Here’s the short answer: no, you can’t.

And I know that’s frustrating to hear—especially if you’ve spent years building a personal gold collection. You’re looking at those American Eagles in your safe, thinking, “Why can’t I just move these into my retirement account?”

The IRS calls it a “prohibited transaction.” And the consequences aren’t a slap on the wrist. We’re talking about your entire IRA getting disqualified. Every dollar in that account—taxable. If you’re under 59½? Add a 10% penalty on top.

But here’s the good news.

There’s a clear, compliant path to holding physical gold in a tax-advantaged retirement account. It just doesn’t involve transferring gold you already own.

Let’s walk through why the rules work this way—and what you can actually do to get the peace of mind that comes with owning real, tangible gold inside your IRA.

Why Can’t I Transfer My Personal Gold Into an IRA?

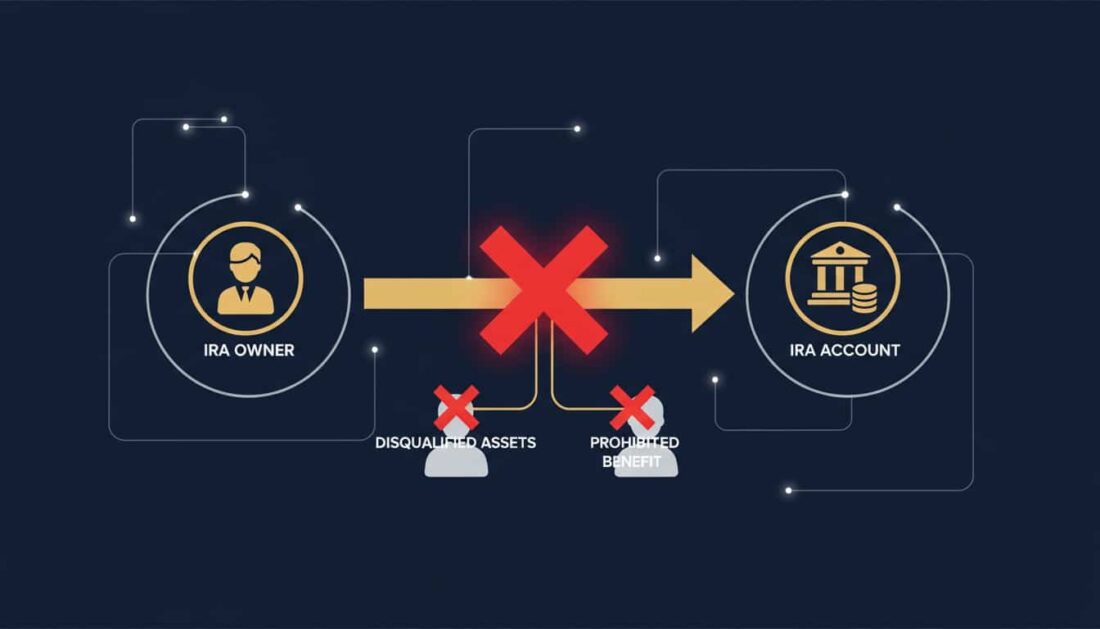

It comes down to one word: self-dealing.

The IRS doesn’t want you using your retirement account to benefit yourself today. That’s the whole point of Internal Revenue Code Section 4975—preventing tax abuse.

Think about it this way. Say you bought gold at $500 an ounce ten years ago. Now it’s worth $2,000. If you could simply transfer it into your IRA? You’d shelter all that appreciation from taxes—without ever using retirement funds to make the purchase.

Congress closed that loophole decades ago.

What Exactly Is a Prohibited Transaction?

The IRS defines prohibited transactions as certain dealings between your IRA and “disqualified persons.”

Who’s disqualified? You are. So is your spouse. Your parents. Your kids. Their spouses.

