctly. Your retirement funds maintain their tax-advantaged status while transitioning from paper assets to physical precious metals.

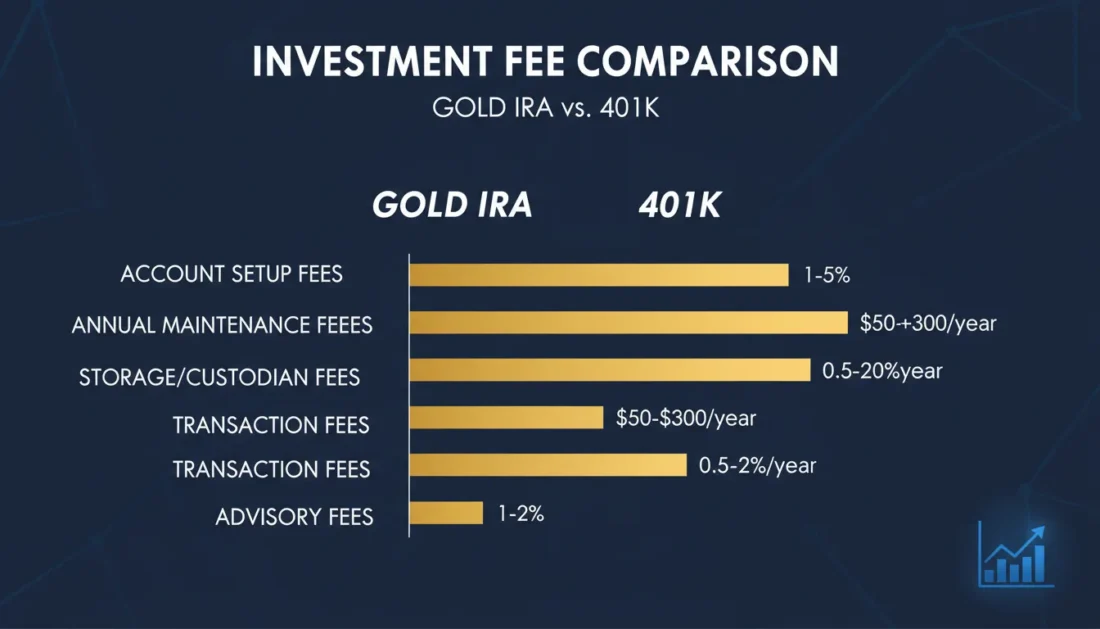

Understanding the Fees: Gold IRA vs. 401(k) Costs

Both account types have costs. The structures are different, and understanding them helps you make a confident decision.

401(k) Fee Structure

401(k) costs are often hidden inside fund expense ratios.

A mutual fund with a 1% expense ratio charges $1,000 per year on a $100,000 balance—but you never see a line item for it. It’s simply deducted from fund performance.

Administrative fees, record-keeping fees, and management fees may also apply. The Department of Labor requires fee disclosure, but the information isn’t always easy to interpret.

Over a 20-year period, a 1% annual fee can reduce your ending balance by 20% or more compared to a lower-cost alternative. That’s the power of compounding working against you.

Gold IRA Fee Structure

Gold IRA fees are typically more transparent. You’ll see:

- Setup fees — Often $50–$100, one-time

- Annual custodian fees — Typically $75–$300, depending on the provider

- Storage fees — $100–$300 annually at most depositories

- Transaction fees — May apply when buying or selling metals

Some precious metals companies structure their offerings to minimize or eliminate custodian fees.

Brighton Gold, for example, offers a No Fee Precious Metals IRA that covers custodial fees for the lifetime of the account on qualified purchases.

| Fee Type | Traditional 401(k) | Self-Directed Gold IRA |

|---|---|---|

| Management/Expense Ratios | 0.5%–2.0% annually | Not applicable |

| Setup Fee | Usually none | $50–$100 (one-time) |

| Annual Custodian Fee | Built into fund costs | $75–$300 (or waived) |

| Storage Fee | Not applicable | $100–$300 annually |

| Transaction Costs | May apply | May apply |

The comparison isn’t apples to apples because you’re holding fundamentally different assets. But knowing both fee structures helps you plan with clarity and control.

How Much Gold Should You Hold?

There’s no universal answer. It depends on your goals, your timeline, and your comfort level with different types of risk.

Some financial professionals suggest precious metals should represent 5–10% of a retirement strategy. Others go higher—particularly for customers closer to retirement who prioritize stability over growth.

Our guide on determining gold allocation for retirement explores the considerations in depth.

A few principles to keep in mind:

Start with your goals, not a percentage. Are you looking to preserve purchasing power? Reduce exposure to market swings? Create something tangible to pass to the next generation? Different goals suggest different approaches.

Consider your timeline. A 35-year-old with decades until retirement has different needs than a 62-year-old planning to retire in three years.

Think about what you already own. If your entire retirement savings is in a 401(k) full of stock-based mutual funds, even a modest allocation to physical metals adds meaningful diversification.

For deeper context on why customers choose precious metals, our overview of the benefits of physical gold ownership provides additional perspective.

What the IRS Requires for Gold IRAs

The IRS has specific rules about what can—and can’t—go into a Gold IRA. Understanding these helps you avoid costly mistakes.

Purity Requirements

Gold held in an IRA must meet a minimum fineness of 99.5% (0.995). Silver must be 99.9% pure. Platinum and palladium must be 99.95% pure.

The one exception: American Gold Eagles, which contain 91.67% gold (22 karat), are specifically approved despite not meeting the 99.5% threshold. The IRS carved out this exception because of the coin’s status as official U.S. legal tender.