Here’s what you can’t do:

- Sell property to your IRA — Even at fair market value

- Buy property from your IRA — Same rule, opposite direction

- Lend money to or from your IRA — No exceptions

- Use IRA assets for personal benefit — Even temporarily

The price doesn’t matter. The IRS cares about the relationship—not whether the deal was “fair.”

But My Gold Already Qualifies for an IRA…

This is where folks get tripped up.

Yes, IRS Publication 590-A allows IRAs to hold certain gold products. American Eagles. Canadian Maple Leafs. Bars meeting 99.5% purity.

But that exception applies to what the IRA can buy—not from whom.

Your IRA can purchase qualifying gold from an authorized dealer. It cannot purchase gold from you. Those are two completely different things under the tax code.

Even if you own the exact same coin an IRA could legally acquire? The moment you sell it to your own account, you’ve crossed the line.

What Happens If You Break the Rules?

![]()

Let me be direct with you—the penalties are severe.

Your Entire IRA Gets Disqualified

If you engage in a prohibited transaction, the IRS treats your whole account as distributed. Not just the gold you transferred. Everything.

Picture this. You have $200,000 in your Precious Metals IRA. In March, you move $30,000 worth of personal gold coins into the account.

The IRS doesn’t penalize just the $30,000. They disqualify the entire $200,000—effective January 1st of that year.

That’s $200,000 of taxable income. In one year. Plus the 10% early withdrawal penalty if you’re under 59½.

We’ve seen people lose $60,000 or more to taxes and penalties from a single mistake.

The McNulty Case: A $300,000 Lesson

Want to know how serious the IRS is about these rules?

In 2021, a couple named the McNultys learned the hard way. They used their self-directed IRAs to buy American Eagle coins through an LLC—then stored them in a safe at home.

The Tax Court ruled against them. The result? Nearly $270,000 in taxes on about $730,000 of IRA assets. Plus penalties exceeding $50,000.

The court called home storage schemes “questionable internet schemes.”

Their entire retirement? Essentially wiped out.

The Penalty Structure

| What Happens | The Consequence |

|---|---|

| Initial violation | 15% excise tax on the transaction amount |

| Failure to correct | Jumps to 100% excise tax |

| IRA disqualification | Entire account balance becomes taxable income |

| Under age 59½ | Additional 10% early withdrawal penalty |

These aren’t theoretical numbers. They’re what people actually pay when they try to work around the rules.

The Right Way to Get Gold Into Your IRA

Now for the good news. Getting physical gold into a tax-advantaged retirement account is straightforward—once you know the process.

Step 1: Open a Self-Directed IRA

Standard IRAs at big brokerages don’t allow physical gold. You’ll need a self-directed IRA with a custodian who specializes in precious metals.

The custodian handles the paperwork—account setup, IRS reporting, coordinating with depositories. They ensure everything stays compliant so you don’t have to worry about it.

That’s the kind of support that gives you clarity and control over your retirement.

Step 2: Fund the Account (Not With Gold—With Cash or Rollovers)

Here’s the key. You’re funding your IRA with money—not with gold you already own.

You have three compliant options:

- Direct Rollover — Funds move straight from your 401(k) or existing IRA to your new self-directed IRA. The money never touches your hands. No taxes. No penalties. For more on rolling over retirement funds to gold, the process is simpler than most people expect.

- Trustee-to-Trustee Transfer — Similar concept for moving funds between IRAs. One custodian sends the money directly to another. Clean and simple.

- Cash Contribution — You can contribute new money up to annual limits ($7,500 for 2026, or $8,600 if you’re 50+).

The entire process for executing a penalty-free 401k rollover typically takes two to four weeks.

Step 3: Purchase IRS-Approved Metals

Once your account is funded, your custodian facilitates the purchase from an authorized dealer.

The dealer ships the gold directly to an IRS-approved depository.

At no point do you take personal possession. That’s what keeps everything compliant—and keeps your retirement protected.

| Funding Method | Taxes? | Deadline? | How It Works |

|---|---|---|---|

| Direct Rollover | None | No deadline | Custodian-to-custodian transfer |

| Trustee-to-Trustee Transfer | None | No deadline | IRA-to-IRA transfer |

| Indirect Rollover | Risk of taxes | 60 days to redeposit | You receive and redeposit funds |

| Cash Contribution | May be deductible | Tax filing deadline | New money into the account |

What Gold Can Actually Go Into an IRA?

Not all gold qualifies—even when purchased the right way.

Purity Requirements

Under IRC Section 408(m)(3), gold must be at least 99.5% pure to go into an IRA.

There’s one exception. American Gold Eagles are only 91.67% pure—but they’re specifically exempted because they’re U.S. legal tender.

Silver must be 99.9% pure. Platinum and palladium? 99.95%.

What Products Qualify?

When choosing IRS-approved gold coins, these are your main options:

- American Gold Eagle — The most popular choice. U.S. Mint. Special purity exemption.

- American Gold Buffalo — 24 karat, 99.99% pure. Also U.S. Mint.

- Canadian Gold Maple Leaf — Royal Canadian Mint. 99.99% pure.

- Austrian Gold Philharmonic — 99.99% pure.

- Australian Gold Kangaroo — Perth Mint. 99.99% pure.

- Gold bars — Must be 99.5%+ pure from approved refiners.

For details on acquiring U.S.-minted gold coins, the American Eagle remains the most recognized option.

What Doesn’t Qualify?

These can’t go into an IRA—no matter how you acquire them:

- Collectible or numismatic coins

- Jewelry

- Foreign coins below purity standards

- Privately minted items without proper certification

- Any gold you personally own (the self-dealing rule)

That last point bears repeating. Even if you own American Eagles that would otherwise qualify? You can’t transfer them from your possession into your IRA.

Why Can’t I Store IRA Gold at Home?

This trips people up almost as often as the self-dealing rules.

The Third-Party Custody Requirement

The IRS is clear about this: precious metals in an IRA must be held by an approved trustee or depository.

Not in your safe. Not in a safety deposit box. Not in any place you control.

Those “home storage IRA” schemes you see advertised online? The McNulty case crushed that argument. The Tax Court ruled that personal possession—regardless of the legal structure—triggers distribution treatment.

How Depository Storage Works

When your IRA purchases gold, the dealer ships it directly to an IRS-approved depository.

The depository stores the metals in secure vaults. They’re insured. They report holdings to your custodian. You can verify your holdings anytime.

You have two main options:

- Segregated Storage — Your metals are stored separately. You get back the exact coins or bars you bought. Fees typically run $150–$300 per year.

- Non-Segregated Storage — Your metals are pooled with similar products from other customers. You receive equivalent metals when you distribute. Fees run $100–$250 per year.

For the full picture on understanding gold IRA fee structures, storage is one part of the cost equation.

Reputable Depositories

| Depository | Location | Insurance | What They Offer |

|---|---|---|---|

| Delaware Depository | Wilmington, DE & Boulder City, NV | $1 billion Lloyd’s coverage | Segregated and non-segregated |

| Brink’s Global Services | Multiple U.S. locations | Lloyd’s of London | Both storage types |

| International Depository Services | Dallas, TX & Delaware | Comprehensive coverage | Segregated and allocated |

| Texas Precious Metals Depository | Shiner, TX | Lloyd’s of London | Segregated only |

Your custodian will have relationships with approved depositories. The metals stay there until you’re eligible for distributions—at which point you can take physical delivery or liquidate for cash.

So What Do I Do With Gold I Already Own?

You’re not out of options. The gold just can’t go directly into your IRA.

Option 1: Sell Your Personal Gold Separately

You can sell your existing gold to a dealer. That cash becomes yours—do whatever you want with it.

Separately, fund your IRA through a rollover or contribution. Let the IRA purchase gold from an authorized dealer.