Approved Products

Eligible gold products include:

- American Gold Eagles (all sizes)

- American Gold Buffalos

- Canadian Gold Maple Leafs

- Austrian Gold Philharmonics

- Australian Gold Kangaroos

- Gold bars from COMEX/NYMEX-approved refiners meeting purity standards

Collectible coins, numismatic coins, jewelry, and gold that doesn’t meet purity requirements aren’t permitted. The IRS treats these as collectibles, which are specifically excluded from IRA holdings.

Storage Requirements

Physical precious metals in an IRA must be stored at an IRS-approved depository.

You can’t store IRA gold at home, in a personal safe deposit box, or anywhere not approved for this purpose.

If you take possession of IRA metals—even briefly—the IRS treats it as a distribution. That means potential taxes and, if you’re under 59½, a 10% early withdrawal penalty.

This isn’t as restrictive as it sounds. Approved depositories offer robust security, insurance, and regular auditing. Your metals are safer there than in most home storage options.

Frequently Asked Questions

Can I move my 401(k) into a Gold IRA while still employed?

It depends on your plan.

Many 401(k)s restrict in-service rollovers while you’re still working and under 59½. Some plans do allow partial rollovers.

Check with your plan administrator. If yours doesn’t permit it, you may need to wait until you change jobs or retire.

What is the penalty for rolling over a 401(k) into physical gold?

Done correctly through a direct rollover, there’s no penalty.

The key is a trustee-to-trustee transfer—funds move directly from your 401(k) custodian to your Gold IRA custodian without passing through your hands.

Miss the 60-day window on an indirect rollover, and you could face income taxes plus a 10% early withdrawal penalty if you’re under 59½.

Is a Gold IRA safer than a traditional 401(k)?

It depends on what concerns you most.

A Gold IRA holds physical metals—protection against currency devaluation without the counterparty risk of paper assets. A 401(k) holds stocks, bonds, and mutual funds—subject to market swings.

Gold has historically held purchasing power during inflation and uncertainty. That said, precious metals may appreciate, depreciate, or stay flat.

Neither is inherently “safer.” They protect against different risks.

Can I have both a 401(k) and a Gold IRA at the same time?

Absolutely.

Many people keep their employer 401(k) to capture matching contributions while also holding a separate Gold IRA.

This lets you build savings through your workplace plan and hold tangible assets outside the traditional financial system. Just remember each account has its own contribution limits.

What are the fees for a Gold IRA compared to 401(k) administrative costs?

Gold IRAs typically have setup fees ($50–$100), annual custodian fees ($75–$300), and storage fees ($100–$300 yearly).

Some companies—like Brighton Gold—offer no-fee structures on qualified purchases covering custodial fees for the lifetime of the account.

Traditional 401(k)s often have expense ratios (0.5%–2% annually) plus administrative fees buried in fund costs. Total cost depends on account size and fee structures.

How do I start a penalty-free rollover into precious metals?

Four steps:

Open a self-directed IRA with a custodian that supports physical metals. Contact your 401(k) administrator to request a direct rollover. Once funds arrive, work with an authorized dealer to select IRS-approved gold or silver. The metals ship to an IRS-approved depository and are stored in your name.

Most people complete this in two weeks or less.

What types of gold are allowed in a Gold IRA?

Gold must meet 99.5% purity minimum—with one exception: American Gold Eagles (91.67% gold) are specifically IRS-approved.

Acceptable products include American Gold Eagles, American Gold Buffalos, Canadian Gold Maple Leafs, Austrian Gold Philharmonics, and gold bars from COMEX/NYMEX-approved refiners.

Collectibles, jewelry, and gold below purity standards aren’t permitted.

What happens to my Gold IRA when I reach retirement age?

You’ve got options.

Take cash distributions—your custodian sells the metals and sends funds. Or request physical delivery of your actual metals (this triggers a distribution with tax implications).

At 73, Required Minimum Distributions begin, same as traditional IRAs. Plan ahead for liquidity—selling physical metals takes longer than liquidating paper assets.

Making the Right Choice for Your Situation

The choice between a 401(k) and a Gold IRA isn’t either/or for most people.

It’s about understanding what each option offers—and crafting a retirement strategy that reflects your actual goals.

A 401(k) offers high contribution limits, potential employer matching, and the convenience of automatic payroll deductions. For many working Americans, it’s the foundation of retirement savings.

A Gold IRA offers something different: direct ownership of physical precious metals, protection against currency devaluation, and an asset that has maintained value across centuries of uncertainty.

The strongest approach for many of our customers combines both.

Continue capturing employer matching through your workplace plan while also holding tangible assets in a self-directed Gold IRA.

Precious metals may appreciate, depreciate, or remain unchanged in value. But they offer something paper assets can’t: true ownership of something real—and the peace of mind that comes with it.

If you’re thinking “this all makes sense, but I don’t have time to figure it out on my own,” you’re not alone. Most of the customers we work with felt the same way before they realized how seamless the process can be with the right guidance.

That’s why we offer a complimentary consultation to walk you through your options—including our No Fee Precious Metals IRA, which covers custodial fees for the lifetime of the account on qualified purchases.

We’ll show you exactly:

- How the No Fee IRA works and whether you qualify

- The difference between U.S.-minted coins and foreign alternatives

- What to expect from the purchasing and delivery process

- How to roll over or transfer existing retirement funds

- What ongoing support looks like after your purchase

Learn About the No Fee IRA—no obligation, just clarity and control over what comes next.

Your retirement is too important to leave entirely in paper promises. Understanding your options is the first step toward securing something more tangible.