Two independent transactions. No prohibited transaction. No problems.

This makes sense if you want to:

- Liquidate older gold that doesn’t meet IRA purity standards

- Consolidate scattered holdings

- Lock in current prices on your personal collection

Option 2: Keep Both—Personal Gold and IRA Gold

Many people maintain two separate holdings:

- Personal Gold — Stored at home or in a private vault. Accessible whenever you want. No IRS reporting.

- IRA Gold — Tax-advantaged growth. Custodian-controlled. Accessible at retirement.

Each serves a different purpose.

Personal gold gives you immediate access and privacy. IRA gold gives you tax benefits and grows within a retirement framework.

For more on the process for precious metals transactions outside retirement accounts, the flexibility is greater—though you lose the tax advantages.

Option 3: Consider Silver for Diversification

If you’re funding a new Precious Metals IRA, you might diversify across both gold and silver.

Silver has a lower entry point per ounce. When selecting top silver bullion coins for an IRA, the same rules apply—99.9% purity, purchased through the IRA, stored at an approved depository.

Common Misconceptions That Get People in Trouble

Let me clear up some persistent myths—because these misunderstandings cost people real money.

“My Gold Already Meets IRA Standards, So I Can Transfer It”

Nope.

The purity of your gold has nothing to do with the self-dealing prohibition. You could own 99.99% pure Gold Buffalos—the exact product an IRA would buy—and still be prohibited from moving them into your account.

The rule focuses on who’s involved, not what’s being sold.

“I Can Use an LLC to Get Around the Rules”

Also no.

Some promoters sell “checkbook IRAs” or “LLC IRAs” that supposedly let you maintain control over IRA assets.

The McNulty case demolished this argument. The court ruled that taking physical possession—even through an LLC—triggers a taxable distribution.

The IRS has never bought these arguments. Courts haven’t either.

“Home Storage Gold IRAs Are Legal”

They’re not.

Despite what some ads claim, the IRS has never approved home storage for IRA metals. The custody rules are explicit.

Storing IRA gold at home doesn’t just risk disqualification—it guarantees it.

“I Can Sell My IRA Gold Back to Myself”

The prohibited transaction rules work both directions.

You can’t sell to your IRA. You can’t buy from your IRA either.

If you want physical possession of your metals, you take a distribution. That distribution is taxable (unless it’s from a Roth and you meet the requirements).

After the distribution, the gold is yours. But while it’s in the IRA? You can’t personally transact with it.

The Clear Path Forward

Let’s bring this together. Here’s the straightforward path to getting physical gold into your retirement account.

If You Have an Existing Retirement Account

Most people start here—with a 401(k), 403(b), TSP, or traditional IRA.

The process:

- Choose a self-directed IRA custodian specializing in precious metals

- Complete the application

- Request a direct rollover from your existing account

- Once funded, direct the custodian to purchase IRS-approved metals

- Metals ship to an approved depository

Two to four weeks. Tax-free if done as a direct transfer. Peace of mind knowing everything is compliant.

If You Don’t Have Retirement Funds to Roll Over

You can still open a Precious Metals IRA and fund it with cash contributions.

The limits are $7,500 for 2026 ($8,600 if you’re 50+). Income limits may affect deductibility.

It takes longer to build substantial holdings this way—but you’re in the market with full compliance from day one.

If You Have Personal Gold You’d Like to Convert

Consider this two-step approach:

- Sell your personal gold to a reputable dealer (completely separate from any IRA transaction)

- Fund your IRA through rollover or contribution, then purchase qualifying metals

You end up with the same end result—gold in your IRA—but through compliant channels.

The methods for silver acquisition follow the same framework if you want to diversify.

Frequently Asked Questions

Can I sell my gold to my own IRA?

No. Selling gold you personally own to your IRA is a prohibited transaction under IRC Section 4975. The IRS considers this self-dealing—even if the sale happens at fair market value. The penalty? Your entire IRA could be disqualified and treated as a taxable distribution.

What happens if I accidentally put my own gold in an IRA depository?

You’ve triggered a prohibited transaction. The IRS will treat your entire IRA as distributed on January 1st of that year. You’ll owe income taxes on the full account value—plus a 10% early withdrawal penalty if you’re under 59½. If this happens, talk to a tax professional immediately.

Are there any exceptions for American Gold Eagles I already own?

No. While American Gold Eagles are IRS-approved for IRA ownership, that only applies when the IRA purchases them from an authorized dealer. The exception doesn’t let you contribute Eagles you already own. The prohibited transaction rules apply regardless of the metal’s IRA eligibility.

Why does the IRS require a third-party dealer for gold purchases?

The third-party requirement prevents self-dealing. If you could sell personal assets to your own IRA, you could shelter appreciated property from taxes—exactly what Congress wanted to prevent. The dealer-to-depository structure keeps you out of the transaction chain.

Can I store IRA gold in my personal safe?

Absolutely not. IRS rules require precious metals in an IRA to be held by an approved trustee or depository. Home storage—even in a sophisticated safe—will disqualify your IRA. The 2021 McNulty case confirmed that home storage schemes result in taxable distributions.

How do I fund a Gold IRA if I don’t have a 401(k) to roll over?

You can fund a Precious Metals IRA through annual cash contributions. The 2026 limit is $7,500 ($8,600 if you’re 50+). You can also transfer from an existing traditional or Roth IRA. If you have retirement funds from a former employer’s plan, those typically qualify for rollover too.

Is it better to hold gold personally or in an IRA?

Both approaches have merit—and many people do both. Personal gold gives you immediate access and privacy with no custody fees. IRA gold gives you tax-advantaged growth but comes with storage costs and distribution rules. It depends on your goals for clarity and control over your retirement.

What’s the difference between a Gold IRA rollover and transfer?

A rollover typically moves funds from a 401(k) or employer plan to an IRA. A transfer moves funds between two IRAs. Both can be done as “direct” transactions—custodian-to-custodian—where funds never touch your hands. Direct transfers avoid the 60-day deadline and withholding issues that come with indirect rollovers.

Conclusion

The IRS prohibition on transferring personal gold to an IRA isn’t arbitrary. It’s designed to prevent tax abuse—and the penalties for violating it are severe.

But here’s what matters: getting physical gold into a tax-advantaged retirement account is completely achievable. You just need to use the right channels.

Open a self-directed IRA. Fund it with a rollover or contribution. Let the IRA purchase qualifying metals from an authorized dealer. Store them at an approved depository.

That’s the path to peace of mind. That’s how you protect your retirement while staying on the right side of the tax code.

For anyone with personal gold—you have options. Sell it separately if that makes sense. Keep it as a separate holding. Or both. Your IRA can still hold physical gold. It just needs to be acquired through compliant channels.

Ready to explore your options?

If you’re thinking “this all makes sense, but I don’t have time to figure it out on my own,” you’re not alone. Most customers we work with felt the same way before they realized how straightforward the process can be with the right guidance.

That’s why we offer a complimentary consultation to walk you through your options—including our No Fee Precious Metals IRA, which covers custodial fees for the lifetime of the account on qualified purchases.

We’ll show you exactly:

- How the No Fee IRA works and whether you qualify

- The difference between U.S.-minted coins and foreign alternatives

- What to expect from the purchasing and delivery process

- How to roll over or transfer existing retirement funds

- What ongoing support looks like after your purchase

Learn About the No Fee IRA — no obligation, just actionable insights you can use whether you work with us or not.

Precious metals may appreciate, depreciate, or remain unchanged in value. Resale values depend on market conditions at the time of sale. Brighton Enterprises does not provide financial, legal, or tax advice. Consult your CPA or tax professional for guidance specific to your situation.